Key Insights

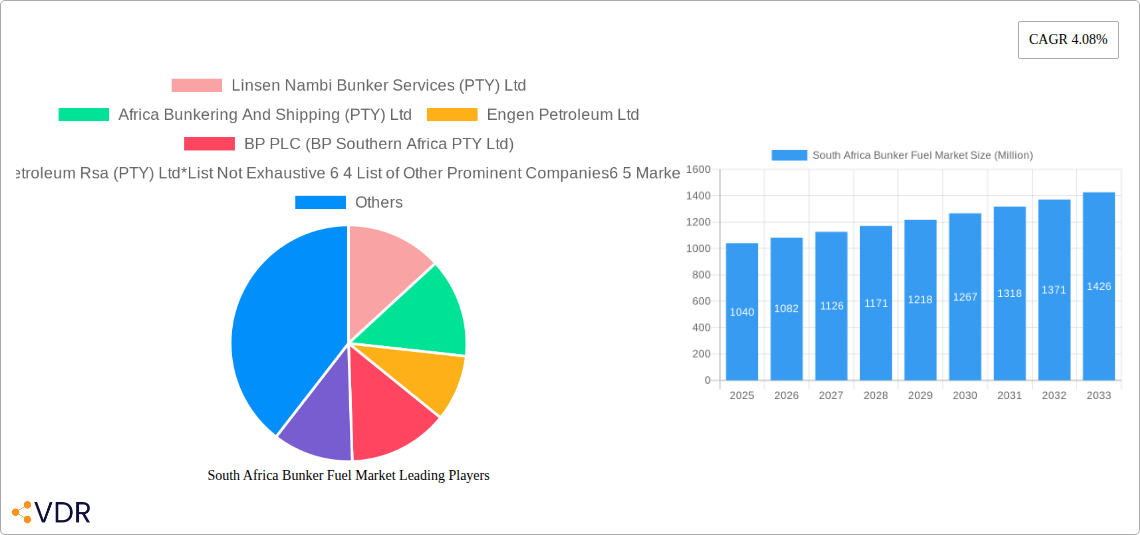

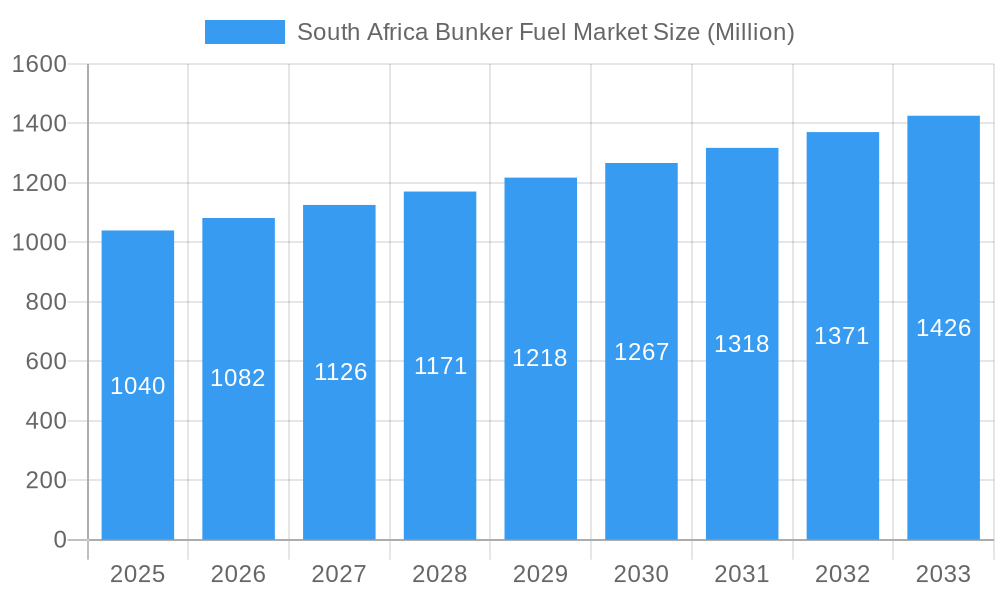

The South African bunker fuel market is poised for steady growth, projected to reach approximately USD 1.04 billion by 2025, with a Compound Annual Growth Rate (CAGR) of 4.08% anticipated from 2019 to 2033. This robust expansion is driven by several key factors, primarily the increasing volume of maritime trade activity in and around South African ports, which serve as crucial hubs for regional and international shipping routes. The growing demand for cleaner fuel alternatives, spurred by stringent environmental regulations like the IMO 2020 sulfur cap, is also a significant catalyst. This has led to a notable shift towards Very Low Sulfur Fuel Oil (VLSFO) and Marine Gas Oil (MGO), while Liquefied Natural Gas (LNG) is emerging as a promising, albeit nascent, alternative fuel for the future. The dominant vessel types contributing to this market include Containers and Tankers, owing to their significant presence in global trade and the types of cargo they transport, followed by General Cargo and Bulk Carriers.

South Africa Bunker Fuel Market Market Size (In Billion)

Despite the positive growth trajectory, the market faces certain restraints. The fluctuating prices of crude oil and bunker fuel directly impact operational costs for shipping companies, potentially leading to cost-saving measures that could temper demand. Furthermore, the initial high investment required for adopting newer, cleaner fuel technologies and retrofitting vessels for LNG can act as a deterrent for smaller operators. Infrastructure development for alternative fuels like LNG at South African ports remains a critical area for future investment and expansion. Key players such as Engen Petroleum Ltd, BP PLC, and Linsen Nambi Bunker Services are actively shaping the market through their supply chain networks and service offerings, vying for market share in this dynamic environment. The market's performance is closely tied to South Africa's broader economic health and its strategic importance in facilitating global maritime commerce.

South Africa Bunker Fuel Market Company Market Share

This in-depth report provides a granular analysis of the South Africa Bunker Fuel Market, offering a strategic overview of its dynamics, growth trajectories, and competitive landscape. Covering a study period from 2019 to 2033, with a base and estimated year of 2025 and a forecast period from 2025 to 2033, this report delves into critical market segments, regional influences, and emerging trends. It is an indispensable resource for stakeholders seeking to understand the complexities of South Africa's maritime fuel sector, including its parent and child market interdependencies.

South Africa Bunker Fuel Market Market Dynamics & Structure

The South Africa Bunker Fuel Market is characterized by a moderately concentrated competitive landscape, with key players strategically vying for market share through pricing, service innovation, and geographical expansion. Technological innovation drivers are increasingly focused on sustainable fuel solutions, responding to global decarbonization pressures and the IMO's stringent environmental regulations. Regulatory frameworks, particularly those concerning emissions standards and fuel quality, exert significant influence, shaping product development and operational strategies. Competitive product substitutes, ranging from traditional High Sulfur Fuel Oil (HSFO) to emerging Very Low Sulfur Fuel Oil (VLSFO) and Marine Gas Oil (MGO), and the nascent Liquefied Natural Gas (LNG) sector, present distinct market opportunities and challenges. End-user demographics are primarily driven by the volume and type of maritime traffic calling at South African ports. Merger and acquisition (M&A) trends are indicative of consolidation efforts and strategic alliances aimed at enhancing market reach and operational efficiency. For instance, an estimated 3-5 significant M&A transactions are projected within the forecast period, driven by companies seeking to expand their bunkering infrastructure and service offerings. Innovation barriers include the substantial capital investment required for alternative fuel infrastructure and the ongoing uncertainty surrounding the widespread adoption of new fuel technologies.

- Market Concentration: Dominated by a few major players with a significant presence in key bunkering hubs.

- Technological Innovation: Focus on VLSFO, MGO, and exploration of LNG and alternative fuels.

- Regulatory Influence: IMO 2020 regulations and upcoming emissions targets are key shapers.

- Competitive Substitutes: Shift from HSFO to lower sulfur alternatives.

- End-User Dynamics: Driven by container, tanker, and bulk carrier segments.

- M&A Activity: Anticipated consolidation and strategic partnerships.

- Innovation Barriers: High infrastructure costs and technological adoption uncertainties.

South Africa Bunker Fuel Market Growth Trends & Insights

The South Africa Bunker Fuel Market is poised for robust growth, propelled by increased maritime trade volumes and the ongoing transition towards cleaner energy solutions. The market size is projected to evolve from approximately $5,500 Million in 2024 to an estimated $8,200 Million by 2033, reflecting a Compound Annual Growth Rate (CAGR) of around 4.5%. Adoption rates for VLSFO and MGO have significantly increased, driven by regulatory compliance and growing environmental consciousness among shipping operators. Technological disruptions, such as advancements in fuel blending capabilities and the development of shore power infrastructure at ports, are poised to further optimize bunkering operations. Consumer behavior shifts are evident, with an increasing demand for reliable and cost-effective supply chains for compliant fuels. The adoption of LNG as a marine fuel, while still in its nascent stages in South Africa, presents a substantial long-term growth opportunity, with adoption rates expected to rise from xx% in 2025 to xx% by 2033. The penetration of sustainable maritime solutions, including biofuels and potential future hydrogen-based fuels, will be a key indicator of market maturity. Furthermore, the strategic location of South African ports along crucial shipping routes will continue to be a primary driver of sustained demand.

Dominant Regions, Countries, or Segments in South Africa Bunker Fuel Market

Within the South Africa Bunker Fuel Market, the Vessel Type: Tankers segment is anticipated to demonstrate the most significant dominance in terms of volume and revenue, driven by the country's substantial crude oil imports and refined product exports. This segment is projected to account for approximately 35-40% of the total market share during the forecast period. The Port of Durban is expected to remain the leading bunkering hub, benefiting from its strategic location, extensive infrastructure, and high vessel traffic. Cape Town and Port Elizabeth also play crucial roles, contributing to regional market dynamics.

- Dominant Vessel Type: Tankers (crude oil, refined products, chemical carriers)

- Key Ports: Durban (leading), Cape Town, Port Elizabeth, Ngqura.

- Fuel Type Dominance: While VLSFO is currently dominant due to regulatory compliance, the demand for MGO for specific vessel types and shorter voyages remains significant. The market for HSFO is gradually declining.

- Economic Policies: Government initiatives supporting maritime trade and port modernization are crucial drivers. For example, the National Maritime Policy aims to boost South Africa's maritime sector, indirectly influencing bunker fuel demand.

- Infrastructure Development: Investments in port facilities and bunkering terminals, such as the ongoing expansion projects at the Port of Durban, are critical for accommodating larger vessels and a wider range of fuel types.

- Growth Potential: Tanker traffic growth is projected at 5.0% CAGR, outpacing other vessel types due to global energy demand. The growth in VLSFO demand is expected to remain strong, with an estimated market share of 60-65% by 2033.

South Africa Bunker Fuel Market Product Landscape

The product landscape of the South Africa Bunker Fuel Market is evolving rapidly, with a clear shift towards cleaner fuel options. Very Low Sulfur Fuel Oil (VLSFO) and Marine Gas Oil (MGO) have become the primary offerings, meeting International Maritime Organization (IMO) 2020 sulfur regulations. The performance metrics for these fuels are critical, focusing on consistent quality, low sulfur content (typically <0.5%), and compatibility with modern engine technologies. While Liquefied Natural Gas (LNG) is emerging, its infrastructure is still developing. Innovations are focused on improving fuel efficiency, reducing emissions, and ensuring reliable supply chains for these advanced fuels.

Key Drivers, Barriers & Challenges in South Africa Bunker Fuel Market

Key Drivers:

- Increasing Global Trade & Maritime Activity: South Africa's strategic position on global shipping lanes ensures consistent demand for bunker fuel.

- Stricter Environmental Regulations: IMO 2020 and future emission reduction targets necessitate the use of cleaner fuels like VLSFO and MGO.

- Port Infrastructure Development: Investments in upgrading and expanding key ports enhance bunkering capabilities.

- Growth in Specific Vessel Segments: Increased activity in container shipping and tanker trade fuels demand.

Barriers & Challenges:

- Volatility in Crude Oil Prices: Fluctuations in global oil prices directly impact bunker fuel costs, affecting profitability and demand.

- Infrastructure for Alternative Fuels: Limited availability of LNG bunkering infrastructure and the high cost of developing new fuel supply chains.

- Competition from Regional Bunkering Hubs: Neighboring countries with competitive pricing or more developed infrastructure can divert demand.

- Supply Chain Disruptions: Geopolitical events or domestic logistical issues can impact the consistent availability of bunker fuels. For example, port congestion can lead to delays and increased costs, estimated to impact supply by 5-10% in critical periods.

Emerging Opportunities in South Africa Bunker Fuel Market

Emerging opportunities within the South Africa Bunker Fuel Market lie in the expansion of LNG bunkering infrastructure, catering to the growing global interest in this transitional fuel. The development of green methanol and ammonia bunkering facilities represents a significant long-term opportunity, aligning with the global push for zero-emission shipping. Furthermore, digitalization of bunkering operations, including advanced tracking, payment systems, and predictive supply chain management, offers avenues for increased efficiency and customer service. Tapping into the offshore supply vessel (OSV) market, supporting offshore oil and gas exploration, also presents a niche growth area.

Growth Accelerators in the South Africa Bunker Fuel Market Industry

Growth in the South Africa Bunker Fuel Market will be significantly accelerated by strategic partnerships between fuel suppliers and shipping lines to develop integrated supply solutions for cleaner fuels. Investments in research and development for alternative marine fuels, including biofuels and synthetic fuels, will be critical for long-term sustainability. Government incentives and policy support for adopting low-emission technologies and expanding bunkering infrastructure will play a pivotal role. The establishment of maritime green corridors, as seen with the South Africa-Europe initiative, will act as powerful catalysts for innovation and adoption of sustainable practices.

Key Players Shaping the South Africa Bunker Fuel Market Market

- Linsen Nambi Bunker Services (PTY) Ltd

- Africa Bunkering And Shipping (PTY) Ltd

- Engen Petroleum Ltd

- BP PLC (BP Southern Africa PTY Ltd)

- Ocean South Petroleum Rsa (PTY) Ltd

Notable Milestones in South Africa Bunker Fuel Market Sector

- April 2024: Navigator Holdings (Navigator Gas) successfully conducted its inaugural ship-to-ship ammonia transfer at the Port of Ngqura, South Africa, demonstrating advancements in handling new maritime fuels.

- March 2023: South Africa and Europe launched a new maritime green corridor project for iron ore transport, focusing on zero-emission shipping through collaboration and innovative bunkering arrangements.

In-Depth South Africa Bunker Fuel Market Market Outlook

The future outlook for the South Africa Bunker Fuel Market is strongly characterized by a transition towards sustainability, driven by stringent environmental regulations and a global commitment to decarbonization. Key growth accelerators will include the expansion of alternative fuel infrastructure, particularly for LNG and potentially hydrogen-based fuels, supported by significant investment and government policy. Strategic alliances between fuel providers and maritime stakeholders will be crucial for developing efficient and cost-effective supply chains for these next-generation fuels. The market is expected to see a continued dominance of VLSFO and MGO in the near to medium term, with a gradual but significant rise in the adoption of lower-carbon and zero-emission alternatives, positioning South Africa as a pivotal player in the evolving global maritime fuel landscape. The market size is projected to reach an impressive $9,500 Million by 2033, driven by these transformative trends.

South Africa Bunker Fuel Market Segmentation

-

1. Fuel Type

- 1.1. High Sulfur Fuel Oil (HSFO)

- 1.2. Very Low Sulfur Fuel Oil (VLSFO)

- 1.3. Marine Gas Oil (MGO)

- 1.4. Liquefied Natural Gas (LNG)

- 1.5. Other Fuel Types

-

2. Vessel Type

- 2.1. Containers

- 2.2. Tankers

- 2.3. General Cargo

- 2.4. Bulk Carriers

- 2.5. Other Vessel Types

South Africa Bunker Fuel Market Segmentation By Geography

- 1. South Africa

South Africa Bunker Fuel Market Regional Market Share

Geographic Coverage of South Africa Bunker Fuel Market

South Africa Bunker Fuel Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.08% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Fuel Type

- 5.1.1. High Sulfur Fuel Oil (HSFO)

- 5.1.2. Very Low Sulfur Fuel Oil (VLSFO)

- 5.1.3. Marine Gas Oil (MGO)

- 5.1.4. Liquefied Natural Gas (LNG)

- 5.1.5. Other Fuel Types

- 5.2. Market Analysis, Insights and Forecast - by Vessel Type

- 5.2.1. Containers

- 5.2.2. Tankers

- 5.2.3. General Cargo

- 5.2.4. Bulk Carriers

- 5.2.5. Other Vessel Types

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. South Africa

- 5.1. Market Analysis, Insights and Forecast - by Fuel Type

- 6. South Africa Bunker Fuel Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Fuel Type

- 6.1.1. High Sulfur Fuel Oil (HSFO)

- 6.1.2. Very Low Sulfur Fuel Oil (VLSFO)

- 6.1.3. Marine Gas Oil (MGO)

- 6.1.4. Liquefied Natural Gas (LNG)

- 6.1.5. Other Fuel Types

- 6.2. Market Analysis, Insights and Forecast - by Vessel Type

- 6.2.1. Containers

- 6.2.2. Tankers

- 6.2.3. General Cargo

- 6.2.4. Bulk Carriers

- 6.2.5. Other Vessel Types

- 6.1. Market Analysis, Insights and Forecast - by Fuel Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Linsen Nambi Bunker Services (PTY) Ltd

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Africa Bunkering And Shipping (PTY) Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Engen Petroleum Ltd

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 BP PLC (BP Southern Africa PTY Ltd)

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Ocean South Petroleum Rsa (PTY) Ltd*List Not Exhaustive 6 4 List of Other Prominent Companies6 5 Market Ranking/Share Analysi

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.1 Linsen Nambi Bunker Services (PTY) Ltd

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: South Africa Bunker Fuel Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: South Africa Bunker Fuel Market Share (%) by Company 2025

List of Tables

- Table 1: South Africa Bunker Fuel Market Revenue Million Forecast, by Fuel Type 2020 & 2033

- Table 2: South Africa Bunker Fuel Market Volume Billion Forecast, by Fuel Type 2020 & 2033

- Table 3: South Africa Bunker Fuel Market Revenue Million Forecast, by Vessel Type 2020 & 2033

- Table 4: South Africa Bunker Fuel Market Volume Billion Forecast, by Vessel Type 2020 & 2033

- Table 5: South Africa Bunker Fuel Market Revenue Million Forecast, by Region 2020 & 2033

- Table 6: South Africa Bunker Fuel Market Volume Billion Forecast, by Region 2020 & 2033

- Table 7: South Africa Bunker Fuel Market Revenue Million Forecast, by Fuel Type 2020 & 2033

- Table 8: South Africa Bunker Fuel Market Volume Billion Forecast, by Fuel Type 2020 & 2033

- Table 9: South Africa Bunker Fuel Market Revenue Million Forecast, by Vessel Type 2020 & 2033

- Table 10: South Africa Bunker Fuel Market Volume Billion Forecast, by Vessel Type 2020 & 2033

- Table 11: South Africa Bunker Fuel Market Revenue Million Forecast, by Country 2020 & 2033

- Table 12: South Africa Bunker Fuel Market Volume Billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the South Africa Bunker Fuel Market?

The projected CAGR is approximately 4.08%.

2. Which companies are prominent players in the South Africa Bunker Fuel Market?

Key companies in the market include Linsen Nambi Bunker Services (PTY) Ltd, Africa Bunkering And Shipping (PTY) Ltd, Engen Petroleum Ltd, BP PLC (BP Southern Africa PTY Ltd), Ocean South Petroleum Rsa (PTY) Ltd*List Not Exhaustive 6 4 List of Other Prominent Companies6 5 Market Ranking/Share Analysi.

3. What are the main segments of the South Africa Bunker Fuel Market?

The market segments include Fuel Type, Vessel Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.04 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Maritime Trade4.; Supportive Government Policy Toward Low-emission Bunker Fuel.

6. What are the notable trends driving market growth?

Increasing Maritime Trade Driving the Market.

7. Are there any restraints impacting market growth?

4.; Increasing Maritime Trade4.; Supportive Government Policy Toward Low-emission Bunker Fuel.

8. Can you provide examples of recent developments in the market?

April 2024: Navigator Holdings (Navigator Gas), based in the United Kingdom and operating a fleet of handy-size liquefied gas carriers, successfully conducted its inaugural ship-to-ship ammonia transfer. At the Port of Ngqura in South Africa, Navigator Gas' 38,000 cbm liquefied petroleum gas (LPG) carrier, NAVIGATOR JORF, took on 25,300 metric tons of anhydrous ammonia (NH3) from the LPG tanker ECO ORACLE, while both vessels were moored side by side.March 2023: South Africa and Europe launched a new maritime green corridor project to transport iron ore between the two regions. The project includes forming a consortium to find ways to achieve zero-emission shipping. Companies like Anglo American, Tata Steel, CMB, VUKA Marine, Freeport Saldanha, and ENGIE are expected to collaborate to develop the green corridor through bunkering and offtake arrangements, green bunker fuel supplies, and financial and business model alternatives.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "South Africa Bunker Fuel Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the South Africa Bunker Fuel Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the South Africa Bunker Fuel Market?

To stay informed about further developments, trends, and reports in the South Africa Bunker Fuel Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence