Key Insights

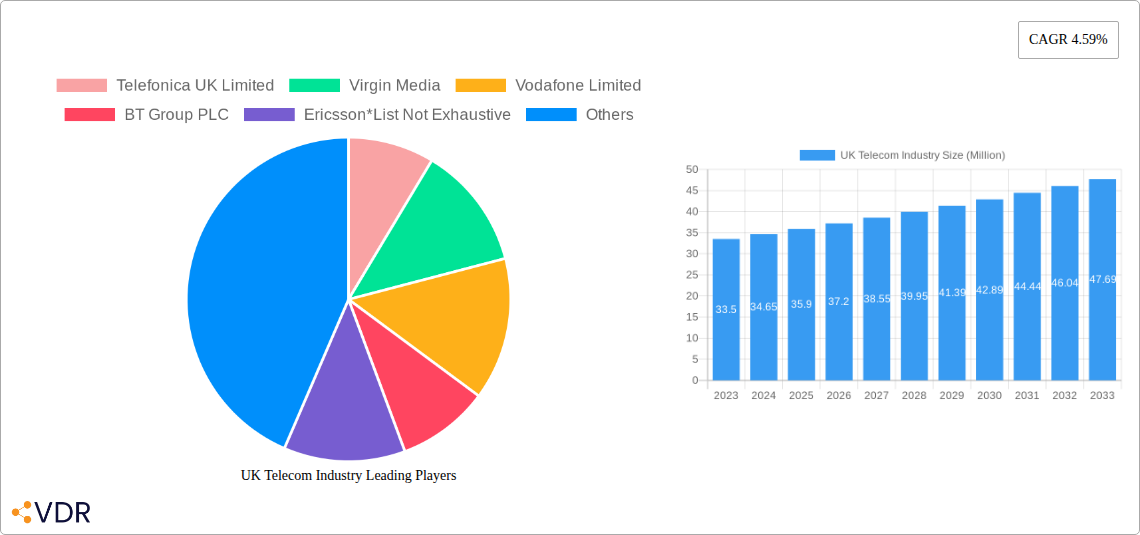

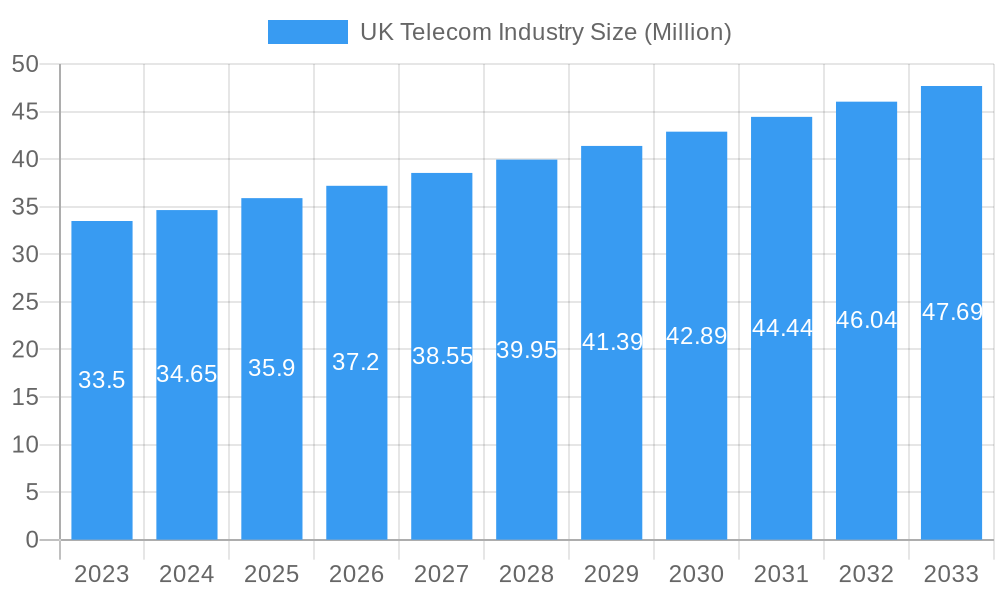

The UK telecom industry is poised for substantial growth, projected to reach approximately $35.90 billion by 2025, with a Compound Annual Growth Rate (CAGR) of 4.59% expected to propel it through 2033. This robust expansion is fueled by a confluence of factors, including the relentless demand for high-speed data services, the increasing adoption of Over-The-Top (OTT) entertainment platforms, and the ongoing evolution of voice services from traditional wired to advanced wireless technologies. The digital transformation across all sectors of the UK economy necessitates a more connected and agile telecommunications infrastructure. Investment in 5G deployment, fiber optic network expansion, and the integration of artificial intelligence for enhanced customer service and network management are key strategic imperatives for leading players. Companies like BT Group PLC, Vodafone Limited, and Virgin Media are at the forefront, vying for market share through innovative service offerings and strategic partnerships.

UK Telecom Industry Market Size (In Million)

Despite this optimistic outlook, the industry faces certain headwinds. Intense competition among established players and emerging MVNOs (Mobile Virtual Network Operators) places pressure on pricing and margins. Regulatory scrutiny concerning data privacy, net neutrality, and infrastructure deployment also presents a complex operating environment. Furthermore, the significant capital expenditure required for network upgrades, particularly for 5G and future generations, demands careful financial planning and strategic investment. However, the growing appetite for immersive digital experiences, the continued rise of remote work, and the increasing penetration of connected devices are expected to outweigh these challenges, ensuring a dynamic and evolving UK telecom market for years to come. The strategic focus on delivering seamless, high-quality voice, data, and integrated entertainment services will be critical for sustained success.

UK Telecom Industry Company Market Share

UK Telecom Industry Market Dynamics & Structure

The UK telecom industry is characterized by a dynamic interplay of market concentration, rapid technological innovation, and evolving regulatory frameworks. Major players like BT Group PLC, Vodafone Limited, and Virgin Media exert significant influence, though competition from newer entrants and challenger brands such as TalkTalk Telecom Group and Lycamobile maintains a degree of dynamism. Technological advancements, particularly in 5G deployment and fibre broadband infrastructure, are pivotal drivers, necessitating substantial capital investment. Regulatory bodies continuously shape the landscape, balancing consumer protection with fostering competition and innovation. Substitute services, notably Over-The-Top (OTT) platforms and the increasing reliance on mobile data, are reshaping traditional voice and data service consumption. End-user demographics are increasingly sophisticated, demanding higher speeds, greater reliability, and seamless connectivity across multiple devices. Mergers and acquisitions remain a strategic tool for consolidation and market expansion, as evidenced by ongoing discussions within the industry.

- Market Concentration: Dominated by a few key players, yet with space for niche and challenger brands.

- Technological Innovation: Driven by 5G, fibre broadband, and AI integration.

- Regulatory Framework: A critical factor influencing investment, competition, and consumer pricing.

- Competitive Substitutes: OTT services and mobile data are increasingly impacting traditional revenue streams.

- End-User Demographics: High demand for speed, reliability, and integrated digital experiences.

- M&A Trends: Strategic consolidation and partnerships are prevalent.

UK Telecom Industry Growth Trends & Insights

The UK telecom industry is poised for robust growth, fueled by escalating demand for high-speed connectivity and the pervasive integration of digital technologies across all facets of life. The market size is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 5.8% over the forecast period of 2025-2033, driven by significant investments in fixed and mobile infrastructure. Adoption rates for fibre broadband continue to surge as consumers and businesses prioritize superior bandwidth and reduced latency, enabling seamless streaming, cloud computing, and remote work capabilities.

Technological disruptions are a constant feature, with the ongoing rollout of 5G networks opening up new avenues for innovation in areas such as the Internet of Things (IoT), enhanced mobile broadband, and ultra-reliable low-latency communication. This technological evolution is directly influencing consumer behavior, leading to a heightened expectation for always-on, high-performance connectivity. The shift towards data-centric services, including streaming entertainment and cloud-based applications, is accelerating, further boosting market penetration.

Furthermore, the increasing digitalization of industries, from healthcare and education to manufacturing and retail, creates a substantial demand for resilient and advanced telecommunications infrastructure. The adoption of AI and machine learning by telecom operators for network optimization, customer service, and personalized offerings is a growing trend, enhancing operational efficiency and customer satisfaction. The market is expected to reach an estimated size of £65,000 Million by 2025, with further expansion anticipated as new services and applications emerge.

- Market Size Evolution: Projected to grow significantly, with an estimated market size of £65,000 Million in 2025.

- Adoption Rates: High and increasing adoption of fibre broadband and 5G services.

- Technological Disruptions: 5G, AI, and IoT are reshaping the service landscape.

- Consumer Behavior Shifts: Growing reliance on data-intensive applications and on-demand services.

- CAGR: Anticipated to be around 5.8% from 2025 to 2033.

Dominant Regions, Countries, or Segments in UK Telecom Industry

Within the UK telecom industry, the Data and OTT Services segment stands out as a dominant growth driver, significantly outperforming traditional Voice Services. This dominance is fueled by an insatiable consumer and business appetite for high-speed internet access, enabling a vast array of data-intensive applications and services. The increasing penetration of smartphones and connected devices further amplifies the demand for robust data networks.

The geographical landscape of the UK, with its dense urban centres and improving rural connectivity, facilitates widespread adoption of these services. Major metropolitan areas, including London, Manchester, and Birmingham, represent concentrated hubs of high data consumption, driven by a confluence of residential users, small to medium-sized enterprises (SMEs), and large corporations. Economic policies that support digital infrastructure development, such as government initiatives to expand fibre broadband and 5G coverage, are crucial in bolstering this segment's growth.

The rise of Over-The-Top (OTT) services, encompassing video streaming platforms, cloud gaming, and digital communication tools, has fundamentally altered how consumers engage with entertainment and information. Telecom operators are increasingly positioning themselves as enablers of these services, offering bundled packages and high-speed internet plans that cater to this demand. Market share within the Data and OTT segment is substantial, with leading providers capturing significant portions of the subscriber base. The growth potential remains exceptionally high as new applications and technologies, such as augmented reality (AR) and virtual reality (VR), become more mainstream, requiring even greater data capacities.

- Dominant Segment: Data and OTT Services.

- Key Drivers:

- High demand for high-speed internet.

- Proliferation of smartphones and connected devices.

- Growth of OTT platforms (streaming, gaming, communication).

- Government support for digital infrastructure.

- Geographical Influence: Urban centres lead in consumption; rural connectivity is improving.

- Market Share: Significant portion captured by leading providers in this segment.

- Growth Potential: Extremely high due to emerging technologies and evolving consumer habits.

UK Telecom Industry Product Landscape

The UK telecom industry's product landscape is defined by a relentless pursuit of enhanced connectivity and innovative service delivery. Advancements in Wi-Fi technology, exemplified by Vodafone's Pro II plan featuring Wi-Fi 6E with its Ultra Hub and Super Wi-Fi booster, are revolutionizing home internet by supporting an unprecedented number of devices and delivering faster speeds. Simultaneously, the integration of artificial intelligence (AI) and machine learning (ML) is transforming network management and service offerings. BT Group PLC's AI Accelerator platform showcases this shift, orchestrating and optimizing AI model deployments to extract maximum value from vast data estates. This focus on cutting-edge technology ensures users experience seamless connectivity, improved network performance, and intelligent service provisioning, setting new benchmarks for the industry.

Key Drivers, Barriers & Challenges in UK Telecom Industry

Key Drivers:

- Technological Advancements: The relentless evolution of 5G, fibre optics, and AI is creating new service possibilities and enhancing existing ones.

- Increasing Data Demand: Growing reliance on streaming, cloud services, and IoT devices fuels the need for higher bandwidth and lower latency.

- Digital Transformation: The push for digitalization across all sectors necessitates robust and reliable telecommunications infrastructure.

- Government Initiatives: Policies supporting infrastructure investment and digital inclusion accelerate market development.

- Strategic Partnerships & M&A: Collaborations and consolidations drive innovation and market reach.

Barriers & Challenges:

- Infrastructure Investment Costs: The deployment of next-generation networks requires substantial capital expenditure.

- Regulatory Hurdles: Evolving regulations concerning data privacy, competition, and spectrum allocation can create complexity.

- Cybersecurity Threats: The increasing interconnectedness of networks makes them vulnerable to sophisticated cyber-attacks, requiring continuous investment in security.

- Skilled Workforce Shortage: A gap exists in the availability of specialized skills required for advanced network deployment and management.

- Competitive Pressures: Intense competition can lead to price wars and pressure on profit margins, impacting investment capacity.

- Supply Chain Disruptions: Global supply chain issues can impact the availability of essential network equipment, leading to project delays. The potential impact of supply chain disruptions on project timelines and costs can range from 5-15% increase in capital expenditure and delays of 3-9 months.

Emerging Opportunities in UK Telecom Industry

Emerging opportunities in the UK telecom industry are abundant, driven by evolving consumer preferences and technological breakthroughs. The expansion of the Internet of Things (IoT) ecosystem presents a significant avenue for growth, with opportunities in smart homes, connected vehicles, and industrial IoT applications requiring robust and reliable connectivity solutions. Furthermore, the demand for enhanced mobile broadband (eMBB) services is expected to grow as more users adopt 5G-enabled devices and consume data-intensive content. The burgeoning field of edge computing, which brings processing power closer to the data source, offers telcos a chance to provide new services for low-latency applications in areas like gaming, augmented reality, and real-time analytics. The increasing focus on sustainability and green technologies also opens doors for telcos to offer energy-efficient network solutions and services that support environmental monitoring and management.

Growth Accelerators in the UK Telecom Industry Industry

Several key factors are poised to accelerate long-term growth in the UK telecom industry. The ongoing nationwide rollout and adoption of 5G technology will unlock a new era of high-speed, low-latency connectivity, enabling a wave of innovative applications and services that were previously unfeasible. Strategic partnerships between telecom operators, technology providers, and content creators will foster ecosystem development, driving demand for advanced network capabilities. Market expansion into underserved rural areas through government-backed initiatives and private investment will broaden the subscriber base and unlock new revenue streams. The continuous integration of Artificial Intelligence (AI) and Machine Learning (ML) into network operations and customer service will improve efficiency, reduce costs, and personalize user experiences, further enhancing customer loyalty and driving adoption.

Key Players Shaping the UK Telecom Industry Market

- Telefonica UK Limited

- Virgin Media

- Vodafone Limited

- BT Group PLC

- Ericsson

- TalkTalk Telecom Group

- Lycamobile

- Sky UK Limited

- Sitel Group

- Teleperformance

Notable Milestones in UK Telecom Industry Sector

- October 2022: Vodafone unveiled its Pro II plan, featuring the speediest Wi-Fi technology across all homes in the United Kingdom. The new Ultra Hub and Super Wi-Fi booster employ Wi-Fi 6E technology, capable of supporting over 150 devices, a first for a major UK broadband provider.

- October 2022: BT Group PLC's digital division launched AI Accelerator, an internal machine learning operations (ML-Ops) platform designed to orchestrate, accelerate, and track AI model deployments, enhancing their effectiveness and value extraction from the company's extensive data estate.

- October 2022: Vodafone confirmed discussions with rival Three regarding a potential merger of their UK businesses. The proposed acquisition would see Vodafone control 51% and CK Hutchison (Three) own 49% of the new entity, creating a formidable competitor with access to a high-quality, secure 5G network.

In-Depth UK Telecom Industry Market Outlook

The UK telecom industry is set for a period of sustained and dynamic growth, driven by technological innovation and evolving consumer needs. The accelerated rollout of 5G and fibre broadband will form the bedrock for an array of new services, from advanced IoT solutions to immersive digital experiences. Strategic investments in network upgrades and expansion, particularly into rural areas, will broaden market reach and inclusivity. The industry's ability to leverage AI and ML for operational efficiencies and personalized customer engagement will be a critical factor in maintaining competitiveness and customer satisfaction. This forward-looking approach, coupled with strategic partnerships and a focus on emerging technologies, positions the UK telecom sector for significant future potential and lucrative opportunities.

UK Telecom Industry Segmentation

-

1. Servi

-

1.1. Voice Services

- 1.1.1. Wired

- 1.1.2. Wireless

- 1.2. Data and

- 1.3. OTT and PayTV Services

-

1.1. Voice Services

UK Telecom Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

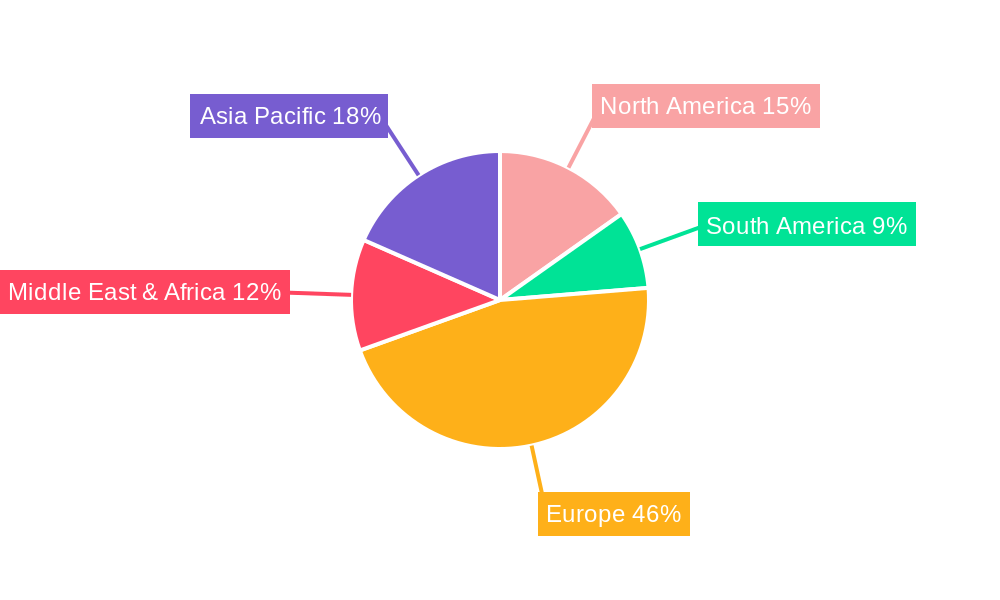

UK Telecom Industry Regional Market Share

Geographic Coverage of UK Telecom Industry

UK Telecom Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.59% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Servi

- 5.1.1. Voice Services

- 5.1.1.1. Wired

- 5.1.1.2. Wireless

- 5.1.2. Data and

- 5.1.3. OTT and PayTV Services

- 5.1.1. Voice Services

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. South America

- 5.2.3. Europe

- 5.2.4. Middle East & Africa

- 5.2.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Servi

- 6. Global UK Telecom Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Servi

- 6.1.1. Voice Services

- 6.1.1.1. Wired

- 6.1.1.2. Wireless

- 6.1.2. Data and

- 6.1.3. OTT and PayTV Services

- 6.1.1. Voice Services

- 6.1. Market Analysis, Insights and Forecast - by Servi

- 7. North America UK Telecom Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Servi

- 7.1.1. Voice Services

- 7.1.1.1. Wired

- 7.1.1.2. Wireless

- 7.1.2. Data and

- 7.1.3. OTT and PayTV Services

- 7.1.1. Voice Services

- 7.1. Market Analysis, Insights and Forecast - by Servi

- 8. South America UK Telecom Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Servi

- 8.1.1. Voice Services

- 8.1.1.1. Wired

- 8.1.1.2. Wireless

- 8.1.2. Data and

- 8.1.3. OTT and PayTV Services

- 8.1.1. Voice Services

- 8.1. Market Analysis, Insights and Forecast - by Servi

- 9. Europe UK Telecom Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Servi

- 9.1.1. Voice Services

- 9.1.1.1. Wired

- 9.1.1.2. Wireless

- 9.1.2. Data and

- 9.1.3. OTT and PayTV Services

- 9.1.1. Voice Services

- 9.1. Market Analysis, Insights and Forecast - by Servi

- 10. Middle East & Africa UK Telecom Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Servi

- 10.1.1. Voice Services

- 10.1.1.1. Wired

- 10.1.1.2. Wireless

- 10.1.2. Data and

- 10.1.3. OTT and PayTV Services

- 10.1.1. Voice Services

- 10.1. Market Analysis, Insights and Forecast - by Servi

- 11. Asia Pacific UK Telecom Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Servi

- 11.1.1. Voice Services

- 11.1.1.1. Wired

- 11.1.1.2. Wireless

- 11.1.2. Data and

- 11.1.3. OTT and PayTV Services

- 11.1.1. Voice Services

- 11.1. Market Analysis, Insights and Forecast - by Servi

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Telefonica UK Limited

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Virgin Media

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Vodafone Limited

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 BT Group PLC

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Ericsson*List Not Exhaustive

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 TalkTalk Telecom Group

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Lycamobile

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Sky UK Limited

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Sitel Group

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Teleperformance

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Telefonica UK Limited

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global UK Telecom Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America UK Telecom Industry Revenue (Million), by Servi 2025 & 2033

- Figure 3: North America UK Telecom Industry Revenue Share (%), by Servi 2025 & 2033

- Figure 4: North America UK Telecom Industry Revenue (Million), by Country 2025 & 2033

- Figure 5: North America UK Telecom Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: South America UK Telecom Industry Revenue (Million), by Servi 2025 & 2033

- Figure 7: South America UK Telecom Industry Revenue Share (%), by Servi 2025 & 2033

- Figure 8: South America UK Telecom Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: South America UK Telecom Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe UK Telecom Industry Revenue (Million), by Servi 2025 & 2033

- Figure 11: Europe UK Telecom Industry Revenue Share (%), by Servi 2025 & 2033

- Figure 12: Europe UK Telecom Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe UK Telecom Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Middle East & Africa UK Telecom Industry Revenue (Million), by Servi 2025 & 2033

- Figure 15: Middle East & Africa UK Telecom Industry Revenue Share (%), by Servi 2025 & 2033

- Figure 16: Middle East & Africa UK Telecom Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Middle East & Africa UK Telecom Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific UK Telecom Industry Revenue (Million), by Servi 2025 & 2033

- Figure 19: Asia Pacific UK Telecom Industry Revenue Share (%), by Servi 2025 & 2033

- Figure 20: Asia Pacific UK Telecom Industry Revenue (Million), by Country 2025 & 2033

- Figure 21: Asia Pacific UK Telecom Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global UK Telecom Industry Revenue Million Forecast, by Servi 2020 & 2033

- Table 2: Global UK Telecom Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 3: Global UK Telecom Industry Revenue Million Forecast, by Servi 2020 & 2033

- Table 4: Global UK Telecom Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 5: United States UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 6: Canada UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 7: Mexico UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Global UK Telecom Industry Revenue Million Forecast, by Servi 2020 & 2033

- Table 9: Global UK Telecom Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 10: Brazil UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Argentina UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Rest of South America UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Global UK Telecom Industry Revenue Million Forecast, by Servi 2020 & 2033

- Table 14: Global UK Telecom Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 15: United Kingdom UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Germany UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: France UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Italy UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Spain UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Russia UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Benelux UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Nordics UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: Rest of Europe UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Global UK Telecom Industry Revenue Million Forecast, by Servi 2020 & 2033

- Table 25: Global UK Telecom Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 26: Turkey UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Israel UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: GCC UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: North Africa UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: South Africa UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 31: Rest of Middle East & Africa UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Global UK Telecom Industry Revenue Million Forecast, by Servi 2020 & 2033

- Table 33: Global UK Telecom Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 34: China UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 35: India UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Japan UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 37: South Korea UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: ASEAN UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 39: Oceania UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 40: Rest of Asia Pacific UK Telecom Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the UK Telecom Industry?

The projected CAGR is approximately 4.59%.

2. Which companies are prominent players in the UK Telecom Industry?

Key companies in the market include Telefonica UK Limited, Virgin Media, Vodafone Limited, BT Group PLC, Ericsson*List Not Exhaustive, TalkTalk Telecom Group, Lycamobile, Sky UK Limited, Sitel Group, Teleperformance.

3. What are the main segments of the UK Telecom Industry?

The market segments include Servi.

4. Can you provide details about the market size?

The market size is estimated to be USD 35.90 Million as of 2022.

5. What are some drivers contributing to market growth?

Rising demand for 5G; Growth of IoT usage in Telecom.

6. What are the notable trends driving market growth?

5G Roll-Out in the United Kingdom to Drive the Market.

7. Are there any restraints impacting market growth?

; Deployment Issues & Competition From Rival LPWAN Technologies.

8. Can you provide examples of recent developments in the market?

October 2022 - Vodafone unveiled its Pro II plan, the speediest Wi-Fi technology across all homes in the United Kingdom. The new Ultra Hub and Super Wi-Fi booster employ the most recent Wi-Fi 6E technology, which may offer Wi-Fi to more than 150 devices. This is a first for any significant broadband provider in the United Kingdom.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "UK Telecom Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the UK Telecom Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the UK Telecom Industry?

To stay informed about further developments, trends, and reports in the UK Telecom Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence