Key Insights

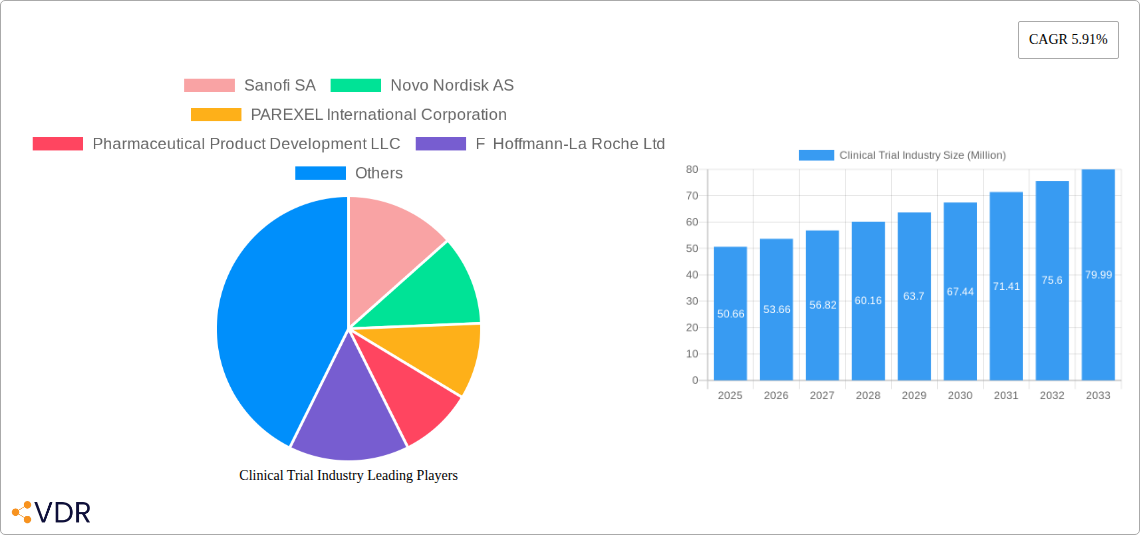

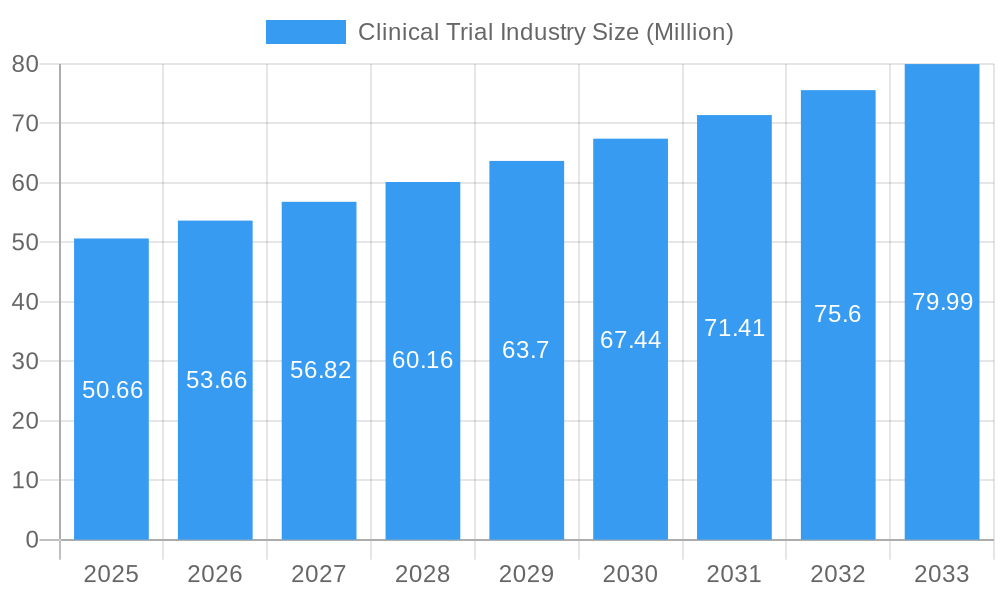

The global Clinical Trial Industry is poised for robust expansion, currently valued at an estimated USD 50.66 million. Driven by an anticipated Compound Annual Growth Rate (CAGR) of 5.91% from 2025 to 2033, the market is experiencing a significant upward trajectory. This growth is propelled by several critical factors, including the escalating demand for novel therapeutics and diagnostics, an increasing prevalence of chronic diseases globally, and the continuous innovation in drug development pipelines across major pharmaceutical and biotechnology companies. The industry's expansion is also significantly influenced by advancements in clinical trial technologies, such as decentralized clinical trials and AI-powered data analysis, which are enhancing efficiency and reducing costs. Furthermore, substantial investments in research and development by leading players like Sanofi SA, Novo Nordisk AS, and Pfizer Inc. are fueling new study initiations and the exploration of novel treatment modalities. The growing complexity of drug development and the need for rigorous testing to meet stringent regulatory requirements also contribute to the sustained demand for clinical trial services.

Clinical Trial Industry Market Size (In Million)

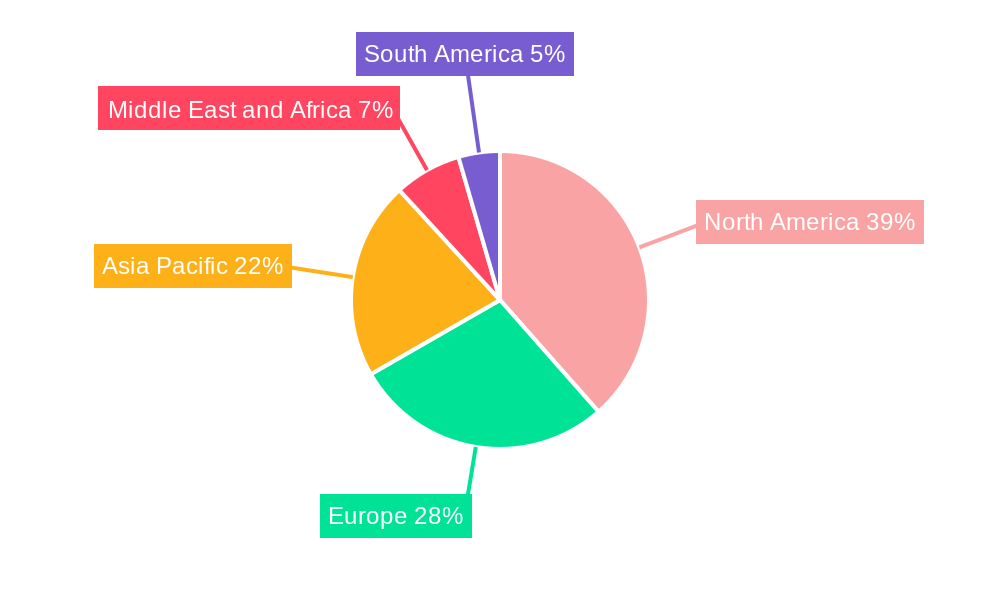

The landscape of the Clinical Trial Industry is marked by a diverse range of segments, encompassing various phases of clinical research, from Phase I to Phase IV, and a spectrum of study designs including randomized control trials, adaptive clinical trials, observational studies like cohort and case-control studies, and cross-sectional studies. Geographically, North America, particularly the United States, is expected to maintain its dominance due to a well-established healthcare infrastructure, substantial R&D investments, and a supportive regulatory environment. Europe and the Asia Pacific region, with China and India emerging as key growth hubs, are also anticipated to witness considerable market expansion, driven by growing healthcare expenditures, a rising patient pool, and an increasing number of contract research organizations (CROs). Key industry players, including PAREXEL International Corporation, IQVIA, and Laboratory Corporation of America, are actively engaged in strategic collaborations and acquisitions to broaden their service offerings and geographical reach, further solidifying the market's growth momentum.

Clinical Trial Industry Company Market Share

This comprehensive report offers an in-depth analysis of the global Clinical Trial Industry, covering market dynamics, growth trends, regional dominance, product landscape, key drivers, challenges, and emerging opportunities. With a study period spanning 2019-2033, a base year of 2025, and a forecast period from 2025-2033, this report provides actionable insights for industry professionals. The market is segmented by Phase (Phase I, II, III, IV) and Design (Treatment Studies: Randomized Control Trial, Adaptive Clinical Trial, Non-randomized Control Trial; Observational Studies: Cohort Study, Case Control Study, Cross Sectional Study, Ecological Study). All values are presented in Million units.

Clinical Trial Industry Market Dynamics & Structure

The Clinical Trial Industry is characterized by a dynamic interplay of factors shaping its structure and concentration. Technological innovation, particularly in areas like decentralized trials and AI-driven data analysis, is a primary driver, fostering a more efficient and patient-centric research environment. The regulatory landscape, evolving with global health concerns and rapid scientific advancements, presents both opportunities and hurdles, influencing trial designs and approval pathways. Competitive product substitutes, while less direct in the trial execution phase, emerge in the form of alternative research methodologies or advancements in diagnostics that might reduce the need for certain trial arms. End-user demographics are increasingly influencing trial recruitment and design, with a growing emphasis on personalized medicine and targeted therapies. Mergers and acquisitions (M&A) trends are notably active as larger Contract Research Organizations (CROs) seek to expand their service portfolios and geographic reach, consolidating market share. For instance, significant M&A activity has been observed in recent years, with several multi-million dollar deals aimed at acquiring specialized capabilities in areas like rare disease trials or real-world evidence generation. The market concentration is moderately high, with a few dominant global players like IQVIA, Laboratory Corporation of America, and PAREXEL International Corporation holding substantial market shares, estimated at over 60% combined in key segments. Innovation barriers include the high cost of drug development, the lengthy duration of clinical trials, and the stringent regulatory requirements, which can deter smaller players.

- Market Concentration: Moderately high, with key players dominating significant market shares.

- Technological Innovation Drivers: AI in data analysis, decentralized clinical trials (DCTs), wearable technology, digital health platforms.

- Regulatory Frameworks: Evolving global regulations (FDA, EMA), ICH guidelines, data privacy laws (GDPR, HIPAA).

- Competitive Product Substitutes: Advanced diagnostic tools, in-silico modeling, alternative research methodologies.

- End-User Demographics: Growing demand for personalized medicine, rare disease treatments, and oncology trials.

- M&A Trends: Consolidation for expanded service offerings, geographic reach, and specialized expertise.

Clinical Trial Industry Growth Trends & Insights

The global Clinical Trial Industry has experienced robust growth, propelled by a confluence of factors including increased R&D investments by pharmaceutical and biotechnology companies, the rising incidence of chronic diseases, and advancements in medical technology. The market size is projected to expand significantly, with an estimated Compound Annual Growth Rate (CAGR) of approximately 7.5% from 2025 to 2033. This growth is underpinned by the continuous pipeline of new drug development and the increasing complexity of therapeutic areas being explored, necessitating more sophisticated clinical trial designs and execution. Adoption rates for innovative trial methodologies, such as adaptive clinical trials and decentralized clinical trials, are on the rise. These approaches offer greater efficiency, improved patient recruitment and retention, and cost savings, making them increasingly attractive to sponsors. Technological disruptions, including the integration of Artificial Intelligence (AI) for data analysis and predictive modeling, real-time monitoring through wearable devices, and blockchain for secure data management, are revolutionizing trial operations. These advancements are not only optimizing trial processes but also enhancing data integrity and reducing the time to market for new therapies. Consumer behavior shifts are also playing a crucial role. Patients are becoming more informed and actively involved in their healthcare decisions, leading to increased participation in clinical trials and a greater demand for patient-centric trial designs that minimize burden and maximize convenience. The penetration of digital health solutions and remote monitoring tools has accelerated, further facilitating the adoption of decentralized and hybrid trial models. The market's trajectory indicates a sustained expansion, driven by the ongoing need for effective treatments across a spectrum of diseases and the industry's capacity to adapt to emerging technologies and patient expectations. The total market size for clinical trials is estimated to reach over $85,000 million by 2025, with projections indicating a substantial increase by the end of the forecast period.

Dominant Regions, Countries, or Segments in Clinical Trial Industry

North America, particularly the United States, consistently emerges as a dominant region in the Clinical Trial Industry. This dominance is attributed to a confluence of factors including a well-established regulatory framework, substantial government and private investment in research and development, the presence of leading pharmaceutical and biotechnology companies, and a robust network of academic medical centers and research institutions. The region exhibits a high market share in all trial phases, with a particular strength in Phase III and Phase IV studies, which involve larger patient populations and are crucial for drug approval.

Within the Phase segmentation, Phase III trials represent a significant portion of the market due to their critical role in demonstrating efficacy and safety of new drugs. Their market share is estimated to be over 40% of the total trial expenditure, followed by Phase II trials at around 30%. Phase IV trials, or post-marketing studies, are also a growing segment, driven by the need for long-term safety monitoring and real-world evidence generation. Phase I trials, while smaller in scale, are foundational for new drug development.

In terms of Design, Treatment Studies, especially Randomized Control Trials (RCTs), hold the largest market share. RCTs remain the gold standard for establishing causality and are extensively utilized across all phases of drug development. The market share for RCTs alone is estimated to be over 55% of the total market value. Adaptive Clinical Trials are gaining traction due to their efficiency and ability to modify trial parameters in response to accumulating data, reducing trial duration and cost. Observational Studies, while important for understanding disease progression and treatment outcomes in real-world settings, represent a smaller but growing segment of the overall clinical trial market, particularly in the context of real-world evidence generation.

- Dominant Region: North America (USA)

- Key Drivers: Robust R&D funding, advanced healthcare infrastructure, strong regulatory support, presence of major pharmaceutical players.

- Market Share: Estimated to hold over 50% of the global clinical trial market.

- Growth Potential: Sustained growth driven by innovation in biotechnology and pharmaceuticals.

- Dominant Phase: Phase III Trials

- Key Drivers: Critical for drug approval, large patient populations required for statistical significance.

- Market Share: Over 40% of the total clinical trial market.

- Dominant Design: Treatment Studies (Randomized Control Trials)

- Key Drivers: Gold standard for efficacy and safety demonstration, widely accepted by regulatory bodies.

- Market Share: Over 55% of the total clinical trial market.

- Emerging Segment: Adaptive Clinical Trials

- Key Drivers: Efficiency, cost-effectiveness, ability to modify trial protocols based on interim results.

Clinical Trial Industry Product Landscape

The Clinical Trial Industry product landscape is characterized by a sophisticated array of services and technologies designed to support drug development. This includes comprehensive clinical trial management software (CTMS), electronic data capture (EDC) systems, interactive response technology (IRT) for patient randomization and drug supply management, and advanced analytical platforms for data interpretation. Unique selling propositions often revolve around real-time data integration, enhanced security features, and AI-powered insights that streamline trial operations. Technological advancements are continually being integrated, such as wearable devices for continuous patient monitoring, digital platforms enabling decentralized clinical trials, and sophisticated tools for patient recruitment and engagement. The performance metrics focus on efficiency gains, reduced data errors, accelerated trial timelines, and improved patient outcomes, all contributing to the overall value proposition of these offerings.

Key Drivers, Barriers & Challenges in Clinical Trial Industry

The Clinical Trial Industry is propelled by several key drivers. Technological advancements, including AI, machine learning, and decentralized trial technologies, are enhancing efficiency and patient engagement. Increasing R&D investments by pharmaceutical and biotechnology companies, fueled by the demand for novel therapies for unmet medical needs, are also critical. Favorable government policies and regulatory support in many regions encourage clinical research.

- Key Drivers:

- Technological innovation (AI, DCTs, wearables)

- Rising R&D investments

- Growing prevalence of chronic diseases

- Demand for personalized medicine

However, significant barriers and challenges restrain market growth. The high cost and lengthy duration of clinical trials remain a primary constraint. Stringent and evolving regulatory requirements across different geographies add complexity and increase compliance costs. Patient recruitment and retention can be difficult, especially for rare diseases or specific patient populations. Supply chain disruptions and the need for specialized infrastructure also pose challenges.

- Key Barriers & Challenges:

- High trial costs and long durations

- Complex and evolving regulatory landscapes

- Patient recruitment and retention difficulties

- Supply chain complexities and logistical hurdles

Emerging Opportunities in Clinical Trial Industry

Emerging opportunities in the Clinical Trial Industry are abundant, driven by advancements in personalized medicine, the increasing focus on rare diseases, and the growing adoption of real-world evidence (RWE). The development of gene therapies and cell therapies presents new frontiers for clinical investigation, requiring specialized trial designs and expertise. Untapped markets in emerging economies are also offering significant growth potential as healthcare infrastructure and research capabilities improve. Furthermore, the integration of digital health tools and artificial intelligence presents opportunities for optimizing trial processes, enhancing data collection, and improving patient outcomes. The growing demand for decentralized clinical trials (DCTs) also opens avenues for innovative service providers and technology solutions.

Growth Accelerators in the Clinical Trial Industry Industry

Long-term growth in the Clinical Trial Industry is being accelerated by several key catalysts. Technological breakthroughs, such as the application of AI for predictive analytics in patient stratification and outcome prediction, are significantly enhancing trial efficiency. Strategic partnerships between pharmaceutical companies, contract research organizations (CROs), and technology providers are fostering innovation and expanding service capabilities. The growing emphasis on rare disease research, driven by unmet medical needs and increased patient advocacy, is also a significant growth accelerator. Furthermore, market expansion into emerging economies, coupled with a growing understanding and acceptance of global clinical trial standards, is opening new avenues for research and development.

Key Players Shaping the Clinical Trial Industry Market

- Sanofi SA

- Novo Nordisk AS

- PAREXEL International Corporation

- Pharmaceutical Product Development LLC

- F Hoffmann-La Roche Ltd

- Syneos Health

- ICON PLC

- Eli Lilly and Company

- ClinDatrix Inc

- Charles River Laboratory

- Clinipace

- IQVIA

- Laboratory Corporation of America

- Pfizer Inc

Notable Milestones in Clinical Trial Industry Sector

- July 2022: An early-stage clinical trial investigating an investigational vaccine to stave off Nipah virus infection was started by the National Institute of Allergy and Infectious Diseases (NIAID), a division of the National Institutes of Health (NIH) of the United States. This highlights a significant advancement in vaccine research for emerging infectious diseases.

- May 2022: The International AIDS Vaccine Initiative (IAVI) and Moderna Inc. started a Phase I clinical trial of an mRNA vaccine antigen in Rwanda and South Africa. This milestone demonstrates the global collaboration in developing novel vaccine platforms for critical public health challenges, particularly in underserved regions.

In-Depth Clinical Trial Industry Market Outlook

The future outlook for the Clinical Trial Industry is exceptionally promising, driven by continuous innovation and a sustained demand for novel therapeutics. Growth accelerators such as advancements in precision medicine, the expanding application of AI in drug discovery and trial optimization, and the increasing adoption of decentralized clinical trial models are poised to redefine the landscape. Strategic opportunities lie in further expanding into underserved geographic markets and fostering collaborative ecosystems that bridge the gap between research, technology, and patient care. The industry's ability to adapt to evolving regulatory environments and patient needs will be paramount in unlocking its full potential and ensuring the efficient delivery of life-saving treatments worldwide.

Clinical Trial Industry Segmentation

-

1. Phase

- 1.1. Phase I

- 1.2. Phase II

- 1.3. Phase III

- 1.4. Phase IV

-

2. Design

-

2.1. Treatment Studies

- 2.1.1. Randomized Control Trial

- 2.1.2. Adaptive Clinical Trial

- 2.1.3. Non-randomized Control Trial

-

2.2. Observational Studies

- 2.2.1. Cohort Study

- 2.2.2. Case Control Study

- 2.2.3. Cross Sectional Study

- 2.2.4. Ecological Study

-

2.1. Treatment Studies

Clinical Trial Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Clinical Trial Industry Regional Market Share

Geographic Coverage of Clinical Trial Industry

Clinical Trial Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.91% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Phase

- 5.1.1. Phase I

- 5.1.2. Phase II

- 5.1.3. Phase III

- 5.1.4. Phase IV

- 5.2. Market Analysis, Insights and Forecast - by Design

- 5.2.1. Treatment Studies

- 5.2.1.1. Randomized Control Trial

- 5.2.1.2. Adaptive Clinical Trial

- 5.2.1.3. Non-randomized Control Trial

- 5.2.2. Observational Studies

- 5.2.2.1. Cohort Study

- 5.2.2.2. Case Control Study

- 5.2.2.3. Cross Sectional Study

- 5.2.2.4. Ecological Study

- 5.2.1. Treatment Studies

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Middle East and Africa

- 5.3.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Phase

- 6. Global Clinical Trial Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Phase

- 6.1.1. Phase I

- 6.1.2. Phase II

- 6.1.3. Phase III

- 6.1.4. Phase IV

- 6.2. Market Analysis, Insights and Forecast - by Design

- 6.2.1. Treatment Studies

- 6.2.1.1. Randomized Control Trial

- 6.2.1.2. Adaptive Clinical Trial

- 6.2.1.3. Non-randomized Control Trial

- 6.2.2. Observational Studies

- 6.2.2.1. Cohort Study

- 6.2.2.2. Case Control Study

- 6.2.2.3. Cross Sectional Study

- 6.2.2.4. Ecological Study

- 6.2.1. Treatment Studies

- 6.1. Market Analysis, Insights and Forecast - by Phase

- 7. North America Clinical Trial Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Phase

- 7.1.1. Phase I

- 7.1.2. Phase II

- 7.1.3. Phase III

- 7.1.4. Phase IV

- 7.2. Market Analysis, Insights and Forecast - by Design

- 7.2.1. Treatment Studies

- 7.2.1.1. Randomized Control Trial

- 7.2.1.2. Adaptive Clinical Trial

- 7.2.1.3. Non-randomized Control Trial

- 7.2.2. Observational Studies

- 7.2.2.1. Cohort Study

- 7.2.2.2. Case Control Study

- 7.2.2.3. Cross Sectional Study

- 7.2.2.4. Ecological Study

- 7.2.1. Treatment Studies

- 7.1. Market Analysis, Insights and Forecast - by Phase

- 8. Europe Clinical Trial Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Phase

- 8.1.1. Phase I

- 8.1.2. Phase II

- 8.1.3. Phase III

- 8.1.4. Phase IV

- 8.2. Market Analysis, Insights and Forecast - by Design

- 8.2.1. Treatment Studies

- 8.2.1.1. Randomized Control Trial

- 8.2.1.2. Adaptive Clinical Trial

- 8.2.1.3. Non-randomized Control Trial

- 8.2.2. Observational Studies

- 8.2.2.1. Cohort Study

- 8.2.2.2. Case Control Study

- 8.2.2.3. Cross Sectional Study

- 8.2.2.4. Ecological Study

- 8.2.1. Treatment Studies

- 8.1. Market Analysis, Insights and Forecast - by Phase

- 9. Asia Pacific Clinical Trial Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Phase

- 9.1.1. Phase I

- 9.1.2. Phase II

- 9.1.3. Phase III

- 9.1.4. Phase IV

- 9.2. Market Analysis, Insights and Forecast - by Design

- 9.2.1. Treatment Studies

- 9.2.1.1. Randomized Control Trial

- 9.2.1.2. Adaptive Clinical Trial

- 9.2.1.3. Non-randomized Control Trial

- 9.2.2. Observational Studies

- 9.2.2.1. Cohort Study

- 9.2.2.2. Case Control Study

- 9.2.2.3. Cross Sectional Study

- 9.2.2.4. Ecological Study

- 9.2.1. Treatment Studies

- 9.1. Market Analysis, Insights and Forecast - by Phase

- 10. Middle East and Africa Clinical Trial Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Phase

- 10.1.1. Phase I

- 10.1.2. Phase II

- 10.1.3. Phase III

- 10.1.4. Phase IV

- 10.2. Market Analysis, Insights and Forecast - by Design

- 10.2.1. Treatment Studies

- 10.2.1.1. Randomized Control Trial

- 10.2.1.2. Adaptive Clinical Trial

- 10.2.1.3. Non-randomized Control Trial

- 10.2.2. Observational Studies

- 10.2.2.1. Cohort Study

- 10.2.2.2. Case Control Study

- 10.2.2.3. Cross Sectional Study

- 10.2.2.4. Ecological Study

- 10.2.1. Treatment Studies

- 10.1. Market Analysis, Insights and Forecast - by Phase

- 11. South America Clinical Trial Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Phase

- 11.1.1. Phase I

- 11.1.2. Phase II

- 11.1.3. Phase III

- 11.1.4. Phase IV

- 11.2. Market Analysis, Insights and Forecast - by Design

- 11.2.1. Treatment Studies

- 11.2.1.1. Randomized Control Trial

- 11.2.1.2. Adaptive Clinical Trial

- 11.2.1.3. Non-randomized Control Trial

- 11.2.2. Observational Studies

- 11.2.2.1. Cohort Study

- 11.2.2.2. Case Control Study

- 11.2.2.3. Cross Sectional Study

- 11.2.2.4. Ecological Study

- 11.2.1. Treatment Studies

- 11.1. Market Analysis, Insights and Forecast - by Phase

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Sanofi SA

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Novo Nordisk AS

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 PAREXEL International Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Pharmaceutical Product Development LLC

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 F Hoffmann-La Roche Ltd

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Syneos Health

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 ICON PLC

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Eli Lilly and Company

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 ClinDatrix Inc

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Charles River Laboratory

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Clinipace

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 IQVIA

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Laboratory Corporation of America

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Pfizer Inc

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.1 Sanofi SA

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Clinical Trial Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Clinical Trial Industry Revenue (Million), by Phase 2025 & 2033

- Figure 3: North America Clinical Trial Industry Revenue Share (%), by Phase 2025 & 2033

- Figure 4: North America Clinical Trial Industry Revenue (Million), by Design 2025 & 2033

- Figure 5: North America Clinical Trial Industry Revenue Share (%), by Design 2025 & 2033

- Figure 6: North America Clinical Trial Industry Revenue (Million), by Country 2025 & 2033

- Figure 7: North America Clinical Trial Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Clinical Trial Industry Revenue (Million), by Phase 2025 & 2033

- Figure 9: Europe Clinical Trial Industry Revenue Share (%), by Phase 2025 & 2033

- Figure 10: Europe Clinical Trial Industry Revenue (Million), by Design 2025 & 2033

- Figure 11: Europe Clinical Trial Industry Revenue Share (%), by Design 2025 & 2033

- Figure 12: Europe Clinical Trial Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe Clinical Trial Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Clinical Trial Industry Revenue (Million), by Phase 2025 & 2033

- Figure 15: Asia Pacific Clinical Trial Industry Revenue Share (%), by Phase 2025 & 2033

- Figure 16: Asia Pacific Clinical Trial Industry Revenue (Million), by Design 2025 & 2033

- Figure 17: Asia Pacific Clinical Trial Industry Revenue Share (%), by Design 2025 & 2033

- Figure 18: Asia Pacific Clinical Trial Industry Revenue (Million), by Country 2025 & 2033

- Figure 19: Asia Pacific Clinical Trial Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East and Africa Clinical Trial Industry Revenue (Million), by Phase 2025 & 2033

- Figure 21: Middle East and Africa Clinical Trial Industry Revenue Share (%), by Phase 2025 & 2033

- Figure 22: Middle East and Africa Clinical Trial Industry Revenue (Million), by Design 2025 & 2033

- Figure 23: Middle East and Africa Clinical Trial Industry Revenue Share (%), by Design 2025 & 2033

- Figure 24: Middle East and Africa Clinical Trial Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Middle East and Africa Clinical Trial Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Clinical Trial Industry Revenue (Million), by Phase 2025 & 2033

- Figure 27: South America Clinical Trial Industry Revenue Share (%), by Phase 2025 & 2033

- Figure 28: South America Clinical Trial Industry Revenue (Million), by Design 2025 & 2033

- Figure 29: South America Clinical Trial Industry Revenue Share (%), by Design 2025 & 2033

- Figure 30: South America Clinical Trial Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: South America Clinical Trial Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Clinical Trial Industry Revenue Million Forecast, by Phase 2020 & 2033

- Table 2: Global Clinical Trial Industry Revenue Million Forecast, by Design 2020 & 2033

- Table 3: Global Clinical Trial Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Clinical Trial Industry Revenue Million Forecast, by Phase 2020 & 2033

- Table 5: Global Clinical Trial Industry Revenue Million Forecast, by Design 2020 & 2033

- Table 6: Global Clinical Trial Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United States Clinical Trial Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Canada Clinical Trial Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Clinical Trial Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Global Clinical Trial Industry Revenue Million Forecast, by Phase 2020 & 2033

- Table 11: Global Clinical Trial Industry Revenue Million Forecast, by Design 2020 & 2033

- Table 12: Global Clinical Trial Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Germany Clinical Trial Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: United Kingdom Clinical Trial Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: France Clinical Trial Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Italy Clinical Trial Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Spain Clinical Trial Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Rest of Europe Clinical Trial Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Global Clinical Trial Industry Revenue Million Forecast, by Phase 2020 & 2033

- Table 20: Global Clinical Trial Industry Revenue Million Forecast, by Design 2020 & 2033

- Table 21: Global Clinical Trial Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 22: China Clinical Trial Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: Japan Clinical Trial Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: India Clinical Trial Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: Australia Clinical Trial Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: South Korea Clinical Trial Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Asia Pacific Clinical Trial Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Global Clinical Trial Industry Revenue Million Forecast, by Phase 2020 & 2033

- Table 29: Global Clinical Trial Industry Revenue Million Forecast, by Design 2020 & 2033

- Table 30: Global Clinical Trial Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 31: GCC Clinical Trial Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: South Africa Clinical Trial Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 33: Rest of Middle East and Africa Clinical Trial Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Global Clinical Trial Industry Revenue Million Forecast, by Phase 2020 & 2033

- Table 35: Global Clinical Trial Industry Revenue Million Forecast, by Design 2020 & 2033

- Table 36: Global Clinical Trial Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 37: Brazil Clinical Trial Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Argentina Clinical Trial Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 39: Rest of South America Clinical Trial Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Clinical Trial Industry?

The projected CAGR is approximately 5.91%.

2. Which companies are prominent players in the Clinical Trial Industry?

Key companies in the market include Sanofi SA, Novo Nordisk AS, PAREXEL International Corporation, Pharmaceutical Product Development LLC, F Hoffmann-La Roche Ltd, Syneos Health, ICON PLC, Eli Lilly and Company, ClinDatrix Inc, Charles River Laboratory, Clinipace, IQVIA, Laboratory Corporation of America, Pfizer Inc.

3. What are the main segments of the Clinical Trial Industry?

The market segments include Phase, Design.

4. Can you provide details about the market size?

The market size is estimated to be USD 50.66 Million as of 2022.

5. What are some drivers contributing to market growth?

Demand for Clinical Trials in the Emerging Markets; High R&D Expenditure of the Pharmaceutical Industry; Rising Prevalence of Diseases.

6. What are the notable trends driving market growth?

Phase III by Phase Segment is Expected to Grow Over the Forecast Period.

7. Are there any restraints impacting market growth?

Lack of Skilled Workforce in Clinical Research; Stringent Regulations for Patient Enrollment.

8. Can you provide examples of recent developments in the market?

July 2022: An early-stage clinical trial investigating an investigational vaccine to stave off Nipah virus infection was started by the National Institute of Allergy and Infectious Diseases (NIAID), a division of the National Institutes of Health (NIH) of the United States.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Clinical Trial Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Clinical Trial Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Clinical Trial Industry?

To stay informed about further developments, trends, and reports in the Clinical Trial Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence