Key Insights

Japan's coal industry is projected to experience sustained growth, with an estimated market size of USD 298.5 million in the base year 2024 and a Compound Annual Growth Rate (CAGR) of 2% through 2033. This expansion is driven by the ongoing, albeit evolving, demand for coal in power generation, particularly thermal power plants. Despite global trends towards renewable energy, Japan's existing energy infrastructure and security imperatives ensure a continued, significant role for coal in its energy mix. Additionally, the coking feedstock market, vital for steel manufacturing, further bolsters demand, underscoring the persistent importance of heavy industries. While environmental regulations and the long-term transition to cleaner sources are noted, the short-to-medium term forecast for coal remains strong, supported by these fundamental industrial and energy requirements.

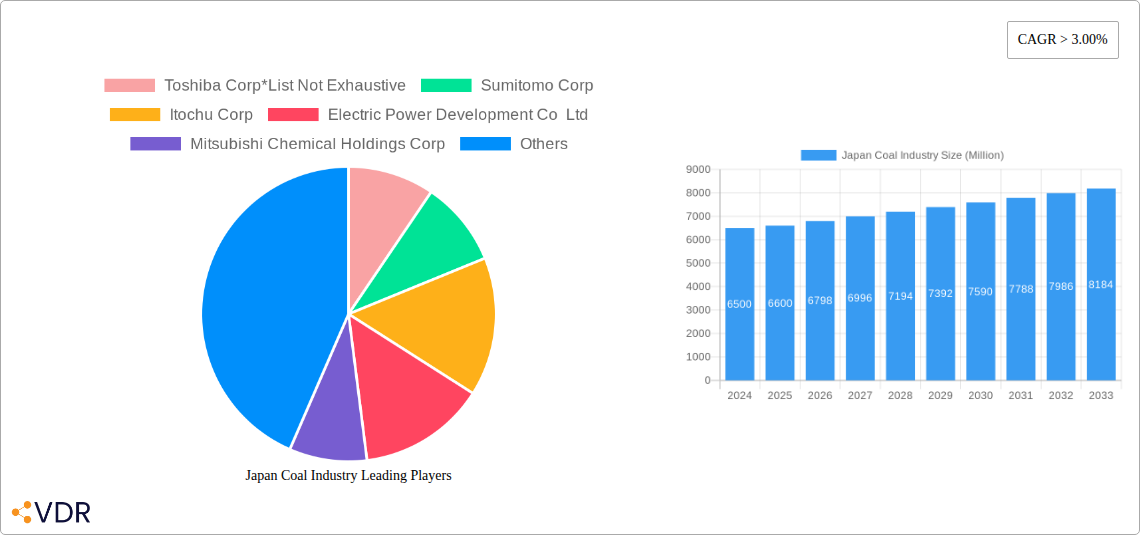

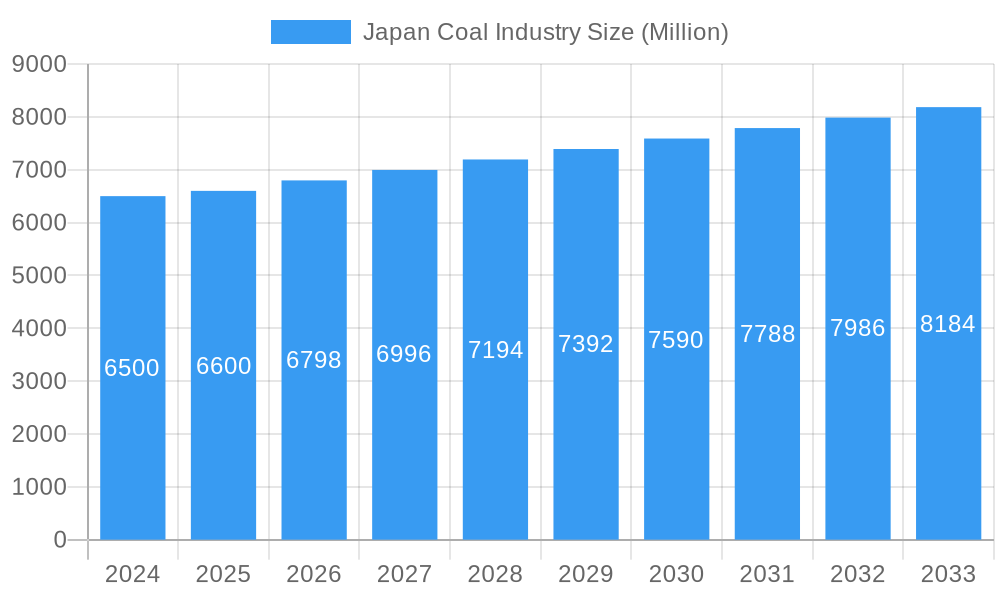

Japan Coal Industry Market Size (In Million)

The market faces considerable challenges, including evolving environmental policies and decarbonization pressures, which necessitate enhanced coal utilization efficiency and accelerated adoption of alternative energy solutions. These factors, alongside global coal price volatility and import logistics, require strategic agility from industry leaders. Major players like Toshiba Corp, Sumitomo Corp, and Mitsubishi Heavy Industries Ltd are actively managing these dynamics through investments in cleaner coal technologies, diversification into renewables, and supply chain optimization. Niche growth opportunities exist within the "Others" segment, covering various industrial applications beyond power and coking, though their market impact is secondary to the primary segments. This analysis focuses exclusively on Japan, highlighting its unique domestic drivers and constraints within the coal sector.

Japan Coal Industry Company Market Share

Japan Coal Industry: Comprehensive Market Analysis & Future Outlook (2019-2033)

This in-depth report provides a granular analysis of the Japan Coal Industry, encompassing market dynamics, growth trends, regional dominance, product landscape, key drivers, emerging opportunities, and a detailed outlook for the period 2019–2033, with a base year of 2025 and forecast period of 2025–2033. Leverage invaluable insights on parent and child markets, crucial for strategic decision-making in the evolving energy sector. All monetary values are presented in Million units.

Japan Coal Industry Market Dynamics & Structure

The Japan Coal Industry is characterized by a moderate level of market concentration, with a few dominant players such as Toshiba Corp, Sumitomo Corp, and Itochu Corp holding significant sway. Technological innovation remains a critical driver, particularly in the realm of cleaner coal combustion and carbon capture technologies, aimed at mitigating environmental concerns associated with traditional coal usage. The regulatory framework, while historically supportive of coal-fired power generation, is increasingly influenced by international climate agreements and domestic environmental targets, creating a dynamic interplay between energy security and sustainability. Competitive product substitutes, primarily natural gas and renewable energy sources like solar and wind power, exert increasing pressure on coal's market share. End-user demographics are heavily skewed towards the Power Station (Thermal Coal) segment, which constitutes the largest consumer of coal for electricity generation. The Coking Feedstock (Coking Coal) segment, vital for the steel industry, also represents a significant, albeit smaller, demand driver. Mergers and acquisitions (M&A) trends are influenced by the drive for operational efficiency and the pursuit of sustainable energy solutions. For instance, recent years have seen strategic alliances aimed at upgrading existing coal-fired power plants and exploring more environmentally friendly coal utilization methods. While innovation barriers exist, primarily due to the capital-intensive nature of developing and deploying advanced coal technologies, the perceived need for stable baseload power ensures continued investment in this sector. The market share of thermal coal in power generation remains substantial, estimated at XX% in the base year 2025, while coking coal holds an estimated XX% share. M&A deal volumes in the past five years have focused on infrastructure upgrades and diversification into cleaner energy solutions.

- Market Concentration: Moderate, with key players dominating specific segments.

- Technological Innovation: Focus on clean coal technologies, carbon capture, and emission reduction.

- Regulatory Framework: Evolving, balancing energy security with environmental commitments.

- Competitive Product Substitutes: Natural gas, renewables (solar, wind).

- End-User Demographics: Primarily Power Station (Thermal Coal), followed by Coking Feedstock (Coking Coal).

- M&A Trends: Driven by efficiency, sustainability, and diversification.

Japan Coal Industry Growth Trends & Insights

The Japan Coal Industry, though facing global decarbonization pressures, exhibits a complex growth trajectory driven by its indispensable role in baseload power generation and industrial processes. The market size evolution is projected to see a nuanced pattern, with a steady demand from power stations for thermal coal, particularly for older, less efficient plants that are being modernized rather than retired prematurely. This is supported by increased government support for coal-fired power plants, which has been a significant policy intervention to ensure energy security amidst fluctuating global energy prices and supply chain vulnerabilities. The adoption rates of clean coal technologies are on an upward trajectory, spurred by regulatory incentives and the industry’s commitment to reduce its environmental footprint. While new coal power plant constructions are limited, the retrofitting and upgrading of existing facilities with advanced emission control systems and more efficient combustion technologies are key growth areas. Technological disruptions are primarily focused on enhancing the efficiency of thermal coal utilization and exploring pathways for co-firing with biomass or hydrogen, thereby reducing the carbon intensity of coal-fired power. Consumer behavior shifts, as reflected in public and corporate demand for sustainable energy, are influencing the pace of coal adoption. However, the imperative for reliable and affordable energy continues to make coal a crucial component of Japan's energy mix for the foreseeable future. The estimated Compound Annual Growth Rate (CAGR) for the overall Japan Coal Industry from 2025 to 2033 is projected at XX%. Market penetration of cleaner coal technologies is expected to increase from XX% in the base year 2025 to XX% by 2033. The demand for thermal coal for power generation is anticipated to remain robust, with an estimated market size of XX Million units in 2025, growing to XX Million units by 2033. The coking coal segment, crucial for the domestic steel industry, is forecast to experience a CAGR of XX% during the same period, driven by infrastructure development and manufacturing demand. Investments in research and development for advanced coal utilization are a key indicator of the industry's commitment to long-term viability. The report will delve into specific metrics such as energy security indices, carbon emission reduction targets achieved through technological adoption, and the economic impact of coal mining and processing activities.

Dominant Regions, Countries, or Segments in Japan Coal Industry

The Power Station (Thermal Coal) segment stands as the undisputed dominant force within the Japan Coal Industry, driving the majority of market demand and growth. This dominance is deeply rooted in Japan's energy security strategy and its historical reliance on coal for stable and affordable baseload electricity generation. Despite global decarbonization efforts, thermal coal continues to be a critical component of the nation's energy mix, especially as the country navigates energy transition challenges and the volatility of international energy markets. The increased government support for coal-fired power plants, particularly in the form of subsidies for operational costs and incentives for plant upgrades, further solidifies this segment's importance.

Key Drivers for the Dominance of Power Station (Thermal Coal):

- Energy Security: Coal provides a reliable and domestically controllable energy source, crucial for Japan's import-dependent energy landscape.

- Baseload Power: Coal-fired power plants are essential for providing consistent, 24/7 electricity, complementing intermittent renewable sources.

- Economic Viability: Despite rising carbon costs, coal remains a relatively cost-effective fuel for electricity generation, especially for existing infrastructure.

- Government Policy: Strategic emphasis on maintaining coal as a transitional fuel and ensuring energy independence.

- Infrastructure: Extensive existing network of coal-fired power plants that require continuous fuel supply.

The estimated market share of the Power Station (Thermal Coal) segment in 2025 is a significant XX% of the total Japan Coal Industry. This segment is projected to experience a steady growth rate, with an estimated CAGR of XX% from 2025 to 2033. The market size for thermal coal in this segment is anticipated to reach XX Million units in 2025 and grow to XX Million units by 2033.

While the Coking Feedstock (Coking Coal) segment, essential for the steel industry, represents a crucial child market, its demand is intrinsically linked to the health of Japan's manufacturing and construction sectors. Its market share, estimated at XX% in 2025, is substantial but considerably smaller than that of thermal coal. Growth potential in this segment is contingent on domestic industrial output and global demand for steel products.

The Others segment, encompassing various industrial applications, holds a smaller market share, estimated at XX% in 2025. This segment's growth is more diversified and dependent on specific industrial trends and technological advancements in areas like chemical production.

Overall, the Power Station (Thermal Coal) segment's dominance is a result of a confluence of economic, strategic, and policy factors, making it the primary engine for the Japan Coal Industry's performance and outlook.

Japan Coal Industry Product Landscape

The Japan Coal Industry's product landscape is primarily defined by its two core categories: thermal coal and coking coal. Thermal coal, characterized by its lower calorific value and higher ash content, is predominantly utilized in power stations for electricity generation. Innovations in this area focus on improving combustion efficiency and reducing emissions through advanced boiler technologies and flue-gas desulfurization systems. Coking coal, on the other hand, boasts higher carbon content and lower volatile matter, making it indispensable as a feedstock for the metallurgical industry, particularly in the production of steel. Product advancements in coking coal revolve around ensuring consistent quality and optimizing its use in blast furnaces to enhance steel production efficiency. The performance metrics for these products are rigorously monitored, with emphasis on calorific value, ash content, sulfur content, and volatile matter to meet the stringent requirements of their respective end-users. Unique selling propositions lie in the reliability of supply, adherence to strict quality standards, and the development of specialized blends for specific industrial applications. Technological advancements are also exploring the potential for pulverized coal injection (PCI) and integrated gasification combined cycle (IGCC) technologies for thermal coal, aiming to improve environmental performance.

Key Drivers, Barriers & Challenges in Japan Coal Industry

The Japan Coal Industry is propelled by several key drivers, most notably the persistent demand for reliable and affordable baseload power to ensure national energy security. Increased government support for coal-fired power plants plays a pivotal role, recognizing coal's contribution to energy independence amidst global market volatility. Technological innovation, particularly in clean coal technologies, also acts as a significant driver, enabling the industry to meet stricter environmental regulations and reduce its carbon footprint. Strategic partnerships with international coal suppliers are crucial for securing consistent and competitively priced raw material.

However, the industry faces substantial barriers and challenges. The most significant is the growing global and domestic pressure to decarbonize and transition towards renewable energy sources, leading to regulatory uncertainty and reputational challenges. Supply chain disruptions, exacerbated by geopolitical events and logistics complexities, pose a constant threat to stable fuel procurement. Furthermore, the high capital expenditure required for implementing advanced emission control technologies and the ongoing operational costs present financial hurdles. Competitive pressures from natural gas and renewables, which are increasingly cost-competitive and perceived as environmentally superior, also impact coal's market share.

Emerging Opportunities in Japan Coal Industry

Emerging opportunities within the Japan Coal Industry lie in the strategic development and deployment of advanced clean coal technologies. Significant potential exists in the investment in and scaling of carbon capture, utilization, and storage (CCUS) technologies, which can dramatically reduce the greenhouse gas emissions from coal-fired power plants. Furthermore, the exploration of co-firing coal with sustainable biomass or hydrogen offers a pathway to reduce the carbon intensity of existing infrastructure, creating a niche market for blended fuels. Partnerships with international entities for the development of innovative coal gasification technologies, producing syngas for various industrial applications beyond power generation, also represent a promising avenue. The increasing global demand for steel, albeit with a focus on sustainable production, will continue to underpin the demand for high-quality coking coal, creating opportunities for efficient and environmentally responsible supply.

Growth Accelerators in the Japan Coal Industry Industry

The long-term growth of the Japan Coal Industry is significantly accelerated by strategic governmental policies that prioritize energy security and the continued utilization of coal as a transitional fuel. Increased government support for coal-fired power plants, including modernization initiatives and operational subsidies, provides a stable demand base. Furthermore, substantial investment in clean coal technologies, such as CCUS and advanced combustion systems, is a critical accelerator, enabling the industry to mitigate its environmental impact and comply with evolving regulations. The formation of strategic partnerships with international coal suppliers ensures a reliable and diversified supply chain, reducing the risk of price volatility and shortages. These accelerators are crucial for maintaining coal's relevance in Japan's energy mix while pursuing a more sustainable future.

Key Players Shaping the Japan Coal Industry Market

The Japan Coal Industry market is shaped by a consortium of influential companies, including:

- Toshiba Corp

- Sumitomo Corp

- Itochu Corp

- Electric Power Development Co Ltd

- Mitsubishi Chemical Holdings Corp

- Marubeni Corp

- Chiyoda Corp

- JFE Engineering Corporation

- Mitsubishi Heavy Industries Ltd

- J-POWER (Electric Power Development Co., Ltd.)

Notable Milestones in Japan Coal Industry Sector

- 2019: Increased government support for coal-fired power plants with the announcement of updated energy policies prioritizing energy security.

- 2020: Significant investment in clean coal technologies, with major power companies announcing R&D initiatives for carbon capture solutions.

- 2021: Establishment of new partnerships with international coal suppliers to secure long-term, stable supply contracts amidst global market fluctuations.

- 2022: Launch of pilot projects for advanced coal combustion technologies aimed at improving efficiency and reducing emissions at key thermal power stations.

- 2023: Further expansion of collaborative efforts between Japanese corporations and international technology providers for the development of next-generation coal utilization systems.

- 2024: Increased focus on integrating digitalization and AI for optimizing coal supply chain logistics and improving operational efficiency of coal-fired power plants.

In-Depth Japan Coal Industry Market Outlook

The future outlook for the Japan Coal Industry is characterized by a strategic recalibration rather than outright decline. The sustained demand for baseload power, coupled with government emphasis on energy security, will ensure a continued, albeit evolving, role for coal. Growth accelerators, particularly substantial investment in clean coal technologies and strategic international partnerships, are critical for navigating the decarbonization landscape. The market's ability to adapt through CCUS adoption and co-firing initiatives will be paramount in maintaining its relevance. Consequently, the industry is poised for a period of transformation, focusing on efficiency, emission reduction, and diversification to meet future energy demands sustainably, with an estimated market potential driven by these innovative strategies.

Japan Coal Industry Segmentation

-

1. End-User

- 1.1. Power Station (Thermal Coal)

- 1.2. Coking Feedstock (Coking Coal)

- 1.3. Others

Japan Coal Industry Segmentation By Geography

- 1. Japan

Japan Coal Industry Regional Market Share

Geographic Coverage of Japan Coal Industry

Japan Coal Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by End-User

- 5.1.1. Power Station (Thermal Coal)

- 5.1.2. Coking Feedstock (Coking Coal)

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Japan

- 5.1. Market Analysis, Insights and Forecast - by End-User

- 6. Japan Coal Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by End-User

- 6.1.1. Power Station (Thermal Coal)

- 6.1.2. Coking Feedstock (Coking Coal)

- 6.1.3. Others

- 6.1. Market Analysis, Insights and Forecast - by End-User

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Toshiba Corp*List Not Exhaustive

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Sumitomo Corp

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Itochu Corp

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Electric Power Development Co Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Mitsubishi Chemical Holdings Corp

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Marubeni Corp

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Chiyoda Corp

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 JFE Engineering Corporation

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Mitsubishi Heavy Industries Ltd

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 J-POWER (Electric Power Development Co. Ltd.)

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Toshiba Corp*List Not Exhaustive

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Japan Coal Industry Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: Japan Coal Industry Share (%) by Company 2025

List of Tables

- Table 1: Japan Coal Industry Revenue million Forecast, by End-User 2020 & 2033

- Table 2: Japan Coal Industry Volume K Tons Forecast, by End-User 2020 & 2033

- Table 3: Japan Coal Industry Revenue million Forecast, by Region 2020 & 2033

- Table 4: Japan Coal Industry Volume K Tons Forecast, by Region 2020 & 2033

- Table 5: Japan Coal Industry Revenue million Forecast, by End-User 2020 & 2033

- Table 6: Japan Coal Industry Volume K Tons Forecast, by End-User 2020 & 2033

- Table 7: Japan Coal Industry Revenue million Forecast, by Country 2020 & 2033

- Table 8: Japan Coal Industry Volume K Tons Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Japan Coal Industry?

The projected CAGR is approximately 2%.

2. Which companies are prominent players in the Japan Coal Industry?

Key companies in the market include Toshiba Corp*List Not Exhaustive, Sumitomo Corp, Itochu Corp, Electric Power Development Co Ltd, Mitsubishi Chemical Holdings Corp, Marubeni Corp, Chiyoda Corp, JFE Engineering Corporation, Mitsubishi Heavy Industries Ltd, J-POWER (Electric Power Development Co., Ltd.).

3. What are the main segments of the Japan Coal Industry?

The market segments include End-User.

4. Can you provide details about the market size?

The market size is estimated to be USD 298.5 million as of 2022.

5. What are some drivers contributing to market growth?

4.; Supportive Government Policies.

6. What are the notable trends driving market growth?

Power Stations Segment to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Rising Adoption Of Alternate Clean Power Sources.

8. Can you provide examples of recent developments in the market?

Increased government support for coal-fired power plants

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Japan Coal Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Japan Coal Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Japan Coal Industry?

To stay informed about further developments, trends, and reports in the Japan Coal Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence