Key Insights

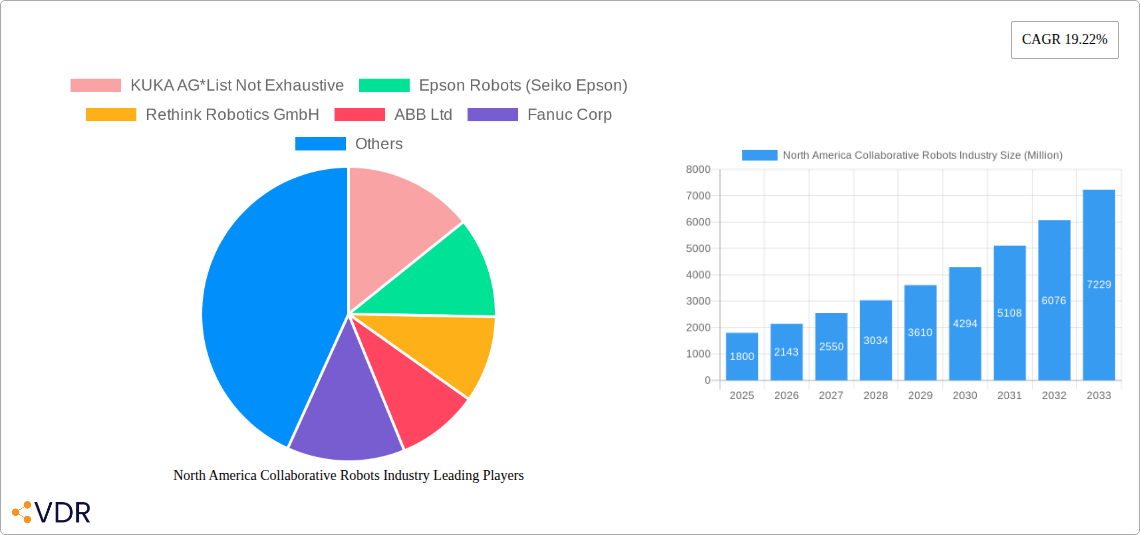

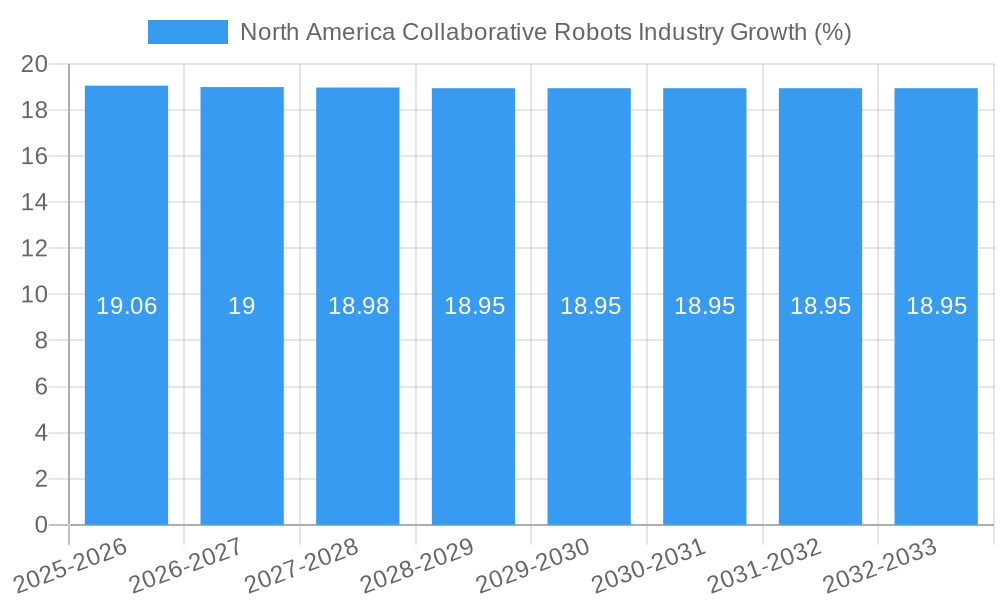

The North American collaborative robots (cobots) industry is poised for remarkable expansion, driven by escalating demand for enhanced automation and flexibility across diverse manufacturing sectors. With an estimated market size of approximately $1.8 billion in 2025, the sector is projected to witness a substantial Compound Annual Growth Rate (CAGR) of 19.22% through 2033. This robust growth is primarily fueled by the increasing adoption of cobots in the electronics/semiconductor & FPD industry and the automotive sector, where their ability to perform tasks such as material handling, pick and place, and assembly with precision and safety is paramount. The inherent advantages of cobots, including ease of deployment, lower upfront investment compared to traditional industrial robots, and their capacity to work alongside human operators, are significant drivers. Furthermore, advancements in AI and machine learning are enhancing cobot capabilities, making them more intelligent and adaptable to complex manufacturing environments, thereby solidifying their position as a critical component of Industry 4.0 initiatives across the region.

The North American cobot market is characterized by a dynamic landscape with key players like KUKA AG, ABB Ltd., Fanuc Corp., and Universal Robots AS leading the charge in innovation and market penetration. While the market is largely dominated by cobots with payloads of 10 kg and above, driven by heavy industrial applications, there's a growing segment for smaller payloads (less than 5 kg and 5-9 kg) in electronics assembly and other intricate tasks. Despite the strong growth trajectory, certain restraints, such as the initial integration challenges and the need for specialized training for operators, could temper rapid adoption in some segments. However, the compelling return on investment, improved worker safety, and increased productivity offered by cobots are expected to outweigh these challenges. The forecast period from 2025 to 2033 signifies a crucial phase for this market, with continuous technological advancements and a broadening application spectrum poised to further accelerate its growth and solidify North America's leadership in collaborative robotics.

North America Collaborative Robots Industry Report: Market Dynamics, Growth Trends, and Key Player Analysis (2019-2033)

This comprehensive report offers an in-depth analysis of the North America collaborative robots (cobots) industry, providing critical insights into market dynamics, growth trajectories, and the competitive landscape. Designed for industry professionals, investors, and strategic planners, this report leverages high-traffic keywords to ensure maximum search engine visibility and delivers actionable intelligence for navigating this rapidly evolving sector. Explore market size evolution, adoption rates, technological disruptions, and regional dominance, with all values presented in Million units.

North America Collaborative Robots Industry Market Dynamics & Structure

The North America collaborative robots industry is characterized by a dynamic and evolving market structure, influenced by a confluence of technological innovation, regulatory shifts, and changing end-user demands. Market concentration is moderately high, with key players investing heavily in research and development to maintain a competitive edge. Technological innovation drivers are primarily focused on enhancing cobot capabilities such as increased payload capacity, improved AI integration for smarter decision-making, and more intuitive human-robot interaction. Regulatory frameworks, while still developing, are increasingly prioritizing safety standards and ethical deployment of cobots, fostering a more secure market environment. Competitive product substitutes are emerging, including advanced automation solutions and traditional industrial robots, yet cobots maintain a distinct advantage in flexibility and ease of use for collaborative tasks. End-user demographics are rapidly expanding, with a growing adoption across diverse sectors seeking to augment human capabilities and address labor shortages. Mergers and acquisitions (M&A) trends indicate a consolidation phase as larger players seek to acquire innovative startups and expand their technological portfolios.

- Market Concentration: Moderate to high, with significant investment in R&D by leading firms.

- Technological Innovation Drivers: AI integration, enhanced payload, intuitive interfaces, mobility.

- Regulatory Frameworks: Focus on safety standards, interoperability, and ethical deployment.

- Competitive Product Substitutes: Advanced traditional robotics, specialized automation equipment.

- End-User Demographics: Diversifying rapidly across manufacturing, logistics, healthcare, and research.

- M&A Trends: Strategic acquisitions of startups for technology and talent acquisition.

North America Collaborative Robots Industry Growth Trends & Insights

The North America collaborative robots industry is poised for substantial growth, driven by a confluence of factors that are reshaping manufacturing and industrial operations. The market size evolution indicates a consistent upward trajectory, fueled by increasing awareness of cobot benefits, including enhanced productivity, improved worker safety, and greater operational flexibility. Adoption rates are accelerating across small, medium, and large enterprises alike, as the return on investment becomes more evident and the technology becomes more accessible. Technological disruptions are continuously enhancing cobot capabilities, with advancements in machine learning enabling more sophisticated task execution and adaptive learning. Consumer behavior shifts, particularly within the B2B space, are emphasizing the need for agile and adaptable automation solutions that can be easily integrated into existing workflows and reprogrammed for new tasks. This report leverages the latest data to deliver a nuanced analysis of these trends, projecting significant market penetration in the coming years. The compound annual growth rate (CAGR) is expected to remain robust, reflecting the growing demand for intelligent and human-centric automation solutions.

Dominant Regions, Countries, or Segments in North America Collaborative Robots Industry

Within the North American collaborative robots industry, the United States currently stands as the dominant region, driven by its robust manufacturing base, significant investments in advanced technologies, and a proactive approach to automation adoption across various sectors. The Automotive end-user industry consistently demonstrates strong growth and substantial market share, a trend amplified by the critical need for precision, efficiency, and worker safety in vehicle production. Furthermore, the Electronics/Semiconductor & FPD sector is a significant contributor to market growth, owing to the intricate and repetitive tasks involved in the manufacturing of sophisticated electronic components, where cobots offer unparalleled precision and consistency.

Examining the Payload segments, the 5-9 kg category is experiencing rapid expansion. This is largely attributed to its versatility in handling a wide array of tasks in assembly, pick and place, and light material handling operations, making it an ideal choice for many SMEs and specific applications within larger enterprises. However, the 10 kg and Above segment is also witnessing considerable demand, particularly from the automotive and heavy manufacturing sectors, where larger components require more robust robotic assistance.

In terms of Application, Material Handling and Pick and Place applications are leading the charge. The inherent flexibility and safety features of cobots make them exceptionally well-suited for these tasks, which are prevalent across nearly all industrial segments. The ease with which cobots can be redeployed for different material handling needs also contributes to their widespread adoption.

- Dominant Region: United States, due to its strong industrial infrastructure and high adoption rates.

- Key End-User Industries:

- Automotive: Driving demand for precision, speed, and safety in production lines.

- Electronics/Semiconductor & FPD: Benefiting from cobots' precision for intricate component handling.

- Dominant Payload Segments:

- 5-9 kg: High versatility for assembly and material handling, appealing to a broad market.

- 10 kg and Above: Crucial for heavy-duty tasks in automotive and manufacturing.

- Leading Applications:

- Material Handling: Essential for efficient supply chain and production flow.

- Pick and Place: A fundamental application where cobots excel in speed and accuracy.

- Growth Potential Factors: Government incentives for automation, skilled workforce development, and the pursuit of Industry 4.0 initiatives.

North America Collaborative Robots Industry Product Landscape

The product landscape of the North America collaborative robots industry is defined by continuous innovation focused on enhancing user-friendliness, safety, and adaptability. Manufacturers are consistently introducing cobots with improved dexterity, higher payload capacities, and expanded reach to cater to a wider range of industrial applications. Key product advancements include integrated vision systems for object recognition and guidance, enhanced force-sensing technology for safer human interaction, and modular designs for easier integration and customization. Unique selling propositions often revolve around the cobots' ability to seamlessly collaborate with human workers, their quick deployment times, and their cost-effectiveness compared to traditional industrial automation. Technological advancements are also pushing towards more intelligent cobots capable of learning and adapting to new tasks with minimal programming.

Key Drivers, Barriers & Challenges in North America Collaborative Robots Industry

Key Drivers:

- Increasing Labor Costs and Shortages: Cobots offer a cost-effective solution to automate repetitive tasks, alleviating pressure from rising labor expenses and a shrinking workforce.

- Demand for Enhanced Productivity and Efficiency: Collaborative robots enable faster cycle times, improved accuracy, and increased throughput in manufacturing processes.

- Growing Emphasis on Worker Safety: Cobots are designed to work alongside humans, reducing the risk of workplace injuries associated with strenuous or hazardous tasks.

- Technological Advancements: Continuous improvements in AI, sensor technology, and user interfaces are making cobots more capable and easier to implement.

- Government Initiatives and Incentives: Support for automation and advanced manufacturing through grants and tax breaks is encouraging adoption.

Barriers & Challenges:

- Initial Investment Costs: While decreasing, the upfront cost of cobot systems can still be a barrier for some small and medium-sized enterprises.

- Integration Complexity: Integrating cobots into existing factory infrastructure and IT systems can require specialized expertise.

- Lack of Skilled Workforce: A shortage of trained personnel to operate, maintain, and program cobots can hinder widespread adoption.

- Perceived Job Displacement Concerns: Societal apprehension about robots taking human jobs can create resistance to automation.

- Standardization and Interoperability: Developing industry-wide standards for cobot communication and operation is crucial for seamless integration across different vendors.

- Supply Chain Disruptions: Global supply chain issues can impact the availability and pricing of cobot components.

Emerging Opportunities in North America Collaborative Robots Industry

Emerging opportunities in the North America collaborative robots industry are abundant, driven by the expanding applicability of cobots beyond traditional manufacturing. The healthcare sector presents a significant untapped market for cobots in tasks such as surgical assistance, patient care, and laboratory automation. Furthermore, the logistics and warehousing industry is increasingly adopting cobots for order fulfillment, sorting, and material handling, especially with the rise of e-commerce. The development of more specialized cobots for niche applications, such as food processing and agriculture, also represents a fertile ground for growth. The increasing demand for flexible and reconfigurable automation solutions in response to dynamic market needs will continue to fuel innovation and the exploration of new collaborative robotic applications.

Growth Accelerators in the North America Collaborative Robots Industry Industry

Several key catalysts are accelerating the long-term growth of the North America collaborative robots industry. Technological breakthroughs, particularly in artificial intelligence and machine learning, are enabling cobots to perform more complex tasks autonomously and adapt to changing environments. Strategic partnerships between cobot manufacturers and software developers are creating more integrated and intelligent automation solutions. Furthermore, market expansion strategies by key players, focusing on educating potential customers about the benefits of cobots and providing robust support services, are driving wider adoption. The ongoing digital transformation across industries, coupled with the drive for operational resilience and agility, further amplifies the demand for collaborative robotic solutions.

Key Players Shaping the North America Collaborative Robots Industry Market

- KUKA AG

- Epson Robots (Seiko Epson)

- Rethink Robotics GmbH

- ABB Ltd

- Fanuc Corp

- Festo Group

- OMRON Corporation

- Universal Robots AS

- SiasunRobot & Automation Co Ltd

- Precise Automation Inc

- Kawasaki Heavy Industries Ltd

- TechManRobot Inc

- Staubli International AG

- AUBO Robotics USA

Notable Milestones in North America Collaborative Robots Industry Sector

- July 2020: Canada's SNC-Lavalin and Kinova collaborated and signed a two-year agreement to deploy robotic solutions in the nuclear sector. SNC-Lavalin has fully integrated Kinova's equipment into a certified, patent-pending solution that enables safe deployment of the collaborative robot into almost any glovebox and other similar applications. The solutions developed are expected to prove deployable in the thousands of nuclear gloveboxes across the world, increasing operator safety, with potential to improve productivity.

- January 2020: ABB invested in Sweden-based, early-stage robotics solution and software start-up MTEK through its venture capital unit to push collaborative robots' boundaries. This collaboration is expected to develop and deploy software, solutions, and services for real-time intelligent and collaborative production for ABB's YuMi.

In-Depth North America Collaborative Robots Industry Market Outlook

The outlook for the North America collaborative robots industry remains exceptionally promising, driven by sustained innovation and a widening array of applications. Growth accelerators such as advancements in AI for enhanced decision-making, the development of more dexterous and versatile cobot designs, and strategic collaborations between technology providers are collectively propelling the market forward. The increasing recognition of cobots as essential tools for enhancing operational flexibility, improving worker safety, and addressing labor challenges across diverse sectors like automotive, electronics, and even healthcare, will continue to fuel demand. Strategic opportunities lie in further penetration of SMB markets, the development of industry-specific cobot solutions, and the integration of cobots into broader smart factory ecosystems. The market is on a strong trajectory, poised for significant expansion and a transformative impact on industrial operations.

North America Collaborative Robots Industry Segmentation

-

1. Payload

- 1.1. Less than 5 kg

- 1.2. 5-9 kg

- 1.3. 10 kg and Above

-

2. End-user Industry

- 2.1. Electronics/Semiconductor & FPD

- 2.2. Automotive

- 2.3. Other End-user Industries

-

3. Application

- 3.1. Material Handling

- 3.2. Pick and Place

- 3.3. Assembly

- 3.4. Other Ap

North America Collaborative Robots Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Collaborative Robots Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 19.22% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. High Return on Investment and Advancements in Edge Computing Leading to Easier Implementation; Increasing Demand for Automation in Various Industrial Processes

- 3.3. Market Restrains

- 3.3.1. High Initial Investment and the Requirement of Skilled Workforce

- 3.4. Market Trends

- 3.4.1. Material Handling is Expected to Witness Significant Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. North America Collaborative Robots Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Payload

- 5.1.1. Less than 5 kg

- 5.1.2. 5-9 kg

- 5.1.3. 10 kg and Above

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Electronics/Semiconductor & FPD

- 5.2.2. Automotive

- 5.2.3. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Material Handling

- 5.3.2. Pick and Place

- 5.3.3. Assembly

- 5.3.4. Other Ap

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Payload

- 6. United States North America Collaborative Robots Industry Analysis, Insights and Forecast, 2019-2031

- 7. Canada North America Collaborative Robots Industry Analysis, Insights and Forecast, 2019-2031

- 8. Mexico North America Collaborative Robots Industry Analysis, Insights and Forecast, 2019-2031

- 9. Rest of North America North America Collaborative Robots Industry Analysis, Insights and Forecast, 2019-2031

- 10. Competitive Analysis

- 10.1. Market Share Analysis 2024

- 10.2. Company Profiles

- 10.2.1 KUKA AG*List Not Exhaustive

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 Epson Robots (Seiko Epson)

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 Rethink Robotics GmbH

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 ABB Ltd

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 Fanuc Corp

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 Festo Group

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 OMRON Corporation

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 Universal Robots AS

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.9 SiasunRobot & Automation Co Ltd

- 10.2.9.1. Overview

- 10.2.9.2. Products

- 10.2.9.3. SWOT Analysis

- 10.2.9.4. Recent Developments

- 10.2.9.5. Financials (Based on Availability)

- 10.2.10 Precise Automation Inc

- 10.2.10.1. Overview

- 10.2.10.2. Products

- 10.2.10.3. SWOT Analysis

- 10.2.10.4. Recent Developments

- 10.2.10.5. Financials (Based on Availability)

- 10.2.11 Kawasaki Heavy Industries Ltd

- 10.2.11.1. Overview

- 10.2.11.2. Products

- 10.2.11.3. SWOT Analysis

- 10.2.11.4. Recent Developments

- 10.2.11.5. Financials (Based on Availability)

- 10.2.12 TechManRobot Inc

- 10.2.12.1. Overview

- 10.2.12.2. Products

- 10.2.12.3. SWOT Analysis

- 10.2.12.4. Recent Developments

- 10.2.12.5. Financials (Based on Availability)

- 10.2.13 StaubliInternational AG

- 10.2.13.1. Overview

- 10.2.13.2. Products

- 10.2.13.3. SWOT Analysis

- 10.2.13.4. Recent Developments

- 10.2.13.5. Financials (Based on Availability)

- 10.2.14 AUBO Robotics USA

- 10.2.14.1. Overview

- 10.2.14.2. Products

- 10.2.14.3. SWOT Analysis

- 10.2.14.4. Recent Developments

- 10.2.14.5. Financials (Based on Availability)

- 10.2.1 KUKA AG*List Not Exhaustive

List of Figures

- Figure 1: North America Collaborative Robots Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: North America Collaborative Robots Industry Share (%) by Company 2024

List of Tables

- Table 1: North America Collaborative Robots Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: North America Collaborative Robots Industry Revenue Million Forecast, by Payload 2019 & 2032

- Table 3: North America Collaborative Robots Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 4: North America Collaborative Robots Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 5: North America Collaborative Robots Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: North America Collaborative Robots Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: United States North America Collaborative Robots Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Canada North America Collaborative Robots Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Mexico North America Collaborative Robots Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Rest of North America North America Collaborative Robots Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: North America Collaborative Robots Industry Revenue Million Forecast, by Payload 2019 & 2032

- Table 12: North America Collaborative Robots Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 13: North America Collaborative Robots Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 14: North America Collaborative Robots Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 15: United States North America Collaborative Robots Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Canada North America Collaborative Robots Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: Mexico North America Collaborative Robots Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Collaborative Robots Industry?

The projected CAGR is approximately 19.22%.

2. Which companies are prominent players in the North America Collaborative Robots Industry?

Key companies in the market include KUKA AG*List Not Exhaustive, Epson Robots (Seiko Epson), Rethink Robotics GmbH, ABB Ltd, Fanuc Corp, Festo Group, OMRON Corporation, Universal Robots AS, SiasunRobot & Automation Co Ltd, Precise Automation Inc, Kawasaki Heavy Industries Ltd, TechManRobot Inc, StaubliInternational AG, AUBO Robotics USA.

3. What are the main segments of the North America Collaborative Robots Industry?

The market segments include Payload, End-user Industry, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

High Return on Investment and Advancements in Edge Computing Leading to Easier Implementation; Increasing Demand for Automation in Various Industrial Processes.

6. What are the notable trends driving market growth?

Material Handling is Expected to Witness Significant Growth.

7. Are there any restraints impacting market growth?

High Initial Investment and the Requirement of Skilled Workforce.

8. Can you provide examples of recent developments in the market?

July 2020 - Canada's SNC-Lavalin and Kinova collaborated and signed a two-year agreement to deploy robotic solutions in the nuclear sector. SNC-Lavalin has fully integrated Kinova's equipment into a certified, patent-pending solution that enables safe deployment of the collaborative robot into almost any glovebox and other similar applications, The solutions developed are expected to prove deployable in the thousands of nuclear gloveboxes across the world, increasing operator safety, with potential to improve productivity.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Collaborative Robots Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Collaborative Robots Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Collaborative Robots Industry?

To stay informed about further developments, trends, and reports in the North America Collaborative Robots Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence