Key Insights

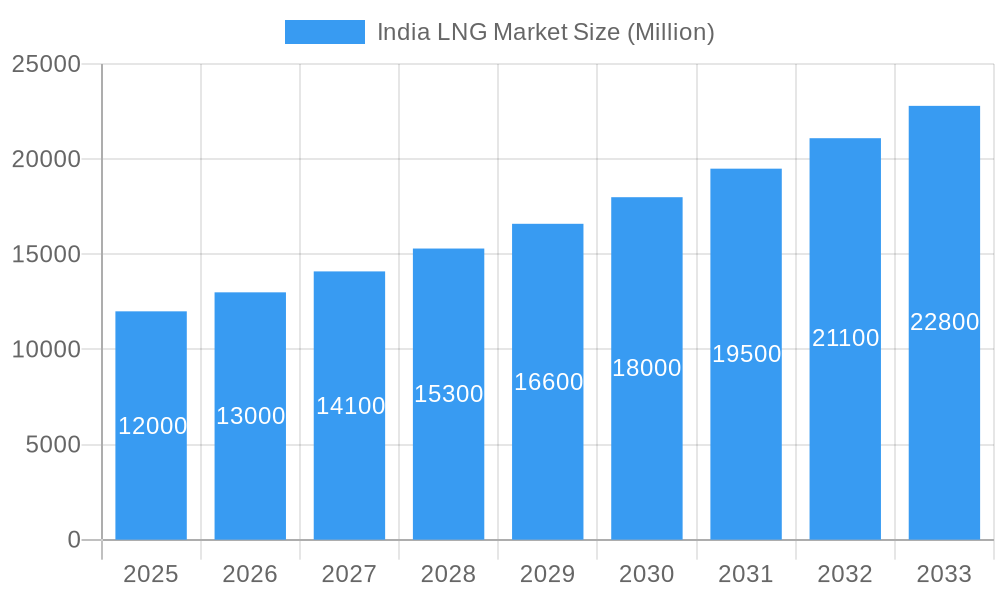

The Indian Liquefied Natural Gas (LNG) market is projected for substantial growth, driven by a Compound Annual Growth Rate (CAGR) exceeding 8%. The market is valued at approximately $15.98 billion in the base year 2024, with an anticipated expansion through 2033. This robust growth is propelled by India's escalating demand for cleaner energy alternatives to support its expanding industrial and residential sectors. Key growth catalysts include the government's strategic initiative to increase natural gas within the national energy mix, the imperative for dependable power generation, and the widening reach of city gas distribution networks to a larger consumer base. The petrochemical industry is also a significant contributor, utilizing LNG as a critical feedstock. Furthermore, the ongoing development and expansion of essential LNG infrastructure, including liquefaction plants, regasification terminals, and a dedicated LNG shipping fleet, are vital for facilitating this market surge and enhancing national import capabilities.

India LNG Market Market Size (In Billion)

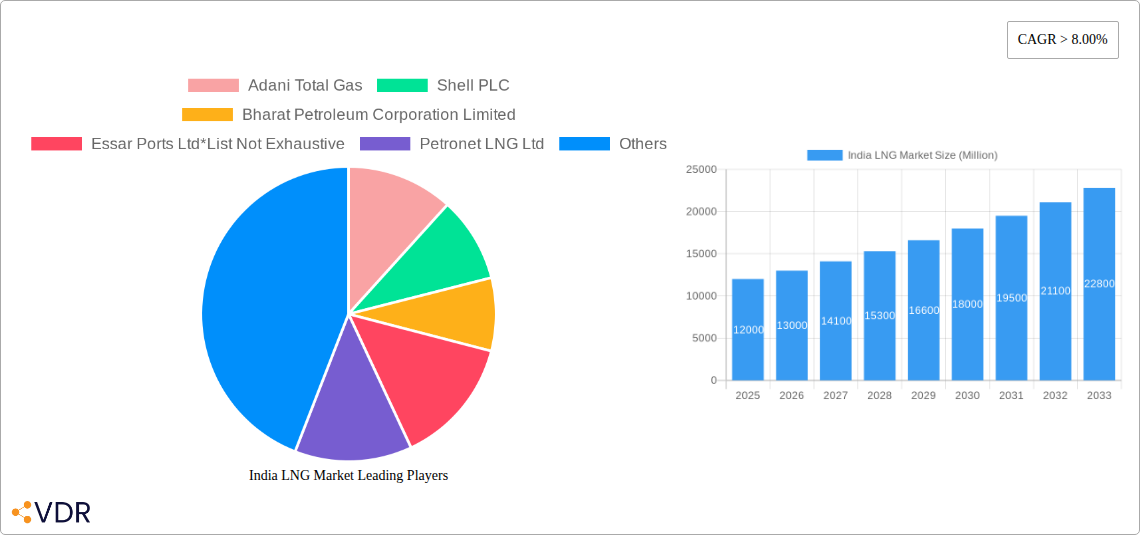

Emerging trends such as the deployment of Floating Storage and Regasification Units (FSRUs) are enhancing market flexibility and reducing upfront capital expenditure for coastal infrastructure. Increasingly stringent environmental regulations and a global emphasis on carbon emission reduction are favoring natural gas over conventional fossil fuels, positioning LNG as a key enabler of the energy transition. However, market expansion may be tempered by the volatility of global LNG prices, geopolitical influences on supply chains, and the substantial capital investment required for large-scale LNG infrastructure development. Despite these challenges, leading market participants, including Adani Total Gas, Shell PLC, Bharat Petroleum Corporation Limited, Petronet LNG Ltd, and GAIL Limited, are actively investing and expanding their operations, highlighting the significant strategic importance of the Indian LNG market globally. The period from 2019 to 2024 has established a strong foundational base, with 2024 serving as the base year for projecting accelerated market expansion towards 2033.

India LNG Market Company Market Share

India LNG Market Report: Unlocking Growth in a Critical Energy Sector (2019–2033)

Unlock the immense potential of India's burgeoning Liquefied Natural Gas (LNG) market with this comprehensive, SEO-optimized report. Designed for industry professionals, investors, and policymakers, this analysis delves into market dynamics, growth trends, dominant segments, and key players shaping the future of LNG in India. Leveraging high-traffic keywords such as "India LNG market," "LNG import terminal," "city gas distribution," "LNG infrastructure," and "petrochemicals," this report offers unparalleled insights into market size evolution, adoption rates, and technological disruptions. Covering the period from 2019 to 2033, with a base and estimated year of 2025, this report provides a forward-looking perspective crucial for strategic decision-making.

India LNG Market Market Dynamics & Structure

The India LNG market is characterized by a dynamic interplay of factors driving its rapid expansion. Market concentration is gradually shifting with the entry of new players and expansion of existing ones, creating a competitive yet collaborative environment. Technological innovation is a significant driver, with advancements in regasification technologies, floating LNG terminals, and LNG bunkering solutions enhancing efficiency and accessibility. Regulatory frameworks, while evolving, are increasingly supportive of LNG adoption, driven by the government's push for a gas-based economy and reduction of carbon emissions. Competitive product substitutes, primarily coal and other fossil fuels, are facing increasing pressure due to environmental concerns and price volatility, further bolstering LNG's appeal. End-user demographics are diverse, ranging from large industrial consumers in petrochemicals and power generation to the rapidly expanding residential and commercial sectors under the city gas distribution network. Mergers and acquisitions (M&A) trends are indicative of consolidation and strategic expansion, as key players seek to secure market share and enhance their integrated offerings. For instance, significant investments in new import terminals and infrastructure projects signal robust growth.

- Market Concentration: Evolving with increasing competition and strategic partnerships.

- Technological Innovation: Focus on floating terminals, regasification efficiency, and bunkering solutions.

- Regulatory Frameworks: Supportive policies encouraging gas-based economy and emission reduction.

- Competitive Substitutes: Coal and other fossil fuels facing pressure from environmental mandates.

- End-User Demographics: Diversifying from industrial to residential and commercial sectors.

- M&A Trends: Indicative of market consolidation and strategic expansion.

India LNG Market Growth Trends & Insights

The India LNG market is poised for exponential growth, projected to reach significant volumes by the forecast period. This expansion is underpinned by a rising adoption rate of LNG across various applications, fueled by increasing energy demands and a conscious shift towards cleaner fuels. Technological disruptions, such as the development of smaller-scale LNG infrastructure and innovations in transportation, are making LNG more accessible to a wider range of consumers. Consumer behavior is shifting towards a preference for cleaner and more reliable energy sources, with a growing awareness of the environmental benefits of natural gas. Market penetration of LNG is accelerating, particularly in the city gas distribution (CGD) segment, driven by government initiatives to expand piped natural gas networks to households and industries. The projected Compound Annual Growth Rate (CAGR) for the India LNG market is robust, reflecting the strong underlying demand drivers and favorable policy environment. This growth trajectory is further bolstered by substantial investments in import terminals, regasification facilities, and the expansion of LNG shipping capabilities to meet the escalating demand. The integration of LNG into the broader energy mix is crucial for India's energy security and its commitment to decarbonization goals.

- Market Size Evolution: Significant projected growth driven by increasing demand and infrastructure development.

- Adoption Rates: Accelerating across industrial, commercial, and residential sectors.

- Technological Disruptions: Innovations in small-scale LNG and transportation enhancing accessibility.

- Consumer Behavior Shifts: Growing preference for cleaner and reliable energy sources.

- Market Penetration: Rapid expansion of City Gas Distribution networks.

- CAGR Projection: Robust growth anticipated due to strong demand and policy support.

Dominant Regions, Countries, or Segments in India LNG Market

Within the India LNG market, LNG Infrastructure, specifically LNG Regasification Facilities, along with the City Gas Distribution (CGD) application segment, are emerging as dominant growth drivers. India’s extensive coastline and strategic geographical location make it an ideal hub for LNG imports, necessitating robust regasification capabilities to convert LNG back into usable natural gas. Major coastal states are witnessing significant investments in LNG import terminals and associated regasification infrastructure. The CGD segment is experiencing unparalleled expansion, driven by the government's ambitious targets to provide clean cooking fuel to millions of households and to supply natural gas to industries and commercial establishments. This segment benefits from favorable policy support, including subsidies and incentives for network expansion, directly impacting the demand for regasified LNG.

- Dominant Segment - LNG Infrastructure:

- LNG Regasification Facilities: Critical for converting imported LNG into natural gas, witnessing substantial investment and capacity expansion.

- LNG Import Terminals: Strategic locations along the coast are crucial for efficient import of LNG, with ongoing development of new terminals.

- LNG Shipping: Essential for transporting LNG globally, with growing demand for specialized vessels.

- Dominant Application - City Gas Distribution (CGD):

- Household Piped Natural Gas (PNG): Rapid network expansion to cater to domestic cooking needs.

- Compressed Natural Gas (CNG): Increasing adoption as a cleaner alternative for transportation.

- Industrial and Commercial Fuel: Growing demand from industries seeking to reduce emissions and operational costs.

- Key Drivers:

- Economic Policies: Government initiatives promoting gas-based economy and clean energy.

- Infrastructure Development: Substantial investments in import terminals, regasification plants, and distribution networks.

- Environmental Concerns: Push for cleaner fuels to meet emission reduction targets.

- Growing Energy Demand: Rapid urbanization and industrialization driving overall energy consumption.

India LNG Market Product Landscape

The India LNG market's product landscape is centered around the efficient and safe delivery and utilization of Liquefied Natural Gas. Key offerings include LNG itself, which is natural gas cooled to approximately -162°C (-260°F) to reduce its volume for transportation and storage. Innovations are continuously enhancing the performance metrics of LNG handling, focusing on minimizing boil-off gas and maximizing energy efficiency throughout the supply chain. Products and services range from the construction and operation of LNG import terminals, regasification facilities, and liquefaction plants to specialized LNG carriers and bunkering solutions for the maritime sector. The application of LNG spans across various industries, with City Gas Distribution (CGD) and the petrochemical industry being significant consumers.

Key Drivers, Barriers & Challenges in India LNG Market

The India LNG market is propelled by several key drivers. Technological advancements in liquefaction, regasification, and transportation technologies are making LNG more viable. Government policies promoting a gas-based economy, coupled with environmental mandates to reduce carbon emissions, are significant drivers. The ever-increasing energy demand from a growing economy further fuels the need for cleaner and more accessible energy sources.

However, the market faces several barriers and challenges. High infrastructure costs associated with developing LNG import terminals, regasification facilities, and distribution networks can be substantial. Price volatility of global LNG prices can impact domestic affordability and competitiveness. Supply chain disruptions due to geopolitical factors or logistical constraints can pose risks. Furthermore, regulatory hurdles and permitting processes can sometimes slow down project development.

- Key Drivers:

- Technological advancements in LNG handling and infrastructure.

- Supportive government policies and emission reduction targets.

- Rising energy demand from a growing economy.

- Barriers & Challenges:

- High capital investment for infrastructure development.

- Global LNG price volatility.

- Supply chain risks and logistical complexities.

- Regulatory complexities and permitting delays.

Emerging Opportunities in India LNG Market

Emerging opportunities in the India LNG market are abundant, particularly in untapped geographical regions and innovative application areas. The expansion of City Gas Distribution networks into tier-2 and tier-3 cities presents a significant opportunity for increasing household and commercial access to natural gas. The development of dedicated LNG bunkering facilities at major ports is an emerging area, driven by the International Maritime Organization's (IMO) stricter emission regulations for ships. Furthermore, the potential for smaller-scale LNG solutions, including virtual pipelines and localized regasification units, can cater to industries and regions not connected by traditional pipeline infrastructure. The growing focus on industrial decarbonization also opens avenues for industries to transition to LNG as a cleaner fuel.

Growth Accelerators in the India LNG Market Industry

Several factors are acting as growth accelerators for the India LNG market. Strategic partnerships and collaborations between domestic energy companies and international LNG suppliers are crucial for securing long-term supply agreements and facilitating infrastructure development. Technological breakthroughs in areas like floating LNG terminals and advanced regasification technologies are enhancing flexibility and reducing project lead times. Market expansion strategies, including the aggressive build-out of CGD networks and the development of LNG hubs, are significantly increasing market reach. The consistent focus on energy security and diversification of energy sources by the Indian government provides a stable policy environment for sustained growth.

Key Players Shaping the India LNG Market Market

- Adani Total Gas

- Bharat Petroleum Corporation Limited

- Essar Ports Ltd

- GAIL Limited

- GSPC LNG Limited

- H-Energy Private Limited

- JSW Infrastructure

- Petronet LNG Ltd

- Shell PLC

Notable Milestones in India LNG Market Sector

- April 2022: Petronet LNG announced the development of a floating LNG terminal in Odisha by 2025, with an investment of INR 1600 crore.

- April 2022: Petronet LNG is likely to invest INR 600 crore in increasing the capacity of the Dahej LNG import terminal to 22.5 million tonnes per annum from the current 17.5 million tonnes.

- January 2022: LNG Alliance announced an investment of approximately USD 290 million for a major LNG import terminal in Karnataka, India's first dedicated LNG bunkering facility with a likely capacity of 4 million tonnes per annum (MTPA).

In-Depth India LNG Market Market Outlook

The India LNG market outlook is exceptionally promising, fueled by sustained demand, supportive government policies, and ongoing infrastructure development. Growth accelerators such as technological innovations in LNG handling and transportation, strategic international collaborations for supply security, and aggressive market expansion through CGD networks are set to significantly boost market penetration. The increasing emphasis on energy security and the transition to cleaner fuels will continue to drive investments in LNG infrastructure, including import terminals and regasification facilities. Emerging opportunities in LNG bunkering and small-scale LNG solutions will further diversify market applications and reach. The overall trajectory indicates a robust and sustained expansion, positioning India as a key global player in the LNG market.

India LNG Market Segmentation

-

1. LNG Infrastructure

- 1.1. LNG Liquefaction Plants

- 1.2. LNG Regasification Facilities

- 1.3. LNG Shipping

- 2. LNG Trade

-

3. Application

- 3.1. City Gas Distribution

- 3.2. Petrochemicals

- 3.3. Other Applications

India LNG Market Segmentation By Geography

- 1. India

India LNG Market Regional Market Share

Geographic Coverage of India LNG Market

India LNG Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by LNG Infrastructure

- 5.1.1. LNG Liquefaction Plants

- 5.1.2. LNG Regasification Facilities

- 5.1.3. LNG Shipping

- 5.2. Market Analysis, Insights and Forecast - by LNG Trade

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. City Gas Distribution

- 5.3.2. Petrochemicals

- 5.3.3. Other Applications

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. India

- 5.1. Market Analysis, Insights and Forecast - by LNG Infrastructure

- 6. India LNG Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by LNG Infrastructure

- 6.1.1. LNG Liquefaction Plants

- 6.1.2. LNG Regasification Facilities

- 6.1.3. LNG Shipping

- 6.2. Market Analysis, Insights and Forecast - by LNG Trade

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. City Gas Distribution

- 6.3.2. Petrochemicals

- 6.3.3. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by LNG Infrastructure

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Adani Total Gas

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Shell PLC

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Bharat Petroleum Corporation Limited

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Essar Ports Ltd*List Not Exhaustive

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Petronet LNG Ltd

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 GSPC LNG Limited

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 GAIL Limited

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 H-Energy Private Limited

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 JSW Infrastructure

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 Adani Total Gas

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: India LNG Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: India LNG Market Share (%) by Company 2025

List of Tables

- Table 1: India LNG Market Revenue billion Forecast, by LNG Infrastructure 2020 & 2033

- Table 2: India LNG Market Volume metric tonnes Forecast, by LNG Infrastructure 2020 & 2033

- Table 3: India LNG Market Revenue billion Forecast, by LNG Trade 2020 & 2033

- Table 4: India LNG Market Volume metric tonnes Forecast, by LNG Trade 2020 & 2033

- Table 5: India LNG Market Revenue billion Forecast, by Application 2020 & 2033

- Table 6: India LNG Market Volume metric tonnes Forecast, by Application 2020 & 2033

- Table 7: India LNG Market Revenue billion Forecast, by Region 2020 & 2033

- Table 8: India LNG Market Volume metric tonnes Forecast, by Region 2020 & 2033

- Table 9: India LNG Market Revenue billion Forecast, by LNG Infrastructure 2020 & 2033

- Table 10: India LNG Market Volume metric tonnes Forecast, by LNG Infrastructure 2020 & 2033

- Table 11: India LNG Market Revenue billion Forecast, by LNG Trade 2020 & 2033

- Table 12: India LNG Market Volume metric tonnes Forecast, by LNG Trade 2020 & 2033

- Table 13: India LNG Market Revenue billion Forecast, by Application 2020 & 2033

- Table 14: India LNG Market Volume metric tonnes Forecast, by Application 2020 & 2033

- Table 15: India LNG Market Revenue billion Forecast, by Country 2020 & 2033

- Table 16: India LNG Market Volume metric tonnes Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the India LNG Market?

The projected CAGR is approximately 8%.

2. Which companies are prominent players in the India LNG Market?

Key companies in the market include Adani Total Gas, Shell PLC, Bharat Petroleum Corporation Limited, Essar Ports Ltd*List Not Exhaustive, Petronet LNG Ltd, GSPC LNG Limited, GAIL Limited, H-Energy Private Limited, JSW Infrastructure.

3. What are the main segments of the India LNG Market?

The market segments include LNG Infrastructure, LNG Trade, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 15.98 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Gas Production and Infrastructure4.; Increasing Exploration and Production Activities.

6. What are the notable trends driving market growth?

City Gas Distribution segments to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Increasing Adoption of Clean Power Sources.

8. Can you provide examples of recent developments in the market?

In April 2022, Petronet LNG announced the development of a floating LNG terminal in Odisha by 2025 at the cost of INR 1600 crore. Furthermore, Petronet is likely to invest INR 600 crore in raising the capacity of the Dahej LNG import terminal to 22.5 million tonnes per annum from the current 17.5 million tonnes.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in metric tonnes.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "India LNG Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the India LNG Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the India LNG Market?

To stay informed about further developments, trends, and reports in the India LNG Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence