Key Insights

The European temperature sensor market is projected for substantial growth, with an estimated market size of $7.43 billion by 2025, exhibiting a CAGR of 3.8%. This expansion is propelled by rising demand across diverse end-user industries. Key sectors like chemical, petrochemical, oil, and gas require precise temperature monitoring for safety and process optimization. The automotive sector's adoption of ADAS and EVs, along with the power generation industry's focus on efficiency and renewables, also drives demand for sophisticated temperature sensors. Emerging applications in medical devices and consumer electronics further broaden market opportunities.

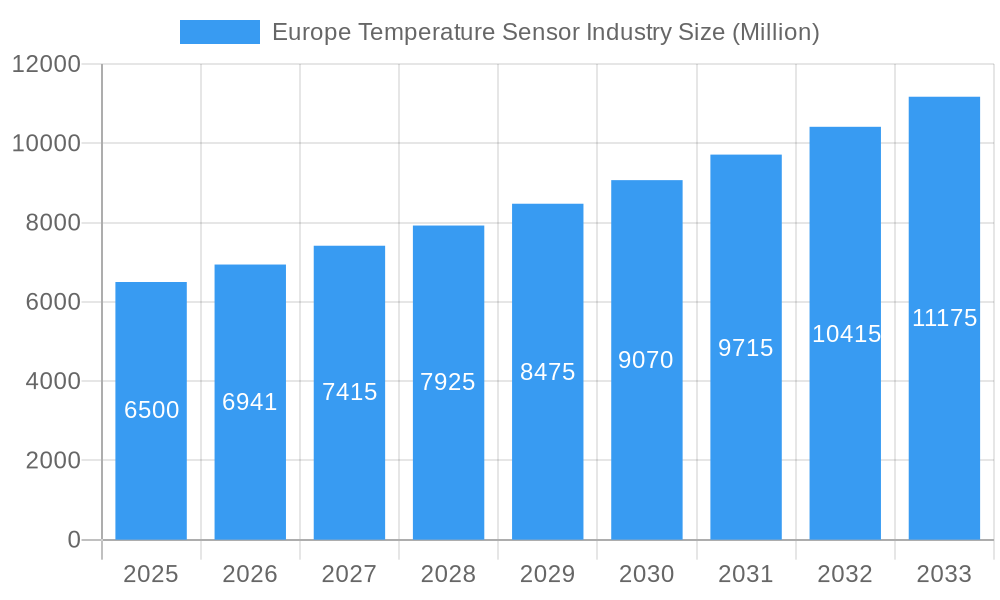

Europe Temperature Sensor Industry Market Size (In Billion)

Technological innovation is a significant market driver. Wireless sensor solutions are gaining traction for their flexibility. Thermistors and RTDs remain dominant due to their accuracy and cost-effectiveness, while thermocouples are increasingly adopted for high-temperature and harsh environments. Fiber optic temperature sensors are also emerging for extreme conditions. Leading companies like Honeywell, ABB, Siemens, and Emerson are investing in R&D for smart sensors with predictive maintenance and remote monitoring capabilities.

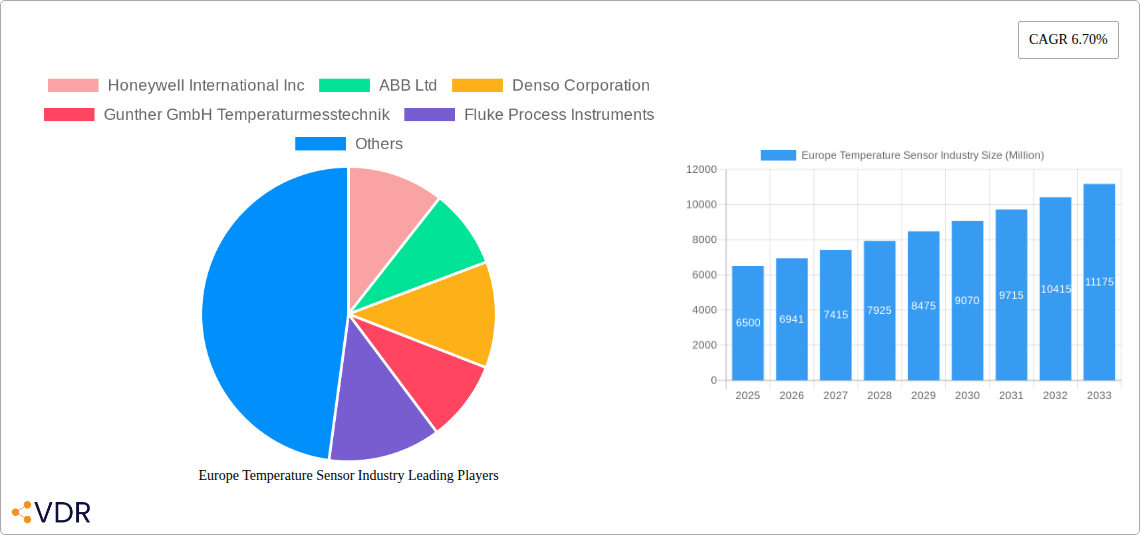

Europe Temperature Sensor Industry Company Market Share

This report offers a comprehensive analysis of the European temperature sensor market from 2019 to 2033, with a base year of 2025. It provides critical insights into market structure, growth, and future outlook, analyzing key segments, regions, and influential players.

Europe Temperature Sensor Industry Market Dynamics & Structure

The European temperature sensor market is characterized by a moderate to high level of concentration, driven by technological innovation and stringent regulatory frameworks. Key players like Honeywell International Inc, Siemens AG, and TE Connectivity Ltd dominate significant market shares, often through strategic acquisitions and continuous product development. The adoption of advanced sensing technologies, such as MEMS-based thermistors and sophisticated wireless sensors, is a primary driver of market evolution. Regulatory compliance, particularly in the automotive, medical, and industrial sectors, mandates high accuracy and reliability, fostering innovation in product design and manufacturing processes. Competitive product substitutes, while present, often struggle to match the integrated performance and reliability offered by established temperature sensor solutions. End-user demographics are increasingly shifting towards demand for smart, connected devices and Industry 4.0 applications, pushing manufacturers to develop interoperable and data-rich sensor solutions. Mergers and acquisitions remain a vital strategy for market consolidation and technological advancement, enabling companies to expand their product portfolios and geographical reach.

- Market Concentration: Moderate to High, with a few key players holding substantial market share.

- Technological Innovation Drivers: Demand for higher accuracy, miniaturization, wireless connectivity, and integration with IoT ecosystems.

- Regulatory Frameworks: Strict standards in automotive (e.g., ECE regulations), medical devices (e.g., MDR), and industrial automation (e.g., ATEX) necessitate advanced, reliable, and certified temperature sensors.

- Competitive Product Substitutes: While alternative measurement methods exist, dedicated temperature sensors offer superior precision, speed, and integration capabilities.

- End-User Demographics: Growing demand from automation, smart cities, advanced healthcare, and the burgeoning electric vehicle market.

- M&A Trends: Ongoing consolidation to gain market share, acquire new technologies, and expand product offerings.

Europe Temperature Sensor Industry Growth Trends & Insights

The European temperature sensor market is poised for robust growth, driven by widespread industrial automation, the burgeoning automotive sector, and the increasing integration of IoT devices across various applications. The market is projected to expand significantly, with a compound annual growth rate (CAGR) of approximately 6.5% during the forecast period of 2025-2033. This growth is fueled by the relentless pursuit of efficiency, safety, and advanced functionality in industrial processes, healthcare, and consumer electronics. The adoption of wireless temperature sensors is accelerating due to their ease of installation and flexibility, particularly in retrofitting older infrastructure and in challenging environments. Technological disruptions, such as the development of more sensitive and cost-effective infrared and fiber optic sensors, are opening up new application areas. Consumer behavior is increasingly influenced by the demand for personalized health monitoring devices and smart home technology, both of which rely heavily on accurate and continuous temperature sensing. The shift towards electrification in the automotive industry, coupled with advancements in electric vehicle battery management systems, represents a substantial growth avenue for high-performance temperature sensors.

- Market Size Evolution: The Europe temperature sensor market, valued at approximately $3,500 million units in 2024, is projected to reach over $6,000 million units by 2033.

- Adoption Rates: High adoption rates in industrial automation and automotive sectors, with significant growth potential in medical and consumer electronics.

- Technological Disruptions: Emergence of advanced materials for thermistors, improved infrared sensor resolution, and enhanced wireless communication protocols for sensor networks.

- Consumer Behavior Shifts: Increased demand for wearable health trackers, smart home appliances, and connected industrial equipment necessitates accurate and reliable temperature monitoring.

- Market Penetration: Expected to reach over 75% penetration across key industrial and automotive applications by 2033.

Dominant Regions, Countries, or Segments in Europe Temperature Sensor Industry

Germany stands as the dominant country within the European temperature sensor market, driven by its strong automotive manufacturing base, advanced industrial automation sector, and significant investment in research and development. The Automotive end-user industry is a primary growth engine, fueled by the increasing demand for electric vehicles (EVs), advanced driver-assistance systems (ADAS), and stringent thermal management requirements in modern vehicles. Germany's robust automotive supply chain, with leading manufacturers and component suppliers, ensures a high and consistent demand for various types of temperature sensors, including RTDs, thermistors, and infrared sensors for engine management, cabin climate control, and battery monitoring.

Beyond Germany, other key regions contributing to market growth include France, the UK, and the Nordic countries, each with their unique drivers. France, with its strong presence in aerospace and medical technology, contributes significantly to the demand for high-precision and reliable temperature sensors. The UK's growing focus on renewable energy and industrial digitalization further bolsters its market share. The Nordic countries, particularly Sweden and Denmark, are leading in smart grid development and sustainable energy solutions, creating a demand for robust temperature sensors in power generation and distribution infrastructure.

Within the technology segments, Resistance Temperature Detectors (RTDs) and Thermistors continue to hold substantial market share due to their accuracy, reliability, and cost-effectiveness in a wide range of industrial and automotive applications. However, Wireless temperature sensors are experiencing the fastest growth rate, driven by the expanding IoT ecosystem, the need for remote monitoring, and the simplification of installation in complex or hard-to-reach areas. The Chemical & Petrochemical and Power Generation industries are also significant contributors, requiring specialized temperature sensors for process control, safety monitoring, and equipment diagnostics in harsh environments. The growing emphasis on energy efficiency and predictive maintenance in these sectors further propels the demand for advanced temperature sensing solutions.

- Dominant Country: Germany, driven by its automotive and industrial sectors.

- Key End-User Industries:

- Automotive: Electric vehicle thermal management, ADAS, engine control.

- Chemical & Petrochemical: Process control, safety monitoring, feedstock management.

- Power Generation: Renewable energy monitoring, grid stability, equipment diagnostics.

- Dominant Technologies:

- Resistance Temperature Detector (RTD): High accuracy and stability for critical applications.

- Thermistor: Cost-effective and versatile for a broad range of temperature monitoring.

- Fastest Growing Segments:

- Wireless Sensors: Facilitating IoT integration and remote monitoring.

- Infrared Sensors: Growing application in non-contact temperature measurement and thermal imaging.

Europe Temperature Sensor Industry Product Landscape

The European temperature sensor market is characterized by continuous product innovation, focusing on enhanced accuracy, miniaturization, and integration capabilities. Manufacturers are developing advanced solutions such as silicon-based temperature sensors with integrated signal conditioning, offering improved performance and reduced component count. Wireless temperature sensors with extended battery life and enhanced communication protocols (e.g., LoRaWAN, NB-IoT) are gaining traction for remote monitoring and IoT applications. Furthermore, specialized infrared sensors are being developed for non-contact temperature measurement in demanding environments, while fiber optic sensors are finding niche applications requiring immunity to electromagnetic interference. These innovations cater to diverse applications, from precise medical temperature monitoring and advanced automotive thermal management to robust industrial process control and consumer electronics integration. The unique selling propositions often lie in sensor precision, response time, operating temperature range, and seamless integration with existing systems.

Key Drivers, Barriers & Challenges in Europe Temperature Sensor Industry

Key Drivers:

- Industrial Automation & Industry 4.0: The widespread adoption of automation and smart manufacturing processes demands precise and reliable temperature monitoring for process optimization, quality control, and predictive maintenance.

- Automotive Electrification: The surge in electric vehicle production necessitates sophisticated thermal management systems, driving demand for high-performance temperature sensors to monitor battery packs, motors, and power electronics.

- Healthcare Advancements: Growing demand for advanced medical devices, including wearables for health monitoring and precise temperature control in diagnostic equipment, fuels innovation in medical-grade temperature sensors.

- Energy Efficiency Initiatives: Stringent regulations and market demand for energy conservation across industries and buildings are pushing the adoption of temperature sensors for optimized HVAC systems, industrial process control, and smart grid management.

Barriers & Challenges:

- Supply Chain Disruptions: Global supply chain volatility, particularly for critical components and raw materials, can lead to increased lead times and production costs.

- Price Sensitivity in Certain Segments: While advanced features command premium pricing, some segments, especially in consumer electronics, remain price-sensitive, posing a challenge for higher-margin, advanced sensor adoption.

- Cybersecurity Concerns for IoT Sensors: The increasing connectivity of temperature sensors in IoT networks raises cybersecurity concerns, requiring robust security measures to prevent data breaches and system manipulation.

- Intense Competition: A crowded market with both established global players and emerging local manufacturers leads to significant competitive pressure on pricing and product differentiation.

Emerging Opportunities in Europe Temperature Sensor Industry

Emerging opportunities in the Europe temperature sensor industry lie in the burgeoning IoT ecosystem, the continued growth of electric mobility, and the increasing need for remote patient monitoring. The expansion of smart city initiatives presents a significant avenue for sensors in infrastructure management, environmental monitoring, and smart utilities. Furthermore, advancements in AI and machine learning are creating opportunities for predictive analytics powered by highly accurate temperature data, enabling proactive maintenance and optimized performance in industrial settings. The development of novel materials for more resilient and cost-effective sensors also opens doors for applications in extreme environments and emerging markets.

Growth Accelerators in the Europe Temperature Sensor Industry Industry

Several factors are accelerating growth in the Europe temperature sensor industry. The increasing investment in smart grid technologies and renewable energy infrastructure across Europe is creating substantial demand for reliable temperature monitoring solutions. Furthermore, strategic partnerships between sensor manufacturers and technology integrators are fostering the development of comprehensive IoT solutions, enhancing the value proposition for end-users. The growing focus on sustainability and circular economy principles is also indirectly boosting demand for sensors that enable efficient resource management and waste reduction in manufacturing processes. Government incentives and funding for research and development in advanced manufacturing and digital technologies further stimulate innovation and market expansion.

Key Players Shaping the Europe Temperature Sensor Industry Market

- Honeywell International Inc

- ABB Ltd

- Denso Corporation

- Gunther GmbH Temperaturmesstechnik

- Fluke Process Instruments

- NXP Semiconductors NV

- GE Sensing & Inspection Technologies GmbH

- Maxim Integrated Products

- Kongsberg Gruppe

- STMicroelectronics

- Siemens AG

- TE Connectivity Ltd

- Robert Bosch GmbH

- Texas Instruments Incorporated

- Microchip Technology Incorporated

- Analog Devices Inc

- Omron Corporation

- FLIR Systems

- Panasonic Corporation

- Thermometris

- Emerson Electric Company

Notable Milestones in Europe Temperature Sensor Industry Sector

- January 2021: Switzerland-based Sensirion announced that the company, LivingPackets, utilized Sensirion's humidity and temperature sensors in its sustainable packaging solutions. Using the solution called THE BOX, packaging waste is expected to be reduced by over 100 billion deliveries annually. THE BOX consists of highly resistant materials. It can be recycled without a specific limit and can survive almost 1,000 transport trips before reprocessing.

- May 2020: The smart wearables company, GOQii, launched a new smart band featuring sensors for measuring body temperature. It partnered with the German health tech startup, Thryve, to conduct a clinical study to detect COVID-19 infections using the device. The device, Vital 3.0, was developed within two months by the company. It can help users track vitals, like body temperature, heart rate, blood pressure, and sleep, apart from the step count. The thermal sensor allows continuous monitoring and on-demand checking. It has an accuracy of 0.3°F.

In-Depth Europe Temperature Sensor Industry Market Outlook

The Europe temperature sensor industry is set for a period of sustained and accelerated growth, driven by the overarching trends of digitalization, sustainability, and technological advancement. Future market potential lies in the deeper integration of temperature sensors within complex IIoT (Industrial Internet of Things) platforms, enabling sophisticated data analytics and predictive maintenance. The electrification of transportation, alongside advancements in battery technology, will continue to be a significant growth catalyst. Furthermore, the increasing emphasis on personalized healthcare and remote patient monitoring presents a substantial opportunity for highly accurate and reliable medical-grade temperature sensors. Strategic collaborations, technological breakthroughs in sensor materials and wireless communication, and favorable regulatory environments will collectively shape a dynamic and expanding market for temperature sensing solutions across Europe.

Europe Temperature Sensor Industry Segmentation

-

1. Type

- 1.1. Wired

- 1.2. Wireless

-

2. Technology

- 2.1. Infrared

- 2.2. Thermocouple

- 2.3. Resistance Temperature Detector

- 2.4. Thermistor

- 2.5. Temperature Transmitter

- 2.6. Fiber Optic

- 2.7. Others

-

3. End-user Industry

- 3.1. Chemical & Petrochemical

- 3.2. Oil & Gas

- 3.3. Metal & Mining

- 3.4. Power Generation

- 3.5. Food & Beverage

- 3.6. Automotive

- 3.7. Medical

- 3.8. Aerospace & Military

- 3.9. Consumer Electronics

- 3.10. Other End-user Industries

Europe Temperature Sensor Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Temperature Sensor Industry Regional Market Share

Geographic Coverage of Europe Temperature Sensor Industry

Europe Temperature Sensor Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Wired

- 5.1.2. Wireless

- 5.2. Market Analysis, Insights and Forecast - by Technology

- 5.2.1. Infrared

- 5.2.2. Thermocouple

- 5.2.3. Resistance Temperature Detector

- 5.2.4. Thermistor

- 5.2.5. Temperature Transmitter

- 5.2.6. Fiber Optic

- 5.2.7. Others

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. Chemical & Petrochemical

- 5.3.2. Oil & Gas

- 5.3.3. Metal & Mining

- 5.3.4. Power Generation

- 5.3.5. Food & Beverage

- 5.3.6. Automotive

- 5.3.7. Medical

- 5.3.8. Aerospace & Military

- 5.3.9. Consumer Electronics

- 5.3.10. Other End-user Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Europe Temperature Sensor Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Wired

- 6.1.2. Wireless

- 6.2. Market Analysis, Insights and Forecast - by Technology

- 6.2.1. Infrared

- 6.2.2. Thermocouple

- 6.2.3. Resistance Temperature Detector

- 6.2.4. Thermistor

- 6.2.5. Temperature Transmitter

- 6.2.6. Fiber Optic

- 6.2.7. Others

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. Chemical & Petrochemical

- 6.3.2. Oil & Gas

- 6.3.3. Metal & Mining

- 6.3.4. Power Generation

- 6.3.5. Food & Beverage

- 6.3.6. Automotive

- 6.3.7. Medical

- 6.3.8. Aerospace & Military

- 6.3.9. Consumer Electronics

- 6.3.10. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Honeywell International Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 ABB Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Denso Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Gunther GmbH Temperaturmesstechnik

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Fluke Process Instruments

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 NXP Semiconductors NV

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 GE Sensing & Inspection Technologies GmbH

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Maxim Integrated Products

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Kongsberg Gruppe

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 STMicroelectronics

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Siemens AG

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 TE Connectivity Ltd

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Robert Bosch GmbH

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 Texas Instruments Incorporated

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.15 Microchip Technology Incorporated

- 7.1.15.1. Company Overview

- 7.1.15.2. Products

- 7.1.15.3. Company Financials

- 7.1.15.4. SWOT Analysis

- 7.1.16 Analog Devices Inc

- 7.1.16.1. Company Overview

- 7.1.16.2. Products

- 7.1.16.3. Company Financials

- 7.1.16.4. SWOT Analysis

- 7.1.17 Omron Corporatio

- 7.1.17.1. Company Overview

- 7.1.17.2. Products

- 7.1.17.3. Company Financials

- 7.1.17.4. SWOT Analysis

- 7.1.18 FLIR Systems

- 7.1.18.1. Company Overview

- 7.1.18.2. Products

- 7.1.18.3. Company Financials

- 7.1.18.4. SWOT Analysis

- 7.1.19 Panasonic Corporation

- 7.1.19.1. Company Overview

- 7.1.19.2. Products

- 7.1.19.3. Company Financials

- 7.1.19.4. SWOT Analysis

- 7.1.20 Thermometris

- 7.1.20.1. Company Overview

- 7.1.20.2. Products

- 7.1.20.3. Company Financials

- 7.1.20.4. SWOT Analysis

- 7.1.21 Emerson Electric Company

- 7.1.21.1. Company Overview

- 7.1.21.2. Products

- 7.1.21.3. Company Financials

- 7.1.21.4. SWOT Analysis

- 7.1.1 Honeywell International Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Temperature Sensor Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Europe Temperature Sensor Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Temperature Sensor Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Europe Temperature Sensor Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 3: Europe Temperature Sensor Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 4: Europe Temperature Sensor Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Europe Temperature Sensor Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Europe Temperature Sensor Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 7: Europe Temperature Sensor Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 8: Europe Temperature Sensor Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: United Kingdom Europe Temperature Sensor Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Germany Europe Temperature Sensor Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: France Europe Temperature Sensor Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Italy Europe Temperature Sensor Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Spain Europe Temperature Sensor Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Netherlands Europe Temperature Sensor Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Belgium Europe Temperature Sensor Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Sweden Europe Temperature Sensor Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Norway Europe Temperature Sensor Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Poland Europe Temperature Sensor Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Denmark Europe Temperature Sensor Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Temperature Sensor Industry?

The projected CAGR is approximately 3.8%.

2. Which companies are prominent players in the Europe Temperature Sensor Industry?

Key companies in the market include Honeywell International Inc, ABB Ltd, Denso Corporation, Gunther GmbH Temperaturmesstechnik, Fluke Process Instruments, NXP Semiconductors NV, GE Sensing & Inspection Technologies GmbH, Maxim Integrated Products, Kongsberg Gruppe, STMicroelectronics, Siemens AG, TE Connectivity Ltd, Robert Bosch GmbH, Texas Instruments Incorporated, Microchip Technology Incorporated, Analog Devices Inc, Omron Corporatio, FLIR Systems, Panasonic Corporation, Thermometris, Emerson Electric Company.

3. What are the main segments of the Europe Temperature Sensor Industry?

The market segments include Type, Technology, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 7.43 billion as of 2022.

5. What are some drivers contributing to market growth?

Growth in Industry 4.0 & Rapid Factory Automation; Increasing Demand for Wearable in Consumer Electronics.

6. What are the notable trends driving market growth?

Oil and Gas to Show Significant Growth.

7. Are there any restraints impacting market growth?

Fluctuation in Raw Material Prices.

8. Can you provide examples of recent developments in the market?

January 2021 - Switzerland-based Sensirion announced that the company, LivingPackets, utilized Sensirion's humidity and temperature sensors in its sustainable packaging solutions. Using the solution called THE BOX, packaging waste is expected to be reduced by over 100 billion deliveries annually. THE BOX consists of highly resistant materials. It can be recycled without a specific limit and can survive almost 1,000 transport trips before reprocessing.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Temperature Sensor Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Temperature Sensor Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Temperature Sensor Industry?

To stay informed about further developments, trends, and reports in the Europe Temperature Sensor Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence