Key Insights

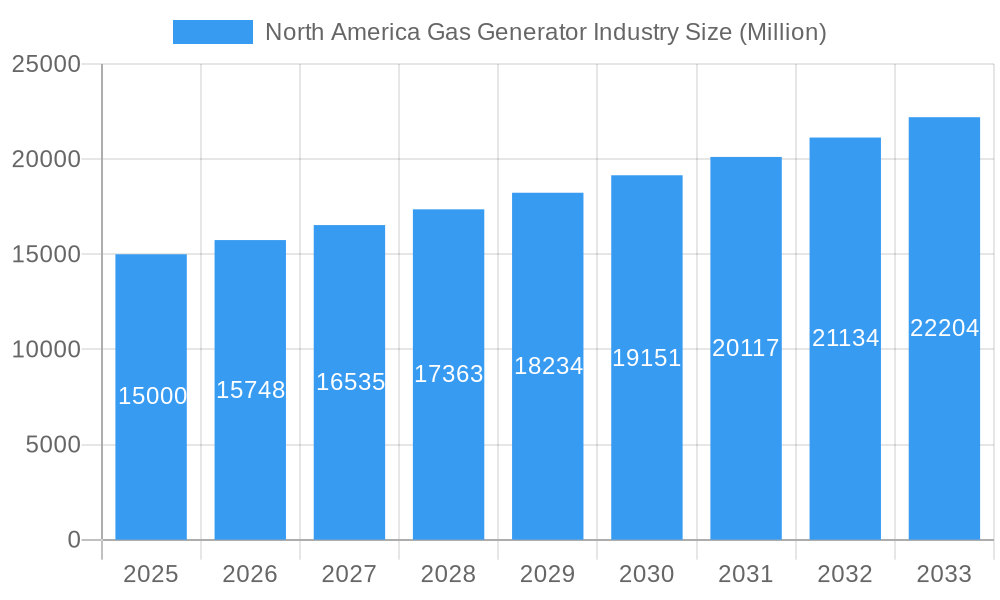

The North America gas generator market is projected for substantial growth, fueled by escalating demand for dependable and sustainable power across diverse sectors. The market is estimated at $7,585 million in the base year 2025, with a Compound Annual Growth Rate (CAGR) of 8.8% anticipated from 2025 to 2033. Key growth drivers include the increasing need for backup power solutions in residential and commercial areas, driven by an aging power grid and a rise in extreme weather events. Industrial sector expansion, coupled with a focus on fuel efficiency and reduced emissions compared to traditional diesel generators, also significantly contributes to market expansion. The shift towards natural gas as a cleaner and more accessible fuel source, particularly in regions with established distribution networks, further propels market growth.

North America Gas Generator Industry Market Size (In Billion)

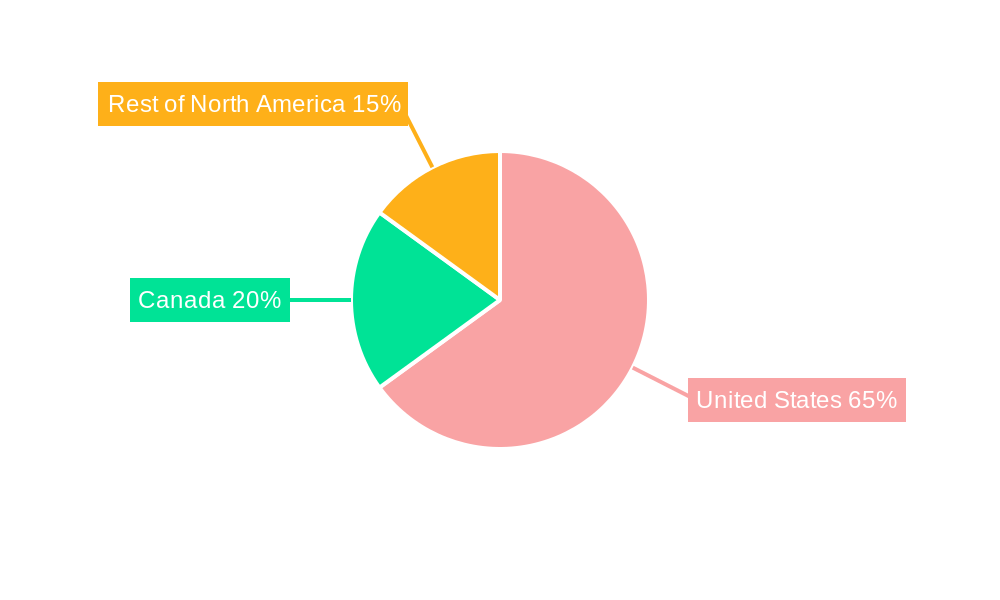

The market is segmented by capacity, with the 75-375 kVA segment expected to lead, offering a balance of power and cost-effectiveness for commercial and light industrial applications. The Above 375 kVA segment is poised for robust growth, driven by the high power demands of large industrial facilities and data centers. Analysis of end-users indicates the industrial sector will remain the largest segment, followed by the commercial sector, as businesses prioritize operational continuity and cost savings. Residential adoption is also anticipated to rise, driven by a desire for energy independence and grid resilience. Geographically, the United States is expected to dominate the market due to its extensive industrial base and natural gas infrastructure, with Canada and the Rest of North America also making significant contributions.

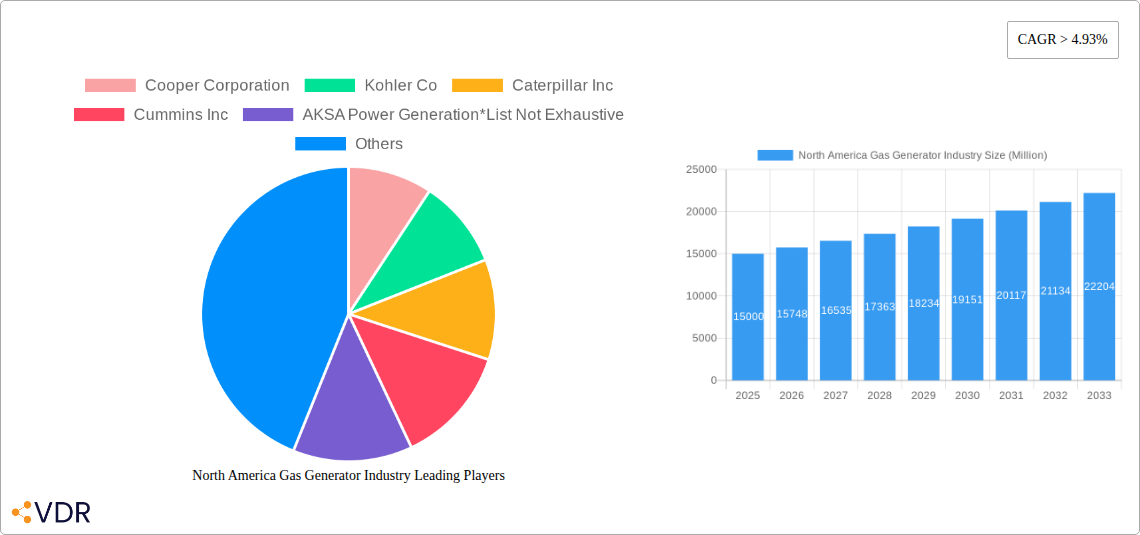

North America Gas Generator Industry Company Market Share

This comprehensive report offers a critical analysis of the North America gas generator industry, detailing market dynamics, growth trends, and future opportunities. Optimized with keywords such as "North America gas generator market," "natural gas generator," "backup power solutions," and "industrial generators," this report is designed for industry professionals, investors, and decision-makers. The analysis covers the historical period (2019–2024), base year (2025), and forecast period (2025–2033), providing essential insights into market size evolution, segmentation, regional trends, technological advancements, and competitive landscapes.

The report examines parent and child market segments, offering a detailed understanding of market forces across various capacities (Less than 75 kVA, 75-375 kVA, Above 375 kVA) and end-user applications (Industrial, Commercial, Residential). We provide quantitative data on market trends and strategic developments, serving as a definitive guide to navigating the North American gas generator market.

North America Gas Generator Industry Market Dynamics & Structure

The North America gas generator industry exhibits a moderately concentrated market structure, with key players like Caterpillar Inc., Cummins Inc., and Generac Holdings Inc. holding significant market shares. Technological innovation, particularly in efficiency, emission reduction, and smart grid integration, acts as a primary driver of market growth. The increasing demand for reliable and cost-effective backup power solutions, coupled with stringent environmental regulations, fuels the adoption of natural gas generators over diesel alternatives. Competitive product substitutes, such as diesel generators and renewable energy sources, present a challenge, but the superior fuel efficiency and lower emissions of gas generators continue to bolster their market position. End-user demographics are shifting, with growing demand from the commercial and industrial sectors for uninterrupted power supply, while the residential segment is increasingly adopting smaller-capacity units for home backup. Mergers and acquisitions (M&A) activity is moderate, indicating strategic consolidation and expansion efforts by leading companies to enhance their product portfolios and market reach. Innovation barriers include the high initial cost of advanced technologies and the need for robust infrastructure for natural gas supply. For instance, an estimated xx% of market share is held by the top five players, with M&A deal volumes averaging around xx per year over the historical period.

North America Gas Generator Industry Growth Trends & Insights

The North America gas generator industry is poised for robust growth, driven by an escalating need for reliable and sustainable power solutions across diverse sectors. The market size is projected to witness a Compound Annual Growth Rate (CAGR) of approximately xx% from 2025 to 2033, expanding from an estimated $xx billion in 2025 to $xx billion by 2033. This growth is underpinned by increasing investments in infrastructure development, the growing prevalence of data centers and critical facilities demanding uninterrupted power, and the ongoing transition towards cleaner energy sources. Adoption rates are accelerating, particularly in the industrial and commercial segments, where operational continuity is paramount. Technological disruptions, including advancements in hybrid power systems and the integration of smart grid technologies, are enhancing the efficiency and adaptability of gas generators. Consumer behavior is shifting towards seeking more sustainable and cost-effective power backup options, favoring natural gas generators due to their lower operational costs and reduced environmental impact compared to traditional diesel alternatives. Market penetration is expected to deepen, with an estimated xx% of commercial establishments and xx% of industrial facilities in key regions utilizing gas generators for backup and prime power applications by 2033. The increasing affordability and accessibility of natural gas also contribute significantly to market expansion.

Dominant Regions, Countries, or Segments in North America Gas Generator Industry

The United States stands as the dominant region within the North America gas generator industry, accounting for an estimated xx% of the total market share in 2025. This dominance is driven by its vast industrial and commercial base, significant investments in infrastructure, and a strong demand for reliable backup power solutions across various end-user segments. The Industrial end-user segment, particularly in sectors such as manufacturing, oil and gas, and data centers, is the leading driver of market growth, contributing approximately xx% of the total demand in 2025. This is due to the critical nature of operations in these sectors, where power outages can lead to substantial financial losses and operational disruptions. Within the capacity segments, Above 375 kVA generators are witnessing the highest demand, catering to the substantial power requirements of industrial and large commercial facilities. The growth in this segment is fueled by large-scale construction projects, expanding manufacturing capabilities, and the increasing need for robust power infrastructure. Economic policies promoting energy independence and grid resilience further bolster the demand for gas generators in the US. Canada, while a significant market, follows with an estimated xx% market share, driven by its own industrial needs and a growing residential demand for backup power. The "Rest of North America" segment, encompassing Mexico and other smaller markets, represents the remaining xx% and offers burgeoning growth potential due to ongoing industrialization and infrastructure development. Key drivers in the US include federal and state incentives for cleaner energy technologies, the continuous expansion of the energy sector, and the need to supplement an aging power grid. Market share within the US Industrial segment is estimated at xx million units in 2025, with a projected CAGR of xx% for the forecast period.

North America Gas Generator Industry Product Landscape

The North America gas generator product landscape is characterized by continuous innovation focused on enhanced efficiency, reduced emissions, and improved reliability. Key product innovations include advanced engine designs that optimize fuel consumption and minimize greenhouse gas emissions, meeting increasingly stringent environmental regulations. Applications range from prime power generation in remote locations and off-grid sites to essential backup power for critical infrastructure like hospitals, data centers, and telecommunication facilities. Performance metrics are steadily improving, with new generator sets offering faster load acceptance, superior transient response, and extended operational lifecycles. Unique selling propositions often revolve around lower total cost of ownership, driven by the cost-effectiveness of natural gas as a fuel, and compliance with EPA standards, making them attractive for environmentally conscious consumers and businesses. Technological advancements are also integrating smart features for remote monitoring, diagnostics, and predictive maintenance, enhancing operational efficiency and reducing downtime.

Key Drivers, Barriers & Challenges in North America Gas Generator Industry

Key Drivers:

- Increasing demand for reliable backup power: Essential for critical infrastructure, data centers, and industrial operations facing grid instability and power outages.

- Environmental regulations and sustainability initiatives: Favoring cleaner-burning natural gas over diesel, driving adoption for reduced emissions.

- Cost-effectiveness of natural gas: Lower fuel prices compared to diesel offer significant operational savings.

- Technological advancements: Improved efficiency, lower emissions, and smart grid integration enhancing performance and appeal.

- Government incentives and policies: Support for cleaner energy adoption and grid modernization.

Barriers & Challenges:

- High initial capital investment: Advanced gas generator sets can have a higher upfront cost compared to basic diesel units.

- Natural gas infrastructure availability: Limited access to natural gas pipelines in some remote or developing areas.

- Price volatility of natural gas: Fluctuations in natural gas prices can impact operational cost predictability.

- Competition from alternative energy sources: Growing adoption of solar, wind, and battery storage solutions.

- Skilled labor shortage: Demand for trained technicians for installation, operation, and maintenance.

The estimated impact of these challenges on market growth could be a reduction in the CAGR by approximately xx% if not addressed. Supply chain disruptions, as seen in recent years, also pose a significant challenge, potentially delaying project timelines and increasing costs.

Emerging Opportunities in North America Gas Generator Industry

Emerging opportunities in the North America gas generator industry lie in the expanding market for distributed energy resources (DERs) and microgrids, driven by the need for enhanced grid resilience and energy independence. The increasing adoption of electric vehicles (EVs) also presents a significant opportunity, as charging infrastructure requires substantial and reliable power, often necessitating backup solutions. Furthermore, the growing demand for modular and containerized generator sets for rapid deployment in disaster-prone areas or for temporary power needs in construction projects offers a niche growth area. The development of advanced biogas and renewable natural gas (RNG) integration capabilities within gas generators represents a significant untapped market, aligning with the global push towards a circular economy and carbon neutrality. Innovative financing models and power purchase agreements can also unlock new customer segments, particularly for small and medium-sized enterprises.

Growth Accelerators in the North America Gas Generator Industry Industry

Several catalysts are accelerating the long-term growth of the North America gas generator industry. Technological breakthroughs in fuel cell technology and combined heat and power (CHP) systems are creating new, highly efficient applications. Strategic partnerships between generator manufacturers and energy service companies (ESCOs) are expanding market reach and offering integrated power solutions. Market expansion strategies, including entering new geographical territories and developing specialized product lines for emerging industries like vertical farming and advanced manufacturing, are also driving growth. The increasing focus on grid modernization and the decentralization of power generation are creating a sustained demand for flexible and reliable power sources, with gas generators playing a pivotal role in this transition.

Key Players Shaping the North America Gas Generator Industry Market

- Cooper Corporation

- Kohler Co

- Caterpillar Inc

- Cummins Inc

- AKSA Power Generation

- MTU America Inc

- General Electric Company

- Honda Power Equipment Mfg Inc

- Generac Holdings Inc

Notable Milestones in North America Gas Generator Industry Sector

- Jan 2022: Caterpillar Inc. unveiled the Cat G3516 Fast Reaction generator set, adding a 1.5 MW power node to its natural-gas power solutions, enhancing load acceptance and transient response for mission-critical applications.

- Dec 2021: HIPOWER SYSTEMS, HIMOINSA's new North American production hub, began operations in Olathe, Kansas, featuring a 515,000-square-foot plant with advanced technology for the North American generator set market.

In-Depth North America Gas Generator Industry Market Outlook

The North America gas generator industry is on an upward trajectory, driven by a confluence of factors including energy security concerns, technological innovation, and a growing imperative for sustainable power solutions. Future market potential is significant, fueled by the ongoing digital transformation, which necessitates robust and uninterrupted power for data centers and telecommunication networks. Strategic opportunities abound in the integration of gas generators with renewable energy sources to create hybrid power systems, offering both reliability and reduced carbon footprints. The increasing demand for distributed generation and microgrids, especially in the face of climate change-induced extreme weather events, presents a substantial growth avenue. Manufacturers are expected to focus on developing even more efficient, intelligent, and emission-compliant generator sets to meet evolving market demands and regulatory landscapes, ensuring continued expansion and market leadership.

North America Gas Generator Industry Segmentation

-

1. Capacity

- 1.1. Less than 75 kVA

- 1.2. 75-375 kVA

- 1.3. Above 375 kVA

-

2. End User

- 2.1. Industrial

- 2.2. Commercial

- 2.3. Residential

-

3. Geography

- 3.1. United States

- 3.2. Canada

- 3.3. Rest of North America

North America Gas Generator Industry Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Rest of North America

North America Gas Generator Industry Regional Market Share

Geographic Coverage of North America Gas Generator Industry

North America Gas Generator Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Capacity

- 5.1.1. Less than 75 kVA

- 5.1.2. 75-375 kVA

- 5.1.3. Above 375 kVA

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Industrial

- 5.2.2. Commercial

- 5.2.3. Residential

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. United States

- 5.3.2. Canada

- 5.3.3. Rest of North America

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United States

- 5.4.2. Canada

- 5.4.3. Rest of North America

- 5.1. Market Analysis, Insights and Forecast - by Capacity

- 6. North America Gas Generator Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Capacity

- 6.1.1. Less than 75 kVA

- 6.1.2. 75-375 kVA

- 6.1.3. Above 375 kVA

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Industrial

- 6.2.2. Commercial

- 6.2.3. Residential

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. United States

- 6.3.2. Canada

- 6.3.3. Rest of North America

- 6.1. Market Analysis, Insights and Forecast - by Capacity

- 7. United States North America Gas Generator Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Capacity

- 7.1.1. Less than 75 kVA

- 7.1.2. 75-375 kVA

- 7.1.3. Above 375 kVA

- 7.2. Market Analysis, Insights and Forecast - by End User

- 7.2.1. Industrial

- 7.2.2. Commercial

- 7.2.3. Residential

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. United States

- 7.3.2. Canada

- 7.3.3. Rest of North America

- 7.1. Market Analysis, Insights and Forecast - by Capacity

- 8. Canada North America Gas Generator Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Capacity

- 8.1.1. Less than 75 kVA

- 8.1.2. 75-375 kVA

- 8.1.3. Above 375 kVA

- 8.2. Market Analysis, Insights and Forecast - by End User

- 8.2.1. Industrial

- 8.2.2. Commercial

- 8.2.3. Residential

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. United States

- 8.3.2. Canada

- 8.3.3. Rest of North America

- 8.1. Market Analysis, Insights and Forecast - by Capacity

- 9. Rest of North America North America Gas Generator Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Capacity

- 9.1.1. Less than 75 kVA

- 9.1.2. 75-375 kVA

- 9.1.3. Above 375 kVA

- 9.2. Market Analysis, Insights and Forecast - by End User

- 9.2.1. Industrial

- 9.2.2. Commercial

- 9.2.3. Residential

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. United States

- 9.3.2. Canada

- 9.3.3. Rest of North America

- 9.1. Market Analysis, Insights and Forecast - by Capacity

- 10. Competitive Analysis

- 10.1. Company Profiles

- 10.1.1 Cooper Corporation

- 10.1.1.1. Company Overview

- 10.1.1.2. Products

- 10.1.1.3. Company Financials

- 10.1.1.4. SWOT Analysis

- 10.1.2 Kohler Co

- 10.1.2.1. Company Overview

- 10.1.2.2. Products

- 10.1.2.3. Company Financials

- 10.1.2.4. SWOT Analysis

- 10.1.3 Caterpillar Inc

- 10.1.3.1. Company Overview

- 10.1.3.2. Products

- 10.1.3.3. Company Financials

- 10.1.3.4. SWOT Analysis

- 10.1.4 Cummins Inc

- 10.1.4.1. Company Overview

- 10.1.4.2. Products

- 10.1.4.3. Company Financials

- 10.1.4.4. SWOT Analysis

- 10.1.5 AKSA Power Generation*List Not Exhaustive

- 10.1.5.1. Company Overview

- 10.1.5.2. Products

- 10.1.5.3. Company Financials

- 10.1.5.4. SWOT Analysis

- 10.1.6 MTU America Inc

- 10.1.6.1. Company Overview

- 10.1.6.2. Products

- 10.1.6.3. Company Financials

- 10.1.6.4. SWOT Analysis

- 10.1.7 General Electric Company

- 10.1.7.1. Company Overview

- 10.1.7.2. Products

- 10.1.7.3. Company Financials

- 10.1.7.4. SWOT Analysis

- 10.1.8 Honda Power Equipment Mfg Inc

- 10.1.8.1. Company Overview

- 10.1.8.2. Products

- 10.1.8.3. Company Financials

- 10.1.8.4. SWOT Analysis

- 10.1.9 Generac Holdings Inc

- 10.1.9.1. Company Overview

- 10.1.9.2. Products

- 10.1.9.3. Company Financials

- 10.1.9.4. SWOT Analysis

- 10.1.1 Cooper Corporation

- 10.2. Market Entropy

- 10.2.1 Company's Key Areas Served

- 10.2.2 Recent Developments

- 10.3. Company Market Share Analysis 2025

- 10.3.1 Top 5 Companies Market Share Analysis

- 10.3.2 Top 3 Companies Market Share Analysis

- 10.4. List of Potential Customers

- 11. Research Methodology

List of Figures

- Figure 1: North America Gas Generator Industry Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: North America Gas Generator Industry Share (%) by Company 2025

List of Tables

- Table 1: North America Gas Generator Industry Revenue million Forecast, by Capacity 2020 & 2033

- Table 2: North America Gas Generator Industry Volume K Unit Forecast, by Capacity 2020 & 2033

- Table 3: North America Gas Generator Industry Revenue million Forecast, by End User 2020 & 2033

- Table 4: North America Gas Generator Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 5: North America Gas Generator Industry Revenue million Forecast, by Geography 2020 & 2033

- Table 6: North America Gas Generator Industry Volume K Unit Forecast, by Geography 2020 & 2033

- Table 7: North America Gas Generator Industry Revenue million Forecast, by Region 2020 & 2033

- Table 8: North America Gas Generator Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 9: North America Gas Generator Industry Revenue million Forecast, by Capacity 2020 & 2033

- Table 10: North America Gas Generator Industry Volume K Unit Forecast, by Capacity 2020 & 2033

- Table 11: North America Gas Generator Industry Revenue million Forecast, by End User 2020 & 2033

- Table 12: North America Gas Generator Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 13: North America Gas Generator Industry Revenue million Forecast, by Geography 2020 & 2033

- Table 14: North America Gas Generator Industry Volume K Unit Forecast, by Geography 2020 & 2033

- Table 15: North America Gas Generator Industry Revenue million Forecast, by Country 2020 & 2033

- Table 16: North America Gas Generator Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 17: North America Gas Generator Industry Revenue million Forecast, by Capacity 2020 & 2033

- Table 18: North America Gas Generator Industry Volume K Unit Forecast, by Capacity 2020 & 2033

- Table 19: North America Gas Generator Industry Revenue million Forecast, by End User 2020 & 2033

- Table 20: North America Gas Generator Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 21: North America Gas Generator Industry Revenue million Forecast, by Geography 2020 & 2033

- Table 22: North America Gas Generator Industry Volume K Unit Forecast, by Geography 2020 & 2033

- Table 23: North America Gas Generator Industry Revenue million Forecast, by Country 2020 & 2033

- Table 24: North America Gas Generator Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 25: North America Gas Generator Industry Revenue million Forecast, by Capacity 2020 & 2033

- Table 26: North America Gas Generator Industry Volume K Unit Forecast, by Capacity 2020 & 2033

- Table 27: North America Gas Generator Industry Revenue million Forecast, by End User 2020 & 2033

- Table 28: North America Gas Generator Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 29: North America Gas Generator Industry Revenue million Forecast, by Geography 2020 & 2033

- Table 30: North America Gas Generator Industry Volume K Unit Forecast, by Geography 2020 & 2033

- Table 31: North America Gas Generator Industry Revenue million Forecast, by Country 2020 & 2033

- Table 32: North America Gas Generator Industry Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Gas Generator Industry?

The projected CAGR is approximately 8.8%.

2. Which companies are prominent players in the North America Gas Generator Industry?

Key companies in the market include Cooper Corporation, Kohler Co, Caterpillar Inc, Cummins Inc, AKSA Power Generation*List Not Exhaustive, MTU America Inc, General Electric Company, Honda Power Equipment Mfg Inc, Generac Holdings Inc.

3. What are the main segments of the North America Gas Generator Industry?

The market segments include Capacity, End User, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 7585 million as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Supply and Consumption of Gas-based Systems in Various End-user Industry4.; Implementation of stricter emission regulations worldwide.

6. What are the notable trends driving market growth?

Below 75 kVA Capacity Gas Generator to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Growing Inclination towards Renewable Sources.

8. Can you provide examples of recent developments in the market?

Jan 2022: Caterpillar Inc. unveiled the Cat G3516 Fast Reaction generator set, which adds a 1.5 MW power node to its increasing array of natural-gas power solutions that deliver market-leading load acceptance, transient response, and EPA certification for mission-critical applications.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Gas Generator Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Gas Generator Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Gas Generator Industry?

To stay informed about further developments, trends, and reports in the North America Gas Generator Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence