Key Insights

The East European battery market is projected for substantial growth, anticipated to reach $30.4 billion by 2025, with a Compound Annual Growth Rate (CAGR) of 10.28% through 2033. This expansion is propelled by robust demand from the automotive sector, fueled by increasing electric vehicle (EV) adoption and the need for reliable battery systems in conventional vehicles. The industrial sector's growing requirement for advanced energy storage to enhance grid stability, integrate renewables, and ensure backup power further contributes significantly. While the portable electronics segment remains a mature market, it continues to provide consistent volume. Favorable regional positioning and a growing emphasis on localized manufacturing and supply chain resilience are also key growth accelerators.

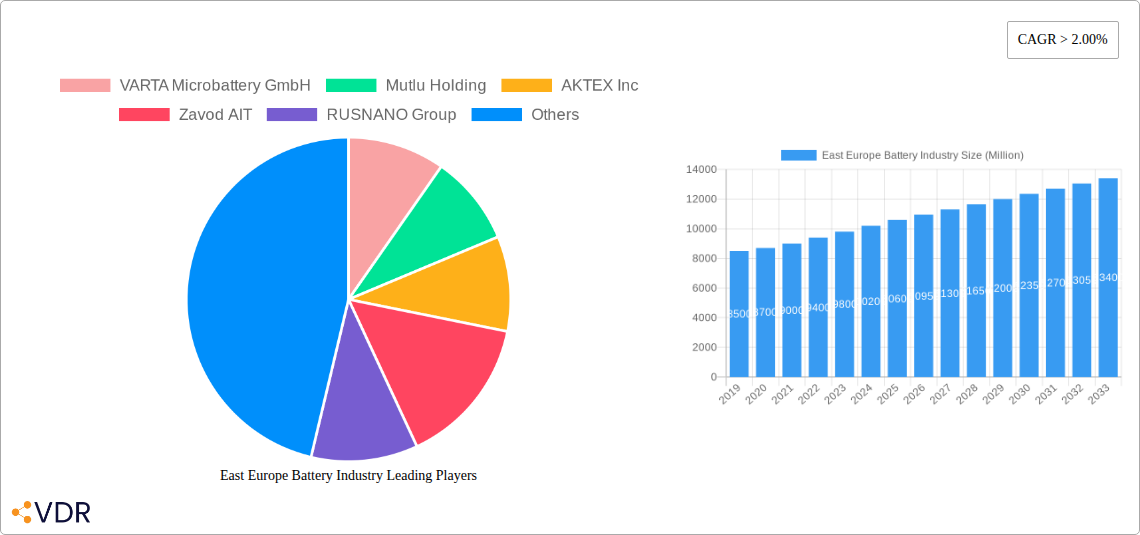

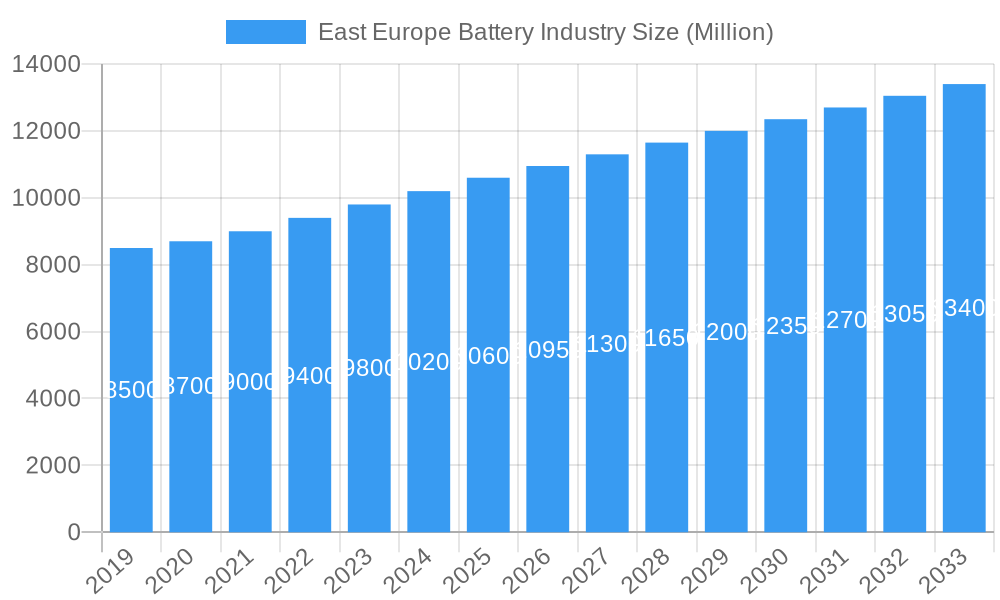

East Europe Battery Industry Market Size (In Billion)

Key trends in the East European battery industry include a strong preference for Lithium-ion battery technology due to its superior energy density, extended lifespan, and decreasing costs, making it ideal for EVs and consumer electronics. Although Lead-acid batteries will persist in specific industrial and automotive backup roles, their market share is expected to decline. Flow batteries are emerging as a viable solution for large-scale stationary energy storage, supporting the region's renewable energy objectives. Market growth faces constraints from volatile raw material prices, particularly for lithium and cobalt, and the necessity for significant investment in manufacturing infrastructure and R&D. Geopolitical dynamics and evolving regulatory frameworks also present challenges that industry players must address. Leading companies, including VARTA Microbattery GmbH, Contemporary Amperex Technology Co Ltd, and Mutlu Holding, are driving market evolution through innovation and strategic initiatives.

East Europe Battery Industry Company Market Share

This comprehensive report offers a definitive analysis of the East European battery market, covering primary and secondary battery types with in-depth insights into lithium-ion, lead-acid, and flow battery technologies. Our research examines automotive, industrial, and portable applications, providing critical intelligence on market dynamics, growth trajectories, and competitive landscapes. Covering the period from 2019 to 2033, with 2025 as the base year, this report is indispensable for stakeholders aiming to comprehend and leverage the burgeoning East Europe battery industry, encompassing EV battery production and battery energy storage systems (BESS).

East Europe Battery Industry Market Dynamics & Structure

The East European battery industry is characterized by a dynamic interplay of market concentration, rapid technological innovation, and evolving regulatory frameworks. The surge in demand for energy storage solutions, particularly driven by the automotive and industrial sectors, is reshaping market dynamics. Significant investments in battery manufacturing and research are evident across key countries, fostering both domestic production capabilities and foreign direct investment. The competitive landscape features a mix of established global players and emerging regional manufacturers, each vying for market share through product differentiation and strategic alliances.

- Market Concentration: While some segments exhibit moderate concentration, the overall market is becoming increasingly competitive with the entry of new players and expansion of existing capacities.

- Technological Innovation Drivers: The primary drivers of innovation include the pursuit of higher energy density, faster charging capabilities, enhanced safety features, and cost reduction for lithium-ion batteries. Flow batteries are gaining traction for grid-scale applications.

- Regulatory Frameworks: Supportive government policies, including subsidies for EV adoption and renewable energy integration, are crucial enablers. Strict environmental regulations also push for the development of more sustainable battery solutions.

- Competitive Product Substitutes: Traditional lead-acid batteries continue to serve cost-sensitive industrial applications, but lithium-ion batteries are rapidly replacing them in automotive and portable electronics due to their superior performance.

- End-User Demographics: The growing middle class, increasing urbanization, and the widespread adoption of electric vehicles are key demographic shifts influencing demand. Industrial automation and the expansion of renewable energy infrastructure further diversify end-user segments.

- M&A Trends: The sector is witnessing strategic mergers and acquisitions aimed at consolidating market share, acquiring advanced technologies, and expanding production footprints to meet escalating demand. For instance, recent investments in expanding EV battery plants highlight a trend towards capacity building.

East Europe Battery Industry Growth Trends & Insights

The East European battery market is poised for remarkable growth, driven by a confluence of factors including government support for green initiatives, the accelerating adoption of electric vehicles, and the expansion of renewable energy infrastructure. The market size is projected to expand significantly over the forecast period (2025-2033), with robust CAGR values reflecting sustained demand across various applications. Technological disruptions, particularly the advancement in lithium-ion battery chemistries and the emergence of next-generation energy storage solutions like solid-state batteries and advanced flow batteries, are fundamentally altering the competitive landscape and opening new avenues for market penetration.

Consumer behavior is also undergoing a perceptible shift, with an increasing preference for sustainable and energy-efficient products. This is evident in the growing demand for electric vehicles, smart home devices, and industrial equipment powered by advanced battery technology. The push for electrification across transportation and industrial sectors, coupled with supportive policies and incentives from the European Union and national governments, is creating a fertile ground for battery manufacturers and suppliers. The market penetration of lithium-ion batteries in automotive applications is expected to reach new heights, while industrial applications will continue to rely on a mix of lead-acid and advanced battery solutions for energy storage and backup power. The development of battery energy storage systems (BESS) is a critical growth area, essential for grid stability and the integration of intermittent renewable energy sources. This surge in demand necessitates increased manufacturing capacity and continuous innovation to meet stringent performance, safety, and cost requirements. The overall market evolution indicates a sustained upward trajectory, driven by technological advancements, supportive policies, and a growing consciousness towards sustainable energy solutions.

Dominant Regions, Countries, or Segments in East Europe Battery Industry

The East European battery industry's growth is predominantly driven by key regions and specific segments that are strategically positioned to leverage market opportunities and capitalize on supportive policies. Among the battery types, Secondary Batteries are unequivocally leading the market expansion. This dominance is largely attributable to the exponential growth in demand for rechargeable battery solutions across a multitude of applications, most notably electric vehicles (EVs) and industrial energy storage.

Within the technology landscape, Lithium-ion Batteries are the primary growth engine. Their superior energy density, longer lifespan, and faster charging capabilities make them the preferred choice for high-demand sectors like automotive and portable electronics. The expansion of EV battery manufacturing facilities, as exemplified by the European Commission's aid for LG Chem in Poland, underscores the significance of this technology.

In terms of applications, the Automotive sector stands out as the most significant contributor to market growth. The accelerating transition towards electric mobility across East European countries, fueled by government incentives and consumer preference for sustainable transportation, has created an unprecedented demand for automotive batteries. Industrial applications, including grid-scale energy storage (BESS) and backup power solutions for critical infrastructure, also represent substantial growth areas.

- Leading Region: While several countries show promise, Poland is emerging as a dominant force due to its strategic location, robust industrial base, and significant investments in battery manufacturing, particularly for EVs. Its role as a hub for international battery manufacturers is a key differentiator.

- Key Drivers:

- Government Incentives and Policy Support: Substantial grants and subsidies for EV adoption and battery production (e.g., Romania's investment in BESS) are crucial catalysts.

- Expanding EV Production Capacity: Investments in expanding EV battery plants are directly translating into increased demand for battery components and finished products.

- Growth of Renewable Energy Sector: The increasing integration of solar and wind power necessitates significant battery energy storage systems for grid stability, driving demand for large-scale batteries.

- Industrial Modernization: The push for automation and electrification in manufacturing and logistics is boosting demand for industrial battery solutions.

- Consumer Adoption of EVs: Growing consumer awareness and acceptance of electric vehicles, coupled with the expanding charging infrastructure, are fueling the automotive battery market.

- Market Share and Growth Potential: Lithium-ion batteries for automotive applications are projected to command the largest market share and exhibit the highest growth potential over the forecast period. The industrial segment, particularly BESS, is also expected to witness substantial expansion.

East Europe Battery Industry Product Landscape

The East European battery industry is characterized by continuous product innovation and diversification to meet the evolving demands of various sectors. Manufacturers are focusing on enhancing the performance metrics of existing battery technologies while also exploring novel solutions. Lithium-ion batteries are seeing advancements in energy density, power output, and charging speeds, crucial for the booming electric vehicle market. Innovations in battery management systems (BMS) are also critical for optimizing performance and ensuring safety. For industrial applications, there's a growing emphasis on robust and long-lasting battery solutions, including advanced lead-acid technologies and the emerging flow battery segment, which offers scalability for grid-level energy storage. Unique selling propositions often lie in customized battery pack designs, integrated energy management solutions, and adherence to stringent safety and environmental standards.

Key Drivers, Barriers & Challenges in East Europe Battery Industry

Key Drivers: The East European battery industry is propelled by robust demand for electric vehicles (EVs) and the burgeoning renewable energy sector. Government incentives, such as grants for battery energy storage systems and EV purchase subsidies, are significant growth accelerators. Technological advancements in lithium-ion battery chemistries, leading to higher energy density and faster charging, are also crucial drivers. The expansion of manufacturing capacities by both established players and new entrants further fuels market growth.

Barriers & Challenges: Significant challenges include intense competition from established global manufacturers, leading to price pressures. Supply chain vulnerabilities, particularly concerning the sourcing of critical raw materials like lithium and cobalt, pose a considerable risk. Stringent regulatory hurdles and the need for significant capital investment for large-scale battery production facilities can also act as barriers. Furthermore, the development of robust recycling infrastructure for end-of-life batteries remains a critical challenge for sustainable growth.

Emerging Opportunities in East Europe Battery Industry

Emerging opportunities in the East European battery industry lie in the increasing demand for battery energy storage systems (BESS) to support grid stability and the integration of renewable energy sources. The continued growth of the electric vehicle market presents opportunities for localized manufacturing and the development of specialized battery solutions for different EV segments. Furthermore, the expansion of smart grid technologies and the growing adoption of portable electronics offer avenues for innovation in primary and secondary battery technologies. Untapped markets in regions with developing industrial bases also represent potential growth areas for affordable and reliable battery solutions.

Growth Accelerators in the East Europe Battery Industry Industry

Several factors are accelerating the long-term growth of the East European battery industry. Strategic partnerships between battery manufacturers, automotive companies, and renewable energy developers are fostering innovation and market expansion. Technological breakthroughs in battery chemistries, such as solid-state batteries and advanced flow batteries, promise higher performance and greater safety, further stimulating market adoption. Government-backed initiatives aimed at establishing regional battery production hubs and securing raw material supply chains are also crucial growth accelerators, creating a more resilient and competitive industry.

Key Players Shaping the East Europe Battery Industry Market

- VARTA Microbattery GmbH

- Mutlu Holding

- AKTEX Inc

- Zavod AIT

- RUSNANO Group

- EAS Batteries GmbH

- Duracell Inc

- CEZ Group

- Contemporary Amperex Technology Co Ltd

Notable Milestones in East Europe Battery Industry Sector

- December 2022: The Romanian government allocated USD 108.6 million grant to support investments in battery energy storage systems and deliver at least 240 MW/480 MWh by 2025. The grants will be allocated for purchasing system components and equipment for the construction of new battery projects, as well as the construction of the BESS facilities.

- March 2022: The European Commission announced that it had approved a USD 105 million aid for Poland to expand LG Chem's Electric Vehicles (EVs) battery plant. The investment will support the expansion of LG Chem's battery cell production facility for EVs in Poland's Dolnośląskie region.

In-Depth East Europe Battery Industry Market Outlook

The East European battery industry is on a trajectory of significant expansion, with future market potential driven by sustained demand from the electric vehicle revolution and the critical need for advanced energy storage solutions. Strategic opportunities abound in scaling up manufacturing capacities, fostering localized supply chains for raw materials, and investing in research and development for next-generation battery technologies. The continued supportive policy environment, coupled with growing environmental consciousness and technological advancements, positions the East European battery market for substantial and sustained growth, making it an attractive landscape for investors and industry participants alike.

East Europe Battery Industry Segmentation

-

1. Type

- 1.1. Primary Battery

- 1.2. Secondary Battery

-

2. Technology

- 2.1. Lithium-ion Battery

- 2.2. Lead-acid Battery

- 2.3. Flow Battery

- 2.4. Others

-

3. Application

- 3.1. Automotive

- 3.2. Industrial

- 3.3. Portable

- 3.4. Others

East Europe Battery Industry Segmentation By Geography

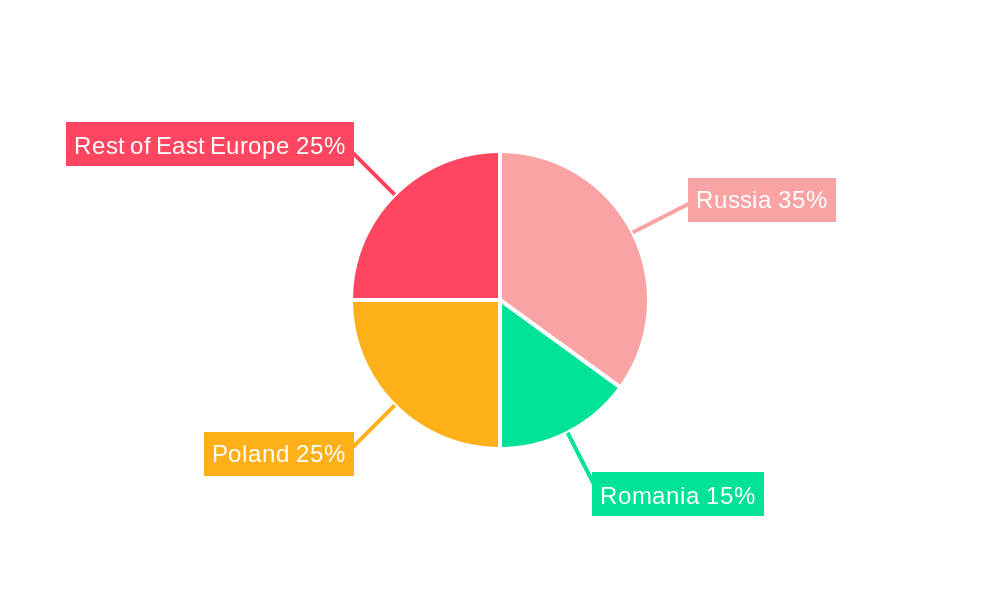

- 1. Russia

- 2. Romania

- 3. Poland

- 4. Rest of East Europe

East Europe Battery Industry Regional Market Share

Geographic Coverage of East Europe Battery Industry

East Europe Battery Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.28% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Primary Battery

- 5.1.2. Secondary Battery

- 5.2. Market Analysis, Insights and Forecast - by Technology

- 5.2.1. Lithium-ion Battery

- 5.2.2. Lead-acid Battery

- 5.2.3. Flow Battery

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Automotive

- 5.3.2. Industrial

- 5.3.3. Portable

- 5.3.4. Others

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Russia

- 5.4.2. Romania

- 5.4.3. Poland

- 5.4.4. Rest of East Europe

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. East Europe Battery Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Primary Battery

- 6.1.2. Secondary Battery

- 6.2. Market Analysis, Insights and Forecast - by Technology

- 6.2.1. Lithium-ion Battery

- 6.2.2. Lead-acid Battery

- 6.2.3. Flow Battery

- 6.2.4. Others

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Automotive

- 6.3.2. Industrial

- 6.3.3. Portable

- 6.3.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Russia East Europe Battery Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Primary Battery

- 7.1.2. Secondary Battery

- 7.2. Market Analysis, Insights and Forecast - by Technology

- 7.2.1. Lithium-ion Battery

- 7.2.2. Lead-acid Battery

- 7.2.3. Flow Battery

- 7.2.4. Others

- 7.3. Market Analysis, Insights and Forecast - by Application

- 7.3.1. Automotive

- 7.3.2. Industrial

- 7.3.3. Portable

- 7.3.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Romania East Europe Battery Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Primary Battery

- 8.1.2. Secondary Battery

- 8.2. Market Analysis, Insights and Forecast - by Technology

- 8.2.1. Lithium-ion Battery

- 8.2.2. Lead-acid Battery

- 8.2.3. Flow Battery

- 8.2.4. Others

- 8.3. Market Analysis, Insights and Forecast - by Application

- 8.3.1. Automotive

- 8.3.2. Industrial

- 8.3.3. Portable

- 8.3.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Poland East Europe Battery Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Primary Battery

- 9.1.2. Secondary Battery

- 9.2. Market Analysis, Insights and Forecast - by Technology

- 9.2.1. Lithium-ion Battery

- 9.2.2. Lead-acid Battery

- 9.2.3. Flow Battery

- 9.2.4. Others

- 9.3. Market Analysis, Insights and Forecast - by Application

- 9.3.1. Automotive

- 9.3.2. Industrial

- 9.3.3. Portable

- 9.3.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Rest of East Europe East Europe Battery Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Primary Battery

- 10.1.2. Secondary Battery

- 10.2. Market Analysis, Insights and Forecast - by Technology

- 10.2.1. Lithium-ion Battery

- 10.2.2. Lead-acid Battery

- 10.2.3. Flow Battery

- 10.2.4. Others

- 10.3. Market Analysis, Insights and Forecast - by Application

- 10.3.1. Automotive

- 10.3.2. Industrial

- 10.3.3. Portable

- 10.3.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 VARTA Microbattery GmbH

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Mutlu Holding

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 AKTEX Inc

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Zavod AIT

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 RUSNANO Group

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 EAS Batteries GmbH

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Duracell Inc*List Not Exhaustive

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 CEZ as (CEZ Group)

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Contemporary Amperex Technology Co Ltd

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.1 VARTA Microbattery GmbH

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: East Europe Battery Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: East Europe Battery Industry Share (%) by Company 2025

List of Tables

- Table 1: East Europe Battery Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: East Europe Battery Industry Volume K Units Forecast, by Type 2020 & 2033

- Table 3: East Europe Battery Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 4: East Europe Battery Industry Volume K Units Forecast, by Technology 2020 & 2033

- Table 5: East Europe Battery Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 6: East Europe Battery Industry Volume K Units Forecast, by Application 2020 & 2033

- Table 7: East Europe Battery Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 8: East Europe Battery Industry Volume K Units Forecast, by Region 2020 & 2033

- Table 9: East Europe Battery Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 10: East Europe Battery Industry Volume K Units Forecast, by Type 2020 & 2033

- Table 11: East Europe Battery Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 12: East Europe Battery Industry Volume K Units Forecast, by Technology 2020 & 2033

- Table 13: East Europe Battery Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 14: East Europe Battery Industry Volume K Units Forecast, by Application 2020 & 2033

- Table 15: East Europe Battery Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: East Europe Battery Industry Volume K Units Forecast, by Country 2020 & 2033

- Table 17: East Europe Battery Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 18: East Europe Battery Industry Volume K Units Forecast, by Type 2020 & 2033

- Table 19: East Europe Battery Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 20: East Europe Battery Industry Volume K Units Forecast, by Technology 2020 & 2033

- Table 21: East Europe Battery Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 22: East Europe Battery Industry Volume K Units Forecast, by Application 2020 & 2033

- Table 23: East Europe Battery Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 24: East Europe Battery Industry Volume K Units Forecast, by Country 2020 & 2033

- Table 25: East Europe Battery Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 26: East Europe Battery Industry Volume K Units Forecast, by Type 2020 & 2033

- Table 27: East Europe Battery Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 28: East Europe Battery Industry Volume K Units Forecast, by Technology 2020 & 2033

- Table 29: East Europe Battery Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 30: East Europe Battery Industry Volume K Units Forecast, by Application 2020 & 2033

- Table 31: East Europe Battery Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 32: East Europe Battery Industry Volume K Units Forecast, by Country 2020 & 2033

- Table 33: East Europe Battery Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 34: East Europe Battery Industry Volume K Units Forecast, by Type 2020 & 2033

- Table 35: East Europe Battery Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 36: East Europe Battery Industry Volume K Units Forecast, by Technology 2020 & 2033

- Table 37: East Europe Battery Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 38: East Europe Battery Industry Volume K Units Forecast, by Application 2020 & 2033

- Table 39: East Europe Battery Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 40: East Europe Battery Industry Volume K Units Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the East Europe Battery Industry?

The projected CAGR is approximately 10.28%.

2. Which companies are prominent players in the East Europe Battery Industry?

Key companies in the market include VARTA Microbattery GmbH, Mutlu Holding, AKTEX Inc, Zavod AIT, RUSNANO Group, EAS Batteries GmbH, Duracell Inc*List Not Exhaustive, CEZ as (CEZ Group), Contemporary Amperex Technology Co Ltd.

3. What are the main segments of the East Europe Battery Industry?

The market segments include Type, Technology, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 30.4 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Favorable Government Policies4.; Reduced Cost of Solar Energy Systems.

6. What are the notable trends driving market growth?

Lithium-ion Batteries Expected to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Lack of Financing Options Coupled with Difficulties in Integrating Residential Solar PV Systems in Regions like Africa.

8. Can you provide examples of recent developments in the market?

December 2022: the Romanian government allocated USD 108.6 million grant to support investments in battery energy storage systems and deliver at least 240 MW/480 MWh by 2025. The grants will be allocated for purchasing system components and equipment for the construction of new battery projects, as well as the construction of the BESS facilities.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Units.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "East Europe Battery Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the East Europe Battery Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the East Europe Battery Industry?

To stay informed about further developments, trends, and reports in the East Europe Battery Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence