Key Insights

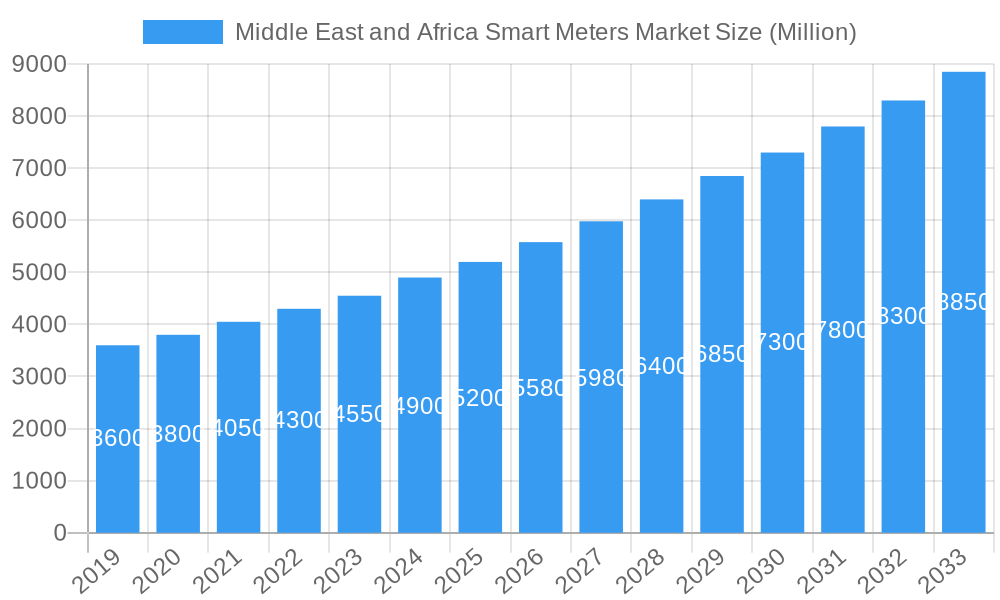

The Middle East and Africa (MEA) smart meters market is projected for significant expansion, forecasted to reach $35.63 billion by 2025, driven by a robust Compound Annual Growth Rate (CAGR) of 9.27%. This growth is attributed to key factors including government-led energy efficiency and grid modernization programs aimed at addressing escalating energy consumption and promoting sustainability. The critical need to minimize revenue losses from water and electricity, alongside the demand for precise billing and enhanced operational efficiency, are substantial catalysts for smart meter adoption. The ongoing development of smart grids and the increasing demand for Advanced Metering Infrastructure (AMI) across residential, commercial, and industrial sectors are further accelerating market penetration.

Middle East and Africa Smart Meters Market Market Size (In Billion)

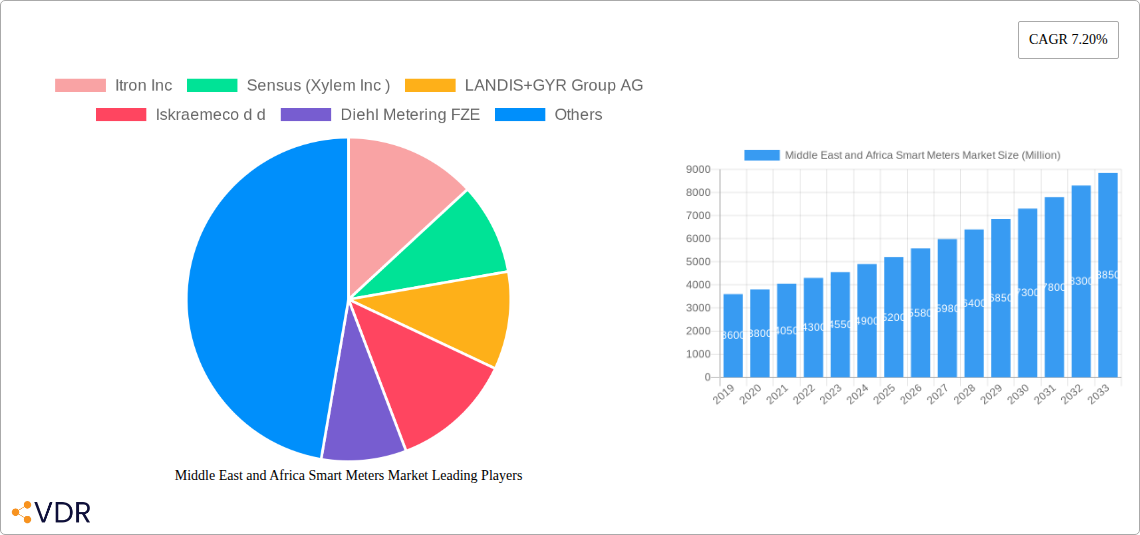

Dynamic trends are actively shaping the MEA smart meters market. A prominent trend is the accelerated integration of IoT-enabled smart meters, providing advanced data analytics and remote management. Significant investments in smart grid infrastructure, particularly in Saudi Arabia and the United Arab Emirates, are fostering substantial demand. Furthermore, a clear shift towards digitalizing utility services is empowering consumers with real-time energy usage insights, promoting smarter consumption patterns. Despite the market's upward trajectory, potential restraints such as high initial deployment costs, integration challenges with legacy systems, and the necessity for stringent cybersecurity measures may influence growth pace. However, the enduring advantages of improved grid reliability, reduced operational expenses, and enhanced sustainability are anticipated to overcome these obstacles, ensuring sustained market development. The competitive environment features established global entities including Itron Inc., Sensus (Xylem Inc.), and LANDIS+GYR Group AG, alongside emerging regional manufacturers, all competing for market leadership.

Middle East and Africa Smart Meters Market Company Market Share

Middle East and Africa Smart Meters Market: Comprehensive Analysis and Future Outlook (2019-2033)

This in-depth report provides a detailed analysis of the Middle East and Africa (MEA) Smart Meters Market, offering a comprehensive understanding of its dynamics, growth trajectories, and future potential. Covering the study period from 2019 to 2033, with a base year of 2025, the report delves into market segmentation, key drivers, emerging opportunities, and the competitive landscape. The MEA smart meter market is witnessing rapid expansion driven by government initiatives, increasing demand for efficient resource management, and technological advancements in smart grid technologies. This report is essential for stakeholders looking to capitalize on the burgeoning opportunities within this dynamic market, including utility providers, technology manufacturers, system integrators, and investors. We present all values in Million units.

Middle East and Africa Smart Meters Market Market Dynamics & Structure

The Middle East and Africa Smart Meters Market is characterized by a moderately consolidated structure, with key players like Itron Inc., Sensus (Xylem Inc.), and LANDIS+GYR Group AG holding significant market shares. Technological innovation is a primary driver, fueled by the imperative for improved energy efficiency, reduced non-revenue water, and enhanced grid reliability. Regulatory frameworks are evolving across the region, with governments increasingly mandating smart meter deployments to achieve national energy goals and support smart city initiatives. While competitive product substitutes exist in traditional metering, the superior data analytics and remote capabilities of smart meters present a compelling value proposition. End-user demographics are shifting towards greater adoption across residential, commercial, and industrial sectors, driven by cost savings and environmental consciousness. Mergers and acquisitions (M&A) are anticipated to play a role in market consolidation, as larger players seek to expand their geographical reach and technological portfolios. Barriers to innovation include the high initial investment costs for utilities and the need for robust cybersecurity infrastructure.

- Market Concentration: Moderate, with established global players and emerging regional contenders.

- Technological Innovation Drivers: Energy efficiency mandates, smart grid development, demand-side management, reduction of AT&C losses.

- Regulatory Frameworks: Supportive government policies, smart city projects, national smart grid strategies are key enablers.

- Competitive Product Substitutes: Traditional meters, though increasingly being phased out due to limitations in data and functionality.

- End-User Demographics: Growing demand from residential, commercial, and industrial sectors seeking advanced monitoring and control.

- M&A Trends: Potential for consolidation to gain market share and leverage technological synergies.

- Innovation Barriers: High upfront costs, data security concerns, and integration challenges with legacy systems.

Middle East and Africa Smart Meters Market Growth Trends & Insights

The MEA Smart Meters Market is poised for substantial growth, with market size projected to expand significantly driven by accelerating adoption rates and technological disruptions. The forecast period (2025–2033) will witness a robust CAGR as utilities across the region invest heavily in modernizing their infrastructure to meet increasing energy demands and sustainability goals. Consumer behavior is shifting towards a greater awareness of energy consumption, fueled by rising utility costs and a growing environmental consciousness, further propelling the demand for smart metering solutions that offer transparency and control. Technological advancements, such as the integration of IoT capabilities, advanced communication protocols (e.g., LoRaWAN, NB-IoT), and AI-powered analytics platforms, are enhancing the functionality and value proposition of smart meters. These disruptions are not only improving operational efficiency for utility providers but also empowering consumers with actionable insights into their usage patterns, leading to significant behavioral changes and energy savings. The penetration of smart meters is expected to increase exponentially as government mandates and pilot projects pave the way for large-scale rollouts. The transition from traditional meters to smart meters signifies a fundamental shift in how energy is managed and consumed, paving the way for a more digitized and intelligent energy ecosystem across the MEA region.

Dominant Regions, Countries, or Segments in Middle East and Africa Smart Meters Market

The Residential segment is emerging as a dominant force driving growth within the Middle East and Africa Smart Meters Market. This dominance is propelled by a confluence of factors, including increasing urbanization, a growing middle-class population with a desire for modern amenities, and a heightened awareness of energy conservation among households. Governments across the region are actively promoting smart home technologies and energy efficiency programs, directly benefiting the residential smart meter market. The sheer volume of residential units, coupled with utility-led initiatives to replace aging traditional meters with smart alternatives, creates a massive addressable market.

- Key Drivers for Residential Dominance:

- Urbanization and Population Growth: Rapid city expansion and increasing population density necessitate efficient utility management.

- Government Mandates and Incentives: Many nations are implementing policies that encourage or mandate smart meter adoption for residential consumers.

- Consumer Demand for Transparency and Control: Households are increasingly seeking tools to monitor and manage their energy and water consumption, leading to potential cost savings.

- Smart Home Integration: The proliferation of smart home devices creates a natural synergy with smart metering technologies.

- Reduction of Non-Revenue Water (NRW) and Energy Losses: Utilities are prioritizing smart metering in residential areas to curb significant losses.

The Commercial sector also represents a significant growth segment, driven by businesses seeking to optimize operational costs, improve sustainability reporting, and comply with environmental regulations. As businesses become more energy-conscious and adopt smart building technologies, the demand for granular energy consumption data provided by smart meters becomes crucial. The Industrial segment, while often characterized by fewer but larger installations, contributes significantly to the overall market value due to the high consumption volumes and the critical need for precise monitoring and control to ensure operational efficiency and prevent costly downtime. Countries like the UAE, Saudi Arabia, and South Africa are leading the charge with substantial investments in smart grid infrastructure, further bolstering the growth of all segments.

Middle East and Africa Smart Meters Market Product Landscape

The product landscape of the MEA Smart Meters Market is characterized by continuous innovation focused on enhancing connectivity, data security, and interoperability. Advanced smart meters now incorporate features such as remote meter reading, outage detection, real-time consumption monitoring, and two-way communication capabilities. Technologies like cellular, radio frequency (RF), and PLC are prevalent communication methods, with a growing emphasis on IoT-enabled solutions leveraging LPWAN technologies. The integration of AI and machine learning algorithms within smart meter platforms is enabling sophisticated data analytics for demand forecasting, anomaly detection, and predictive maintenance, offering unique selling propositions. Furthermore, the development of smart meters for water and gas is expanding the market's scope beyond electricity, catering to the integrated utility management needs of the region.

Key Drivers, Barriers & Challenges in Middle East and Africa Smart Meters Market

Key Drivers: The Middle East and Africa Smart Meters Market is propelled by several key drivers. Government initiatives and national smart grid strategies are instrumental, with many countries investing in modernization to improve energy efficiency and reduce losses. The increasing demand for effective water management, particularly in arid regions, is a significant catalyst for smart water meter adoption. Furthermore, rising energy costs and a growing environmental consciousness among consumers and businesses are creating a pull for smart metering solutions that offer transparency and control over consumption. Technological advancements, such as the integration of IoT and advanced communication technologies, are enhancing the functionality and appeal of smart meters.

Barriers & Challenges: Despite the growth potential, the market faces several barriers and challenges. The high upfront capital investment required for large-scale smart meter deployments remains a significant hurdle for many utilities. Robust cybersecurity infrastructure is crucial to protect sensitive data, and the threat of cyberattacks poses a constant concern. Regulatory fragmentation across different countries in the MEA region can complicate deployment strategies. Supply chain disruptions and the availability of skilled labor for installation and maintenance can also impact project timelines and costs. Intense competition among vendors, while beneficial for consumers, can also put pressure on profit margins for market players.

Emerging Opportunities in Middle East and Africa Smart Meters Market

Emerging opportunities in the MEA Smart Meters Market lie in the expanding smart city initiatives across the region, which often include integrated smart metering solutions for utilities. The increasing focus on renewable energy integration and grid stability presents a significant avenue for advanced smart meters capable of managing distributed energy resources. Furthermore, the growing demand for smart water management solutions in water-scarce countries offers a substantial untapped market. The development of sophisticated data analytics platforms that leverage smart meter data for grid optimization, predictive maintenance, and customer engagement represents another key opportunity for service providers. The potential for partnerships between technology providers, utilities, and government bodies to co-develop and implement innovative solutions is also high.

Growth Accelerators in the Middle East and Africa Smart Meters Market Industry

The Middle East and Africa Smart Meters Market is experiencing accelerated growth driven by several catalysts. Strategic partnerships between global smart meter manufacturers and local utility providers are crucial for market penetration and customized solution development. Government mandates and supportive policies, such as incentives for smart grid deployment and ambitious energy efficiency targets, are significantly accelerating adoption rates. Technological breakthroughs, including advancements in communication technologies, data analytics, and cybersecurity, are continuously enhancing the value proposition of smart meters, making them more attractive to utilities and consumers alike. The expansion of smart city projects across the region further acts as a major growth accelerator, integrating smart metering as a foundational element of urban infrastructure.

Key Players Shaping the Middle East and Africa Smart Meters Market Market

- Itron Inc.

- Sensus (Xylem Inc.)

- LANDIS+GYR Group AG

- Iskraemeco d d

- Diehl Metering FZE

- Kamstrup AS

- Hexing Electric Co Ltd

- Electromed (Termikel Group)

- Sagemcom SAS

- Holley Technology

Notable Milestones in Middle East and Africa Smart Meters Market Sector

- June 2022: The National Iranian Gas Company (NIGC) announced its intention to install 26 million smart gas meters across Iran over the next four years, signaling a major push for gas metering modernization.

- May 2022: Dubai Electricity & Water Authority (DEWA) revealed plans to invest upwards of USD 1.9 billion in implementing its updated Smart Grid Strategy for 2021-2035, highlighting a long-term commitment to smart utility infrastructure. This strategy builds upon the successful replacement of existing water and electricity meters with smart meters between 2015 and 2020 as part of the prior 2014-2035 Smart Grid Strategy.

- April 2022: DEWA launched a unique smart tool for assessing water and electricity consumption in Dubai homes, enhancing its Smart Living initiative. The addition of the Self-Assessment tool empowers residential customers to quickly understand their consumption patterns, utilizing a proactive mechanism that interacts with customers equipped with smart electricity and water meters.

In-Depth Middle East and Africa Smart Meters Market Market Outlook

The future outlook for the Middle East and Africa Smart Meters Market is exceptionally promising, fueled by sustained government backing, increasing utility investments in grid modernization, and a growing consumer demand for efficient resource management. Key growth accelerators include the rapid expansion of smart city projects, which integrate smart metering as a core component of urban infrastructure, and the ongoing technological evolution of smart meters to incorporate advanced IoT features and AI-driven analytics. Strategic partnerships between international technology providers and regional utilities will be crucial in tailoring solutions to meet specific market needs and overcome local challenges. The increasing focus on water conservation and the integration of renewable energy sources further present significant untapped market potential. Overall, the MEA smart meter market is on a trajectory of robust expansion, offering substantial opportunities for innovation and strategic investment in the coming years.

Middle East and Africa Smart Meters Market Segmentation

-

1. End User

- 1.1. Residential

- 1.2. Commercial

- 1.3. Industrial

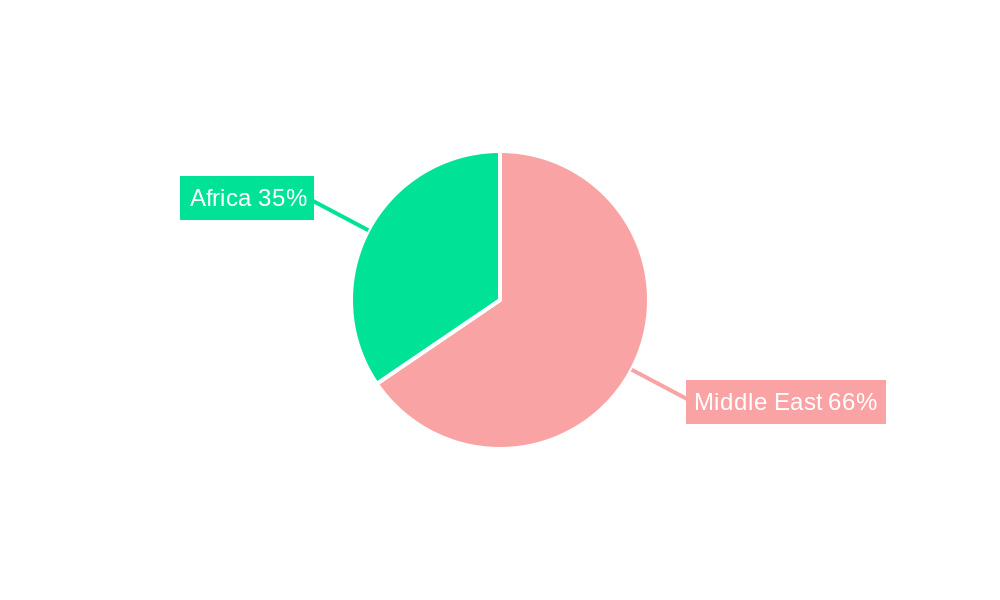

Middle East and Africa Smart Meters Market Segmentation By Geography

-

1. Middle East

- 1.1. Saudi Arabia

- 1.2. United Arab Emirates

- 1.3. Israel

- 1.4. Qatar

- 1.5. Kuwait

- 1.6. Oman

- 1.7. Bahrain

- 1.8. Jordan

- 1.9. Lebanon

Middle East and Africa Smart Meters Market Regional Market Share

Geographic Coverage of Middle East and Africa Smart Meters Market

Middle East and Africa Smart Meters Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.27% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by End User

- 5.1.1. Residential

- 5.1.2. Commercial

- 5.1.3. Industrial

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Middle East

- 5.1. Market Analysis, Insights and Forecast - by End User

- 6. Middle East and Africa Smart Meters Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by End User

- 6.1.1. Residential

- 6.1.2. Commercial

- 6.1.3. Industrial

- 6.1. Market Analysis, Insights and Forecast - by End User

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Itron Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Sensus (Xylem Inc )

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 LANDIS+GYR Group AG

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Iskraemeco d d

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Diehl Metering FZE

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Kamstrup AS

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Hexing Electric Co Ltd

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Electromed (Termikel Group)

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Sagemcom SAS*List Not Exhaustive

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Holley Technology

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Itron Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Middle East and Africa Smart Meters Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Middle East and Africa Smart Meters Market Share (%) by Company 2025

List of Tables

- Table 1: Middle East and Africa Smart Meters Market Revenue billion Forecast, by End User 2020 & 2033

- Table 2: Middle East and Africa Smart Meters Market Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Middle East and Africa Smart Meters Market Revenue billion Forecast, by End User 2020 & 2033

- Table 4: Middle East and Africa Smart Meters Market Revenue billion Forecast, by Country 2020 & 2033

- Table 5: Saudi Arabia Middle East and Africa Smart Meters Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 6: United Arab Emirates Middle East and Africa Smart Meters Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 7: Israel Middle East and Africa Smart Meters Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Qatar Middle East and Africa Smart Meters Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Kuwait Middle East and Africa Smart Meters Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Oman Middle East and Africa Smart Meters Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Bahrain Middle East and Africa Smart Meters Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Jordan Middle East and Africa Smart Meters Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Lebanon Middle East and Africa Smart Meters Market Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Middle East and Africa Smart Meters Market?

The projected CAGR is approximately 9.27%.

2. Which companies are prominent players in the Middle East and Africa Smart Meters Market?

Key companies in the market include Itron Inc, Sensus (Xylem Inc ), LANDIS+GYR Group AG, Iskraemeco d d, Diehl Metering FZE, Kamstrup AS, Hexing Electric Co Ltd, Electromed (Termikel Group), Sagemcom SAS*List Not Exhaustive, Holley Technology.

3. What are the main segments of the Middle East and Africa Smart Meters Market?

The market segments include End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 35.63 billion as of 2022.

5. What are some drivers contributing to market growth?

Need For Improvement in Energy Efficiency and Smart City Investments; Supportive Government Initiatives and Regulations.

6. What are the notable trends driving market growth?

Commercial Sector to Hold Significant Share.

7. Are there any restraints impacting market growth?

High Costs and Integration Difficulties with Smart Meters; Lack of Capital Investment for Infrastructure Installation.

8. Can you provide examples of recent developments in the market?

June 2022: The National Iranian Gas Company (NIGC) intends to install 26 million smart gas meters across Iran over the next four years.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Middle East and Africa Smart Meters Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Middle East and Africa Smart Meters Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Middle East and Africa Smart Meters Market?

To stay informed about further developments, trends, and reports in the Middle East and Africa Smart Meters Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence