Key Insights

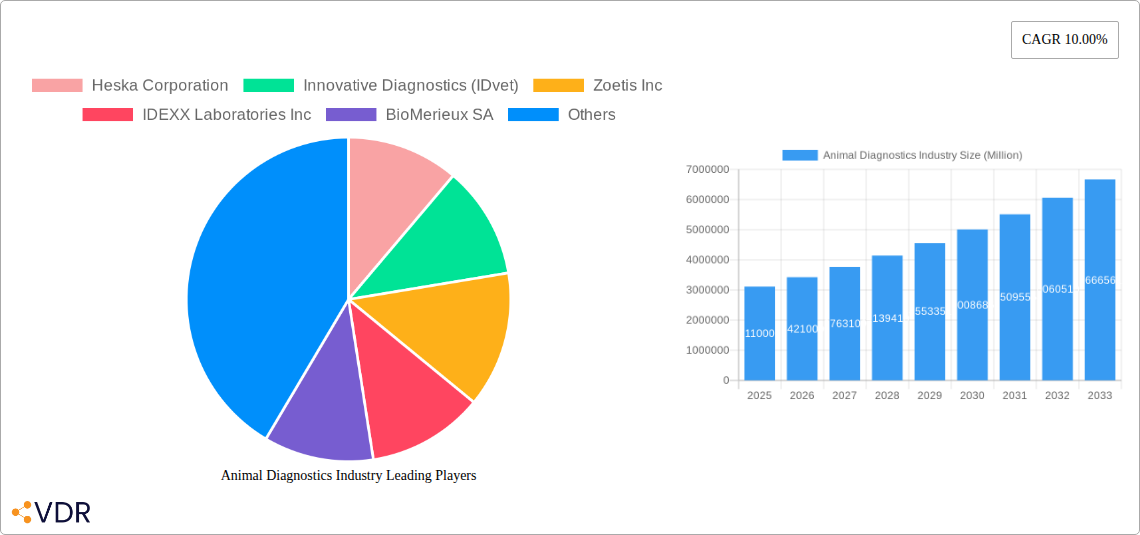

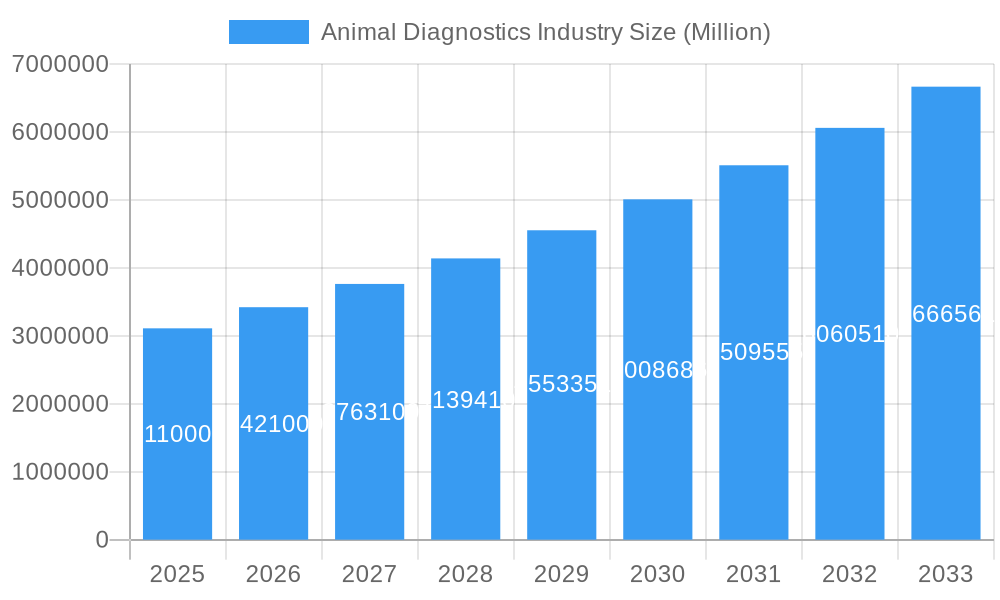

The global Animal Diagnostics market is experiencing robust growth, projected to reach approximately $3.11 million in value units, with a compelling Compound Annual Growth Rate (CAGR) of 10.00% from 2025 to 2033. This expansion is primarily fueled by a confluence of critical drivers, including the increasing pet humanization trend, leading to greater investment in companion animal health and advanced veterinary care. Furthermore, the rising incidence of zoonotic diseases, emphasizing the interconnectedness of animal and human health, alongside the growing demand for rapid and accurate diagnostic solutions in livestock farming to ensure food safety and productivity, are significant contributors. Technological advancements, such as the proliferation of point-of-care diagnostic devices and the integration of artificial intelligence in interpreting diagnostic results, are also revolutionizing the industry, making diagnostics more accessible and efficient for veterinarians and pet owners alike.

Animal Diagnostics Industry Market Size (In Million)

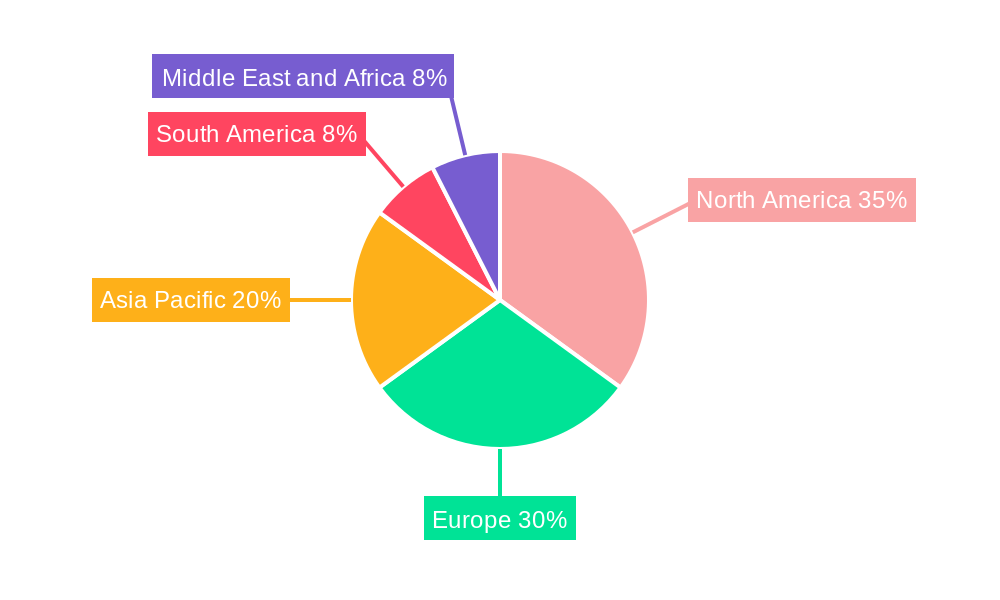

The market is segmented across key areas, with strong demand anticipated in the "Dogs" and "Cats" animal segments, reflecting the dominant pet ownership trends. In terms of application, "Bacteriology" and "Clinical Pathology" are expected to lead, driven by the need for early disease detection and comprehensive health assessments. The "Immunodiagnostic Tests" and "Molecular Diagnostics" technologies are at the forefront of innovation, offering high sensitivity and specificity for a wide range of diagnostic challenges. Geographically, North America and Europe currently hold significant market shares due to advanced veterinary infrastructure and high disposable incomes dedicated to pet care. However, the Asia Pacific region is poised for substantial growth, driven by increasing pet ownership, a burgeoning livestock industry, and rising awareness of animal health management. Key players like Zoetis Inc., IDEXX Laboratories Inc., and Heska Corporation are actively innovating and expanding their product portfolios to cater to these evolving market demands, consolidating their positions through strategic partnerships and acquisitions.

Animal Diagnostics Industry Company Market Share

Animal Diagnostics Market: Comprehensive Report 2024-2033 - Growth, Trends, and Key Players

Unlock critical insights into the rapidly evolving global animal diagnostics market. This in-depth report provides a detailed analysis of market dynamics, growth trajectories, and competitive landscapes from 2019 to 2033, with a base and estimated year of 2025. With a focus on high-traffic keywords such as "veterinary diagnostics," "animal health testing," "pet diagnostics," and "livestock disease detection," this report is essential for manufacturers, veterinary professionals, researchers, and investors seeking to capitalize on lucrative opportunities in the animal health sector. Explore parent and child market segments, including diagnostics for cats, dogs, and other animals, and delve into applications spanning bacteriology, parasitology, and clinical pathology. Understand the impact of cutting-edge technologies like immunodiagnostic tests and molecular diagnostics, and gain a competitive edge by analyzing market trends, drivers, barriers, and emerging opportunities.

Animal Diagnostics Industry Market Dynamics & Structure

The global animal diagnostics market is characterized by a moderate level of concentration, with key players like Zoetis Inc., IDEXX Laboratories Inc., and Heska Corporation holding significant market shares. Technological innovation is a primary driver, fueled by advancements in molecular diagnostics, point-of-care testing, and AI-powered diagnostic imaging, enabling earlier and more accurate disease detection in both companion animals and livestock. The evolving regulatory frameworks, particularly concerning animal welfare and food safety, also shape market strategies. Competitive product substitutes are emerging, especially in the form of at-home testing kits and advanced imaging techniques. End-user demographics are shifting, with increasing pet humanization leading to higher spending on pet healthcare and diagnostics, alongside a growing demand for efficient and cost-effective diagnostics in commercial animal agriculture. Mergers and acquisitions (M&A) are a recurring trend, with companies seeking to expand their product portfolios, geographic reach, and technological capabilities. For instance, the acquisition of Antech Diagnostics by Mars Petcare in 2019 was a significant move in consolidating market presence.

- Market Concentration: Moderate, with a few major players dominating the landscape.

- Technological Innovation Drivers: Molecular diagnostics, point-of-care testing, AI, advanced imaging.

- Regulatory Frameworks: Stringent regulations for animal welfare and food safety, driving demand for reliable diagnostics.

- Competitive Product Substitutes: Home testing kits, advanced imaging, multiplex assays.

- End-User Demographics: Rising pet humanization, increased disposable income, growing awareness of zoonotic diseases.

- M&A Trends: Strategic acquisitions for portfolio expansion and market consolidation.

Animal Diagnostics Industry Growth Trends & Insights

The animal diagnostics market is experiencing robust growth, projected to expand at a significant Compound Annual Growth Rate (CAGR) of approximately 7.5% from 2019 to 2033. This expansion is propelled by a confluence of factors, including the escalating prevalence of zoonotic diseases, a growing global pet population, and a heightened awareness among pet owners and livestock producers regarding the importance of early disease detection and preventative care. The trend of pet humanization, where pets are increasingly viewed as integral family members, has led to greater investment in veterinary care, including advanced diagnostic services. Furthermore, technological advancements are revolutionizing the field, making diagnostics more accessible, accurate, and faster. Molecular diagnostics, for example, is witnessing rapid adoption for infectious disease detection, offering higher sensitivity and specificity compared to traditional methods. The increasing demand for rapid diagnostic tests (RDTs) that provide results at the point of care is also a major growth driver, enabling veterinarians to make quicker clinical decisions and initiate timely treatment.

The adoption rates for advanced diagnostic technologies are steadily increasing across both veterinary clinics and diagnostic laboratories. This surge is supported by the development of more user-friendly instruments and the availability of comprehensive test menus. For instance, the introduction of multiplex assays that can detect multiple pathogens simultaneously is gaining traction, improving efficiency and reducing costs. Consumer behavior shifts are also evident, with pet owners actively seeking out services that offer advanced diagnostics, reflecting a willingness to invest in their pets' well-being. In the livestock sector, the focus on herd health management and biosecurity, driven by concerns over food security and the economic impact of disease outbreaks, is spurring the adoption of sophisticated diagnostic tools for disease surveillance and outbreak management. The market penetration of specific diagnostic technologies, such as immunoassay-based tests for antibody and antigen detection, remains high due to their cost-effectiveness and reliability. However, molecular diagnostics, particularly PCR-based tests, are experiencing a substantial growth spurt due to their unparalleled sensitivity and ability to detect nucleic acids of pathogens, even at low concentrations.

Dominant Regions, Countries, or Segments in Animal Diagnostics Industry

North America currently holds a dominant position in the global animal diagnostics market, driven by a highly developed veterinary infrastructure, a large and affluent pet population, and significant investments in animal health research and development. The United States, in particular, exhibits a high level of pet ownership and a strong emphasis on preventative veterinary care, leading to substantial demand for a wide range of diagnostic services, including clinical pathology, bacteriology, and parasitology. The presence of leading animal diagnostics companies like IDEXX Laboratories Inc. and Zoetis Inc. in this region further solidifies its leadership. Furthermore, stringent regulations regarding food safety and animal welfare in North America incentivize the widespread adoption of advanced diagnostic technologies in the livestock sector.

Europe follows closely, characterized by a similar trend of increasing pet ownership and a growing awareness of animal health. Countries like Germany, the UK, and France are key contributors to the European market, with robust veterinary networks and a proactive approach to disease surveillance. The region benefits from significant research initiatives and a strong presence of both multinational and specialized European diagnostic companies such as BioMerieux SA and Randox Laboratories Ltd. Asia-Pacific is emerging as a high-growth region, fueled by a rapidly expanding middle class, increasing disposable incomes, and a growing pet population in countries like China and India. The livestock sector in this region is also undergoing modernization, with a greater focus on disease control and productivity, thereby boosting the demand for animal diagnostics.

Within the segmentation, Dogs represent a leading segment within the animal diagnostics market due to their status as the most popular pet globally and the high willingness of owners to spend on their health. Applications such as Clinical Pathology, encompassing hematology, clinical chemistry, and urinalysis, are also dominant, forming the backbone of routine veterinary diagnostics. In terms of technology, Immunodiagnostic Tests, including ELISA and lateral flow assays, continue to be widely adopted due to their cost-effectiveness, speed, and versatility in detecting antibodies and antigens.

Animal Diagnostics Industry Product Landscape

The product landscape in the animal diagnostics industry is characterized by continuous innovation aimed at enhancing accuracy, speed, and user-friendliness. Manufacturers are actively developing advanced immunoassay platforms for rapid detection of infectious diseases and biomarkers, alongside sophisticated molecular diagnostic kits utilizing PCR and next-generation sequencing for precise pathogen identification. Diagnostic imaging technologies, including portable ultrasound and digital radiography, are becoming more accessible and integrated into veterinary practices, offering non-invasive diagnostic capabilities. The unique selling proposition of many new products lies in their ability to provide point-of-care results, enabling immediate clinical decision-making. Technological advancements are focused on miniaturization, automation, and cloud-based data management solutions, facilitating seamless integration into veterinary workflows and improving patient outcomes.

Key Drivers, Barriers & Challenges in Animal Diagnostics Industry

Key Drivers:

- Rising Pet Humanization: Increased emotional and financial investment in companion animal health drives demand for advanced diagnostics.

- Growing Awareness of Zoonotic Diseases: Public health concerns and the interconnectedness of human and animal health necessitate robust disease surveillance.

- Technological Advancements: Innovations in molecular diagnostics, AI, and point-of-care testing are expanding capabilities and accessibility.

- Demand for Food Safety and Security: Growing global population fuels the need for efficient livestock diagnostics to ensure healthy animal populations.

- Economic Growth and Increased Disposable Income: Enables greater spending on veterinary care and diagnostics in both developed and emerging economies.

Key Barriers & Challenges:

- High Cost of Advanced Technologies: The initial investment for sophisticated diagnostic equipment and reagents can be prohibitive for some veterinary practices and emerging markets.

- Regulatory Hurdles: Obtaining approvals for new diagnostic tests and devices can be a lengthy and complex process, impacting time-to-market.

- Limited Skilled Veterinary Professionals: A shortage of trained personnel to operate advanced diagnostic equipment and interpret results can hinder adoption.

- Data Integration and Standardization: Challenges in integrating data from various diagnostic platforms and ensuring interoperability can affect comprehensive patient management.

- Supply Chain Disruptions: Global events can impact the availability and cost of essential reagents and consumables.

Emerging Opportunities in Animal Diagnostics Industry

Emerging opportunities in the animal diagnostics industry are primarily driven by the expansion of point-of-care testing, the growing demand for companion animal genetic testing, and the development of novel diagnostics for non-infectious diseases. The increasing popularity of telehealth and at-home pet care services presents a significant avenue for the development and distribution of user-friendly diagnostic kits that can be utilized by pet owners under veterinary guidance. Furthermore, the burgeoning field of microbiome analysis in animals offers a new frontier for understanding gut health and developing targeted nutritional and therapeutic interventions. The integration of artificial intelligence and machine learning for predictive diagnostics and personalized treatment plans is another promising area, enabling earlier identification of at-risk animals and optimizing therapeutic strategies.

Growth Accelerators in the Animal Diagnostics Industry Industry

Several key catalysts are accelerating the growth of the animal diagnostics industry. Technological breakthroughs in areas such as CRISPR-based diagnostics and liquid biopsy are paving the way for highly sensitive and non-invasive diagnostic methods. Strategic partnerships between diagnostic companies, veterinary pharmaceutical firms, and technology providers are fostering innovation and expanding market reach. For example, collaborations focused on developing integrated diagnostic and therapeutic solutions are gaining traction. Furthermore, the expansion of veterinary services into underserved markets, coupled with increasing government initiatives promoting animal health and biosecurity, are significant growth accelerators. The growing trend of pet insurance also indirectly fuels the demand for diagnostics by making advanced veterinary care more accessible to pet owners.

Key Players Shaping the Animal Diagnostics Industry Market

- Heska Corporation

- Innovative Diagnostics (IDvet)

- Zoetis Inc

- IDEXX Laboratories Inc

- BioMerieux SA

- Randox Laboratories Ltd

- Chembio Diagnostic Systems Inc

- Thermo Fisher Scientific Inc

- Indical Bioscience GmbH

- Creative Diagnostics

- Agrolabo SpA

- Virbac

- Neogen Corporation

Notable Milestones in Animal Diagnostics Industry Sector

- August 2022: PepiPets launched a new mobile diagnostic testing service, enhancing at-home diagnostic testing accessibility for pets.

- January 2022: Idexx Laboratories, Inc. announced significant product and service enhancements, including the IDEXX 4Dx Plus Test, VetConnectPLUS Mobile App, SediVue Dx Urine Sediment Analyzer, and New Catalyst SDMA Test, aimed at improving veterinary practice efficiency and enabling faster, more confident clinical decisions.

In-Depth Animal Diagnostics Industry Market Outlook

The future outlook for the animal diagnostics industry is exceptionally positive, driven by continued technological innovation and a sustained increase in global pet ownership and investment in animal health. The market will likely witness a greater integration of AI and machine learning for predictive analytics and personalized medicine, while point-of-care diagnostics will become even more sophisticated and accessible. Emerging applications in areas like companion animal genetics and microbiome analysis will open up new revenue streams. Furthermore, the ongoing emphasis on zoonotic disease prevention and food safety will maintain strong demand for robust livestock diagnostics. Strategic collaborations and market expansion into emerging economies are expected to be key growth strategies for leading players, solidifying the industry's trajectory as a vital component of global health and well-being.

Animal Diagnostics Industry Segmentation

-

1. Animals

- 1.1. Cats

- 1.2. Dogs

- 1.3. Other Animals

-

2. Application

- 2.1. Bacteriology

- 2.2. Parasitology

- 2.3. Clinical Pathology

- 2.4. Other Applications

-

3. Technology

- 3.1. Immunodiagnostic Tests

- 3.2. Molecular Diagnostics

- 3.3. Diagnostic Imaging

- 3.4. Other Diagnostics

Animal Diagnostics Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Animal Diagnostics Industry Regional Market Share

Geographic Coverage of Animal Diagnostics Industry

Animal Diagnostics Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.00% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Animals

- 5.1.1. Cats

- 5.1.2. Dogs

- 5.1.3. Other Animals

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Bacteriology

- 5.2.2. Parasitology

- 5.2.3. Clinical Pathology

- 5.2.4. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Technology

- 5.3.1. Immunodiagnostic Tests

- 5.3.2. Molecular Diagnostics

- 5.3.3. Diagnostic Imaging

- 5.3.4. Other Diagnostics

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Middle East and Africa

- 5.4.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Animals

- 6. Global Animal Diagnostics Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Animals

- 6.1.1. Cats

- 6.1.2. Dogs

- 6.1.3. Other Animals

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Bacteriology

- 6.2.2. Parasitology

- 6.2.3. Clinical Pathology

- 6.2.4. Other Applications

- 6.3. Market Analysis, Insights and Forecast - by Technology

- 6.3.1. Immunodiagnostic Tests

- 6.3.2. Molecular Diagnostics

- 6.3.3. Diagnostic Imaging

- 6.3.4. Other Diagnostics

- 6.1. Market Analysis, Insights and Forecast - by Animals

- 7. North America Animal Diagnostics Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Animals

- 7.1.1. Cats

- 7.1.2. Dogs

- 7.1.3. Other Animals

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Bacteriology

- 7.2.2. Parasitology

- 7.2.3. Clinical Pathology

- 7.2.4. Other Applications

- 7.3. Market Analysis, Insights and Forecast - by Technology

- 7.3.1. Immunodiagnostic Tests

- 7.3.2. Molecular Diagnostics

- 7.3.3. Diagnostic Imaging

- 7.3.4. Other Diagnostics

- 7.1. Market Analysis, Insights and Forecast - by Animals

- 8. Europe Animal Diagnostics Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Animals

- 8.1.1. Cats

- 8.1.2. Dogs

- 8.1.3. Other Animals

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Bacteriology

- 8.2.2. Parasitology

- 8.2.3. Clinical Pathology

- 8.2.4. Other Applications

- 8.3. Market Analysis, Insights and Forecast - by Technology

- 8.3.1. Immunodiagnostic Tests

- 8.3.2. Molecular Diagnostics

- 8.3.3. Diagnostic Imaging

- 8.3.4. Other Diagnostics

- 8.1. Market Analysis, Insights and Forecast - by Animals

- 9. Asia Pacific Animal Diagnostics Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Animals

- 9.1.1. Cats

- 9.1.2. Dogs

- 9.1.3. Other Animals

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Bacteriology

- 9.2.2. Parasitology

- 9.2.3. Clinical Pathology

- 9.2.4. Other Applications

- 9.3. Market Analysis, Insights and Forecast - by Technology

- 9.3.1. Immunodiagnostic Tests

- 9.3.2. Molecular Diagnostics

- 9.3.3. Diagnostic Imaging

- 9.3.4. Other Diagnostics

- 9.1. Market Analysis, Insights and Forecast - by Animals

- 10. Middle East and Africa Animal Diagnostics Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Animals

- 10.1.1. Cats

- 10.1.2. Dogs

- 10.1.3. Other Animals

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Bacteriology

- 10.2.2. Parasitology

- 10.2.3. Clinical Pathology

- 10.2.4. Other Applications

- 10.3. Market Analysis, Insights and Forecast - by Technology

- 10.3.1. Immunodiagnostic Tests

- 10.3.2. Molecular Diagnostics

- 10.3.3. Diagnostic Imaging

- 10.3.4. Other Diagnostics

- 10.1. Market Analysis, Insights and Forecast - by Animals

- 11. South America Animal Diagnostics Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Animals

- 11.1.1. Cats

- 11.1.2. Dogs

- 11.1.3. Other Animals

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Bacteriology

- 11.2.2. Parasitology

- 11.2.3. Clinical Pathology

- 11.2.4. Other Applications

- 11.3. Market Analysis, Insights and Forecast - by Technology

- 11.3.1. Immunodiagnostic Tests

- 11.3.2. Molecular Diagnostics

- 11.3.3. Diagnostic Imaging

- 11.3.4. Other Diagnostics

- 11.1. Market Analysis, Insights and Forecast - by Animals

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Heska Corporation

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Innovative Diagnostics (IDvet)

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Zoetis Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 IDEXX Laboratories Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 BioMerieux SA

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Randox Laboratories Ltd

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Chembio Diagnostic Systems Inc

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Thermo Fisher Scientific Inc

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Indical Bioscience GmbH

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Creative Diagnostics

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Agrolabo SpA

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Virbac

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Neogen Corporation

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.1 Heska Corporation

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Animal Diagnostics Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global Animal Diagnostics Industry Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America Animal Diagnostics Industry Revenue (Million), by Animals 2025 & 2033

- Figure 4: North America Animal Diagnostics Industry Volume (K Unit), by Animals 2025 & 2033

- Figure 5: North America Animal Diagnostics Industry Revenue Share (%), by Animals 2025 & 2033

- Figure 6: North America Animal Diagnostics Industry Volume Share (%), by Animals 2025 & 2033

- Figure 7: North America Animal Diagnostics Industry Revenue (Million), by Application 2025 & 2033

- Figure 8: North America Animal Diagnostics Industry Volume (K Unit), by Application 2025 & 2033

- Figure 9: North America Animal Diagnostics Industry Revenue Share (%), by Application 2025 & 2033

- Figure 10: North America Animal Diagnostics Industry Volume Share (%), by Application 2025 & 2033

- Figure 11: North America Animal Diagnostics Industry Revenue (Million), by Technology 2025 & 2033

- Figure 12: North America Animal Diagnostics Industry Volume (K Unit), by Technology 2025 & 2033

- Figure 13: North America Animal Diagnostics Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 14: North America Animal Diagnostics Industry Volume Share (%), by Technology 2025 & 2033

- Figure 15: North America Animal Diagnostics Industry Revenue (Million), by Country 2025 & 2033

- Figure 16: North America Animal Diagnostics Industry Volume (K Unit), by Country 2025 & 2033

- Figure 17: North America Animal Diagnostics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: North America Animal Diagnostics Industry Volume Share (%), by Country 2025 & 2033

- Figure 19: Europe Animal Diagnostics Industry Revenue (Million), by Animals 2025 & 2033

- Figure 20: Europe Animal Diagnostics Industry Volume (K Unit), by Animals 2025 & 2033

- Figure 21: Europe Animal Diagnostics Industry Revenue Share (%), by Animals 2025 & 2033

- Figure 22: Europe Animal Diagnostics Industry Volume Share (%), by Animals 2025 & 2033

- Figure 23: Europe Animal Diagnostics Industry Revenue (Million), by Application 2025 & 2033

- Figure 24: Europe Animal Diagnostics Industry Volume (K Unit), by Application 2025 & 2033

- Figure 25: Europe Animal Diagnostics Industry Revenue Share (%), by Application 2025 & 2033

- Figure 26: Europe Animal Diagnostics Industry Volume Share (%), by Application 2025 & 2033

- Figure 27: Europe Animal Diagnostics Industry Revenue (Million), by Technology 2025 & 2033

- Figure 28: Europe Animal Diagnostics Industry Volume (K Unit), by Technology 2025 & 2033

- Figure 29: Europe Animal Diagnostics Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 30: Europe Animal Diagnostics Industry Volume Share (%), by Technology 2025 & 2033

- Figure 31: Europe Animal Diagnostics Industry Revenue (Million), by Country 2025 & 2033

- Figure 32: Europe Animal Diagnostics Industry Volume (K Unit), by Country 2025 & 2033

- Figure 33: Europe Animal Diagnostics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Europe Animal Diagnostics Industry Volume Share (%), by Country 2025 & 2033

- Figure 35: Asia Pacific Animal Diagnostics Industry Revenue (Million), by Animals 2025 & 2033

- Figure 36: Asia Pacific Animal Diagnostics Industry Volume (K Unit), by Animals 2025 & 2033

- Figure 37: Asia Pacific Animal Diagnostics Industry Revenue Share (%), by Animals 2025 & 2033

- Figure 38: Asia Pacific Animal Diagnostics Industry Volume Share (%), by Animals 2025 & 2033

- Figure 39: Asia Pacific Animal Diagnostics Industry Revenue (Million), by Application 2025 & 2033

- Figure 40: Asia Pacific Animal Diagnostics Industry Volume (K Unit), by Application 2025 & 2033

- Figure 41: Asia Pacific Animal Diagnostics Industry Revenue Share (%), by Application 2025 & 2033

- Figure 42: Asia Pacific Animal Diagnostics Industry Volume Share (%), by Application 2025 & 2033

- Figure 43: Asia Pacific Animal Diagnostics Industry Revenue (Million), by Technology 2025 & 2033

- Figure 44: Asia Pacific Animal Diagnostics Industry Volume (K Unit), by Technology 2025 & 2033

- Figure 45: Asia Pacific Animal Diagnostics Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 46: Asia Pacific Animal Diagnostics Industry Volume Share (%), by Technology 2025 & 2033

- Figure 47: Asia Pacific Animal Diagnostics Industry Revenue (Million), by Country 2025 & 2033

- Figure 48: Asia Pacific Animal Diagnostics Industry Volume (K Unit), by Country 2025 & 2033

- Figure 49: Asia Pacific Animal Diagnostics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Asia Pacific Animal Diagnostics Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: Middle East and Africa Animal Diagnostics Industry Revenue (Million), by Animals 2025 & 2033

- Figure 52: Middle East and Africa Animal Diagnostics Industry Volume (K Unit), by Animals 2025 & 2033

- Figure 53: Middle East and Africa Animal Diagnostics Industry Revenue Share (%), by Animals 2025 & 2033

- Figure 54: Middle East and Africa Animal Diagnostics Industry Volume Share (%), by Animals 2025 & 2033

- Figure 55: Middle East and Africa Animal Diagnostics Industry Revenue (Million), by Application 2025 & 2033

- Figure 56: Middle East and Africa Animal Diagnostics Industry Volume (K Unit), by Application 2025 & 2033

- Figure 57: Middle East and Africa Animal Diagnostics Industry Revenue Share (%), by Application 2025 & 2033

- Figure 58: Middle East and Africa Animal Diagnostics Industry Volume Share (%), by Application 2025 & 2033

- Figure 59: Middle East and Africa Animal Diagnostics Industry Revenue (Million), by Technology 2025 & 2033

- Figure 60: Middle East and Africa Animal Diagnostics Industry Volume (K Unit), by Technology 2025 & 2033

- Figure 61: Middle East and Africa Animal Diagnostics Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 62: Middle East and Africa Animal Diagnostics Industry Volume Share (%), by Technology 2025 & 2033

- Figure 63: Middle East and Africa Animal Diagnostics Industry Revenue (Million), by Country 2025 & 2033

- Figure 64: Middle East and Africa Animal Diagnostics Industry Volume (K Unit), by Country 2025 & 2033

- Figure 65: Middle East and Africa Animal Diagnostics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 66: Middle East and Africa Animal Diagnostics Industry Volume Share (%), by Country 2025 & 2033

- Figure 67: South America Animal Diagnostics Industry Revenue (Million), by Animals 2025 & 2033

- Figure 68: South America Animal Diagnostics Industry Volume (K Unit), by Animals 2025 & 2033

- Figure 69: South America Animal Diagnostics Industry Revenue Share (%), by Animals 2025 & 2033

- Figure 70: South America Animal Diagnostics Industry Volume Share (%), by Animals 2025 & 2033

- Figure 71: South America Animal Diagnostics Industry Revenue (Million), by Application 2025 & 2033

- Figure 72: South America Animal Diagnostics Industry Volume (K Unit), by Application 2025 & 2033

- Figure 73: South America Animal Diagnostics Industry Revenue Share (%), by Application 2025 & 2033

- Figure 74: South America Animal Diagnostics Industry Volume Share (%), by Application 2025 & 2033

- Figure 75: South America Animal Diagnostics Industry Revenue (Million), by Technology 2025 & 2033

- Figure 76: South America Animal Diagnostics Industry Volume (K Unit), by Technology 2025 & 2033

- Figure 77: South America Animal Diagnostics Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 78: South America Animal Diagnostics Industry Volume Share (%), by Technology 2025 & 2033

- Figure 79: South America Animal Diagnostics Industry Revenue (Million), by Country 2025 & 2033

- Figure 80: South America Animal Diagnostics Industry Volume (K Unit), by Country 2025 & 2033

- Figure 81: South America Animal Diagnostics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 82: South America Animal Diagnostics Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Animal Diagnostics Industry Revenue Million Forecast, by Animals 2020 & 2033

- Table 2: Global Animal Diagnostics Industry Volume K Unit Forecast, by Animals 2020 & 2033

- Table 3: Global Animal Diagnostics Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 4: Global Animal Diagnostics Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 5: Global Animal Diagnostics Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 6: Global Animal Diagnostics Industry Volume K Unit Forecast, by Technology 2020 & 2033

- Table 7: Global Animal Diagnostics Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 8: Global Animal Diagnostics Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 9: Global Animal Diagnostics Industry Revenue Million Forecast, by Animals 2020 & 2033

- Table 10: Global Animal Diagnostics Industry Volume K Unit Forecast, by Animals 2020 & 2033

- Table 11: Global Animal Diagnostics Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 12: Global Animal Diagnostics Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 13: Global Animal Diagnostics Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 14: Global Animal Diagnostics Industry Volume K Unit Forecast, by Technology 2020 & 2033

- Table 15: Global Animal Diagnostics Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Global Animal Diagnostics Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 17: United States Animal Diagnostics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: United States Animal Diagnostics Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 19: Canada Animal Diagnostics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Canada Animal Diagnostics Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 21: Mexico Animal Diagnostics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Mexico Animal Diagnostics Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 23: Global Animal Diagnostics Industry Revenue Million Forecast, by Animals 2020 & 2033

- Table 24: Global Animal Diagnostics Industry Volume K Unit Forecast, by Animals 2020 & 2033

- Table 25: Global Animal Diagnostics Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 26: Global Animal Diagnostics Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 27: Global Animal Diagnostics Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 28: Global Animal Diagnostics Industry Volume K Unit Forecast, by Technology 2020 & 2033

- Table 29: Global Animal Diagnostics Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 30: Global Animal Diagnostics Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 31: Germany Animal Diagnostics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Germany Animal Diagnostics Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 33: United Kingdom Animal Diagnostics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: United Kingdom Animal Diagnostics Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 35: France Animal Diagnostics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: France Animal Diagnostics Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 37: Italy Animal Diagnostics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Italy Animal Diagnostics Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 39: Spain Animal Diagnostics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 40: Spain Animal Diagnostics Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 41: Rest of Europe Animal Diagnostics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: Rest of Europe Animal Diagnostics Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 43: Global Animal Diagnostics Industry Revenue Million Forecast, by Animals 2020 & 2033

- Table 44: Global Animal Diagnostics Industry Volume K Unit Forecast, by Animals 2020 & 2033

- Table 45: Global Animal Diagnostics Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 46: Global Animal Diagnostics Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 47: Global Animal Diagnostics Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 48: Global Animal Diagnostics Industry Volume K Unit Forecast, by Technology 2020 & 2033

- Table 49: Global Animal Diagnostics Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 50: Global Animal Diagnostics Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 51: China Animal Diagnostics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 52: China Animal Diagnostics Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 53: Japan Animal Diagnostics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 54: Japan Animal Diagnostics Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 55: India Animal Diagnostics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 56: India Animal Diagnostics Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 57: Australia Animal Diagnostics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 58: Australia Animal Diagnostics Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 59: South Korea Animal Diagnostics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 60: South Korea Animal Diagnostics Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 61: Rest of Asia Pacific Animal Diagnostics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 62: Rest of Asia Pacific Animal Diagnostics Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 63: Global Animal Diagnostics Industry Revenue Million Forecast, by Animals 2020 & 2033

- Table 64: Global Animal Diagnostics Industry Volume K Unit Forecast, by Animals 2020 & 2033

- Table 65: Global Animal Diagnostics Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 66: Global Animal Diagnostics Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 67: Global Animal Diagnostics Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 68: Global Animal Diagnostics Industry Volume K Unit Forecast, by Technology 2020 & 2033

- Table 69: Global Animal Diagnostics Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 70: Global Animal Diagnostics Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 71: GCC Animal Diagnostics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 72: GCC Animal Diagnostics Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 73: South Africa Animal Diagnostics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 74: South Africa Animal Diagnostics Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 75: Rest of Middle East and Africa Animal Diagnostics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 76: Rest of Middle East and Africa Animal Diagnostics Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 77: Global Animal Diagnostics Industry Revenue Million Forecast, by Animals 2020 & 2033

- Table 78: Global Animal Diagnostics Industry Volume K Unit Forecast, by Animals 2020 & 2033

- Table 79: Global Animal Diagnostics Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 80: Global Animal Diagnostics Industry Volume K Unit Forecast, by Application 2020 & 2033

- Table 81: Global Animal Diagnostics Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 82: Global Animal Diagnostics Industry Volume K Unit Forecast, by Technology 2020 & 2033

- Table 83: Global Animal Diagnostics Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 84: Global Animal Diagnostics Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 85: Brazil Animal Diagnostics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 86: Brazil Animal Diagnostics Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 87: Argentina Animal Diagnostics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 88: Argentina Animal Diagnostics Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 89: Rest of South America Animal Diagnostics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 90: Rest of South America Animal Diagnostics Industry Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Animal Diagnostics Industry?

The projected CAGR is approximately 10.00%.

2. Which companies are prominent players in the Animal Diagnostics Industry?

Key companies in the market include Heska Corporation, Innovative Diagnostics (IDvet), Zoetis Inc , IDEXX Laboratories Inc, BioMerieux SA, Randox Laboratories Ltd, Chembio Diagnostic Systems Inc, Thermo Fisher Scientific Inc, Indical Bioscience GmbH, Creative Diagnostics, Agrolabo SpA, Virbac, Neogen Corporation.

3. What are the main segments of the Animal Diagnostics Industry?

The market segments include Animals, Application, Technology.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.11 Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Demand for Pet Insurance; Growth in the Companion Animal Population; Increasing Number of Veterinary Practitioners in Developed Economies.

6. What are the notable trends driving market growth?

Molecular Diagnostics is Expected to Witness Growth Over the Forecast Period.

7. Are there any restraints impacting market growth?

Rising Burden of the Pet Care Cost.

8. Can you provide examples of recent developments in the market?

August 2022: PepiPets launched a new mobile diagnostic testing service allowing clients to receive diagnostic testing at home for their pets.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Animal Diagnostics Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Animal Diagnostics Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Animal Diagnostics Industry?

To stay informed about further developments, trends, and reports in the Animal Diagnostics Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence