Key Insights

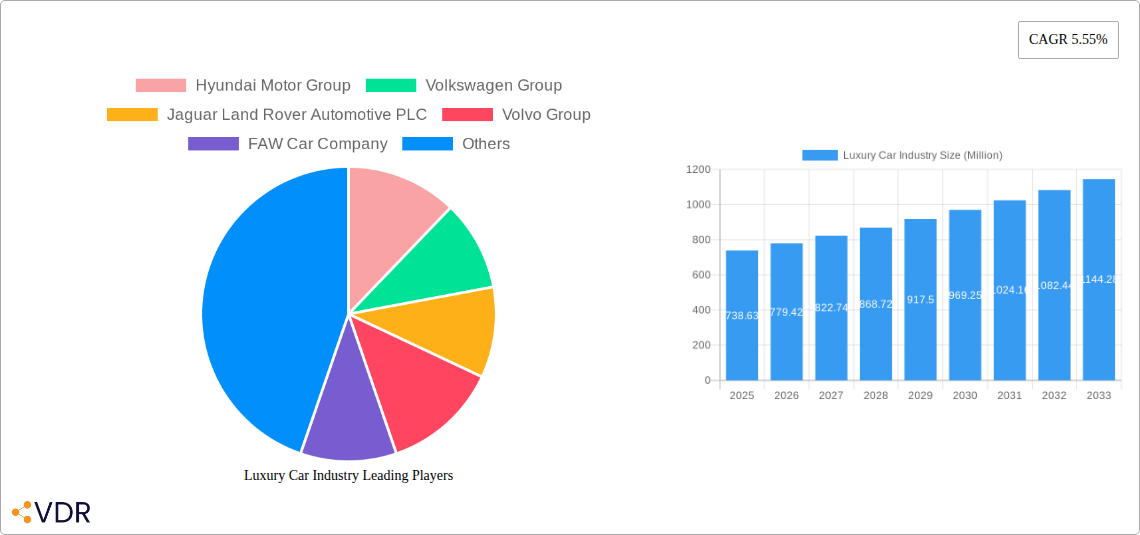

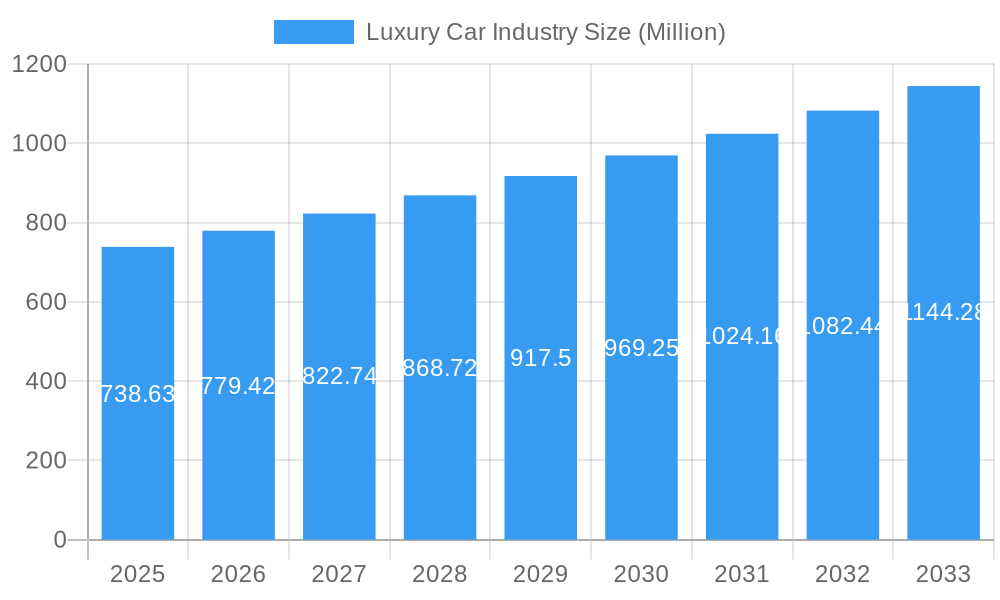

The global Luxury Car Industry is poised for robust growth, with a current market size of USD 738.63 million. This expansion is underpinned by a projected Compound Annual Growth Rate (CAGR) of 5.55% over the forecast period of 2025-2033, indicating a dynamic and evolving market landscape. A significant driver of this growth is the increasing disposable income in emerging economies, coupled with a rising consumer preference for premium vehicles that offer superior performance, advanced technology, and enhanced comfort. Furthermore, the industry is witnessing a pronounced shift towards electrification, with electric and hybrid luxury cars gaining substantial traction. This trend is fueled by growing environmental consciousness among consumers and supportive government regulations aimed at promoting sustainable mobility. Key segments contributing to this growth include Sports Utility Vehicles (SUVs) and Sedans, which continue to dominate consumer choices due to their versatility and appeal. The "Other Vehicle Types" category, encompassing high-performance sports cars, is also expected to see steady demand from enthusiasts and collectors, further bolstering market expansion.

Luxury Car Industry Market Size (In Million)

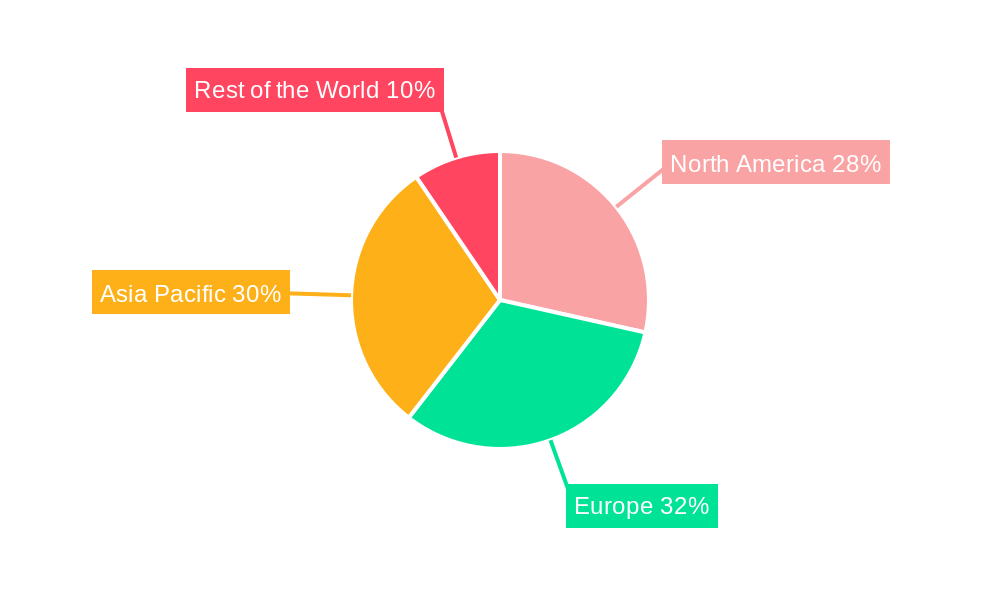

The competitive landscape of the luxury car market is characterized by intense innovation and strategic collaborations among leading global players. Companies such as BMW AG, Mercedes-Benz Group AG, and Tesla Inc. are at the forefront of introducing cutting-edge technologies, including autonomous driving features, sophisticated infotainment systems, and luxurious interior designs. The market is segmented by vehicle class, with the Mid-level Luxury Class experiencing strong demand, followed by the Entry-level Luxury Class and the Ultra Luxury Class. Geographically, Asia Pacific, particularly China, is emerging as a pivotal growth region, driven by its vast consumer base and rapid economic development. North America and Europe remain significant markets, with a strong consumer preference for advanced safety features and sustainable powertrains. Restraints to growth may include increasing production costs, evolving emission standards, and potential economic downturns. However, the industry's commitment to innovation and adapting to evolving consumer preferences suggests a resilient and upward trajectory for the luxury car market.

Luxury Car Industry Company Market Share

Luxury Car Industry: Market Dynamics, Growth Trends, and Future Outlook (2019-2033)

This comprehensive report delves into the dynamic luxury car industry, offering an in-depth analysis of market structures, growth trajectories, regional dominance, and key player strategies from 2019 to 2033. With the base year set at 2025, this report provides critical insights into the luxury automotive market, including electric luxury cars, premium sedans, luxury SUVs, and ultra-luxury vehicles. We examine the evolving landscape shaped by technological advancements, shifting consumer preferences, and robust industry developments. This report is essential for automotive manufacturers, suppliers, investors, and industry analysts seeking to understand the burgeoning opportunities and challenges within the global luxury car market.

Luxury Car Industry Market Dynamics & Structure

The luxury car industry is characterized by a concentrated market structure with a few dominant global players, though emerging brands are increasingly carving out niches. Technological innovation is a primary driver, with significant investments in electric vehicle (EV) powertrains, autonomous driving features, and advanced connectivity solutions shaping product development. Regulatory frameworks, particularly concerning emissions standards and safety mandates, exert considerable influence, pushing manufacturers towards sustainable and technologically advanced offerings. Competitive product substitutes, ranging from high-end mainstream vehicles to bespoke custom creations, necessitate continuous innovation to maintain market share. End-user demographics are evolving, with a growing segment of affluent millennials and Gen Z consumers seeking sustainability, personalization, and digital integration alongside traditional luxury attributes. Mergers and acquisition (M&A) trends are less about consolidation of major players and more about strategic partnerships and acquisitions of specialized technology firms to enhance capabilities in areas like battery technology, AI, and software development.

- Market Concentration: Dominated by key automotive groups, but with increasing fragmentation in specialized segments.

- Technological Innovation Drivers: Emphasis on electrification, autonomous driving, digital cockpits, and sustainable materials.

- Regulatory Frameworks: Stringent emissions standards (e.g., Euro 7) and safety regulations are shaping product roadmaps.

- Competitive Product Substitutes: Range from high-performance EVs to limited-edition hypercars.

- End-User Demographics: Growing demand from younger affluent consumers; increased focus on brand values and experiential ownership.

- M&A Trends: Strategic acquisitions of tech startups and joint ventures for technology development.

Luxury Car Industry Growth Trends & Insights

The luxury car industry is poised for robust growth, fueled by increasing global wealth, evolving consumer aspirations, and rapid technological advancements. Market size evolution indicates a consistent upward trajectory, with a projected Compound Annual Growth Rate (CAGR) of xx% over the forecast period (2025–2033). The adoption rates of electric luxury cars are accelerating, driven by environmental consciousness, government incentives, and improved battery technology offering longer ranges and faster charging. Technological disruptions, such as the integration of AI-powered in-car assistants and advanced driver-assistance systems (ADAS), are redefining the luxury driving experience. Consumer behavior shifts are evident, with a pronounced preference for personalized configurations, digital ownership experiences, and a growing interest in subscription-based models and mobility services. The luxury automotive market is no longer solely defined by performance and prestige but also by sustainability, connectivity, and a seamless digital-to-physical integration. The premium sedans and luxury SUVs segments continue to lead in sales volume, while the ultra-luxury vehicles segment demonstrates resilience and strong demand for exclusivity.

Dominant Regions, Countries, or Segments in Luxury Car Industry

The luxury car industry exhibits strong regional and segment-specific dominance. North America, particularly the United States, remains a pivotal market, driven by a high concentration of affluent consumers and a robust demand for Sports Utility Vehicles (SUVs) and performance luxury cars. Europe, with its stringent environmental regulations and sophisticated consumer base, is at the forefront of electric and hybrid luxury vehicle adoption. Asia-Pacific, led by China, is emerging as a significant growth engine, with a rapidly expanding affluent population and a strong appetite for premium sedans and innovative EV technology.

- Dominant Vehicle Type: Sports Utility Vehicles (SUVs) continue to lead market share, appealing to families and individuals seeking versatility, performance, and advanced technology. However, Sedans remain a strong contender, especially in the ultra-luxury segment, offering unparalleled comfort and executive appeal.

- Dominant Drive Type: The shift towards Electric and Hybrid powertrains is a dominant trend, driven by regulatory pressures and growing consumer demand for sustainable mobility. Internal Combustion Engine (ICE) vehicles still hold significant market share, particularly in emerging economies and for specific performance applications.

- Dominant Vehicle Class: The Mid-level Luxury Class commands the largest market share, offering a balance of premium features, performance, and relative affordability for a broader segment of affluent buyers. The Entry-level Luxury Class is crucial for brand acquisition, while the Ultra Luxury Class represents a niche but highly profitable segment, driven by exclusivity and bespoke customization.

Key drivers for regional dominance include economic policies supporting luxury goods and automotive manufacturing, substantial investments in charging infrastructure for EVs, and the presence of established luxury automotive brands with strong brand loyalty. The market share in these dominant segments is projected to grow at xx% CAGR (2025-2033).

Luxury Car Industry Product Landscape

The luxury car industry product landscape is defined by an unwavering commitment to innovation, superior performance, and exquisite craftsmanship. Product innovations are increasingly focused on electrification, with manufacturers like Tesla Inc. and Mercedes-Benz Group AG pushing boundaries in battery technology, charging speeds, and electric powertrain efficiency. The integration of advanced infotainment systems, augmented reality displays, and intuitive user interfaces is transforming the in-car experience. Performance metrics are being redefined not only by raw power but also by the seamless integration of driving dynamics, comfort, and advanced driver-assistance systems. Unique selling propositions often revolve around bespoke customization options, sustainable material sourcing, and cutting-edge connectivity features that offer a truly personalized and exclusive ownership experience. The launch of ultra-luxury electric sedans, such as those seen from NIO, signifies a new era of sustainable opulence.

Key Drivers, Barriers & Challenges in Luxury Car Industry

The luxury car industry is propelled by several key drivers, including escalating global wealth and a growing affluent population, technological advancements in electrification and autonomous driving, and the increasing demand for personalized and exclusive mobility solutions. Brand prestige and heritage also continue to play a crucial role in attracting and retaining discerning customers.

- Key Drivers:

- Growing disposable incomes of high-net-worth individuals.

- Rapid advancements in EV technology and infrastructure.

- Consumer desire for exclusivity, customization, and status symbols.

- Brand loyalty and established reputation of premium marques.

- Government incentives for EV adoption and emission reduction.

However, the industry faces significant barriers and challenges. Supply chain disruptions, particularly for critical components like semiconductors and batteries, can impact production volumes and timelines. Stringent regulatory hurdles, especially concerning emissions and safety standards across different global markets, require substantial investment in research and development. Intense competitive pressures from both established players and new entrants, including technology companies, further challenge market dynamics.

- Key Barriers & Challenges:

- Global semiconductor shortages and battery raw material sourcing.

- Navigating complex and evolving international emissions and safety regulations.

- High cost of R&D for new technologies and platforms.

- Intensifying competition from traditional and new automotive players.

- Economic downturns impacting discretionary spending on luxury goods.

Emerging Opportunities in Luxury Car Industry

Emerging opportunities in the luxury car industry are abundant, stemming from evolving consumer preferences and technological breakthroughs. The burgeoning demand for sustainable luxury transportation presents a significant avenue for growth, with a focus on advanced electric vehicle (EV) platforms and eco-friendly materials. Untapped markets in developing economies with a rapidly growing affluent class offer substantial expansion potential. Innovative applications of AI and connectivity are creating opportunities for personalized in-car experiences, predictive maintenance, and seamless integration with smart home ecosystems. The rise of the experience economy also presents opportunities for luxury automotive brands to offer exclusive lifestyle packages, curated events, and bespoke ownership journeys beyond the vehicle itself. Subscription models and flexible ownership programs are also gaining traction, catering to a younger demographic seeking adaptability.

Growth Accelerators in the Luxury Car Industry Industry

The luxury car industry is experiencing significant growth acceleration driven by strategic initiatives and technological breakthroughs. The rapid expansion of the electric luxury car segment, propelled by substantial investments from key players like Hyundai Motor Group and Volkswagen Group, is a major catalyst. Enhanced battery technology, leading to longer ranges and faster charging times, is making EVs more practical and desirable for luxury consumers. Furthermore, the increasing focus on autonomous driving features and advanced connectivity solutions enhances the appeal and functionality of luxury vehicles. Strategic partnerships and collaborations, particularly in R&D and supply chain management, are crucial for navigating complex technological landscapes and optimizing production. Market expansion into emerging economies, coupled with the introduction of tailored product offerings, is also a key growth accelerator.

Key Players Shaping the Luxury Car Industry Market

- Hyundai Motor Group

- Volkswagen Group

- Jaguar Land Rover Automotive PLC

- Volvo Group

- FAW Car Company

- Fiat Chrysler Automobiles

- BMW AG

- Tesla Inc.

- Mercedes-Benz Group AG

- Ford Motor Company

Notable Milestones in Luxury Car Industry Sector

- November 2023: Nio revealed the launch of a major product on Nio Day in December. It was a CNY 1 million (USD 140 thousand) luxurious electric sedan to compete with the Maybach S class in China.

- September 2023: Toyota Motor Corporation unveiled a new luxury Century model. The new model was to be launched by the end of 2023. The new model of the Century would be fully customizable on a global basis.

- January 2023: BMW launched its much-awaited i7 sedan in India. Based on the flagship 7-Series, the i7 would go up against Mercedes Benz’s EQS, which was introduced in 2022. While Mercedes Benz has localized the assembly of its EQS sedan, BMW will introduce the i7 as a fully built-up unit (FBU).

In-Depth Luxury Car Industry Market Outlook

The luxury car industry is set for a dynamic and expansive future, driven by a confluence of technological innovation, evolving consumer desires, and strategic market expansion. Growth accelerators like the relentless pursuit of electrification and the integration of sophisticated autonomous driving systems will continue to redefine premium mobility. Future market potential is immense, particularly in emerging economies where a burgeoning affluent class is seeking sophisticated and sustainable transportation. Strategic opportunities lie in capitalizing on the demand for personalized digital experiences, expanding into niche segments with bespoke offerings, and forging collaborations that enhance technological capabilities and supply chain resilience. The industry's ability to adapt to changing regulatory landscapes and consumer preferences for sustainability will be paramount to its sustained success.

Luxury Car Industry Segmentation

-

1. Vehicle Type

- 1.1. Hatchbacks

- 1.2. Sedans

- 1.3. Sports Utility Vehicles (SUVs)

- 1.4. Multi-purpose Vehicles (MPVs)

- 1.5. Other Vehicle Types (Sports, Etc.)

-

2. Drive Type

- 2.1. Internal Combustion Engine (ICE)

- 2.2. Electric and Hybrid

-

3. Vehicle Class

- 3.1. Entry-level Luxury Class

- 3.2. Mid-level Luxury Class

- 3.3. Ultra Luxury Class

Luxury Car Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Rest of North America

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. South Korea

- 3.5. Rest of Asia Pacific

-

4. Rest of the World

- 4.1. South America

- 4.2. Middle East and Africa

Luxury Car Industry Regional Market Share

Geographic Coverage of Luxury Car Industry

Luxury Car Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.55% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.1.1. Hatchbacks

- 5.1.2. Sedans

- 5.1.3. Sports Utility Vehicles (SUVs)

- 5.1.4. Multi-purpose Vehicles (MPVs)

- 5.1.5. Other Vehicle Types (Sports, Etc.)

- 5.2. Market Analysis, Insights and Forecast - by Drive Type

- 5.2.1. Internal Combustion Engine (ICE)

- 5.2.2. Electric and Hybrid

- 5.3. Market Analysis, Insights and Forecast - by Vehicle Class

- 5.3.1. Entry-level Luxury Class

- 5.3.2. Mid-level Luxury Class

- 5.3.3. Ultra Luxury Class

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6. Global Luxury Car Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.1.1. Hatchbacks

- 6.1.2. Sedans

- 6.1.3. Sports Utility Vehicles (SUVs)

- 6.1.4. Multi-purpose Vehicles (MPVs)

- 6.1.5. Other Vehicle Types (Sports, Etc.)

- 6.2. Market Analysis, Insights and Forecast - by Drive Type

- 6.2.1. Internal Combustion Engine (ICE)

- 6.2.2. Electric and Hybrid

- 6.3. Market Analysis, Insights and Forecast - by Vehicle Class

- 6.3.1. Entry-level Luxury Class

- 6.3.2. Mid-level Luxury Class

- 6.3.3. Ultra Luxury Class

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 7. North America Luxury Car Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 7.1.1. Hatchbacks

- 7.1.2. Sedans

- 7.1.3. Sports Utility Vehicles (SUVs)

- 7.1.4. Multi-purpose Vehicles (MPVs)

- 7.1.5. Other Vehicle Types (Sports, Etc.)

- 7.2. Market Analysis, Insights and Forecast - by Drive Type

- 7.2.1. Internal Combustion Engine (ICE)

- 7.2.2. Electric and Hybrid

- 7.3. Market Analysis, Insights and Forecast - by Vehicle Class

- 7.3.1. Entry-level Luxury Class

- 7.3.2. Mid-level Luxury Class

- 7.3.3. Ultra Luxury Class

- 7.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 8. Europe Luxury Car Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 8.1.1. Hatchbacks

- 8.1.2. Sedans

- 8.1.3. Sports Utility Vehicles (SUVs)

- 8.1.4. Multi-purpose Vehicles (MPVs)

- 8.1.5. Other Vehicle Types (Sports, Etc.)

- 8.2. Market Analysis, Insights and Forecast - by Drive Type

- 8.2.1. Internal Combustion Engine (ICE)

- 8.2.2. Electric and Hybrid

- 8.3. Market Analysis, Insights and Forecast - by Vehicle Class

- 8.3.1. Entry-level Luxury Class

- 8.3.2. Mid-level Luxury Class

- 8.3.3. Ultra Luxury Class

- 8.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 9. Asia Pacific Luxury Car Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 9.1.1. Hatchbacks

- 9.1.2. Sedans

- 9.1.3. Sports Utility Vehicles (SUVs)

- 9.1.4. Multi-purpose Vehicles (MPVs)

- 9.1.5. Other Vehicle Types (Sports, Etc.)

- 9.2. Market Analysis, Insights and Forecast - by Drive Type

- 9.2.1. Internal Combustion Engine (ICE)

- 9.2.2. Electric and Hybrid

- 9.3. Market Analysis, Insights and Forecast - by Vehicle Class

- 9.3.1. Entry-level Luxury Class

- 9.3.2. Mid-level Luxury Class

- 9.3.3. Ultra Luxury Class

- 9.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 10. Rest of the World Luxury Car Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 10.1.1. Hatchbacks

- 10.1.2. Sedans

- 10.1.3. Sports Utility Vehicles (SUVs)

- 10.1.4. Multi-purpose Vehicles (MPVs)

- 10.1.5. Other Vehicle Types (Sports, Etc.)

- 10.2. Market Analysis, Insights and Forecast - by Drive Type

- 10.2.1. Internal Combustion Engine (ICE)

- 10.2.2. Electric and Hybrid

- 10.3. Market Analysis, Insights and Forecast - by Vehicle Class

- 10.3.1. Entry-level Luxury Class

- 10.3.2. Mid-level Luxury Class

- 10.3.3. Ultra Luxury Class

- 10.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Hyundai Motor Group

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Volkswagen Group

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Jaguar Land Rover Automotive PLC

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Volvo Group

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 FAW Car Company

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Fiat Chrysler Automobiles

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 BMW AG

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Tesla Inc

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Mercedes-Benz Group AG

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Ford Motor Company

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.1 Hyundai Motor Group

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Luxury Car Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Luxury Car Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 3: North America Luxury Car Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 4: North America Luxury Car Industry Revenue (Million), by Drive Type 2025 & 2033

- Figure 5: North America Luxury Car Industry Revenue Share (%), by Drive Type 2025 & 2033

- Figure 6: North America Luxury Car Industry Revenue (Million), by Vehicle Class 2025 & 2033

- Figure 7: North America Luxury Car Industry Revenue Share (%), by Vehicle Class 2025 & 2033

- Figure 8: North America Luxury Car Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: North America Luxury Car Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Luxury Car Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 11: Europe Luxury Car Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 12: Europe Luxury Car Industry Revenue (Million), by Drive Type 2025 & 2033

- Figure 13: Europe Luxury Car Industry Revenue Share (%), by Drive Type 2025 & 2033

- Figure 14: Europe Luxury Car Industry Revenue (Million), by Vehicle Class 2025 & 2033

- Figure 15: Europe Luxury Car Industry Revenue Share (%), by Vehicle Class 2025 & 2033

- Figure 16: Europe Luxury Car Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Europe Luxury Car Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Luxury Car Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 19: Asia Pacific Luxury Car Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 20: Asia Pacific Luxury Car Industry Revenue (Million), by Drive Type 2025 & 2033

- Figure 21: Asia Pacific Luxury Car Industry Revenue Share (%), by Drive Type 2025 & 2033

- Figure 22: Asia Pacific Luxury Car Industry Revenue (Million), by Vehicle Class 2025 & 2033

- Figure 23: Asia Pacific Luxury Car Industry Revenue Share (%), by Vehicle Class 2025 & 2033

- Figure 24: Asia Pacific Luxury Car Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Asia Pacific Luxury Car Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Rest of the World Luxury Car Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 27: Rest of the World Luxury Car Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 28: Rest of the World Luxury Car Industry Revenue (Million), by Drive Type 2025 & 2033

- Figure 29: Rest of the World Luxury Car Industry Revenue Share (%), by Drive Type 2025 & 2033

- Figure 30: Rest of the World Luxury Car Industry Revenue (Million), by Vehicle Class 2025 & 2033

- Figure 31: Rest of the World Luxury Car Industry Revenue Share (%), by Vehicle Class 2025 & 2033

- Figure 32: Rest of the World Luxury Car Industry Revenue (Million), by Country 2025 & 2033

- Figure 33: Rest of the World Luxury Car Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Luxury Car Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 2: Global Luxury Car Industry Revenue Million Forecast, by Drive Type 2020 & 2033

- Table 3: Global Luxury Car Industry Revenue Million Forecast, by Vehicle Class 2020 & 2033

- Table 4: Global Luxury Car Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Global Luxury Car Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 6: Global Luxury Car Industry Revenue Million Forecast, by Drive Type 2020 & 2033

- Table 7: Global Luxury Car Industry Revenue Million Forecast, by Vehicle Class 2020 & 2033

- Table 8: Global Luxury Car Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: United States Luxury Car Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Canada Luxury Car Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Rest of North America Luxury Car Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Global Luxury Car Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 13: Global Luxury Car Industry Revenue Million Forecast, by Drive Type 2020 & 2033

- Table 14: Global Luxury Car Industry Revenue Million Forecast, by Vehicle Class 2020 & 2033

- Table 15: Global Luxury Car Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Germany Luxury Car Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: United Kingdom Luxury Car Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: France Luxury Car Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Italy Luxury Car Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Spain Luxury Car Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Rest of Europe Luxury Car Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Global Luxury Car Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 23: Global Luxury Car Industry Revenue Million Forecast, by Drive Type 2020 & 2033

- Table 24: Global Luxury Car Industry Revenue Million Forecast, by Vehicle Class 2020 & 2033

- Table 25: Global Luxury Car Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 26: China Luxury Car Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Japan Luxury Car Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: India Luxury Car Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: South Korea Luxury Car Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Rest of Asia Pacific Luxury Car Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 31: Global Luxury Car Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 32: Global Luxury Car Industry Revenue Million Forecast, by Drive Type 2020 & 2033

- Table 33: Global Luxury Car Industry Revenue Million Forecast, by Vehicle Class 2020 & 2033

- Table 34: Global Luxury Car Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 35: South America Luxury Car Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Middle East and Africa Luxury Car Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Luxury Car Industry?

The projected CAGR is approximately 5.55%.

2. Which companies are prominent players in the Luxury Car Industry?

Key companies in the market include Hyundai Motor Group, Volkswagen Group, Jaguar Land Rover Automotive PLC, Volvo Group, FAW Car Company, Fiat Chrysler Automobiles, BMW AG, Tesla Inc, Mercedes-Benz Group AG, Ford Motor Company.

3. What are the main segments of the Luxury Car Industry?

The market segments include Vehicle Type, Drive Type, Vehicle Class.

4. Can you provide details about the market size?

The market size is estimated to be USD 738.63 Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Demand for Comfortable Driving Experience and Vehicle Safety is Driving the Market; Increasing Number of High Net Worth Individuals (HNWI) and Ultra HNWIs Drives Demand.

6. What are the notable trends driving market growth?

SUVs will be the Leading Segment in the Luxury Car Market.

7. Are there any restraints impacting market growth?

High Initial Cost of Ownership is a Challenge.

8. Can you provide examples of recent developments in the market?

November 2023: Nio revealed the launch of a major product on Nio Day in December. It was a CNY 1 million (USD 140 thousand) luxurious electric sedan to compete with the Maybach S class in China.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Luxury Car Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Luxury Car Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Luxury Car Industry?

To stay informed about further developments, trends, and reports in the Luxury Car Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence