Key Insights

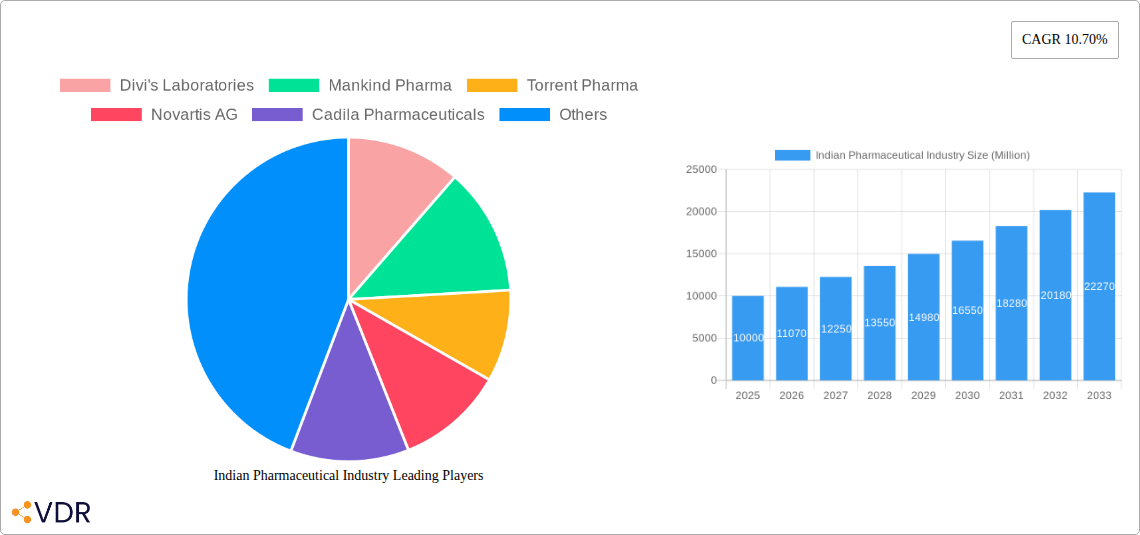

The Indian pharmaceutical industry, valued at approximately $XX million in 2025, is projected to experience robust growth, exhibiting a Compound Annual Growth Rate (CAGR) of 10.70% from 2025 to 2033. This expansion is fueled by several key drivers, including a rising prevalence of chronic diseases like diabetes and cardiovascular ailments within India's large and growing population. Furthermore, increasing government initiatives promoting healthcare accessibility and affordability, coupled with a surge in demand for generic drugs, are significantly contributing to market expansion. The industry benefits from a large pool of skilled labor and a robust manufacturing base, making it a cost-effective producer of pharmaceuticals for both domestic consumption and global export markets. However, stringent regulatory requirements, pricing pressures, and the intense competition from both domestic and multinational pharmaceutical companies present significant challenges to sustained growth.

Segmentation analysis reveals a diversified market across various drug types (Prescription, OTC, Generic) and therapeutic categories. Anti-infectives, cardiovascular, and gastrointestinal medications dominate market share, reflecting prevalent health concerns. Key players such as Sun Pharmaceutical Industries, Cipla, Dr. Reddy's Laboratories, and others are actively engaged in research and development, focusing on innovative drug delivery systems and novel therapeutic areas to maintain a competitive edge. The regional distribution showcases varied market penetration across North, South, East, and West India, with potential for further expansion in less-penetrated regions. Growth trajectory is expected to be influenced by factors such as the evolving healthcare landscape, technological advancements, and the effectiveness of public health initiatives. Successful navigation of regulatory hurdles and strategic partnerships will be critical for industry players to capitalize on the long-term growth opportunities presented by this dynamic market.

This comprehensive report provides an in-depth analysis of the Indian pharmaceutical industry, encompassing market dynamics, growth trends, key players, and future outlook. Covering the period 2019-2033, with a focus year of 2025, this report is an invaluable resource for industry professionals, investors, and researchers seeking to understand this dynamic sector. The report delves into both parent and child market segments, providing granular insights into various drug types and therapeutic categories.

Indian Pharmaceutical Industry Market Dynamics & Structure

The Indian pharmaceutical industry is characterized by a complex interplay of factors shaping its structure and growth trajectory. Market concentration is moderate, with a few large players dominating alongside numerous smaller companies. Technological innovation is a significant driver, particularly in generic drug manufacturing and the development of novel drug delivery systems. Stringent regulatory frameworks, including those set by the Drugs Controller General of India (DCGI), impact product approvals and market entry. The industry also faces competition from both domestic and international pharmaceutical companies. Furthermore, the market is influenced by evolving end-user demographics, rising healthcare expenditure, and increasing prevalence of chronic diseases. Mergers and acquisitions (M&A) activity plays a vital role in industry consolidation and expansion.

- Market Concentration: Moderate, with top 10 players holding approximately xx% of market share in 2024.

- Technological Innovation: Focus on generic drug production, biosimilars, and advanced drug delivery systems.

- Regulatory Framework: Stringent regulations impacting product approvals and timelines.

- Competitive Landscape: Intense competition from both domestic and multinational pharmaceutical companies.

- M&A Activity: Significant M&A activity observed in recent years, with xx deals valued at approximately xx Million units in 2024.

Indian Pharmaceutical Industry Growth Trends & Insights

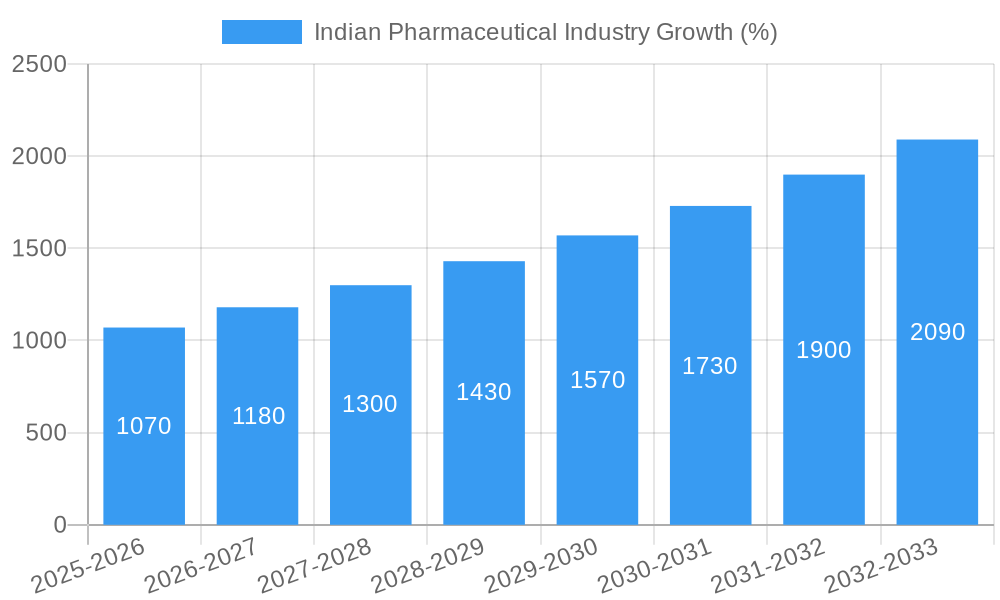

The Indian pharmaceutical market has exhibited robust growth over the historical period (2019-2024), driven by factors such as increasing healthcare expenditure, rising prevalence of chronic diseases, and growing demand for affordable medicines. The market size experienced a CAGR of xx% during 2019-2024, reaching xx Million units in 2024. This positive trend is projected to continue during the forecast period (2025-2033), with an anticipated CAGR of xx%. Technological advancements, particularly in the development of biosimilars and personalized medicines, are expected to significantly influence market growth. Changing consumer behavior, including increased awareness of health and wellness, is also contributing to market expansion. The adoption rate of new technologies and innovative therapies is gradually increasing.

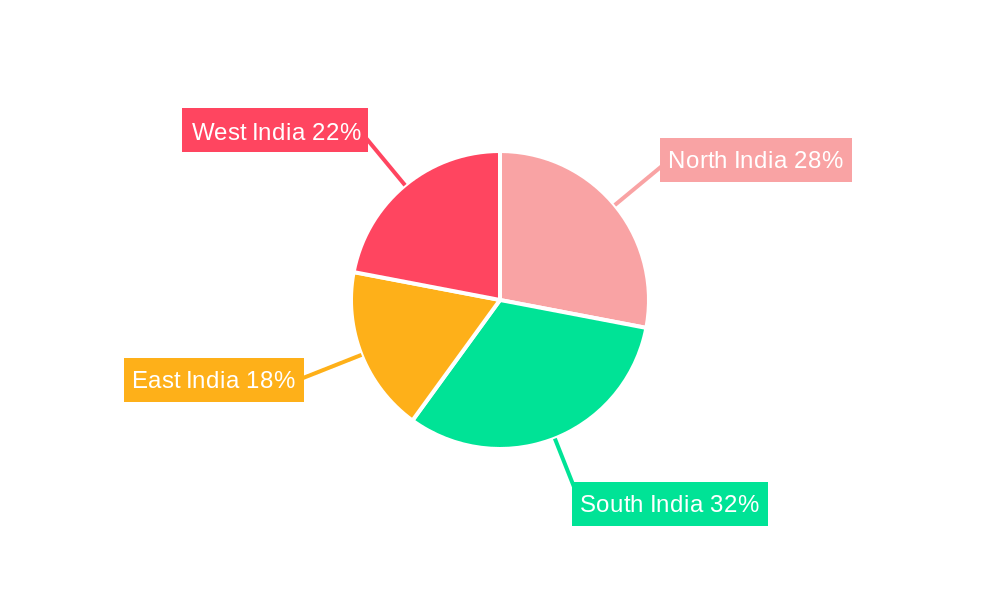

Dominant Regions, Countries, or Segments in Indian Pharmaceutical Industry

While the Indian pharmaceutical market is relatively widespread, certain regions and segments are showing accelerated growth. Within drug types, the generic drug segment dominates, accounting for approximately xx% of the market share in 2024, driven by affordability and cost-effectiveness. Among therapeutic categories, anti-infectives, cardiovascular, and anti-diabetic segments are leading the growth, driven by the high prevalence of related diseases. Metropolitan areas and economically developed states exhibit higher market penetration compared to rural areas.

- Dominant Drug Type: Generic Drugs (xx Million units in 2024)

- Leading Therapeutic Categories: Anti-infectives, Cardiovascular, Anti-diabetic.

- Key Growth Drivers: Rising prevalence of chronic diseases, increasing healthcare expenditure, government initiatives promoting affordable healthcare.

- Regional Variations: Higher market penetration in urban areas and economically developed states.

Indian Pharmaceutical Industry Product Landscape

The Indian pharmaceutical industry offers a diverse range of products, including innovative drugs, generic medicines, and biosimilars. Product innovation focuses primarily on improving efficacy, safety, and affordability. Key performance metrics include drug efficacy, safety profile, and cost-effectiveness. Companies are increasingly adopting strategies to enhance the unique selling propositions (USPs) of their products, focusing on factors like faster onset of action, improved bioavailability, and patient-centric formulations. Technological advancements in drug delivery systems, such as sustained-release formulations and targeted drug delivery, are also shaping the product landscape.

Key Drivers, Barriers & Challenges in Indian Pharmaceutical Industry

Key Drivers:

- Increasing prevalence of chronic diseases

- Rising healthcare expenditure

- Government initiatives to promote affordable healthcare

- Growing demand for generic and biosimilar drugs.

Challenges:

- Stringent regulatory requirements leading to longer approval timelines. (Impacting market entry by xx%)

- Supply chain disruptions causing production delays and price volatility. (Estimated impact on production: xx%)

- Intense competition from both domestic and international companies.

Emerging Opportunities in Indian Pharmaceutical Industry

The Indian pharmaceutical industry presents several lucrative opportunities, including the untapped potential of rural markets, the growing demand for specialized healthcare services, and the expanding market for biosimilars. The increasing adoption of digital health technologies also opens new opportunities for remote patient monitoring and personalized medicine. Furthermore, the government's focus on promoting healthcare infrastructure creates a favorable environment for investment and growth.

Growth Accelerators in the Indian Pharmaceutical Industry

Several factors are expected to fuel the long-term growth of the Indian pharmaceutical industry. These include advancements in drug discovery and development, increased investments in research and development, strategic collaborations between domestic and international companies, expansion into new geographical markets, and increasing government support for the sector.

Key Players Shaping the Indian Pharmaceutical Industry Market

- Divi's Laboratories

- Mankind Pharma

- Torrent Pharma

- Novartis AG

- Cadila Pharmaceuticals

- Aurobindo Pharma Limited

- Merck & Co Inc

- Sun Pharmaceutical Industries Ltd

- Cipla Inc

- Lupin Limited

- Biocon Limited

- GlaxoSmithKline plc

- Dr Reddy's Laboratories Ltd

- Abbott

- Pfizer Inc

Notable Milestones in Indian Pharmaceutical Industry Sector

- November 2021: Cipla Limited received EUA permission from the DCGI for Molnupiravir.

- February 2022: Dr. Reddy's Laboratories Ltd. secured DCGI approval for the Sputnik Light vaccine.

In-Depth Indian Pharmaceutical Industry Market Outlook

The Indian pharmaceutical industry is poised for continued growth, driven by a confluence of factors including increasing healthcare spending, a rising prevalence of chronic diseases, and the potential for significant innovation within the sector. Strategic partnerships, investments in R&D, and expansion into new markets will play crucial roles in unlocking the industry's full potential. The focus on affordable healthcare and the government's support for the pharmaceutical sector contribute to a positive outlook for the coming years.

Indian Pharmaceutical Industry Segmentation

-

1. Therapeutic Category

- 1.1. Anti-Infectives

- 1.2. Cardiovascular

- 1.3. Gastrointestinal

- 1.4. Anti Diabetic

- 1.5. Respiratory

- 1.6. Dermatologicals

- 1.7. Musculo-Skeletal System

- 1.8. Nervous System

- 1.9. Others

-

2. Drug Type

-

2.1. Prescription Drug

- 2.1.1. Branded Drugs

- 2.1.2. Generic Drugs

- 2.2. OTC Drugs

-

2.1. Prescription Drug

Indian Pharmaceutical Industry Segmentation By Geography

- 1. India

Indian Pharmaceutical Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 10.70% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Low Cost of Production and Increased R&D Activities; Increased Expenditure on Healthcare and Medicine

- 3.3. Market Restrains

- 3.3.1. Lack of a Stable Pricing and Policy Environment; Lack in Development of Innovative Drugs

- 3.4. Market Trends

- 3.4.1. The Respiratory Therapeutic Category Segment is Expected to Show Healthy Market Growth in the Forecast Period

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Indian Pharmaceutical Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Therapeutic Category

- 5.1.1. Anti-Infectives

- 5.1.2. Cardiovascular

- 5.1.3. Gastrointestinal

- 5.1.4. Anti Diabetic

- 5.1.5. Respiratory

- 5.1.6. Dermatologicals

- 5.1.7. Musculo-Skeletal System

- 5.1.8. Nervous System

- 5.1.9. Others

- 5.2. Market Analysis, Insights and Forecast - by Drug Type

- 5.2.1. Prescription Drug

- 5.2.1.1. Branded Drugs

- 5.2.1.2. Generic Drugs

- 5.2.2. OTC Drugs

- 5.2.1. Prescription Drug

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. India

- 5.1. Market Analysis, Insights and Forecast - by Therapeutic Category

- 6. North India Indian Pharmaceutical Industry Analysis, Insights and Forecast, 2019-2031

- 7. South India Indian Pharmaceutical Industry Analysis, Insights and Forecast, 2019-2031

- 8. East India Indian Pharmaceutical Industry Analysis, Insights and Forecast, 2019-2031

- 9. West India Indian Pharmaceutical Industry Analysis, Insights and Forecast, 2019-2031

- 10. Competitive Analysis

- 10.1. Market Share Analysis 2024

- 10.2. Company Profiles

- 10.2.1 Divi's Laboratories

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 Mankind Pharma

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 Torrent Pharma

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 Novartis AG

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 Cadila Pharmaceuticals

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 Aurobindo Pharma Limited

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 Merck & Co Inc

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 Sun Pharmaceutical Industries Ltd

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.9 Cipla Inc

- 10.2.9.1. Overview

- 10.2.9.2. Products

- 10.2.9.3. SWOT Analysis

- 10.2.9.4. Recent Developments

- 10.2.9.5. Financials (Based on Availability)

- 10.2.10 Lupin Limited

- 10.2.10.1. Overview

- 10.2.10.2. Products

- 10.2.10.3. SWOT Analysis

- 10.2.10.4. Recent Developments

- 10.2.10.5. Financials (Based on Availability)

- 10.2.11 Biocon Limited

- 10.2.11.1. Overview

- 10.2.11.2. Products

- 10.2.11.3. SWOT Analysis

- 10.2.11.4. Recent Developments

- 10.2.11.5. Financials (Based on Availability)

- 10.2.12 GlaxoSmithKline plc

- 10.2.12.1. Overview

- 10.2.12.2. Products

- 10.2.12.3. SWOT Analysis

- 10.2.12.4. Recent Developments

- 10.2.12.5. Financials (Based on Availability)

- 10.2.13 Dr Reddy's Laboratories Ltd

- 10.2.13.1. Overview

- 10.2.13.2. Products

- 10.2.13.3. SWOT Analysis

- 10.2.13.4. Recent Developments

- 10.2.13.5. Financials (Based on Availability)

- 10.2.14 Abbott

- 10.2.14.1. Overview

- 10.2.14.2. Products

- 10.2.14.3. SWOT Analysis

- 10.2.14.4. Recent Developments

- 10.2.14.5. Financials (Based on Availability)

- 10.2.15 Pfizer Inc

- 10.2.15.1. Overview

- 10.2.15.2. Products

- 10.2.15.3. SWOT Analysis

- 10.2.15.4. Recent Developments

- 10.2.15.5. Financials (Based on Availability)

- 10.2.1 Divi's Laboratories

List of Figures

- Figure 1: Indian Pharmaceutical Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Indian Pharmaceutical Industry Share (%) by Company 2024

List of Tables

- Table 1: Indian Pharmaceutical Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Indian Pharmaceutical Industry Revenue Million Forecast, by Therapeutic Category 2019 & 2032

- Table 3: Indian Pharmaceutical Industry Revenue Million Forecast, by Drug Type 2019 & 2032

- Table 4: Indian Pharmaceutical Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Indian Pharmaceutical Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: North India Indian Pharmaceutical Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: South India Indian Pharmaceutical Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: East India Indian Pharmaceutical Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: West India Indian Pharmaceutical Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Indian Pharmaceutical Industry Revenue Million Forecast, by Therapeutic Category 2019 & 2032

- Table 11: Indian Pharmaceutical Industry Revenue Million Forecast, by Drug Type 2019 & 2032

- Table 12: Indian Pharmaceutical Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Indian Pharmaceutical Industry?

The projected CAGR is approximately 10.70%.

2. Which companies are prominent players in the Indian Pharmaceutical Industry?

Key companies in the market include Divi's Laboratories, Mankind Pharma, Torrent Pharma, Novartis AG, Cadila Pharmaceuticals, Aurobindo Pharma Limited, Merck & Co Inc, Sun Pharmaceutical Industries Ltd, Cipla Inc, Lupin Limited, Biocon Limited, GlaxoSmithKline plc, Dr Reddy's Laboratories Ltd, Abbott, Pfizer Inc.

3. What are the main segments of the Indian Pharmaceutical Industry?

The market segments include Therapeutic Category, Drug Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Low Cost of Production and Increased R&D Activities; Increased Expenditure on Healthcare and Medicine.

6. What are the notable trends driving market growth?

The Respiratory Therapeutic Category Segment is Expected to Show Healthy Market Growth in the Forecast Period.

7. Are there any restraints impacting market growth?

Lack of a Stable Pricing and Policy Environment; Lack in Development of Innovative Drugs.

8. Can you provide examples of recent developments in the market?

In February 2022, Dr. Reddy's Laboratories Ltd. announced that the Drugs Controller General of India (DCGI) had approved the single-shot Sputnik Light vaccine for restricted use in an emergency in India.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Indian Pharmaceutical Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Indian Pharmaceutical Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Indian Pharmaceutical Industry?

To stay informed about further developments, trends, and reports in the Indian Pharmaceutical Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence