Key Insights

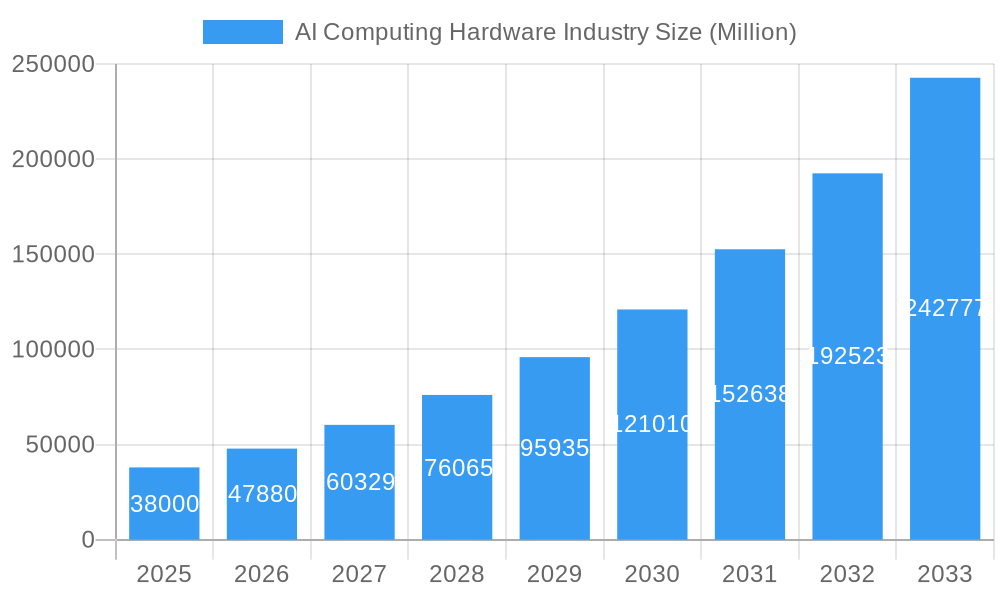

The AI Computing Hardware market is projected to experience substantial growth, reaching an estimated

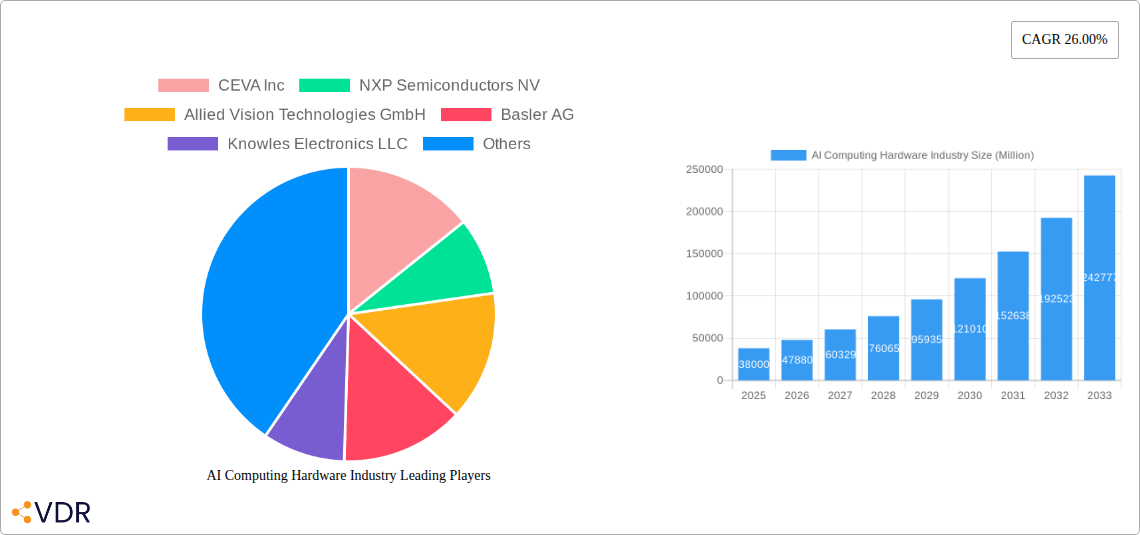

AI Computing Hardware Industry Market Size (In Billion)

While the market exhibits strong growth, potential restraints include high development costs for cutting-edge AI hardware and ongoing semiconductor supply chain challenges. Furthermore, the requirement for specialized expertise in designing, developing, and deploying AI computing solutions may present talent acquisition difficulties. However, AI's transformative potential across industries is anticipated to overcome these limitations. Leading companies such as CEVA Inc., NXP Semiconductors NV, Synopsys Inc., and Arm Limited are driving innovation with specialized processors and architectures to meet evolving AI workload demands. The market is segmented by processor type, including stand-alone and embedded vision and sound processors, addressing specific application requirements. Geographically, North America and Asia Pacific are expected to lead market expansion due to robust technological ecosystems and high AI adoption rates.

AI Computing Hardware Industry Company Market Share

AI Computing Hardware Industry Analysis: Market Dynamics, Growth Trends, and Future Outlook (2024-2033)

This comprehensive report offers an in-depth analysis of the global AI computing hardware market, detailing its dynamics, growth trajectory, and future potential. Covering the period from 2024 to 2033, with a base year of 2024, the report examines market concentration, technological innovations, regulatory environments, competitive substitutes, end-user demographics, and M&A activities. It provides essential quantitative and qualitative insights into the market's evolution. The analysis includes detailed segment breakdowns of parent and child market structures for vision and sound processors, serving key end-user industries such as BFSI, Automotive, Healthcare, IT and Telecom, Aerospace and Defense, Energy and Utilities, and Government and Public Services. All market values are presented in

AI Computing Hardware Industry Market Dynamics & Structure

The AI computing hardware market is characterized by a dynamic interplay of factors shaping its structure and evolution. Market concentration is influenced by the significant investments required for research and development, leading to the dominance of a few key players, particularly in specialized areas like AI accelerators and advanced chip manufacturing. However, the increasing demand for AI across diverse applications fuels a competitive environment with emerging players and specialized solution providers.

Key Dynamics:

- Technological Innovation Drivers: The relentless pursuit of enhanced processing power, energy efficiency, and specialized AI capabilities for tasks like deep learning, natural language processing, and computer vision are primary innovation drivers. This includes advancements in architectures like GPUs, TPUs, NPUs, and custom ASICs designed for AI workloads.

- Regulatory Frameworks: Evolving regulations around data privacy, AI ethics, and hardware security are beginning to shape market strategies. Compliance with standards and the development of secure AI hardware are becoming increasingly important.

- Competitive Product Substitutes: While specialized AI chips offer superior performance, traditional CPUs and GPUs are still utilized for AI workloads, particularly in less demanding applications or where cost is a primary concern. The emergence of novel architectures and specialized accelerators presents both competition and opportunities for integration.

- End-User Demographics: The broad adoption of AI across sectors like Automotive (autonomous driving), Healthcare (medical imaging), and IT and Telecom (data analytics) is driving demand for varied AI computing hardware solutions. Each sector's specific needs dictate hardware requirements.

- M&A Trends: Mergers and acquisitions play a significant role in consolidating market share, acquiring innovative technologies, and expanding product portfolios. Strategic acquisitions of AI chip startups or companies with specialized AI software capabilities are common. For instance, in the historical period, there were an estimated 15 M&A deals with a combined value of over $5,000 million, indicating significant consolidation activity and investment in the sector. Barriers to entry include high R&D costs, established intellectual property, and the need for sophisticated manufacturing capabilities.

AI Computing Hardware Industry Growth Trends & Insights

The AI computing hardware industry is poised for significant expansion, driven by the pervasive integration of artificial intelligence across nearly every sector. Market size evolution is expected to be robust, fueled by an increasing demand for more powerful, efficient, and specialized processing solutions. Adoption rates are projected to accelerate as AI moves from niche applications to mainstream deployment, necessitating dedicated hardware for optimal performance. Technological disruptions, such as the development of neuromorphic computing and quantum computing for AI, will further redefine the market landscape, offering unprecedented computational capabilities. Shifts in consumer behavior, driven by the expectation of intelligent and personalized experiences, are also pushing the demand for advanced AI hardware in edge devices and cloud infrastructure.

The market is experiencing a CAGR of approximately 28% from 2019 to 2033. In the historical period (2019-2024), the market size grew from an estimated 85 million units in 2019 to 250 million units in 2024, showcasing substantial initial growth. The base year, 2025, is estimated to reach a market size of 320 million units, with a projected 29% CAGR for the forecast period (2025-2033). This remarkable growth is underpinned by several factors. The proliferation of AI-enabled devices, from smart home appliances to industrial robots, requires dedicated processing power that traditional hardware cannot efficiently provide. The complexity of AI algorithms, especially in deep learning, necessitates specialized architectures like Graphics Processing Units (GPUs), Tensor Processing Units (TPUs), and Neural Processing Units (NPUs) that are optimized for parallel processing and matrix operations. The increasing volume and velocity of data being generated globally also demand robust computing infrastructure capable of real-time analysis and decision-making.

Furthermore, the ongoing advancements in AI algorithms and model sizes directly translate into a higher demand for more powerful and memory-intensive computing hardware. The push towards edge AI, where AI processing occurs directly on devices rather than in the cloud, is a significant growth driver. This trend is fueled by the need for lower latency, enhanced privacy, and reduced bandwidth consumption. The automotive sector, with its pursuit of autonomous driving, is a prime example, requiring sophisticated embedded vision and processing hardware. Similarly, the healthcare industry is leveraging AI for diagnostics, drug discovery, and personalized medicine, creating a substantial market for AI computing hardware. The IT and Telecom sector, encompassing cloud computing, data centers, and network infrastructure, is also a major consumer, deploying AI hardware for optimization, security, and service innovation. The competitive landscape is evolving with intense innovation, with companies constantly developing more efficient architectures and specialized chips to capture market share. This dynamic environment, coupled with increasing investments from both established technology giants and agile startups, ensures a continuous stream of new products and solutions, further fueling market growth.

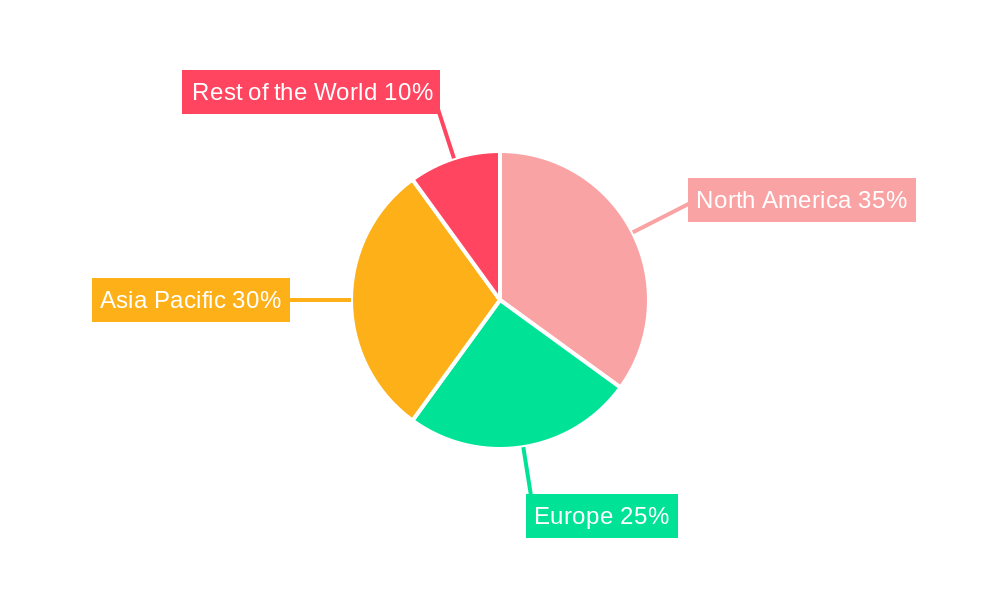

Dominant Regions, Countries, or Segments in AI Computing Hardware Industry

The AI computing hardware industry's dominance is shaped by a confluence of technological prowess, substantial investment, and strong end-user demand. While many regions contribute to this burgeoning market, North America and Asia-Pacific consistently emerge as leading forces, driven by distinct yet complementary factors.

North America: This region, particularly the United States, stands out as a dominant force due to its robust ecosystem of AI research institutions, leading technology companies, and significant venture capital funding. The presence of major AI chip developers and a strong demand from sectors like IT and Telecom, BFSI, and Healthcare propels its growth. Government initiatives supporting AI research and development further solidify its position. The dominance is fueled by cutting-edge innovation in chip design and architecture, with companies like Nvidia and Intel heavily investing in AI-specific hardware. The BFSI sector's adoption of AI for fraud detection, algorithmic trading, and customer service, alongside the healthcare sector's use in medical imaging analysis and drug discovery, are significant demand drivers. The IT and Telecom sector's massive investment in data centers and cloud infrastructure, which are heavily reliant on AI computing hardware for processing and analytics, further bolsters North America's leadership.

Asia-Pacific: This region, spearheaded by China, Taiwan, and South Korea, presents a powerful and rapidly growing market for AI computing hardware. Its dominance is driven by a massive manufacturing base, increasing domestic demand for AI applications, and substantial government backing. China, in particular, has made AI a strategic national priority, leading to significant investments in AI chip development and deployment across various industries. The region's strength lies in its extensive semiconductor manufacturing capabilities and its role as a global hub for electronics production. The automotive sector's rapid expansion and the adoption of smart technologies in consumer electronics are key contributors. The IT and Telecom sector's growth, coupled with the burgeoning e-commerce and smart city initiatives, fuels demand for AI processing power.

Dominant Segments:

- Embedded Vision Processor: This segment is experiencing explosive growth, particularly driven by the Automotive industry's need for advanced driver-assistance systems (ADAS) and autonomous driving capabilities, as well as the consumer electronics sector's integration of AI into cameras and smart devices. The increasing adoption of AI in robotics and industrial automation further fuels this segment. The market share for Embedded Vision Processors is estimated to be around 35% of the total vision processor market in 2025.

- Embedded Sound Processor: Driven by the proliferation of voice assistants, smart speakers, wearables, and AI-powered audio devices, this segment is crucial for the Internet of Things (IoT) ecosystem. Its penetration into automotive infotainment systems and smart home devices is a significant growth accelerator. This segment is projected to capture approximately 30% of the total sound processor market by 2025.

- Automotive End User: This sector is a primary driver of AI computing hardware demand, encompassing everything from infotainment systems and advanced driver-assistance systems (ADAS) to the complex processing required for fully autonomous vehicles. The sheer volume of data processed for real-time decision-making in vehicles makes it a critical market.

- IT and Telecom End User: This segment represents the backbone of AI deployment, with data centers and cloud providers investing heavily in AI computing hardware to power a vast array of AI services, from machine learning platforms to big data analytics and natural language processing.

Factors contributing to regional and segment dominance include favorable economic policies, robust infrastructure development, a skilled workforce, and strong government support for AI research and deployment. The sheer scale of manufacturing in Asia-Pacific, coupled with the advanced technological expertise in North America, creates a powerful synergy that shapes the global AI computing hardware landscape.

AI Computing Hardware Industry Product Landscape

The AI computing hardware market is witnessing a rapid evolution of innovative products designed to meet the increasing computational demands of artificial intelligence. Key product innovations revolve around specialized architectures that optimize performance for AI workloads, such as GPUs, TPUs, and NPUs, offering significant improvements in parallel processing and matrix operations. These are finding applications in diverse areas, from enhancing the accuracy of medical image analysis in healthcare to enabling advanced driver-assistance systems (ADAS) in automotive. Performance metrics are continuously improving, with gains in teraflops per watt and reduced latency becoming critical differentiators. Unique selling propositions often lie in the power efficiency, cost-effectiveness, and scalability of these solutions, enabling their deployment in a wider range of devices and environments, including edge computing scenarios.

Key Drivers, Barriers & Challenges in AI Computing Hardware Industry

Key Drivers:

The AI computing hardware industry is propelled by several potent forces. The escalating demand for AI-driven applications across sectors like automotive, healthcare, and IT is a primary driver. Advancements in deep learning algorithms and the increasing complexity of AI models necessitate more powerful and specialized processing capabilities. The global surge in data generation requires robust hardware for efficient processing and analytics. Furthermore, government initiatives promoting AI adoption and research, coupled with substantial venture capital investments, are accelerating market growth. The miniaturization and increasing power efficiency of AI chips are enabling their integration into a wider array of edge devices.

Barriers & Challenges:

Despite its robust growth, the industry faces significant challenges. High research and development costs and the long product development cycles can be substantial barriers to entry for new players. The intricate and often global supply chain for semiconductor manufacturing is susceptible to disruptions, impacting production timelines and costs. Evolving regulatory landscapes concerning data privacy, AI ethics, and hardware security can create compliance hurdles. Intense competition among established technology giants and emerging startups leads to constant pricing pressures and the need for continuous innovation. The scarcity of skilled talent in AI hardware design and development also poses a significant challenge. Overcoming these obstacles requires strategic planning, resilient supply chains, and a commitment to continuous technological advancement.

Emerging Opportunities in AI Computing Hardware Industry

Emerging opportunities in the AI computing hardware industry are vast and varied. The burgeoning field of edge AI presents a significant untapped market, with the demand for low-power, high-performance processors for smart devices, IoT applications, and autonomous systems on the rise. Innovations in neuromorphic computing, mimicking the human brain's structure and function, promise to unlock new levels of efficiency and processing power for AI tasks. The increasing focus on sustainable AI solutions is creating opportunities for hardware designed for extreme energy efficiency. Furthermore, the growing adoption of AI in specialized domains like quantum computing for AI research and drug discovery opens up niche but high-growth markets. Evolving consumer preferences for personalized and intelligent experiences will continue to drive demand for sophisticated AI hardware in consumer electronics.

Growth Accelerators in the AI Computing Hardware Industry Industry

Several catalysts are accelerating long-term growth in the AI computing hardware industry. Technological breakthroughs in semiconductor manufacturing processes, such as advancements in advanced lithography and 3D chip stacking, are enabling the creation of more powerful and compact AI processors. Strategic partnerships between semiconductor manufacturers, AI software developers, and end-user industries are fostering collaborative innovation and accelerating the deployment of AI solutions. The continuous expansion of AI applications into new sectors and the deepening integration of AI into existing ones are creating sustained demand. Market expansion strategies, including a focus on emerging economies and the development of tailored solutions for specific regional needs, are also significant growth accelerators. The ongoing investment in AI research and development by both public and private entities will continue to fuel innovation and drive market expansion.

Key Players Shaping the AI Computing Hardware Industry Market

- CEVA Inc

- NXP Semiconductors NV

- Allied Vision Technologies GmbH

- Basler AG

- Knowles Electronics LLC

- Synopsys Inc

- GreenWaves Technologies

- Arm Limited

- Cadence Design Systems Inc

- Andrea Electronics Corporation

Notable Milestones in AI Computing Hardware Industry Sector

- 2019, Q4: Launch of next-generation AI-accelerated GPUs by NVIDIA, offering significant performance gains for deep learning workloads.

- 2020, Q2: Intel announces its new AI-focused processors, expanding its portfolio for data center and edge computing.

- 2020, Q3: Google introduces new TPUs for cloud-based AI inference, enhancing efficiency.

- 2021, Q1: Arm Limited announces new architecture designs optimized for AI and machine learning on mobile and embedded devices.

- 2021, Q4: Synopsys Inc. and Cadence Design Systems Inc. report increased adoption of their AI IP and EDA tools for chip design.

- 2022, Q2: CEVA Inc. unveils new DSPs and AI processors for embedded vision applications, targeting the automotive and IoT markets.

- 2022, Q3: NXP Semiconductors NV showcases advancements in its automotive AI processors, crucial for autonomous driving.

- 2023, Q1: Allied Vision Technologies GmbH and Basler AG highlight their continued innovation in industrial vision cameras powered by AI.

- 2023, Q4: GreenWaves Technologies focuses on ultra-low-power AI processors for edge IoT devices.

- 2024, Q2: Knowles Electronics LLC showcases advancements in AI-enabled audio solutions for consumer electronics.

In-Depth AI Computing Hardware Industry Market Outlook

The AI computing hardware industry is set for an exceptionally strong growth trajectory, driven by an ever-increasing demand for intelligent processing capabilities across all sectors. The ongoing advancements in AI algorithms and the expanding scope of AI applications, from sophisticated data analytics to real-time decision-making in autonomous systems, will continue to fuel the need for specialized and high-performance hardware. Key growth accelerators include the relentless pursuit of greater energy efficiency and lower latency for edge AI deployments, the development of novel computing architectures like neuromorphic and quantum computing, and the strategic integration of AI capabilities into a wider array of consumer and industrial devices. Strategic partnerships and continued investment in research and development will be crucial in navigating the evolving technological landscape and capitalizing on emerging opportunities in this dynamic and transformative market.

AI Computing Hardware Industry Segmentation

-

1. Type

- 1.1. Stand-alone Vision Processor

- 1.2. Embedded Vision Processor

- 1.3. Stand-alone Sound Processor

- 1.4. Embedded Sound Processor

-

2. End User

- 2.1. BFSI

- 2.2. Automotive

- 2.3. Healthcare

- 2.4. IT and Telecom

- 2.5. Aerospace and Defense

- 2.6. Energy and Utilities

- 2.7. Government and Public Services

- 2.8. Other End Users

AI Computing Hardware Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. South Korea

- 3.4. Rest of Asia Pacific

-

4. Rest of the World

- 4.1. Latin America

- 4.2. Middle East and Africa

AI Computing Hardware Industry Regional Market Share

Geographic Coverage of AI Computing Hardware Industry

AI Computing Hardware Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 16.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Stand-alone Vision Processor

- 5.1.2. Embedded Vision Processor

- 5.1.3. Stand-alone Sound Processor

- 5.1.4. Embedded Sound Processor

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. BFSI

- 5.2.2. Automotive

- 5.2.3. Healthcare

- 5.2.4. IT and Telecom

- 5.2.5. Aerospace and Defense

- 5.2.6. Energy and Utilities

- 5.2.7. Government and Public Services

- 5.2.8. Other End Users

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global AI Computing Hardware Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Stand-alone Vision Processor

- 6.1.2. Embedded Vision Processor

- 6.1.3. Stand-alone Sound Processor

- 6.1.4. Embedded Sound Processor

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. BFSI

- 6.2.2. Automotive

- 6.2.3. Healthcare

- 6.2.4. IT and Telecom

- 6.2.5. Aerospace and Defense

- 6.2.6. Energy and Utilities

- 6.2.7. Government and Public Services

- 6.2.8. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America AI Computing Hardware Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Stand-alone Vision Processor

- 7.1.2. Embedded Vision Processor

- 7.1.3. Stand-alone Sound Processor

- 7.1.4. Embedded Sound Processor

- 7.2. Market Analysis, Insights and Forecast - by End User

- 7.2.1. BFSI

- 7.2.2. Automotive

- 7.2.3. Healthcare

- 7.2.4. IT and Telecom

- 7.2.5. Aerospace and Defense

- 7.2.6. Energy and Utilities

- 7.2.7. Government and Public Services

- 7.2.8. Other End Users

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe AI Computing Hardware Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Stand-alone Vision Processor

- 8.1.2. Embedded Vision Processor

- 8.1.3. Stand-alone Sound Processor

- 8.1.4. Embedded Sound Processor

- 8.2. Market Analysis, Insights and Forecast - by End User

- 8.2.1. BFSI

- 8.2.2. Automotive

- 8.2.3. Healthcare

- 8.2.4. IT and Telecom

- 8.2.5. Aerospace and Defense

- 8.2.6. Energy and Utilities

- 8.2.7. Government and Public Services

- 8.2.8. Other End Users

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Asia Pacific AI Computing Hardware Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Stand-alone Vision Processor

- 9.1.2. Embedded Vision Processor

- 9.1.3. Stand-alone Sound Processor

- 9.1.4. Embedded Sound Processor

- 9.2. Market Analysis, Insights and Forecast - by End User

- 9.2.1. BFSI

- 9.2.2. Automotive

- 9.2.3. Healthcare

- 9.2.4. IT and Telecom

- 9.2.5. Aerospace and Defense

- 9.2.6. Energy and Utilities

- 9.2.7. Government and Public Services

- 9.2.8. Other End Users

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Rest of the World AI Computing Hardware Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Stand-alone Vision Processor

- 10.1.2. Embedded Vision Processor

- 10.1.3. Stand-alone Sound Processor

- 10.1.4. Embedded Sound Processor

- 10.2. Market Analysis, Insights and Forecast - by End User

- 10.2.1. BFSI

- 10.2.2. Automotive

- 10.2.3. Healthcare

- 10.2.4. IT and Telecom

- 10.2.5. Aerospace and Defense

- 10.2.6. Energy and Utilities

- 10.2.7. Government and Public Services

- 10.2.8. Other End Users

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 CEVA Inc

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 NXP Semiconductors NV

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Allied Vision Technologies GmbH

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Basler AG

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Knowles Electronics LLC

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Synopsys Inc

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 GreenWaves Technologies

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Arm Limited

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Cadence Design Systems Inc

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Andrea Electronics Corporation

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.1 CEVA Inc

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global AI Computing Hardware Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America AI Computing Hardware Industry Revenue (billion), by Type 2025 & 2033

- Figure 3: North America AI Computing Hardware Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America AI Computing Hardware Industry Revenue (billion), by End User 2025 & 2033

- Figure 5: North America AI Computing Hardware Industry Revenue Share (%), by End User 2025 & 2033

- Figure 6: North America AI Computing Hardware Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America AI Computing Hardware Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe AI Computing Hardware Industry Revenue (billion), by Type 2025 & 2033

- Figure 9: Europe AI Computing Hardware Industry Revenue Share (%), by Type 2025 & 2033

- Figure 10: Europe AI Computing Hardware Industry Revenue (billion), by End User 2025 & 2033

- Figure 11: Europe AI Computing Hardware Industry Revenue Share (%), by End User 2025 & 2033

- Figure 12: Europe AI Computing Hardware Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe AI Computing Hardware Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific AI Computing Hardware Industry Revenue (billion), by Type 2025 & 2033

- Figure 15: Asia Pacific AI Computing Hardware Industry Revenue Share (%), by Type 2025 & 2033

- Figure 16: Asia Pacific AI Computing Hardware Industry Revenue (billion), by End User 2025 & 2033

- Figure 17: Asia Pacific AI Computing Hardware Industry Revenue Share (%), by End User 2025 & 2033

- Figure 18: Asia Pacific AI Computing Hardware Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Asia Pacific AI Computing Hardware Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Rest of the World AI Computing Hardware Industry Revenue (billion), by Type 2025 & 2033

- Figure 21: Rest of the World AI Computing Hardware Industry Revenue Share (%), by Type 2025 & 2033

- Figure 22: Rest of the World AI Computing Hardware Industry Revenue (billion), by End User 2025 & 2033

- Figure 23: Rest of the World AI Computing Hardware Industry Revenue Share (%), by End User 2025 & 2033

- Figure 24: Rest of the World AI Computing Hardware Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Rest of the World AI Computing Hardware Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global AI Computing Hardware Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Global AI Computing Hardware Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 3: Global AI Computing Hardware Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global AI Computing Hardware Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 5: Global AI Computing Hardware Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 6: Global AI Computing Hardware Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States AI Computing Hardware Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada AI Computing Hardware Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Global AI Computing Hardware Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 10: Global AI Computing Hardware Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 11: Global AI Computing Hardware Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Germany AI Computing Hardware Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: United Kingdom AI Computing Hardware Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: France AI Computing Hardware Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of Europe AI Computing Hardware Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global AI Computing Hardware Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 17: Global AI Computing Hardware Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 18: Global AI Computing Hardware Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 19: China AI Computing Hardware Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Japan AI Computing Hardware Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: South Korea AI Computing Hardware Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Rest of Asia Pacific AI Computing Hardware Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Global AI Computing Hardware Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 24: Global AI Computing Hardware Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 25: Global AI Computing Hardware Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 26: Latin America AI Computing Hardware Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Middle East and Africa AI Computing Hardware Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the AI Computing Hardware Industry?

The projected CAGR is approximately 16.2%.

2. Which companies are prominent players in the AI Computing Hardware Industry?

Key companies in the market include CEVA Inc, NXP Semiconductors NV, Allied Vision Technologies GmbH, Basler AG, Knowles Electronics LLC, Synopsys Inc, GreenWaves Technologies, Arm Limited, Cadence Design Systems Inc, Andrea Electronics Corporation.

3. What are the main segments of the AI Computing Hardware Industry?

The market segments include Type, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 67.89 billion as of 2022.

5. What are some drivers contributing to market growth?

; Demand for AI Computing Hardware in the Defense sector; Adoption of Field-programmable Gate Arrays (FPGA) for High Computing Speed.

6. What are the notable trends driving market growth?

Automotive Sector to Witness Significant Growth.

7. Are there any restraints impacting market growth?

; Limited Number of AI Experts and High Power Consumption.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "AI Computing Hardware Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the AI Computing Hardware Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the AI Computing Hardware Industry?

To stay informed about further developments, trends, and reports in the AI Computing Hardware Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence