Key Insights

Japan's data center construction market is projected for significant expansion, with an estimated market size of 7.5 billion by 2025. The market is anticipated to grow at a Compound Annual Growth Rate (CAGR) of 6.54% from the base year 2025 through 2033. This growth is propelled by widespread digital transformation initiatives, driving demand for scalable data infrastructure. Key growth factors include the increasing adoption of cloud computing, big data analytics, and the proliferation of Internet of Things (IoT) devices. Japan's position as a technology leader and government support for the digital economy further foster data center investment. The market shows a strong emphasis on electrical infrastructure, particularly power distribution units (PDUs) and switchgear, complemented by essential backup solutions like uninterruptible power supplies (UPS) and generators for continuous operations.

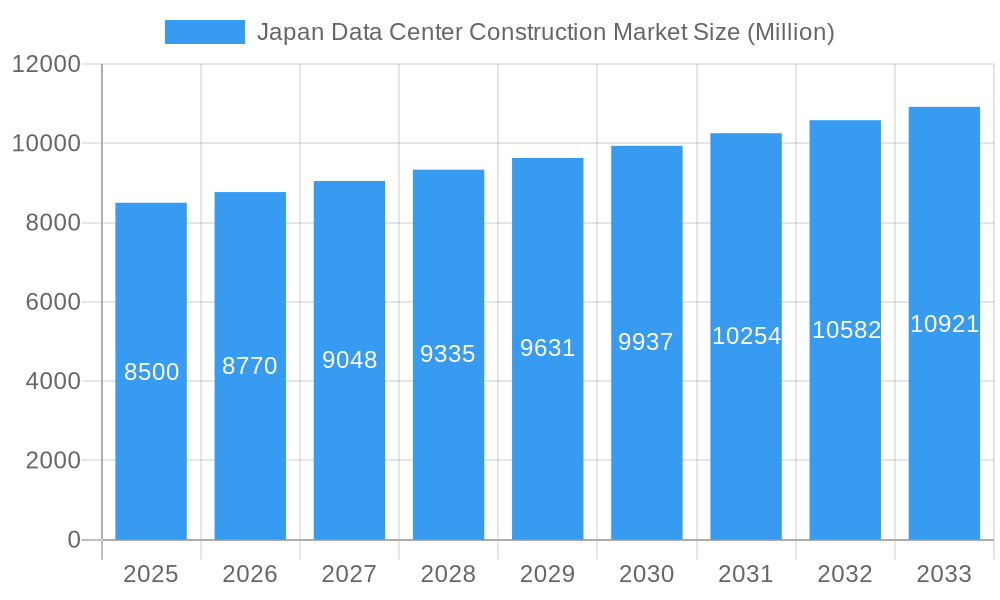

Japan Data Center Construction Market Market Size (In Billion)

The mechanical infrastructure segment is also expanding, with advanced cooling systems such as immersion cooling and direct-to-chip solutions becoming crucial for managing heat in high-density computing environments. Data centers with Tier-III and Tier-IV classifications, offering enhanced availability and redundancy, are in high demand from enterprises with mission-critical operations. The Information Technology (IT) and Telecommunications sectors, along with Banking, Financial Services, and Insurance (BFSI) and Government & Defense, are the leading end-users. Prominent market players, including Schneider Electric SE, NTT Ltd, and AECOM, are driving innovation and project execution. Challenges include substantial initial capital investment, strict regulatory compliance, and the ongoing difficulty in securing suitable land with reliable power and network connectivity.

Japan Data Center Construction Market Company Market Share

This comprehensive market analysis provides an in-depth examination of the Japan Data Center Construction Market, a vital sector influenced by escalating digital transformation and the growing need for advanced IT infrastructure. The report explores market dynamics, growth trajectories, segmentation, product advancements, key industry participants, and future prospects within this rapidly evolving landscape. The analysis covers the period from 2019 to 2033, with a base year of 2025, offering a robust outlook for investors and stakeholders. All financial figures are presented in billions.

Japan Data Center Construction Market Market Dynamics & Structure

The Japan Data Center Construction Market is characterized by a moderate to high level of market concentration, with a few key players dominating significant portions of the construction and infrastructure supply chain. Technological innovation is a primary driver, fueled by the increasing adoption of AI, IoT, and cloud computing, necessitating more sophisticated and energy-efficient data center designs. Regulatory frameworks, while generally supportive of digital infrastructure development, include stringent environmental and seismic safety standards that influence construction methodologies and material choices. Competitive product substitutes are emerging, particularly in areas like modular data center solutions and advanced cooling technologies, offering alternatives to traditional build-outs. End-user demographics are diverse, with significant demand from IT and Telecommunications, BFSI, and Government sectors, each with unique infrastructure requirements. Mergers and acquisitions (M&A) trends indicate strategic consolidation, with larger construction firms acquiring specialized providers to enhance their service offerings and expand their market reach.

- Market Concentration: Dominated by major construction firms and specialized infrastructure providers, with growing influence of hyperscale cloud providers.

- Technological Innovation Drivers: AI/ML integration, 5G deployment, edge computing, and sustainable construction practices.

- Regulatory Frameworks: Strict seismic resilience, energy efficiency mandates (e.g., PUE targets), and data localization policies.

- Competitive Product Substitutes: Modular data centers, liquid cooling solutions, and advanced power management systems.

- End-User Demographics: IT & Telecommunications (XX% market share), BFSI (XX% market share), Government & Defense (XX% market share), Healthcare (XX% market share).

- M&A Trends: Acquisition of specialized engineering firms, strategic alliances for technology integration, and expansion into new regions within Japan.

Japan Data Center Construction Market Growth Trends & Insights

The Japan Data Center Construction Market is projected for substantial growth, driven by the relentless expansion of digital services and the increasing data processing needs of enterprises across various sectors. The market size is expected to witness a Compound Annual Growth Rate (CAGR) of approximately 8.5% during the forecast period, escalating from an estimated XX,XXX million in 2025 to XX,XXX million by 2033. This growth trajectory is underpinned by factors such as Japan's advanced technological ecosystem, government initiatives promoting digital transformation, and a strong domestic demand for high-performance computing and cloud services. The adoption of cutting-edge technologies like AI and IoT necessitates the construction of more powerful and resilient data centers, with a particular emphasis on high-density computing and advanced cooling solutions.

Consumer behavior shifts are also playing a pivotal role, with businesses increasingly prioritizing colocation and managed services to optimize their IT infrastructure investments. This trend fuels demand for hyperscale and enterprise-grade data centers capable of supporting these services. Furthermore, the ongoing digital transformation across industries such as finance, healthcare, and manufacturing is creating a sustained need for new data center capacity. The market's evolution is also marked by a growing preference for sustainable and energy-efficient designs, influencing the choice of construction materials, power systems, and cooling technologies. The increasing prevalence of hybrid cloud strategies is further augmenting the demand for flexible and scalable data center solutions that can accommodate both on-premise and off-premise workloads.

- Market Size Evolution: Projected to grow from XX,XXX million in 2025 to XX,XXX million by 2033.

- CAGR: Approximately 8.5% during the forecast period (2025-2033).

- Adoption Rates: High adoption of cloud services, AI, and IoT driving demand for new data center capacity.

- Technological Disruptions: Emergence of liquid cooling, AI-driven infrastructure management, and edge computing solutions.

- Consumer Behavior Shifts: Increased demand for colocation, managed services, and hybrid cloud solutions.

- Market Penetration: Estimated XX% penetration for hyperscale data centers, with steady growth in enterprise and edge deployments.

Dominant Regions, Countries, or Segments in Japan Data Center Construction Market

Within the Japan Data Center Construction Market, the IT and Telecommunications segment stands out as the dominant force driving growth, attributed to the continuous demand for cloud computing services, 5G infrastructure expansion, and the increasing digitalization of business operations. This segment consistently requires the deployment of new data centers and the expansion of existing facilities to accommodate ever-growing data volumes and processing power. The infrastructure segment also plays a crucial role, with Electrical Infrastructure, particularly Power Distribution Solutions, exhibiting significant market share due to the fundamental need for reliable and efficient power management.

The Tier-III data center category is experiencing robust demand, balancing availability and maintainability to meet the critical uptime requirements of many businesses, especially within the BFSI and IT sectors. Geographically, major metropolitan areas like Tokyo continue to lead in data center construction due to their established connectivity, access to skilled labor, and proximity to a large concentration of end-users.

- Dominant End User Segment: IT and Telecommunications, accounting for an estimated XX% of the market in 2025.

- Key Drivers: Cloud service expansion, 5G network build-out, and enterprise digitalization initiatives.

- Dominant Infrastructure Sub-Segment (Electrical): Power Distribution Solutions, including PDU (Basic & Smart - Metered & Switched Solutions) and Transfer Switches (Automatic (ATS)), vital for uninterrupted operations.

- Market Share: XX% of the electrical infrastructure market.

- Dominant Tier Type: Tier-III, offering a balance of redundancy and maintainability, crucial for business continuity.

- Growth Potential: Expected CAGR of XX% in this tier segment.

- Dominant Geographic Hub: Tokyo metropolitan area, benefiting from existing infrastructure and high concentration of businesses.

- Investment: Significant capital expenditure from both domestic and international players in this region.

Japan Data Center Construction Market Product Landscape

The Japan Data Center Construction Market is witnessing a rapid evolution in its product landscape, with a strong emphasis on efficiency, reliability, and sustainability. Innovations in Electrical Infrastructure include advanced Power Distribution Solutions such as smart PDUs offering granular monitoring and control, and highly reliable automatic transfer switches (ATS) ensuring seamless power transition. In Power Back-up Solutions, high-efficiency UPS systems and advanced generator technologies are being deployed to guarantee continuous operation. For Mechanical Infrastructure, the focus is shifting towards energy-efficient Cooling Systems. While traditional In-row and In-rack cooling remain prevalent, cutting-edge solutions like Immersion Cooling and Direct-to-Chip Cooling are gaining traction for high-density computing environments. These advancements enable data centers to handle increasing heat loads more effectively, reducing operational costs and environmental impact.

Key Drivers, Barriers & Challenges in Japan Data Center Construction Market

Key Drivers: The Japan Data Center Construction Market is propelled by several powerful forces. The relentless digital transformation across industries, fueled by AI, IoT, and big data analytics, creates an insatiable demand for more sophisticated and expansive data center facilities. Government initiatives promoting digital infrastructure development and innovation, coupled with Japan's status as a global technology leader, provide a fertile ground for growth. Furthermore, the increasing adoption of cloud computing and hybrid IT strategies by businesses necessitates robust and scalable data center solutions. Strategic investments by hyperscale cloud providers to expand their presence in Japan are also a significant growth accelerator.

Barriers & Challenges: Despite the promising outlook, the market faces notable challenges. High land acquisition costs, particularly in prime urban locations like Tokyo, can significantly inflate project expenses. Stringent environmental regulations and the increasing demand for sustainable construction practices require significant investment in eco-friendly technologies and materials. The availability of skilled labor for specialized construction and maintenance tasks can also pose a constraint. Supply chain disruptions for critical components, exacerbated by global events, can lead to project delays and cost overruns. Competitive pressures among construction firms and infrastructure providers also necessitate continuous innovation and cost-efficiency.

Emerging Opportunities in Japan Data Center Construction Market

Emerging opportunities in the Japan Data Center Construction Market are diverse and significant. The growing adoption of edge computing presents a substantial opportunity for the development of smaller, distributed data centers closer to end-users, catering to low-latency applications such as autonomous driving and smart cities. The increasing demand for specialized data centers for AI training and high-performance computing (HPC) is another key area, requiring advanced cooling and power solutions. Furthermore, the market is ripe for innovations in sustainable data center construction, including the integration of renewable energy sources and advanced waste heat recovery systems. The growing healthcare sector's need for secure and compliant data storage also opens avenues for specialized healthcare data center development.

Growth Accelerators in the Japan Data Center Construction Market Industry

Several catalysts are accelerating the long-term growth of the Japan Data Center Construction Market. Technological breakthroughs in areas like artificial intelligence for infrastructure management and predictive maintenance are enhancing operational efficiency and reducing downtime. Strategic partnerships between construction firms, technology providers, and colocation operators are facilitating the development of integrated solutions and expanding market reach. The increasing global interest in Japan as a stable and technologically advanced market is attracting foreign investment, further stimulating new project developments. Continuous government support for digitalization and the development of smart city initiatives are also expected to drive sustained demand for data center infrastructure.

Key Players Shaping the Japan Data Center Construction Market Market

- SAS Institute Inc

- Fortis Construction

- Daiwa House Industry Co Ltd

- Hutchinson Builders

- Kienta Engineering Construction

- DSCO Group

- IBM Corporation

- GIGA-BYTE Technology Co Ltd

- Sato Kogyo (S) Pte Ltd

- Nakano Corporation

- Schneider Electric SE

- Turner Construction Co

- Hensel Phelps Construction Co Inc

- Obayashi Corporation

- CSF Group

- HIBIYA ENGINEERING Ltd

- Cummins Inc

- AECOM

- NTT Ltd

Notable Milestones in Japan Data Center Construction Market Sector

- November 2022: Equinix announced its 15th international business exchange (IBX) data center in Tokyo, Japan, with an initial investment of USD 115 million. The new data center, TY15, is expected to provide an initial capacity of approximately 1,200 cabinets, scaling to 3,700 cabinets when fully built out, signifying substantial growth opportunities for vendors.

- September 2022: NTT Corporation announced an investment of approximately YEN 40 billion through NTT Global Data Centers Corporation to build a new "Keihanna Data Center" in Kyoto Prefecture. This 4-story facility will offer 30 MW of IT load capacity across 10,900 sqm of server room space, equivalent to 4,800 racks, presenting significant opportunities for market participants.

In-Depth Japan Data Center Construction Market Market Outlook

The Japan Data Center Construction Market is poised for a dynamic future, driven by an unwavering demand for digital infrastructure. The continuous integration of advanced technologies like AI and 5G will necessitate the construction of more powerful, energy-efficient, and resilient data centers. Emerging trends such as edge computing and the expansion of specialized HPC facilities present significant avenues for growth. Strategic investments by major players, coupled with government support for digitalization, are expected to create a robust market environment. The focus on sustainability and advanced cooling solutions will shape future construction methodologies, offering opportunities for innovative solutions and eco-friendly practices. The market's outlook remains highly positive, with substantial potential for further expansion and technological advancement.

Japan Data Center Construction Market Segmentation

-

1. Market Segmentation

-

1.1. By Infrastructure

-

1.1.1. By Electrical Infrastructure

-

1.1.1.1. Power Distribution Solutions

- 1.1.1.1.1. PDU - Basic & Smart - Metered & Switched Solutions

-

1.1.1.1.2. Transfer Switches

- 1.1.1.1.2.1. Static

- 1.1.1.1.2.2. Automatic (ATS)

-

1.1.1.1.3. Switchgear

- 1.1.1.1.3.1. Low-voltage

- 1.1.1.1.3.2. Medium-voltage

- 1.1.1.1.4. Power Panels and Components

- 1.1.1.1.5. Other Power Distribution Solutions

-

1.1.1.2. Power Back-up Solutions

- 1.1.1.2.1. UPS

- 1.1.1.2.2. Generators

- 1.1.1.3. Service

-

1.1.1.1. Power Distribution Solutions

-

1.1.2. By Mechanical Infrastructure

-

1.1.2.1. Cooling Systems

- 1.1.2.1.1. Immersion Cooling

- 1.1.2.1.2. Direct-to-Chip Cooling

- 1.1.2.1.3. Rear Door Heat Exchanger

- 1.1.2.1.4. In-row and In-rack Cooling

- 1.1.2.1.5. Racks

- 1.1.2.1.6. Other Mechanical Infrastructure

-

1.1.2.1. Cooling Systems

- 1.1.3. General Construction

-

1.1.1. By Electrical Infrastructure

-

1.2. By Tier Type

- 1.2.1. Tier-I and II

- 1.2.2. Tier-III

- 1.2.3. Tier-IV

-

1.3. By End User

- 1.3.1. Banking, Financial Services, and Insurance

- 1.3.2. IT and Telecommunications

- 1.3.3. Government and Defense

- 1.3.4. Healthcare

- 1.3.5. Other End Users

-

1.1. By Infrastructure

-

2. Infrastructure

-

2.1. By Electrical Infrastructure

-

2.1.1. Power Distribution Solutions

- 2.1.1.1. PDU - Basic & Smart - Metered & Switched Solutions

-

2.1.1.2. Transfer Switches

- 2.1.1.2.1. Static

- 2.1.1.2.2. Automatic (ATS)

-

2.1.1.3. Switchgear

- 2.1.1.3.1. Low-voltage

- 2.1.1.3.2. Medium-voltage

- 2.1.1.4. Power Panels and Components

- 2.1.1.5. Other Power Distribution Solutions

-

2.1.2. Power Back-up Solutions

- 2.1.2.1. UPS

- 2.1.2.2. Generators

- 2.1.3. Service

-

2.1.1. Power Distribution Solutions

-

2.2. By Mechanical Infrastructure

-

2.2.1. Cooling Systems

- 2.2.1.1. Immersion Cooling

- 2.2.1.2. Direct-to-Chip Cooling

- 2.2.1.3. Rear Door Heat Exchanger

- 2.2.1.4. In-row and In-rack Cooling

- 2.2.1.5. Racks

- 2.2.1.6. Other Mechanical Infrastructure

-

2.2.1. Cooling Systems

- 2.3. General Construction

-

2.1. By Electrical Infrastructure

-

3. Tier Type

- 3.1. Tier-I and II

- 3.2. Tier-III

- 3.3. Tier-IV

-

4. End User

- 4.1. Banking, Financial Services, and Insurance

- 4.2. IT and Telecommunications

- 4.3. Government and Defense

- 4.4. Healthcare

- 4.5. Other End Users

Japan Data Center Construction Market Segmentation By Geography

- 1. Japan

Japan Data Center Construction Market Regional Market Share

Geographic Coverage of Japan Data Center Construction Market

Japan Data Center Construction Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.54% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Growing E-commerce and Hi-tech industries driving the DC construction in the country; Major initiatives undertaken by government to promote digital economy and connectivity infrastructure

- 3.3. Market Restrains

- 3.3.1. High Power Consumption and emission contribution of Data Centers

- 3.4. Market Trends

- 3.4.1. Tier 3 is the largest Tier Type

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Japan Data Center Construction Market Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Market Segmentation

- 5.1.1. By Infrastructure

- 5.1.1.1. By Electrical Infrastructure

- 5.1.1.1.1. Power Distribution Solutions

- 5.1.1.1.1.1. PDU - Basic & Smart - Metered & Switched Solutions

- 5.1.1.1.1.2. Transfer Switches

- 5.1.1.1.1.2.1. Static

- 5.1.1.1.1.2.2. Automatic (ATS)

- 5.1.1.1.1.3. Switchgear

- 5.1.1.1.1.3.1. Low-voltage

- 5.1.1.1.1.3.2. Medium-voltage

- 5.1.1.1.1.4. Power Panels and Components

- 5.1.1.1.1.5. Other Power Distribution Solutions

- 5.1.1.1.2. Power Back-up Solutions

- 5.1.1.1.2.1. UPS

- 5.1.1.1.2.2. Generators

- 5.1.1.1.3. Service

- 5.1.1.1.1. Power Distribution Solutions

- 5.1.1.2. By Mechanical Infrastructure

- 5.1.1.2.1. Cooling Systems

- 5.1.1.2.1.1. Immersion Cooling

- 5.1.1.2.1.2. Direct-to-Chip Cooling

- 5.1.1.2.1.3. Rear Door Heat Exchanger

- 5.1.1.2.1.4. In-row and In-rack Cooling

- 5.1.1.2.1.5. Racks

- 5.1.1.2.1.6. Other Mechanical Infrastructure

- 5.1.1.2.1. Cooling Systems

- 5.1.1.3. General Construction

- 5.1.1.1. By Electrical Infrastructure

- 5.1.2. By Tier Type

- 5.1.2.1. Tier-I and II

- 5.1.2.2. Tier-III

- 5.1.2.3. Tier-IV

- 5.1.3. By End User

- 5.1.3.1. Banking, Financial Services, and Insurance

- 5.1.3.2. IT and Telecommunications

- 5.1.3.3. Government and Defense

- 5.1.3.4. Healthcare

- 5.1.3.5. Other End Users

- 5.1.1. By Infrastructure

- 5.2. Market Analysis, Insights and Forecast - by Infrastructure

- 5.2.1. By Electrical Infrastructure

- 5.2.1.1. Power Distribution Solutions

- 5.2.1.1.1. PDU - Basic & Smart - Metered & Switched Solutions

- 5.2.1.1.2. Transfer Switches

- 5.2.1.1.2.1. Static

- 5.2.1.1.2.2. Automatic (ATS)

- 5.2.1.1.3. Switchgear

- 5.2.1.1.3.1. Low-voltage

- 5.2.1.1.3.2. Medium-voltage

- 5.2.1.1.4. Power Panels and Components

- 5.2.1.1.5. Other Power Distribution Solutions

- 5.2.1.2. Power Back-up Solutions

- 5.2.1.2.1. UPS

- 5.2.1.2.2. Generators

- 5.2.1.3. Service

- 5.2.1.1. Power Distribution Solutions

- 5.2.2. By Mechanical Infrastructure

- 5.2.2.1. Cooling Systems

- 5.2.2.1.1. Immersion Cooling

- 5.2.2.1.2. Direct-to-Chip Cooling

- 5.2.2.1.3. Rear Door Heat Exchanger

- 5.2.2.1.4. In-row and In-rack Cooling

- 5.2.2.1.5. Racks

- 5.2.2.1.6. Other Mechanical Infrastructure

- 5.2.2.1. Cooling Systems

- 5.2.3. General Construction

- 5.2.1. By Electrical Infrastructure

- 5.3. Market Analysis, Insights and Forecast - by Tier Type

- 5.3.1. Tier-I and II

- 5.3.2. Tier-III

- 5.3.3. Tier-IV

- 5.4. Market Analysis, Insights and Forecast - by End User

- 5.4.1. Banking, Financial Services, and Insurance

- 5.4.2. IT and Telecommunications

- 5.4.3. Government and Defense

- 5.4.4. Healthcare

- 5.4.5. Other End Users

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. Japan

- 5.1. Market Analysis, Insights and Forecast - by Market Segmentation

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 SAS Institute Inc

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Fortis Construction

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Daiwa House Industry Co Ltd

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Hutchinson Builders

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Kienta Engineering Construction

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 DSCO Group

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 IBM Corporation

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 GIGA-BYTE Technology Co Ltd

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Sato Kogyo (S) Pte Ltd

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Nakano Corporation

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 Schneider Electric SE

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.12 Turner Construction Co

- 6.2.12.1. Overview

- 6.2.12.2. Products

- 6.2.12.3. SWOT Analysis

- 6.2.12.4. Recent Developments

- 6.2.12.5. Financials (Based on Availability)

- 6.2.13 Hensel Phelps Construction Co Inc

- 6.2.13.1. Overview

- 6.2.13.2. Products

- 6.2.13.3. SWOT Analysis

- 6.2.13.4. Recent Developments

- 6.2.13.5. Financials (Based on Availability)

- 6.2.14 Obayashi Corporation

- 6.2.14.1. Overview

- 6.2.14.2. Products

- 6.2.14.3. SWOT Analysis

- 6.2.14.4. Recent Developments

- 6.2.14.5. Financials (Based on Availability)

- 6.2.15 CSF Group

- 6.2.15.1. Overview

- 6.2.15.2. Products

- 6.2.15.3. SWOT Analysis

- 6.2.15.4. Recent Developments

- 6.2.15.5. Financials (Based on Availability)

- 6.2.16 HIBIYA ENGINEERINGLtd

- 6.2.16.1. Overview

- 6.2.16.2. Products

- 6.2.16.3. SWOT Analysis

- 6.2.16.4. Recent Developments

- 6.2.16.5. Financials (Based on Availability)

- 6.2.17 Cummins Inc

- 6.2.17.1. Overview

- 6.2.17.2. Products

- 6.2.17.3. SWOT Analysis

- 6.2.17.4. Recent Developments

- 6.2.17.5. Financials (Based on Availability)

- 6.2.18 AECOM

- 6.2.18.1. Overview

- 6.2.18.2. Products

- 6.2.18.3. SWOT Analysis

- 6.2.18.4. Recent Developments

- 6.2.18.5. Financials (Based on Availability)

- 6.2.19 NTT Ltd

- 6.2.19.1. Overview

- 6.2.19.2. Products

- 6.2.19.3. SWOT Analysis

- 6.2.19.4. Recent Developments

- 6.2.19.5. Financials (Based on Availability)

- 6.2.1 SAS Institute Inc

List of Figures

- Figure 1: Japan Data Center Construction Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Japan Data Center Construction Market Share (%) by Company 2025

List of Tables

- Table 1: Japan Data Center Construction Market Revenue billion Forecast, by Market Segmentation 2020 & 2033

- Table 2: Japan Data Center Construction Market Volume K Unit Forecast, by Market Segmentation 2020 & 2033

- Table 3: Japan Data Center Construction Market Revenue billion Forecast, by Infrastructure 2020 & 2033

- Table 4: Japan Data Center Construction Market Volume K Unit Forecast, by Infrastructure 2020 & 2033

- Table 5: Japan Data Center Construction Market Revenue billion Forecast, by Tier Type 2020 & 2033

- Table 6: Japan Data Center Construction Market Volume K Unit Forecast, by Tier Type 2020 & 2033

- Table 7: Japan Data Center Construction Market Revenue billion Forecast, by End User 2020 & 2033

- Table 8: Japan Data Center Construction Market Volume K Unit Forecast, by End User 2020 & 2033

- Table 9: Japan Data Center Construction Market Revenue billion Forecast, by Region 2020 & 2033

- Table 10: Japan Data Center Construction Market Volume K Unit Forecast, by Region 2020 & 2033

- Table 11: Japan Data Center Construction Market Revenue billion Forecast, by Market Segmentation 2020 & 2033

- Table 12: Japan Data Center Construction Market Volume K Unit Forecast, by Market Segmentation 2020 & 2033

- Table 13: Japan Data Center Construction Market Revenue billion Forecast, by Infrastructure 2020 & 2033

- Table 14: Japan Data Center Construction Market Volume K Unit Forecast, by Infrastructure 2020 & 2033

- Table 15: Japan Data Center Construction Market Revenue billion Forecast, by Tier Type 2020 & 2033

- Table 16: Japan Data Center Construction Market Volume K Unit Forecast, by Tier Type 2020 & 2033

- Table 17: Japan Data Center Construction Market Revenue billion Forecast, by End User 2020 & 2033

- Table 18: Japan Data Center Construction Market Volume K Unit Forecast, by End User 2020 & 2033

- Table 19: Japan Data Center Construction Market Revenue billion Forecast, by Country 2020 & 2033

- Table 20: Japan Data Center Construction Market Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Japan Data Center Construction Market?

The projected CAGR is approximately 6.54%.

2. Which companies are prominent players in the Japan Data Center Construction Market?

Key companies in the market include SAS Institute Inc, Fortis Construction, Daiwa House Industry Co Ltd, Hutchinson Builders, Kienta Engineering Construction, DSCO Group, IBM Corporation, GIGA-BYTE Technology Co Ltd, Sato Kogyo (S) Pte Ltd, Nakano Corporation, Schneider Electric SE, Turner Construction Co, Hensel Phelps Construction Co Inc, Obayashi Corporation, CSF Group, HIBIYA ENGINEERINGLtd, Cummins Inc, AECOM, NTT Ltd.

3. What are the main segments of the Japan Data Center Construction Market?

The market segments include Market Segmentation, Infrastructure, Tier Type, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 7.5 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing E-commerce and Hi-tech industries driving the DC construction in the country; Major initiatives undertaken by government to promote digital economy and connectivity infrastructure.

6. What are the notable trends driving market growth?

Tier 3 is the largest Tier Type.

7. Are there any restraints impacting market growth?

High Power Consumption and emission contribution of Data Centers.

8. Can you provide examples of recent developments in the market?

November 2022: Equinix announced its 15th international business exchange (IBX) data center in Tokyo, Japan. The company said that it had made an initial investment of USD 115 million on the new data center, touted TY15. The first phase of TY15 is expected to provide an initial capacity of approximately 1,200 cabinets and 3,700 cabinets when fully built out. Such investments provide opportunities for the vendors in the market.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Japan Data Center Construction Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Japan Data Center Construction Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Japan Data Center Construction Market?

To stay informed about further developments, trends, and reports in the Japan Data Center Construction Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence