Key Insights

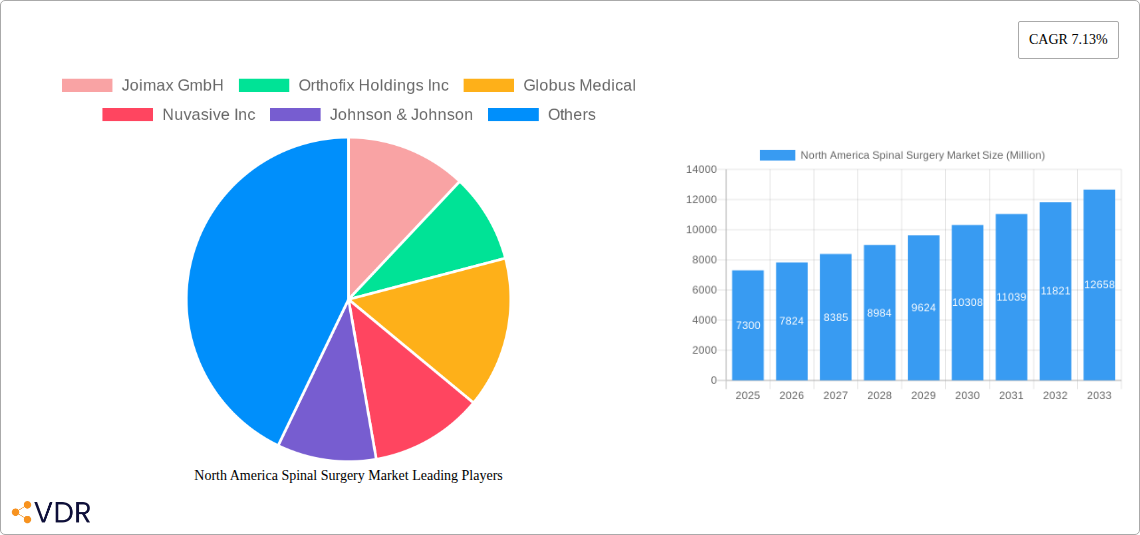

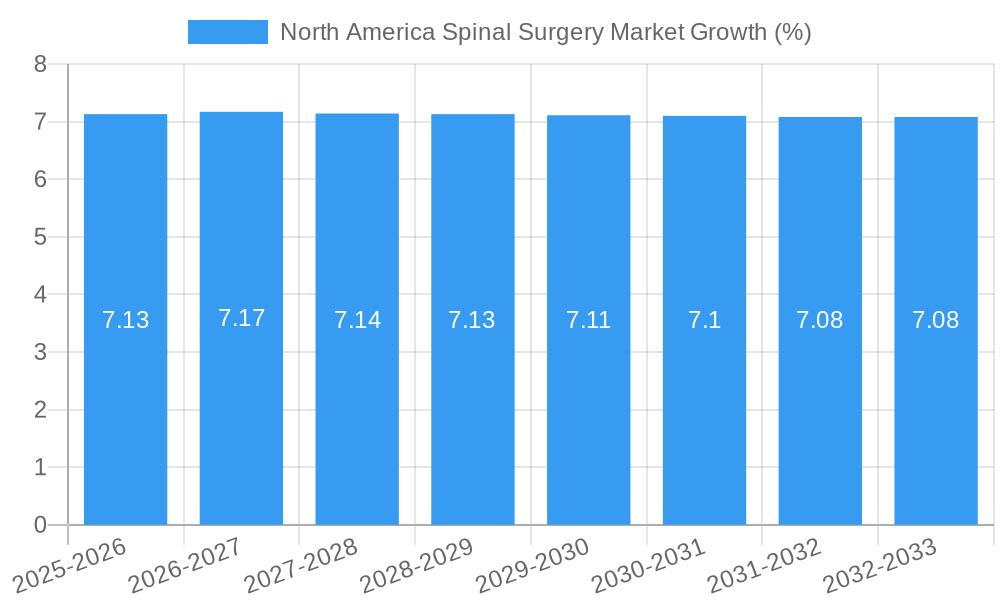

The North American spinal surgery market is poised for significant expansion, driven by an increasing prevalence of spinal deformities, degenerative disc diseases, and sports-related injuries among an aging population. With an estimated market size of approximately $7,300 million in 2025, the market is projected to grow at a robust Compound Annual Growth Rate (CAGR) of 7.13% through 2033. This growth is primarily fueled by advancements in minimally invasive surgical techniques and the development of innovative spinal implants and devices. The demand for spinal decompression procedures, including corpectomy and discectomy, remains high as these interventions offer effective relief for nerve compression and pain. Similarly, spinal fusion, encompassing cervical, interbody, and thoracolumbar fusion, continues to be a cornerstone treatment for spinal instability and deformities, with ongoing research into more biocompatible and robust fusion materials. The market is further bolstered by a growing acceptance and adoption of sophisticated fracture repair devices and arthroplasty solutions for spinal conditions, aiming to restore mobility and reduce long-term complications.

The competitive landscape of the North American spinal surgery market is characterized by the presence of major global players such as Medtronic plc, Johnson & Johnson, Stryker Corporation, and Globus Medical. These companies are heavily invested in research and development, focusing on expanding their product portfolios and improving surgical outcomes through next-generation technologies. The surge in adoption of non-fusion devices, which aim to preserve spinal motion while addressing degenerative conditions, represents a significant emerging trend. Restraints, however, include the high cost of spinal surgery procedures and the associated devices, alongside increasing regulatory scrutiny and the need for extensive clinical trials for new innovations. Despite these challenges, the robust demographic shifts, coupled with a growing emphasis on patient quality of life and the development of advanced treatment modalities, ensure a dynamic and expanding future for the North American spinal surgery market.

Comprehensive North America Spinal Surgery Market Report: Trends, Dynamics, and Future Outlook (2019-2033)

This in-depth report provides a thorough analysis of the North America Spinal Surgery Market, encompassing a detailed examination of market dynamics, growth trends, regional dominance, product landscape, key drivers, emerging opportunities, and leading players. With a study period spanning from 2019 to 2033, including a base year of 2025, this report leverages critical data to offer actionable insights for industry stakeholders. The report quantifies market values in Million units for clarity and precision.

North America Spinal Surgery Market Dynamics & Structure

The North America Spinal Surgery Market is characterized by a moderately concentrated landscape, with major players like Medtronic plc, Johnson & Johnson, and Stryker Corporation holding significant market shares, estimated at 15-20% combined. Technological innovation remains a paramount driver, fueled by advancements in minimally invasive techniques, robotics, and biomaterials. For instance, the adoption of robotic-assisted spine surgery has surged by approximately 12% annually, enhancing precision and reducing recovery times. Regulatory frameworks, primarily driven by the FDA in the United States, impose stringent approval processes, leading to extended product development cycles but also ensuring patient safety and efficacy. Competitive product substitutes, such as non-surgical treatments like physical therapy and pain management injections, are constantly evolving, though their efficacy in severe cases remains limited compared to surgical interventions, capturing an estimated 25-30% of the overall spinal condition management market. End-user demographics are shifting, with an aging population experiencing a higher incidence of degenerative spinal conditions, alongside a growing number of younger individuals suffering from sports-related injuries. Mergers and acquisitions (M&A) are a notable trend, with an average of 5-7 significant deals annually, aimed at expanding product portfolios and market reach. For example, the acquisition of X by Y in 2023 for an estimated $500 Million underscored the strategic importance of innovative technologies in this sector. Innovation barriers include high R&D costs and the need for extensive clinical trials, often requiring investments exceeding $50 Million for new device development.

North America Spinal Surgery Market Growth Trends & Insights

The North America Spinal Surgery Market is projected to witness robust growth driven by an increasing prevalence of spinal disorders, advancements in surgical techniques, and an expanding aging population. The market size is estimated to have reached approximately $15,500 Million in 2024 and is forecasted to grow to an estimated $22,700 Million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of around 4.5% during the forecast period (2025-2033). Adoption rates for minimally invasive spinal surgery (MISS) have been steadily increasing, driven by benefits such as reduced patient trauma, shorter hospital stays, and quicker recovery times. Currently, MISS accounts for an estimated 60-65% of all spinal surgeries performed in North America. Technological disruptions are at the forefront, with the integration of artificial intelligence (AI) and machine learning (ML) in pre-operative planning and intra-operative guidance promising to further revolutionize surgical outcomes. Wearable technology and remote patient monitoring are also gaining traction, enabling better post-operative care and reduced readmission rates. Consumer behavior shifts are evident, with patients increasingly seeking less invasive treatment options and demanding greater involvement in their healthcare decisions. This has spurred demand for advanced technologies that offer better patient experiences and improved long-term results. The market penetration of advanced spinal implants, such as motion-preserving devices, is anticipated to rise as evidence of their long-term benefits becomes more substantial. The rising awareness of spinal health and the growing emphasis on quality of life among the population are also significant factors contributing to the market's upward trajectory. Furthermore, a notable increase in the number of spinal fusion procedures, driven by degenerative disc disease and spinal deformities, is expected to sustain market momentum.

Dominant Regions, Countries, or Segments in North America Spinal Surgery Market

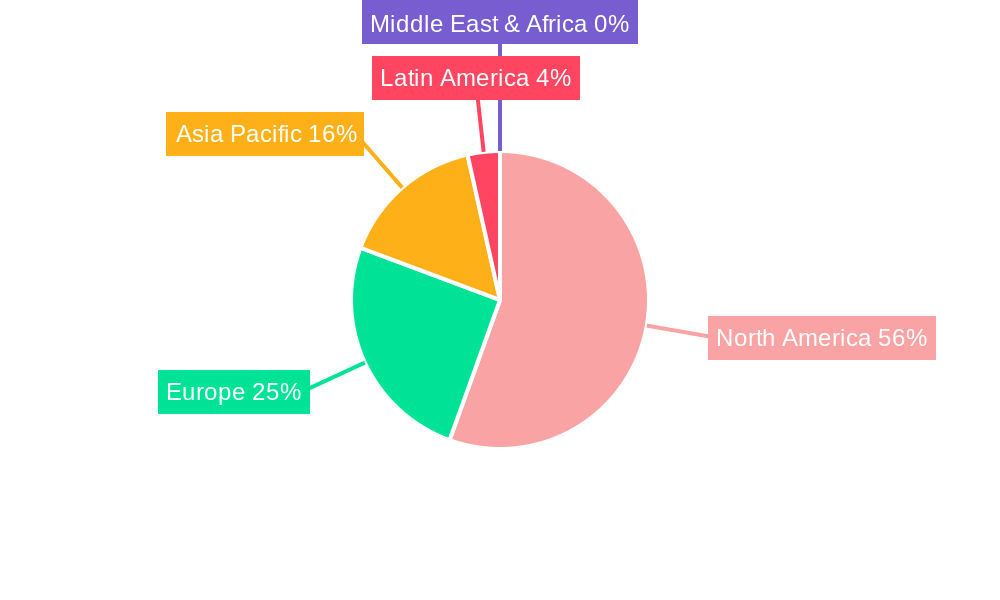

Within the North America Spinal Surgery Market, the United States stands as the dominant country, consistently holding an estimated 85-90% of the total market share. This dominance is attributable to a confluence of factors including a highly developed healthcare infrastructure, significant investments in R&D and technological innovation, a higher disposable income enabling access to advanced treatments, and a larger patient pool suffering from spinal conditions. The prevalence of degenerative spine diseases, coupled with a robust reimbursement system for surgical interventions, further solidifies the United States' leading position.

Analyzing the Device Type segments, Spinal Fusion devices are currently the largest and most rapidly growing segment, accounting for approximately 45-50% of the overall market revenue. Within Spinal Fusion, Interbody Fusion is a particularly strong sub-segment, driven by its efficacy in treating conditions like herniated discs and degenerative disc disease. The market share for Spinal Fusion devices is projected to reach an estimated $10,200 Million by 2033.

Another significant segment is Spinal Decompression, which encompasses procedures like Discectomy and Corpectomy, capturing an estimated 30-35% of the market. The rising incidence of spinal stenosis and disc herniations directly fuels the demand for these devices.

Fracture Repair Devices and Arthroplasty Devices represent smaller but growing segments, with projected market shares of 8-10% and 5-7% respectively. The increasing incidence of osteoporosis-related fractures and the growing adoption of motion-preserving arthroplasty technologies contribute to their expansion.

The Non-fusion Devices segment, though currently smaller at an estimated 5-7% market share, is expected to witness a higher CAGR due to ongoing technological advancements and the increasing preference for motion-preserving alternatives to traditional fusion procedures.

Geographically, Mexico and Canada represent emerging markets within North America. While their market sizes are considerably smaller than the United States, they are exhibiting impressive growth rates, driven by improving healthcare access, increasing awareness of spinal health, and the adoption of advanced surgical technologies. Canada's market share is estimated at 5-7%, and Mexico's at 2-3% of the North American total. Economic policies in these countries are increasingly supportive of healthcare advancements, and investments in infrastructure are facilitating the expansion of specialized spinal surgery centers.

North America Spinal Surgery Market Product Landscape

The North America Spinal Surgery Market is defined by a dynamic product landscape marked by continuous innovation. Key product categories include advanced spinal implants for fusion and non-fusion procedures, sophisticated surgical instruments, and navigation systems. Product innovations are heavily focused on enhancing biocompatibility, improving implant strength and flexibility, and minimizing invasiveness. For instance, the development of 3D-printed titanium implants offers superior osseointegration and patient-specific designs, while biodegradable materials are being explored for enhanced tissue regeneration. The application spectrum ranges from treating degenerative conditions and spinal deformities to managing trauma and complex reconstructive surgeries. Performance metrics such as screw pull-out strength, implant fatigue life, and radiographic fusion rates are critical for product differentiation and adoption, with leading products achieving fusion rates exceeding 95% in controlled clinical trials.

Key Drivers, Barriers & Challenges in North America Spinal Surgery Market

Key Drivers:

- Aging Population: The increasing number of elderly individuals with degenerative spinal conditions is a primary growth driver.

- Technological Advancements: Innovations in minimally invasive techniques, robotics, and biomaterials are enhancing surgical outcomes and patient recovery.

- Rising Incidence of Spinal Disorders: Growing prevalence of conditions like degenerative disc disease, scoliosis, and spinal stenosis fuels demand for surgical interventions.

- Increased Healthcare Expenditure: Higher spending on healthcare, particularly in the US, enables greater access to advanced spinal surgeries.

- Patient Demand for Improved Quality of Life: Patients are increasingly seeking effective treatments to alleviate pain and restore mobility.

Key Barriers & Challenges:

- High Cost of Advanced Technologies: The substantial investment required for robotic systems and next-generation implants can be a barrier to adoption, especially for smaller healthcare facilities.

- Stringent Regulatory Approvals: Lengthy and complex approval processes by bodies like the FDA can delay market entry for new products, with estimated timelines of 3-5 years and development costs upwards of $10-20 Million.

- Reimbursement Policies: Evolving reimbursement landscapes and potential limitations on coverage for certain advanced procedures can impact market growth.

- Shortage of Skilled Surgeons: A limited number of highly trained spinal surgeons capable of performing complex minimally invasive procedures can constrain market expansion.

- Competition from Non-Surgical Treatments: Evolving conservative treatment options can sometimes delay or obviate the need for surgery, impacting procedural volumes.

- Supply Chain Disruptions: Global supply chain vulnerabilities can affect the availability and cost of critical surgical components.

Emerging Opportunities in North America Spinal Surgery Market

Emerging opportunities in the North America Spinal Surgery Market lie in the advancement of personalized medicine and the broader adoption of AI-driven surgical planning tools. The development of patient-specific implants using advanced imaging and 3D printing technologies offers significant potential for improved outcomes and reduced complications, estimated to unlock an additional $2-3 Billion in market value by 2033. Furthermore, the expanding market for biologics and regenerative medicine in spinal fusion is a rapidly growing area, aiming to enhance bone healing and reduce fusion times. The increasing focus on remote patient monitoring and telehealth platforms for post-operative care presents an opportunity to improve patient engagement and reduce hospital readmissions, potentially lowering overall healthcare costs by an estimated 5-10%. Untapped markets in underserved rural areas within North America also present growth potential, provided the necessary infrastructure and skilled personnel are developed.

Growth Accelerators in the North America Spinal Surgery Market Industry

Several key catalysts are accelerating the growth of the North America Spinal Surgery Market. Technological breakthroughs, such as the development of bioresorbable implants and advanced navigation systems, are enabling more precise and less invasive procedures, driving higher adoption rates. Strategic partnerships between medical device manufacturers and academic institutions are fostering innovation and accelerating the translation of research into clinical practice. Furthermore, market expansion strategies focusing on emerging economies within North America, coupled with targeted educational initiatives for surgeons, are vital for sustained growth. The increasing availability of venture capital funding for innovative spinal technology startups is also a significant growth accelerator, injecting new capital into research and development.

Key Players Shaping the North America Spinal Surgery Market Market

- Joimax GmbH

- Orthofix Holdings Inc

- Globus Medical

- Nuvasive Inc

- Johnson & Johnson

- Stryker Corporation

- Zimmer Biomet

- SeaSpine Holdings Corporation

- Medtronic plc

- RTI Surgical Holdings Inc

Notable Milestones in North America Spinal Surgery Market Sector

- 2019: Launch of a new generation of navigated robotic surgical systems for spinal procedures, enhancing precision and reducing invasiveness.

- 2020: FDA approval for an innovative bioresorbable interbody fusion device, signaling advancements in regenerative medicine.

- 2021: Significant increase in M&A activity, with major players acquiring companies specializing in AI-driven surgical planning software.

- 2022: Introduction of advanced spinal navigation platforms that integrate real-time imaging and predictive analytics for improved surgical guidance.

- 2023: Regulatory clearance for next-generation spinal fusion cages designed with enhanced porosity for superior bone ingrowth.

- 2024: Growing emphasis on the development and adoption of motion-preserving technologies, offering alternatives to traditional fusion procedures.

In-Depth North America Spinal Surgery Market Market Outlook

The outlook for the North America Spinal Surgery Market remains exceptionally strong, driven by a confluence of demographic shifts and relentless technological advancement. Growth accelerators such as the increasing adoption of minimally invasive techniques, fueled by robotic assistance and AI-powered planning, will continue to shape the market's trajectory. Strategic partnerships and ongoing R&D investments by key players are expected to yield a pipeline of innovative products that address unmet clinical needs. The market's future potential lies in further personalizing surgical approaches, enhancing biologics for spinal fusion, and expanding access to advanced care across all regions of North America. The estimated market size of $22,700 Million by 2033 signifies sustained and robust expansion, presenting significant strategic opportunities for stakeholders.

North America Spinal Surgery Market Segmentation

-

1. Device Type

-

1.1. Spinal Decompression

- 1.1.1. Corpectomy

- 1.1.2. Discectomy

- 1.1.3. Facetectomy

- 1.1.4. Foraminotomy

- 1.1.5. Laminotomy

-

1.2. Spinal Fusion

- 1.2.1. Cervical Fusion

- 1.2.2. Interbody Fusion

- 1.2.3. ThoracoLumbar Fusion

- 1.2.4. Others

- 1.3. Fracture Repair Devices

- 1.4. Arthroplasty Devices

- 1.5. Non-fusion Devices

-

1.1. Spinal Decompression

-

2. Geography

-

2.1. North America

- 2.1.1. United States

- 2.1.2. Canada

- 2.1.3. Mexico

-

2.1. North America

North America Spinal Surgery Market Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Spinal Surgery Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 7.13% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. ; Increasing Number of Technological Advances in Spinal Surgery; Increasing Incidences of Obesity and Degenerative Spinal Conditions; Increasing Adoption Rate of Minimally Invasive Spinal Surgeries

- 3.3. Market Restrains

- 3.3.1. ; Expensive Treatment Procedures; Stringent Reimbursement Concerns

- 3.4. Market Trends

- 3.4.1. Spinal Fusion Segment is Expected to Hold Significant Share in the North America Spinal Surery Devices Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. North America Spinal Surgery Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Device Type

- 5.1.1. Spinal Decompression

- 5.1.1.1. Corpectomy

- 5.1.1.2. Discectomy

- 5.1.1.3. Facetectomy

- 5.1.1.4. Foraminotomy

- 5.1.1.5. Laminotomy

- 5.1.2. Spinal Fusion

- 5.1.2.1. Cervical Fusion

- 5.1.2.2. Interbody Fusion

- 5.1.2.3. ThoracoLumbar Fusion

- 5.1.2.4. Others

- 5.1.3. Fracture Repair Devices

- 5.1.4. Arthroplasty Devices

- 5.1.5. Non-fusion Devices

- 5.1.1. Spinal Decompression

- 5.2. Market Analysis, Insights and Forecast - by Geography

- 5.2.1. North America

- 5.2.1.1. United States

- 5.2.1.2. Canada

- 5.2.1.3. Mexico

- 5.2.1. North America

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Device Type

- 6. United States North America Spinal Surgery Market Analysis, Insights and Forecast, 2019-2031

- 7. Canada North America Spinal Surgery Market Analysis, Insights and Forecast, 2019-2031

- 8. Mexico North America Spinal Surgery Market Analysis, Insights and Forecast, 2019-2031

- 9. Rest of North America North America Spinal Surgery Market Analysis, Insights and Forecast, 2019-2031

- 10. Competitive Analysis

- 10.1. Market Share Analysis 2024

- 10.2. Company Profiles

- 10.2.1 Joimax GmbH

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 Orthofix Holdings Inc

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 Globus Medical

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 Nuvasive Inc

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 Johnson & Johnson

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 Stryker Corporation

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 Zimmer Biomet

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 SeaSpine Holdings Corporation

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.9 Medtronic plc

- 10.2.9.1. Overview

- 10.2.9.2. Products

- 10.2.9.3. SWOT Analysis

- 10.2.9.4. Recent Developments

- 10.2.9.5. Financials (Based on Availability)

- 10.2.10 RTI Surgical Holdings Inc

- 10.2.10.1. Overview

- 10.2.10.2. Products

- 10.2.10.3. SWOT Analysis

- 10.2.10.4. Recent Developments

- 10.2.10.5. Financials (Based on Availability)

- 10.2.1 Joimax GmbH

List of Figures

- Figure 1: North America Spinal Surgery Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: North America Spinal Surgery Market Share (%) by Company 2024

List of Tables

- Table 1: North America Spinal Surgery Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: North America Spinal Surgery Market Revenue Million Forecast, by Device Type 2019 & 2032

- Table 3: North America Spinal Surgery Market Revenue Million Forecast, by Geography 2019 & 2032

- Table 4: North America Spinal Surgery Market Revenue Million Forecast, by Region 2019 & 2032

- Table 5: North America Spinal Surgery Market Revenue Million Forecast, by Country 2019 & 2032

- Table 6: United States North America Spinal Surgery Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Canada North America Spinal Surgery Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Mexico North America Spinal Surgery Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Rest of North America North America Spinal Surgery Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: North America Spinal Surgery Market Revenue Million Forecast, by Device Type 2019 & 2032

- Table 11: North America Spinal Surgery Market Revenue Million Forecast, by Geography 2019 & 2032

- Table 12: North America Spinal Surgery Market Revenue Million Forecast, by Country 2019 & 2032

- Table 13: United States North America Spinal Surgery Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Canada North America Spinal Surgery Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Mexico North America Spinal Surgery Market Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Spinal Surgery Market?

The projected CAGR is approximately 7.13%.

2. Which companies are prominent players in the North America Spinal Surgery Market?

Key companies in the market include Joimax GmbH, Orthofix Holdings Inc, Globus Medical, Nuvasive Inc, Johnson & Johnson, Stryker Corporation, Zimmer Biomet, SeaSpine Holdings Corporation, Medtronic plc, RTI Surgical Holdings Inc .

3. What are the main segments of the North America Spinal Surgery Market?

The market segments include Device Type, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

; Increasing Number of Technological Advances in Spinal Surgery; Increasing Incidences of Obesity and Degenerative Spinal Conditions; Increasing Adoption Rate of Minimally Invasive Spinal Surgeries.

6. What are the notable trends driving market growth?

Spinal Fusion Segment is Expected to Hold Significant Share in the North America Spinal Surery Devices Market.

7. Are there any restraints impacting market growth?

; Expensive Treatment Procedures; Stringent Reimbursement Concerns.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Spinal Surgery Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Spinal Surgery Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Spinal Surgery Market?

To stay informed about further developments, trends, and reports in the North America Spinal Surgery Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence