Key Insights

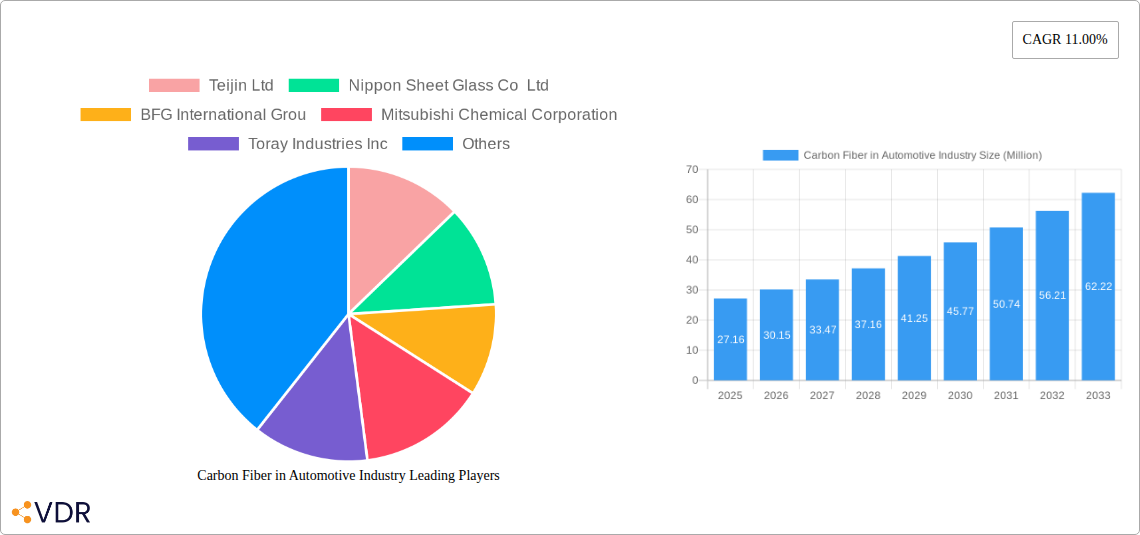

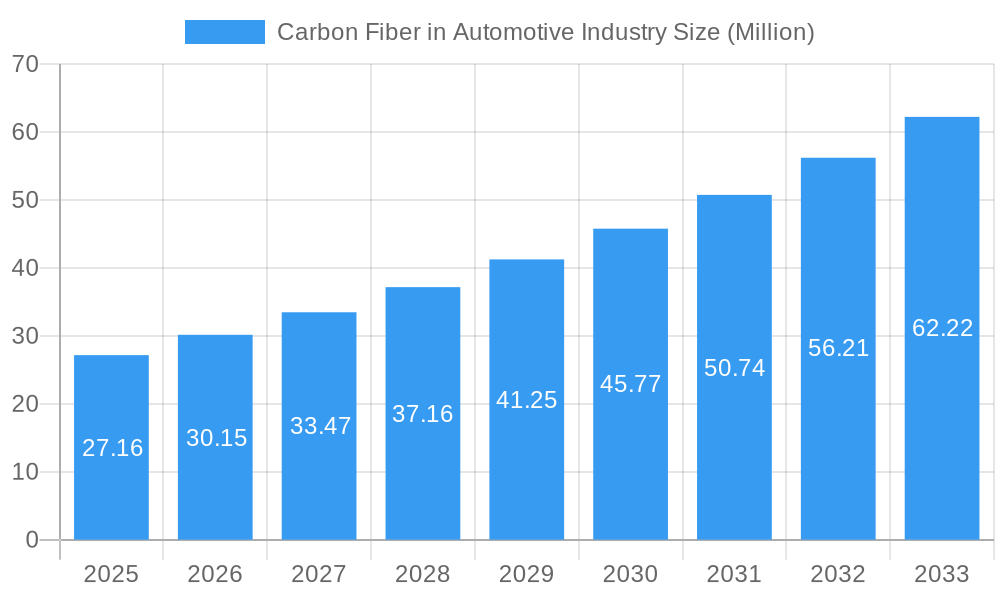

The global market for carbon fiber in the automotive industry is poised for substantial growth, projected to reach approximately USD 27.16 million by 2025, driven by an impressive Compound Annual Growth Rate (CAGR) of 11.00% during the forecast period of 2025-2033. This robust expansion is primarily fueled by the increasing demand for lightweight materials that enhance fuel efficiency and reduce emissions in passenger cars and commercial vehicles. The automotive sector's relentless pursuit of sustainability and performance improvements is a key determinant, pushing manufacturers to adopt advanced composite materials like carbon fiber. Furthermore, the evolving regulatory landscape, emphasizing stricter environmental standards and promoting the adoption of electric and hybrid powertrains, acts as a significant catalyst for this market's ascent. The rising integration of battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs) necessitates lighter chassis and body components to offset the weight of batteries, making carbon fiber an indispensable material. Innovations in manufacturing processes and a growing awareness of carbon fiber's superior strength-to-weight ratio are also contributing to its widespread adoption across various automotive applications, including structural assembly, powertrain components, interiors, and exteriors.

Carbon Fiber in Automotive Industry Market Size (In Million)

The market's trajectory is further shaped by key trends such as the development of cost-effective carbon fiber production techniques and the increasing use of advanced manufacturing methods like automated tape laying and resin transfer molding, which accelerate production cycles and reduce manufacturing costs. The growing emphasis on vehicle safety and crashworthiness also plays a crucial role, as carbon fiber composites offer exceptional impact resistance. While the market benefits from strong demand, it faces certain restraints, including the relatively high cost of raw materials and the complexity of recycling carbon fiber components. However, ongoing research and development efforts focused on improving recyclability and developing bio-based carbon fibers are expected to mitigate these challenges in the long run. Geographically, Asia Pacific, led by China, is anticipated to emerge as a dominant region due to its large automotive production base and increasing investments in electric vehicle technology. North America and Europe are also significant markets, driven by stringent emission norms and a strong presence of premium vehicle manufacturers already incorporating carbon fiber.

Carbon Fiber in Automotive Industry Company Market Share

Comprehensive Report: Carbon Fiber in the Automotive Industry Market Insights 2019-2033

Unlock critical insights into the rapidly evolving carbon fiber market for the automotive sector. This in-depth report, covering 2019-2033 with a base year of 2025, analyzes market dynamics, growth trends, dominant segments, product innovations, key drivers, challenges, and emerging opportunities. Discover how companies like Teijin Ltd, Nippon Sheet Glass Co Ltd, and Toray Industries Inc. are shaping the future of lightweight, high-performance vehicles. Explore parent and child market segments including Structural Assembly, Powertrain Components, Interiors, Exteriors, Passenger Cars, Commercial Vehicles, Internal Combustion Engine, Battery Electric Vehicles, Hybrid Electric Vehicles, Plug-in Hybrid Electric Vehicles, and Fuel Cell Electric Vehicles.

Carbon Fiber in Automotive Industry Market Dynamics & Structure

The automotive carbon fiber market is characterized by a moderate to high concentration, with key players like Toray Industries Inc., Hexcel Corporation, and SGL Carbon SE holding significant market shares. Technological innovation is a primary driver, fueled by the relentless pursuit of lighter, stronger, and more fuel-efficient vehicles, particularly in the electric vehicle (EV) segment. Regulatory frameworks, mandating stricter emissions standards and promoting lightweighting, further bolster demand. Competitive product substitutes, such as advanced high-strength steels and aluminum alloys, present a challenge, but carbon fiber's superior strength-to-weight ratio often outweighs cost considerations for premium applications. End-user demographics are shifting towards environmentally conscious consumers and fleet operators seeking performance and sustainability. Mergers and acquisitions (M&A) activity is moderate, with companies consolidating to enhance R&D capabilities and expand production capacity. For instance, acquisitions aimed at securing raw material supply chains and integrating advanced manufacturing techniques are on the rise. Innovation barriers include the high cost of raw materials and complex manufacturing processes, though ongoing research into low-cost carbon fiber production and automated manufacturing is addressing these challenges.

- Market Concentration: Dominated by a few key global players, but with increasing participation from niche material suppliers.

- Technological Innovation Drivers: Lightweighting for fuel efficiency, crash safety improvements, EV range extension, and design freedom.

- Regulatory Frameworks: Emission standards (e.g., Euro 7), fuel economy mandates, and government incentives for EVs.

- Competitive Product Substitutes: Advanced High-Strength Steel (AHSS), Aluminum Alloys, Magnesium Alloys.

- End-User Demographics: Premium vehicle buyers, EV adopters, performance-oriented consumers, commercial fleet operators.

- M&A Trends: Strategic acquisitions for vertical integration, technology acquisition, and market expansion.

Carbon Fiber in Automotive Industry Growth Trends & Insights

The carbon fiber in the automotive industry is poised for significant expansion, driven by an escalating demand for lightweight materials that enhance fuel efficiency and extend the range of electric vehicles. Market size is projected to grow from approximately $18,500 Million units in 2025 to an estimated $35,200 Million units by 2033, exhibiting a compound annual growth rate (CAGR) of approximately 8.5%. Adoption rates are accelerating, especially in the passenger car segment, with a growing percentage of new vehicle models incorporating carbon fiber for structural components and body panels. Technological disruptions, such as advancements in automated fiber placement and resin transfer molding, are improving manufacturing efficiency and reducing costs, making carbon fiber more accessible. Consumer behavior shifts towards sustainability and performance are also playing a crucial role, with consumers increasingly valuing the environmental benefits of lightweight vehicles and the enhanced driving dynamics that carbon fiber enables. The integration of carbon fiber in structural assembly, such as chassis and body-in-white components, is a key trend, contributing significantly to overall vehicle weight reduction. The increasing proliferation of Battery Electric Vehicles (BEVs) is a major growth accelerator, as manufacturers strive to offset the weight of batteries by using lighter materials in other parts of the vehicle. Furthermore, the development of novel carbon fiber composite materials with enhanced recyclability and lower environmental impact is gaining traction, aligning with the industry's sustainability goals. The penetration of carbon fiber in powertrain components, while currently lower than in structural applications, is expected to see robust growth as manufacturers explore its use in high-stress components.

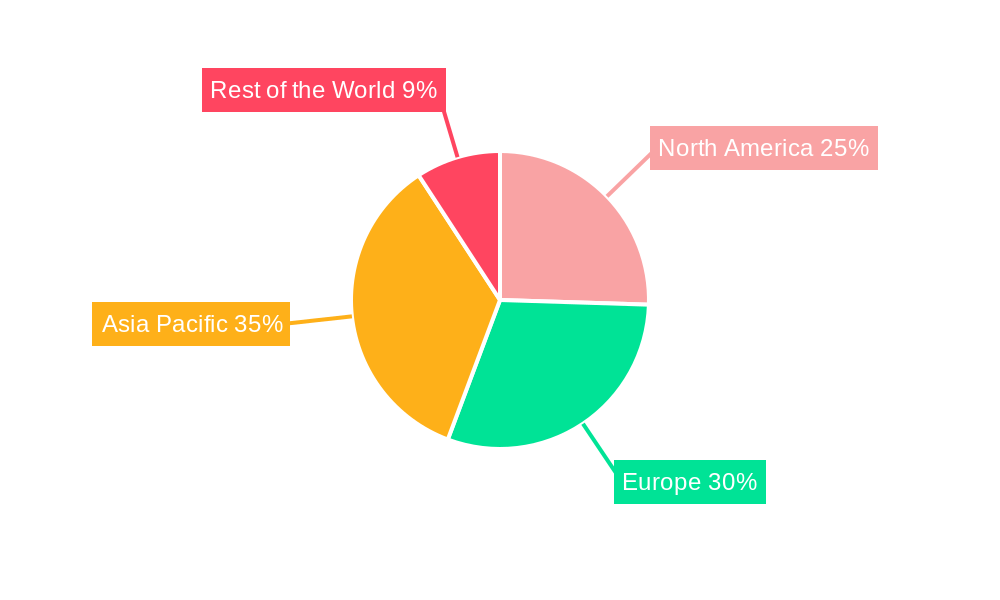

Dominant Regions, Countries, or Segments in Carbon Fiber in Automotive Industry

The Passenger Car segment is currently the dominant force driving growth in the automotive carbon fiber market. This dominance is attributed to several factors, including the high-volume production of passenger vehicles globally, the increasing demand for premium and performance-oriented models, and the aggressive push towards lightweighting for improved fuel economy and electric vehicle range extension. The stringent emission regulations in major automotive markets like Europe and North America necessitate the adoption of advanced lightweight materials, making carbon fiber an attractive solution.

- Application Dominance: Structural Assembly is the leading application, accounting for a substantial market share. This includes critical components like chassis, body panels, and structural reinforcements, where carbon fiber's high strength-to-weight ratio directly contributes to vehicle safety and performance.

- Vehicle Type Dominance: Passenger Cars are the primary volume drivers. Their widespread adoption and the consumer demand for performance and efficiency in this segment make them a natural fit for carbon fiber applications.

- Propulsion Dominance: While Internal Combustion Engine (ICE) vehicles still represent a significant portion of the market, the growth trajectory is increasingly being influenced by Battery Electric Vehicles (BEVs). The need to counteract battery weight and maximize range is a powerful incentive for BEV manufacturers to adopt carbon fiber. Hybrid Electric Vehicles (HEVs) and Plug-in Hybrid Electric Vehicles (PHEVs) also contribute to this trend.

- Regional Influence: Asia Pacific, particularly China, Japan, and South Korea, is emerging as a dominant region due to its massive automotive manufacturing base, increasing adoption of EVs, and supportive government policies promoting advanced materials and green transportation. North America and Europe also hold significant sway due to established premium automotive markets and stringent environmental regulations.

Carbon Fiber in Automotive Industry Product Landscape

The carbon fiber product landscape in the automotive industry is characterized by continuous innovation aimed at enhancing performance, reducing costs, and improving sustainability. Advancements in carbon fiber tow sizes, resin systems, and manufacturing processes are leading to the development of tailored materials for specific automotive applications. For example, high-strength carbon fibers like Toray's TORAYCA T1200 offer exceptional mechanical properties, enabling the creation of lighter and more robust components. Innovations also focus on developing carbon fiber composites with improved impact resistance and fire retardancy, crucial for automotive safety standards. The emergence of bio-based carbon fibers, such as Teijin's environmentally friendly Tenax carbon fiber, represents a significant step towards a more sustainable automotive supply chain.

Key Drivers, Barriers & Challenges in Carbon Fiber in Automotive Industry

Key Drivers:

- Lightweighting for Fuel Efficiency and EV Range: The primary catalyst is the need to reduce vehicle weight to improve fuel economy in ICE vehicles and extend the range of Battery Electric Vehicles (BEVs).

- Stricter Emission Regulations: Government mandates globally are pushing manufacturers to adopt lighter materials to meet stringent CO2 emission targets.

- Performance and Safety Enhancements: Carbon fiber’s high strength-to-weight ratio offers superior crashworthiness and improved vehicle dynamics, appealing to performance-oriented segments.

- Advancements in Manufacturing Technologies: Innovations in automated manufacturing processes are making carbon fiber components more cost-effective and scalable.

Barriers & Challenges:

- High Material Cost: The production of carbon fiber remains more expensive than traditional materials like steel and aluminum, limiting its widespread adoption in mass-market vehicles.

- Complex Manufacturing Processes: The fabrication of carbon fiber composite parts can be labor-intensive and require specialized equipment, contributing to higher production costs and longer lead times.

- Recyclability and End-of-Life Management: Developing efficient and cost-effective methods for recycling carbon fiber composites is an ongoing challenge, impacting the material's overall sustainability profile.

- Supply Chain Volatility: The global supply chain for carbon fiber can be subject to disruptions, impacting availability and pricing.

Emerging Opportunities in Carbon Fiber in Automotive Industry

Emerging opportunities lie in the development of low-cost, high-volume production methods for carbon fiber, making it accessible to a wider range of vehicle segments. The increasing demand for advanced driver-assistance systems (ADAS) and autonomous driving technologies creates a need for lightweight sensor housings and integrated structural components, where carbon fiber can offer significant advantages. Furthermore, the exploration of novel composite structures, such as woven or braided carbon fiber preforms, alongside advancements in additive manufacturing (3D printing) of carbon fiber reinforced polymers, presents exciting avenues for complex part integration and design optimization. The growing emphasis on a circular economy also presents opportunities for innovation in carbon fiber recycling and the development of bio-based precursors for carbon fiber production.

Growth Accelerators in the Carbon Fiber in the Automotive Industry Industry

The long-term growth of the carbon fiber in the automotive industry is significantly accelerated by breakthroughs in materials science, leading to the development of carbon fibers with enhanced properties at reduced costs. Strategic partnerships between carbon fiber manufacturers and automotive OEMs are crucial for co-developing tailored solutions and streamlining integration into vehicle platforms. Market expansion strategies, including the penetration of carbon fiber into less traditional vehicle segments and applications, alongside the increasing electrification of transportation, are key accelerators. The development of advanced recycling technologies and the establishment of robust carbon fiber circular economy models will also further bolster its adoption by addressing sustainability concerns and improving cost-effectiveness over the vehicle's lifecycle.

Key Players Shaping the Carbon Fiber in Automotive Industry Market

- Teijin Ltd

- Nippon Sheet Glass Co Ltd

- BFG International Grou

- Mitsubishi Chemical Corporation

- Toray Industries Inc

- Dow Inc

- BASF SE

- Solvay SA

- Bcomp Ltd

- Hexcel Corporation

- SGL Carbon SE

Notable Milestones in Carbon Fiber in Automotive Industry Sector

- December 2023: Teijin Limited announced plans to start producing and selling Tenax carbon fiber made from environmentally friendly materials. This material helps in the reduction of greenhouse gas emissions throughout the product's life cycle.

- December 2023: Foton Motor introduced a super low-carbon truck, the Toano V next-generation light bus, and a full range of hybrid vehicles.

- October 2023: Toray Industries Inc. developed TORAYCA T1200 carbon fiber, which boasts the highest strength of 1,160 kilopounds per square inch (Ksi). This advancement will aid the company in reducing its environmental footprint by using lighter carbon-fiber-reinforced plastic materials.

In-Depth Carbon Fiber in Automotive Industry Market Outlook

The future outlook for carbon fiber in the automotive industry is exceptionally bright, driven by the accelerating global transition towards sustainable mobility and the continuous demand for enhanced vehicle performance. The synergy between lightweighting mandates, stringent environmental regulations, and the rapid expansion of the electric vehicle market will continue to be the primary growth engine. Strategic investments in advanced manufacturing technologies and R&D for cost reduction and improved recyclability will further democratize its application. Emerging opportunities in smart mobility, autonomous systems, and the development of integrated structural components will unlock new avenues for innovation and market penetration. The industry is set to witness a paradigm shift, with carbon fiber evolving from a premium material to a more ubiquitous component in a wide array of automotive applications, ultimately contributing to a more efficient, sustainable, and high-performing automotive future.

Carbon Fiber in Automotive Industry Segmentation

-

1. Application

- 1.1. Structural Assembly

- 1.2. Powertrain Components

- 1.3. Interiors

- 1.4. Exteriors

-

2. Vehicle Type

- 2.1. Passenger Car

- 2.2. Commercial Vehicle

-

3. Propulsion

- 3.1. Internal Combustion Engine

- 3.2. Battery Electric Vehicles

- 3.3. Hybrid Electric Vehicles

- 3.4. Plug-in Hybrid Electric Vehicles

- 3.5. Fuel Cell Electric Vehicles

Carbon Fiber in Automotive Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Rest of North America

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. South Korea

- 3.5. Rest of Asia Pacific

-

4. Rest of the World

- 4.1. South America

- 4.2. Middle East and Africa

Carbon Fiber in Automotive Industry Regional Market Share

Geographic Coverage of Carbon Fiber in Automotive Industry

Carbon Fiber in Automotive Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.00% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Structural Assembly

- 5.1.2. Powertrain Components

- 5.1.3. Interiors

- 5.1.4. Exteriors

- 5.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.2.1. Passenger Car

- 5.2.2. Commercial Vehicle

- 5.3. Market Analysis, Insights and Forecast - by Propulsion

- 5.3.1. Internal Combustion Engine

- 5.3.2. Battery Electric Vehicles

- 5.3.3. Hybrid Electric Vehicles

- 5.3.4. Plug-in Hybrid Electric Vehicles

- 5.3.5. Fuel Cell Electric Vehicles

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Carbon Fiber in Automotive Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Structural Assembly

- 6.1.2. Powertrain Components

- 6.1.3. Interiors

- 6.1.4. Exteriors

- 6.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.2.1. Passenger Car

- 6.2.2. Commercial Vehicle

- 6.3. Market Analysis, Insights and Forecast - by Propulsion

- 6.3.1. Internal Combustion Engine

- 6.3.2. Battery Electric Vehicles

- 6.3.3. Hybrid Electric Vehicles

- 6.3.4. Plug-in Hybrid Electric Vehicles

- 6.3.5. Fuel Cell Electric Vehicles

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Carbon Fiber in Automotive Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Structural Assembly

- 7.1.2. Powertrain Components

- 7.1.3. Interiors

- 7.1.4. Exteriors

- 7.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 7.2.1. Passenger Car

- 7.2.2. Commercial Vehicle

- 7.3. Market Analysis, Insights and Forecast - by Propulsion

- 7.3.1. Internal Combustion Engine

- 7.3.2. Battery Electric Vehicles

- 7.3.3. Hybrid Electric Vehicles

- 7.3.4. Plug-in Hybrid Electric Vehicles

- 7.3.5. Fuel Cell Electric Vehicles

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Carbon Fiber in Automotive Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Structural Assembly

- 8.1.2. Powertrain Components

- 8.1.3. Interiors

- 8.1.4. Exteriors

- 8.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 8.2.1. Passenger Car

- 8.2.2. Commercial Vehicle

- 8.3. Market Analysis, Insights and Forecast - by Propulsion

- 8.3.1. Internal Combustion Engine

- 8.3.2. Battery Electric Vehicles

- 8.3.3. Hybrid Electric Vehicles

- 8.3.4. Plug-in Hybrid Electric Vehicles

- 8.3.5. Fuel Cell Electric Vehicles

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Asia Pacific Carbon Fiber in Automotive Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Structural Assembly

- 9.1.2. Powertrain Components

- 9.1.3. Interiors

- 9.1.4. Exteriors

- 9.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 9.2.1. Passenger Car

- 9.2.2. Commercial Vehicle

- 9.3. Market Analysis, Insights and Forecast - by Propulsion

- 9.3.1. Internal Combustion Engine

- 9.3.2. Battery Electric Vehicles

- 9.3.3. Hybrid Electric Vehicles

- 9.3.4. Plug-in Hybrid Electric Vehicles

- 9.3.5. Fuel Cell Electric Vehicles

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Rest of the World Carbon Fiber in Automotive Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Structural Assembly

- 10.1.2. Powertrain Components

- 10.1.3. Interiors

- 10.1.4. Exteriors

- 10.2. Market Analysis, Insights and Forecast - by Vehicle Type

- 10.2.1. Passenger Car

- 10.2.2. Commercial Vehicle

- 10.3. Market Analysis, Insights and Forecast - by Propulsion

- 10.3.1. Internal Combustion Engine

- 10.3.2. Battery Electric Vehicles

- 10.3.3. Hybrid Electric Vehicles

- 10.3.4. Plug-in Hybrid Electric Vehicles

- 10.3.5. Fuel Cell Electric Vehicles

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Teijin Ltd

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Nippon Sheet Glass Co Ltd

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 BFG International Grou

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Mitsubishi Chemical Corporation

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Toray Industries Inc

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Dow Inc

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 BASF SE

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Solvay SA

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Bcomp Ltd

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Hexcel Corporation

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.11 SGL Carbon SE

- 11.1.11.1. Company Overview

- 11.1.11.2. Products

- 11.1.11.3. Company Financials

- 11.1.11.4. SWOT Analysis

- 11.1.1 Teijin Ltd

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Carbon Fiber in Automotive Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Carbon Fiber in Automotive Industry Revenue (Million), by Application 2025 & 2033

- Figure 3: North America Carbon Fiber in Automotive Industry Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Carbon Fiber in Automotive Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 5: North America Carbon Fiber in Automotive Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 6: North America Carbon Fiber in Automotive Industry Revenue (Million), by Propulsion 2025 & 2033

- Figure 7: North America Carbon Fiber in Automotive Industry Revenue Share (%), by Propulsion 2025 & 2033

- Figure 8: North America Carbon Fiber in Automotive Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: North America Carbon Fiber in Automotive Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Carbon Fiber in Automotive Industry Revenue (Million), by Application 2025 & 2033

- Figure 11: Europe Carbon Fiber in Automotive Industry Revenue Share (%), by Application 2025 & 2033

- Figure 12: Europe Carbon Fiber in Automotive Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 13: Europe Carbon Fiber in Automotive Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 14: Europe Carbon Fiber in Automotive Industry Revenue (Million), by Propulsion 2025 & 2033

- Figure 15: Europe Carbon Fiber in Automotive Industry Revenue Share (%), by Propulsion 2025 & 2033

- Figure 16: Europe Carbon Fiber in Automotive Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Europe Carbon Fiber in Automotive Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Carbon Fiber in Automotive Industry Revenue (Million), by Application 2025 & 2033

- Figure 19: Asia Pacific Carbon Fiber in Automotive Industry Revenue Share (%), by Application 2025 & 2033

- Figure 20: Asia Pacific Carbon Fiber in Automotive Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 21: Asia Pacific Carbon Fiber in Automotive Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 22: Asia Pacific Carbon Fiber in Automotive Industry Revenue (Million), by Propulsion 2025 & 2033

- Figure 23: Asia Pacific Carbon Fiber in Automotive Industry Revenue Share (%), by Propulsion 2025 & 2033

- Figure 24: Asia Pacific Carbon Fiber in Automotive Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Asia Pacific Carbon Fiber in Automotive Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Rest of the World Carbon Fiber in Automotive Industry Revenue (Million), by Application 2025 & 2033

- Figure 27: Rest of the World Carbon Fiber in Automotive Industry Revenue Share (%), by Application 2025 & 2033

- Figure 28: Rest of the World Carbon Fiber in Automotive Industry Revenue (Million), by Vehicle Type 2025 & 2033

- Figure 29: Rest of the World Carbon Fiber in Automotive Industry Revenue Share (%), by Vehicle Type 2025 & 2033

- Figure 30: Rest of the World Carbon Fiber in Automotive Industry Revenue (Million), by Propulsion 2025 & 2033

- Figure 31: Rest of the World Carbon Fiber in Automotive Industry Revenue Share (%), by Propulsion 2025 & 2033

- Figure 32: Rest of the World Carbon Fiber in Automotive Industry Revenue (Million), by Country 2025 & 2033

- Figure 33: Rest of the World Carbon Fiber in Automotive Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Carbon Fiber in Automotive Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 2: Global Carbon Fiber in Automotive Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 3: Global Carbon Fiber in Automotive Industry Revenue Million Forecast, by Propulsion 2020 & 2033

- Table 4: Global Carbon Fiber in Automotive Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Global Carbon Fiber in Automotive Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 6: Global Carbon Fiber in Automotive Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 7: Global Carbon Fiber in Automotive Industry Revenue Million Forecast, by Propulsion 2020 & 2033

- Table 8: Global Carbon Fiber in Automotive Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: United States Carbon Fiber in Automotive Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Canada Carbon Fiber in Automotive Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Rest of North America Carbon Fiber in Automotive Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Global Carbon Fiber in Automotive Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 13: Global Carbon Fiber in Automotive Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 14: Global Carbon Fiber in Automotive Industry Revenue Million Forecast, by Propulsion 2020 & 2033

- Table 15: Global Carbon Fiber in Automotive Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Germany Carbon Fiber in Automotive Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: United Kingdom Carbon Fiber in Automotive Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: France Carbon Fiber in Automotive Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Italy Carbon Fiber in Automotive Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Rest of Europe Carbon Fiber in Automotive Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Global Carbon Fiber in Automotive Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 22: Global Carbon Fiber in Automotive Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 23: Global Carbon Fiber in Automotive Industry Revenue Million Forecast, by Propulsion 2020 & 2033

- Table 24: Global Carbon Fiber in Automotive Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 25: China Carbon Fiber in Automotive Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Japan Carbon Fiber in Automotive Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: India Carbon Fiber in Automotive Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: South Korea Carbon Fiber in Automotive Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: Rest of Asia Pacific Carbon Fiber in Automotive Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Global Carbon Fiber in Automotive Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 31: Global Carbon Fiber in Automotive Industry Revenue Million Forecast, by Vehicle Type 2020 & 2033

- Table 32: Global Carbon Fiber in Automotive Industry Revenue Million Forecast, by Propulsion 2020 & 2033

- Table 33: Global Carbon Fiber in Automotive Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 34: South America Carbon Fiber in Automotive Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 35: Middle East and Africa Carbon Fiber in Automotive Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Carbon Fiber in Automotive Industry?

The projected CAGR is approximately 11.00%.

2. Which companies are prominent players in the Carbon Fiber in Automotive Industry?

Key companies in the market include Teijin Ltd, Nippon Sheet Glass Co Ltd, BFG International Grou, Mitsubishi Chemical Corporation, Toray Industries Inc, Dow Inc, BASF SE, Solvay SA, Bcomp Ltd, Hexcel Corporation, SGL Carbon SE.

3. What are the main segments of the Carbon Fiber in Automotive Industry?

The market segments include Application, Vehicle Type, Propulsion.

4. Can you provide details about the market size?

The market size is estimated to be USD 27.16 Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Demand for Lightweight Materials from the Automotive industry.

6. What are the notable trends driving market growth?

Passenger Car Segment Holds a Major Market Share.

7. Are there any restraints impacting market growth?

High Processing and Manufacturing Cost of Composites.

8. Can you provide examples of recent developments in the market?

December 2023: Teijin Limited announced plans to start producing and selling Tenax carbon fiber made from environmentally friendly materials. This material helps in the reduction of greenhouse gas emissions throughout the product's life cycle.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Carbon Fiber in Automotive Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Carbon Fiber in Automotive Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Carbon Fiber in Automotive Industry?

To stay informed about further developments, trends, and reports in the Carbon Fiber in Automotive Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence