Key Insights

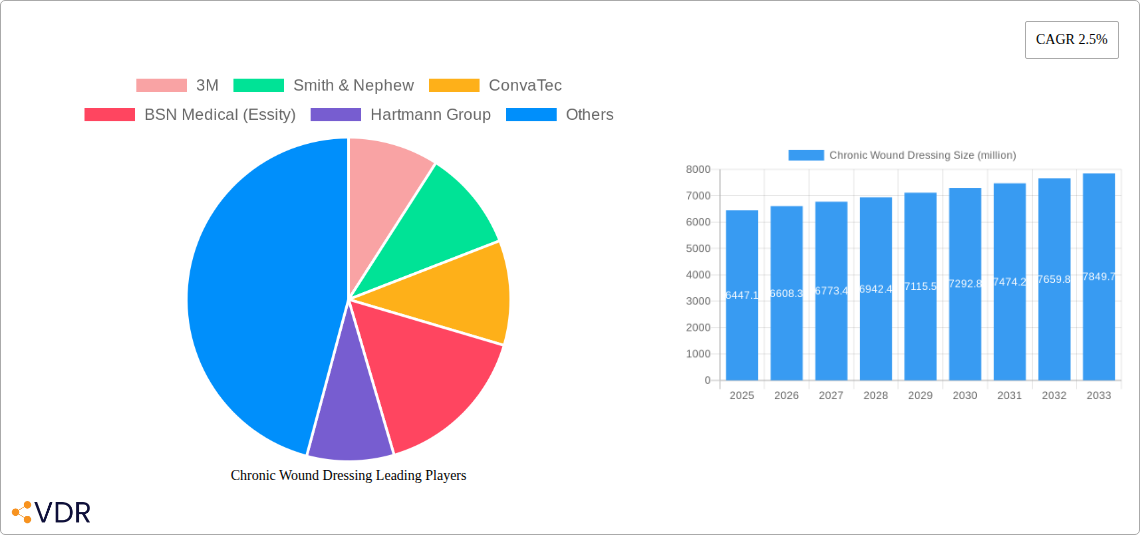

The global Chronic Wound Dressing market is poised for steady expansion, projected to reach a significant valuation of USD 6,447.1 million. This growth is underpinned by a Compound Annual Growth Rate (CAGR) of 2.5% over the forecast period from 2025 to 2033. The increasing prevalence of chronic conditions such as diabetes and an aging global population are primary drivers, leading to a higher incidence of complications like diabetic ulcers, pressure ulcers, and venous ulcers. Advancements in wound care technology are also fueling market growth, with a rising demand for innovative dressing types that promote faster healing and reduce the risk of infection. These include sophisticated hydrogel, alginate, and collagen-based dressings designed for specific wound environments.

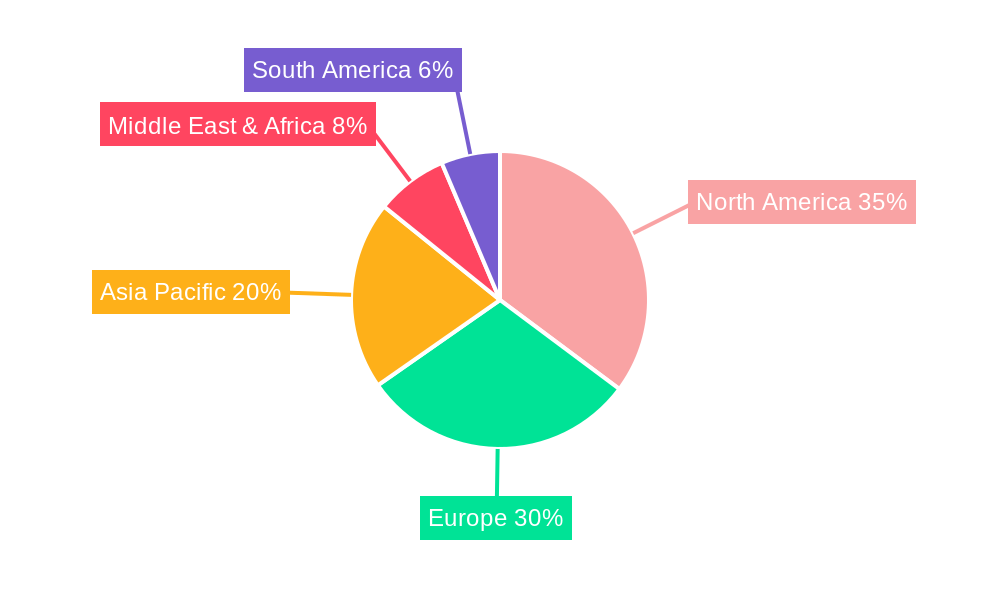

The market landscape is characterized by a competitive environment with established players like 3M, Smith & Nephew, and ConvaTec leading the way. These companies are actively investing in research and development to introduce novel wound care solutions and expand their product portfolios. The market segmentation reveals a diverse range of applications, with diabetic ulcers and pressure ulcers representing key segments due to their high prevalence. Similarly, the variety of dressing types, from traditional foam and hydrocolloid dressings to advanced hydrogel and alginate options, caters to the specific needs of different wound types and patient populations. Geographically, North America and Europe are anticipated to remain dominant markets, driven by advanced healthcare infrastructure and high healthcare spending. However, the Asia Pacific region is expected to witness robust growth due to increasing awareness of advanced wound care and a burgeoning patient base.

This in-depth market research report offers a definitive analysis of the global chronic wound dressing market, providing critical insights for stakeholders navigating this dynamic industry. Covering the period from 2019 to 2033, with a base year of 2025, this report meticulously examines market dynamics, growth trends, regional dominance, product innovation, and the strategic landscapes of key players. It delves into the intricacies of various applications, including diabetic ulcers, pressure ulcers, and venous ulcers, alongside a comprehensive breakdown of dressing types such as foam, hydrocolloid, film, alginate, hydrogel, and collagen dressings.

Chronic Wound Dressing Market Dynamics & Structure

The global chronic wound dressing market is characterized by a moderately concentrated structure, with a mix of large multinational corporations and smaller specialized manufacturers. Technological innovation serves as a primary driver, with ongoing research and development focused on advanced wound healing technologies, smart dressings, and bioengineered materials. Regulatory frameworks, including stringent FDA and EMA approvals, play a significant role in product market entry and adoption, influencing the pace of innovation and market accessibility. The threat of competitive product substitutes, while present from basic wound care products, is largely mitigated by the specialized nature and efficacy requirements of chronic wound management. End-user demographics, predominantly an aging global population and a rising incidence of chronic diseases like diabetes, are creating sustained demand. Merger and acquisition (M&A) trends are evident as larger players seek to expand their portfolios, gain market share, and acquire innovative technologies. In the historical period (2019-2024), an estimated 35 M&A deals were completed, with a total disclosed value of approximately $1.8 billion. The market concentration is estimated at around 60% by the top 10 players. Barriers to innovation include the high cost of clinical trials and the lengthy regulatory approval processes.

- Market Concentration: Moderate, with top 10 players holding approximately 60% market share.

- Technological Innovation Drivers: Advanced materials, smart dressings, bioengineered solutions, antimicrobial properties.

- Regulatory Frameworks: FDA (USA), EMA (Europe) – crucial for market access and product differentiation.

- Competitive Product Substitutes: Limited for advanced chronic wound care, but basic dressings pose some threat.

- End-User Demographics: Aging population, increasing prevalence of diabetes and cardiovascular diseases, growing healthcare expenditure.

- M&A Trends: Strategic acquisitions for portfolio expansion and technology integration.

- M&A Deal Volume (2019-2024): Approximately 35 deals.

- M&A Deal Value (2019-2024): Approximately $1.8 billion.

Chronic Wound Dressing Growth Trends & Insights

The chronic wound dressing market is poised for robust growth, driven by an expanding patient population and significant advancements in wound care technologies. The global market size is projected to grow from approximately $11.5 billion in 2024 to an estimated $20.5 billion by 2033, exhibiting a compound annual growth rate (CAGR) of around 6.8% during the forecast period (2025–2033). Adoption rates for advanced wound dressings are steadily increasing as healthcare providers and patients recognize their superior efficacy in promoting healing, reducing infection risk, and improving patient quality of life. Technological disruptions, such as the integration of antimicrobial agents, biosensors for real-time monitoring, and personalized wound management solutions, are reshaping the market landscape. Consumer behavior is shifting towards more proactive and outcome-oriented wound care, favoring dressings that offer faster healing times and reduced pain. The rising prevalence of chronic diseases like diabetes, which directly contributes to the incidence of diabetic foot ulcers, is a significant market driver. Furthermore, increased awareness campaigns and educational initiatives regarding proper wound management are contributing to higher market penetration. The development of novel drug-eluting dressings and negative pressure wound therapy (NPWT) systems continues to fuel market expansion. Market penetration for advanced dressings is estimated to increase from 45% in 2024 to approximately 65% by 2033.

Dominant Regions, Countries, or Segments in Chronic Wound Dressing

North America currently holds a dominant position in the global chronic wound dressing market, driven by a confluence of factors including a high prevalence of chronic diseases such as diabetes and pressure ulcers, advanced healthcare infrastructure, and significant investment in research and development. The United States, in particular, contributes substantially to this regional dominance. In terms of applications, Diabetic Ulcers represent the largest and fastest-growing segment, accounting for an estimated 35% of the total market share in 2025. This is directly attributable to the global epidemic of diabetes and its severe complications, leading to a significant number of chronic wound cases. Foam Dressings are the leading type of chronic wound dressing, projected to hold approximately 25% of the market share in 2025, due to their versatility, absorbency, and ability to maintain a moist wound environment.

Key drivers of dominance in North America include:

- High Prevalence of Chronic Diseases: A large and aging population coupled with high rates of diabetes, obesity, and vascular diseases fuels demand for chronic wound management solutions.

- Advanced Healthcare Infrastructure: Well-established healthcare systems and extensive network of hospitals and specialized wound care centers ensure wider access to advanced dressings.

- Reimbursement Policies: Favorable reimbursement policies for advanced wound care products in countries like the United States encourage their adoption.

- Research & Development Investments: Significant R&D expenditure by leading companies in the region leads to continuous innovation and product development.

- Technological Adoption: High receptiveness to new and innovative medical technologies accelerates the uptake of advanced wound dressings.

Within the application segments, Diabetic Ulcers are expected to maintain their lead throughout the forecast period, with an estimated market size of $4.0 billion in 2025 and projected to reach $7.3 billion by 2033. The rising global incidence of diabetes and the associated complications, such as neuropathy and poor circulation, directly contribute to the development of chronic foot ulcers, making this application a critical market segment.

Among the dressing types, Foam Dressings are projected to remain the dominant choice, with an estimated market value of $2.9 billion in 2025, expanding to $5.0 billion by 2033. Their widespread use is attributed to their excellent absorption capabilities, cushioning effect, and ability to conform to wound contours, making them suitable for a broad range of exudate levels and wound types.

Chronic Wound Dressing Product Landscape

The chronic wound dressing market is witnessing continuous innovation, focusing on advanced materials and intelligent functionalities. Product launches increasingly incorporate antimicrobial agents, such as silver or iodine, to combat infection, and growth factors to accelerate tissue regeneration. Smart dressings with embedded sensors for real-time monitoring of wound parameters like temperature, pH, and moisture levels are emerging, offering personalized treatment and early detection of complications. These advancements aim to improve patient outcomes, reduce healing times, and minimize the burden of chronic wounds.

Key Drivers, Barriers & Challenges in Chronic Wound Dressing

Key Drivers:

- Rising Prevalence of Chronic Diseases: The escalating incidence of diabetes, obesity, and vascular diseases globally directly fuels the demand for chronic wound management.

- Technological Advancements: Innovations in material science, bioengineering, and smart technologies are creating more effective and patient-friendly wound dressings.

- Aging Global Population: Older individuals are more susceptible to chronic wounds, leading to sustained market growth.

- Increased Healthcare Expenditure: Growing investment in healthcare infrastructure and wound care services globally supports market expansion.

- Growing Awareness and Education: Enhanced understanding of wound care best practices among healthcare professionals and patients drives the adoption of advanced dressings.

Key Barriers & Challenges:

- High Cost of Advanced Dressings: The premium pricing of innovative wound care products can be a barrier to adoption in resource-limited settings.

- Regulatory Hurdles: Stringent approval processes for new medical devices and dressings can delay market entry and increase development costs.

- Reimbursement Policies: Inconsistent or inadequate reimbursement policies in certain regions can limit access to advanced wound care solutions.

- Supply Chain Disruptions: Global events and logistical challenges can impact the availability and cost of raw materials and finished products.

- Competition from Traditional Dressings: While advanced dressings offer superior outcomes, basic wound care products remain a cost-effective alternative for less complex wounds.

- Lack of Skilled Personnel: Shortages of trained wound care specialists in some areas can hinder the effective utilization of advanced dressings.

Emerging Opportunities in Chronic Wound Dressing

Emerging opportunities lie in the development of cost-effective, yet highly effective, wound care solutions for developing economies. The integration of telemedicine and digital health platforms for remote wound monitoring and patient education presents a significant avenue for growth. Nanotechnology-based dressings offering targeted drug delivery and enhanced antimicrobial properties are also a promising area. Furthermore, the expansion of home healthcare services creates a burgeoning market for easy-to-use, advanced wound dressings. The increasing focus on preventive wound care for at-risk populations also presents a substantial untapped market.

Growth Accelerators in the Chronic Wound Dressing Industry

Growth in the chronic wound dressing industry will be significantly accelerated by breakthroughs in regenerative medicine, including the development of tissue-engineered skin substitutes and advanced biologic dressings that promote cellular repair and tissue regeneration. Strategic partnerships between wound care companies and academic research institutions will foster a pipeline of novel technologies. Market expansion into emerging economies, driven by increasing healthcare access and rising disposable incomes, will provide substantial growth impetus. The development of personalized wound management strategies, tailored to individual patient needs and wound characteristics, will also be a key accelerator.

Key Players Shaping the Chronic Wound Dressing Market

- 3M

- Smith & Nephew

- ConvaTec

- BSN Medical (Essity)

- Hartmann Group

- Coloplast

- Cardinal Health

- Molnlycke Health Care

- Medline Industries

- B. Braun

- Integra LifeSciences

- Hollister Incorporated

- Nitto Denko

- Urgo Group

- Winner Medical

- Lohmann & Rauscher

- Advanced Medical Solutions

- Genewel

Notable Milestones in Chronic Wound Dressing Sector

- 2020: Launch of advanced antimicrobial foam dressings by leading companies, enhancing infection control.

- 2021: Increased investment in R&D for smart wound dressings with embedded sensors.

- 2022: Emergence of bioengineered skin substitutes showing promising results in clinical trials.

- 2023: Strategic acquisitions aimed at consolidating market share and expanding product portfolios in advanced wound care.

- 2024: Growing focus on sustainable wound dressing materials and manufacturing processes.

In-Depth Chronic Wound Dressing Market Outlook

- 2020: Launch of advanced antimicrobial foam dressings by leading companies, enhancing infection control.

- 2021: Increased investment in R&D for smart wound dressings with embedded sensors.

- 2022: Emergence of bioengineered skin substitutes showing promising results in clinical trials.

- 2023: Strategic acquisitions aimed at consolidating market share and expanding product portfolios in advanced wound care.

- 2024: Growing focus on sustainable wound dressing materials and manufacturing processes.

In-Depth Chronic Wound Dressing Market Outlook

The future of the chronic wound dressing market is exceptionally bright, fueled by ongoing demographic shifts and relentless technological innovation. The growing global burden of chronic diseases, particularly diabetes, will continue to be a primary demand driver. Advancements in regenerative medicine, nanotechnology, and smart dressing technology are poised to revolutionize wound management, offering more efficient healing, reduced complications, and improved patient quality of life. Strategic collaborations and market expansion into underserved regions will further accelerate growth. Stakeholders can anticipate sustained growth and significant opportunities in this critical healthcare sector.

Chronic Wound Dressing Segmentation

-

1. Application

- 1.1. Diabetic Ulcers

- 1.2. Pressure Ulcers

- 1.3. Venous Ulcers

- 1.4. Other Chronic Wounds

-

2. Types

- 2.1. Foam Dressing

- 2.2. Hydrocolloid Dressing

- 2.3. Film Dressing

- 2.4. Alginate Dressing

- 2.5. Hydrogel Dressing

- 2.6. Collagen Dressing

- 2.7. Others

Chronic Wound Dressing Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Chronic Wound Dressing REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 2.5% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Chronic Wound Dressing Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Diabetic Ulcers

- 5.1.2. Pressure Ulcers

- 5.1.3. Venous Ulcers

- 5.1.4. Other Chronic Wounds

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Foam Dressing

- 5.2.2. Hydrocolloid Dressing

- 5.2.3. Film Dressing

- 5.2.4. Alginate Dressing

- 5.2.5. Hydrogel Dressing

- 5.2.6. Collagen Dressing

- 5.2.7. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Chronic Wound Dressing Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Diabetic Ulcers

- 6.1.2. Pressure Ulcers

- 6.1.3. Venous Ulcers

- 6.1.4. Other Chronic Wounds

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Foam Dressing

- 6.2.2. Hydrocolloid Dressing

- 6.2.3. Film Dressing

- 6.2.4. Alginate Dressing

- 6.2.5. Hydrogel Dressing

- 6.2.6. Collagen Dressing

- 6.2.7. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Chronic Wound Dressing Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Diabetic Ulcers

- 7.1.2. Pressure Ulcers

- 7.1.3. Venous Ulcers

- 7.1.4. Other Chronic Wounds

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Foam Dressing

- 7.2.2. Hydrocolloid Dressing

- 7.2.3. Film Dressing

- 7.2.4. Alginate Dressing

- 7.2.5. Hydrogel Dressing

- 7.2.6. Collagen Dressing

- 7.2.7. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Chronic Wound Dressing Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Diabetic Ulcers

- 8.1.2. Pressure Ulcers

- 8.1.3. Venous Ulcers

- 8.1.4. Other Chronic Wounds

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Foam Dressing

- 8.2.2. Hydrocolloid Dressing

- 8.2.3. Film Dressing

- 8.2.4. Alginate Dressing

- 8.2.5. Hydrogel Dressing

- 8.2.6. Collagen Dressing

- 8.2.7. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Chronic Wound Dressing Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Diabetic Ulcers

- 9.1.2. Pressure Ulcers

- 9.1.3. Venous Ulcers

- 9.1.4. Other Chronic Wounds

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Foam Dressing

- 9.2.2. Hydrocolloid Dressing

- 9.2.3. Film Dressing

- 9.2.4. Alginate Dressing

- 9.2.5. Hydrogel Dressing

- 9.2.6. Collagen Dressing

- 9.2.7. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Chronic Wound Dressing Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Diabetic Ulcers

- 10.1.2. Pressure Ulcers

- 10.1.3. Venous Ulcers

- 10.1.4. Other Chronic Wounds

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Foam Dressing

- 10.2.2. Hydrocolloid Dressing

- 10.2.3. Film Dressing

- 10.2.4. Alginate Dressing

- 10.2.5. Hydrogel Dressing

- 10.2.6. Collagen Dressing

- 10.2.7. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 3M

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Smith & Nephew

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 ConvaTec

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 BSN Medical (Essity)

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Hartmann Group

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Coloplast

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Cardinal Health

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Molnlycke Health Care

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Medline Industries

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 B.Braun

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Integra LifeSciences

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Hollister Incorporated

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Nitto Denko

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Urgo Group

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Winner Medical

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Lohmann & Rauscher

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Advanced Medical Solutions

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Genewel

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.1 3M

List of Figures

- Figure 1: Global Chronic Wound Dressing Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Chronic Wound Dressing Revenue (million), by Application 2024 & 2032

- Figure 3: North America Chronic Wound Dressing Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Chronic Wound Dressing Revenue (million), by Types 2024 & 2032

- Figure 5: North America Chronic Wound Dressing Revenue Share (%), by Types 2024 & 2032

- Figure 6: North America Chronic Wound Dressing Revenue (million), by Country 2024 & 2032

- Figure 7: North America Chronic Wound Dressing Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Chronic Wound Dressing Revenue (million), by Application 2024 & 2032

- Figure 9: South America Chronic Wound Dressing Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Chronic Wound Dressing Revenue (million), by Types 2024 & 2032

- Figure 11: South America Chronic Wound Dressing Revenue Share (%), by Types 2024 & 2032

- Figure 12: South America Chronic Wound Dressing Revenue (million), by Country 2024 & 2032

- Figure 13: South America Chronic Wound Dressing Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Chronic Wound Dressing Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Chronic Wound Dressing Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Chronic Wound Dressing Revenue (million), by Types 2024 & 2032

- Figure 17: Europe Chronic Wound Dressing Revenue Share (%), by Types 2024 & 2032

- Figure 18: Europe Chronic Wound Dressing Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Chronic Wound Dressing Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Chronic Wound Dressing Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Chronic Wound Dressing Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Chronic Wound Dressing Revenue (million), by Types 2024 & 2032

- Figure 23: Middle East & Africa Chronic Wound Dressing Revenue Share (%), by Types 2024 & 2032

- Figure 24: Middle East & Africa Chronic Wound Dressing Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Chronic Wound Dressing Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Chronic Wound Dressing Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Chronic Wound Dressing Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Chronic Wound Dressing Revenue (million), by Types 2024 & 2032

- Figure 29: Asia Pacific Chronic Wound Dressing Revenue Share (%), by Types 2024 & 2032

- Figure 30: Asia Pacific Chronic Wound Dressing Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Chronic Wound Dressing Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Chronic Wound Dressing Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Chronic Wound Dressing Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Chronic Wound Dressing Revenue million Forecast, by Types 2019 & 2032

- Table 4: Global Chronic Wound Dressing Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Chronic Wound Dressing Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Chronic Wound Dressing Revenue million Forecast, by Types 2019 & 2032

- Table 7: Global Chronic Wound Dressing Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Chronic Wound Dressing Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Chronic Wound Dressing Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Chronic Wound Dressing Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Chronic Wound Dressing Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Chronic Wound Dressing Revenue million Forecast, by Types 2019 & 2032

- Table 13: Global Chronic Wound Dressing Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Chronic Wound Dressing Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Chronic Wound Dressing Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Chronic Wound Dressing Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Chronic Wound Dressing Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Chronic Wound Dressing Revenue million Forecast, by Types 2019 & 2032

- Table 19: Global Chronic Wound Dressing Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Chronic Wound Dressing Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Chronic Wound Dressing Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Chronic Wound Dressing Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Chronic Wound Dressing Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Chronic Wound Dressing Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Chronic Wound Dressing Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Chronic Wound Dressing Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Chronic Wound Dressing Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Chronic Wound Dressing Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Chronic Wound Dressing Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Chronic Wound Dressing Revenue million Forecast, by Types 2019 & 2032

- Table 31: Global Chronic Wound Dressing Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Chronic Wound Dressing Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Chronic Wound Dressing Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Chronic Wound Dressing Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Chronic Wound Dressing Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Chronic Wound Dressing Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Chronic Wound Dressing Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Chronic Wound Dressing Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Chronic Wound Dressing Revenue million Forecast, by Types 2019 & 2032

- Table 40: Global Chronic Wound Dressing Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Chronic Wound Dressing Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Chronic Wound Dressing Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Chronic Wound Dressing Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Chronic Wound Dressing Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Chronic Wound Dressing Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Chronic Wound Dressing Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Chronic Wound Dressing Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Chronic Wound Dressing?

The projected CAGR is approximately 2.5%.

2. Which companies are prominent players in the Chronic Wound Dressing?

Key companies in the market include 3M, Smith & Nephew, ConvaTec, BSN Medical (Essity), Hartmann Group, Coloplast, Cardinal Health, Molnlycke Health Care, Medline Industries, B.Braun, Integra LifeSciences, Hollister Incorporated, Nitto Denko, Urgo Group, Winner Medical, Lohmann & Rauscher, Advanced Medical Solutions, Genewel.

3. What are the main segments of the Chronic Wound Dressing?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 6447.1 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Chronic Wound Dressing," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Chronic Wound Dressing report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Chronic Wound Dressing?

To stay informed about further developments, trends, and reports in the Chronic Wound Dressing, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence