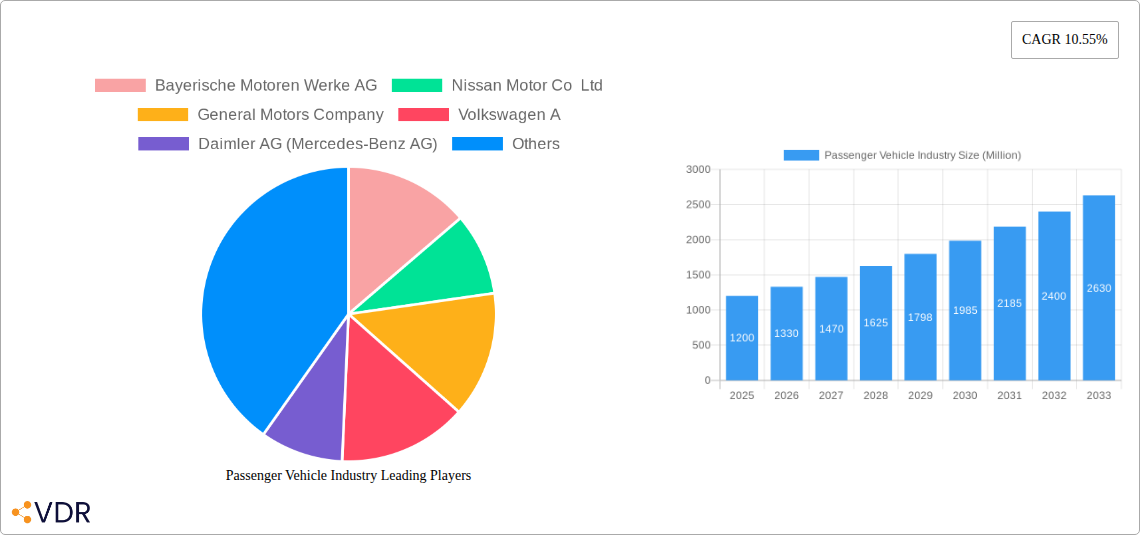

Key Insights

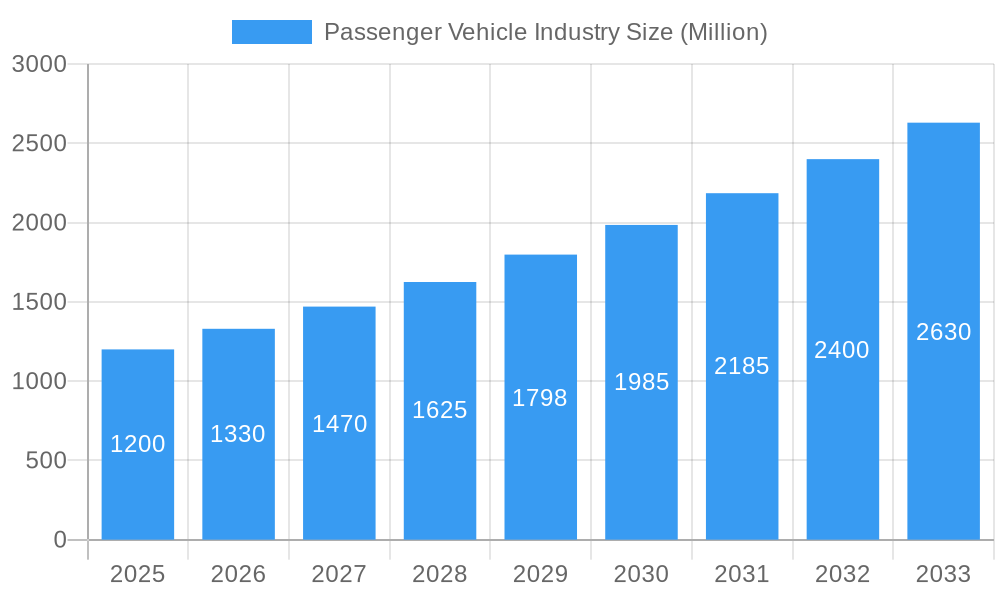

The global passenger vehicle market is projected for significant expansion, anticipated to reach 11.37 billion by 2025, with a Compound Annual Growth Rate (CAGR) of 11.24%. This robust growth is propelled by rising disposable incomes in emerging markets, increased demand for personal mobility, and advancements in automotive technology. Key drivers include the adoption of Advanced Driver-Assistance Systems (ADAS), enhanced connectivity, and improved fuel efficiency. The transition to sustainable transportation, driven by environmental concerns and regulatory mandates, is a major catalyst, particularly for Battery Electric Vehicles (BEV), Fuel Cell Electric Vehicles (FCEV), Hybrid Electric Vehicles (HEV), and Plug-in Hybrid Electric Vehicles (PHEV). The market also sees strong demand for Sports Utility Vehicles (SUVs) and crossovers, alongside continued popularity of sedans and hatchbacks.

Passenger Vehicle Industry Market Size (In Billion)

Market challenges include raw material price volatility, geopolitical uncertainties impacting supply chains, and the higher initial cost of electric vehicles. Continuous innovation in battery technology, material science, and manufacturing processes, alongside government incentives and growing consumer environmental awareness, are expected to overcome these obstacles and accelerate the shift towards cleaner mobility, ensuring sustained growth for the passenger vehicle sector.

Passenger Vehicle Industry Company Market Share

Passenger Vehicle Industry: Comprehensive Market Analysis and Future Outlook (2019–2033)

This in-depth report provides a definitive analysis of the global Passenger Vehicle Industry, covering historical trends, current dynamics, and future projections from 2019 to 2033. With the base year at 2025 and a forecast period extending to 2033, this report leverages high-traffic keywords and granular market segmentation to offer unparalleled insights for industry professionals, investors, and strategists. We analyze the intricate parent and child market structures, focusing on key vehicle configurations and propulsion types to deliver a holistic view of this dynamic sector. All quantitative data is presented in Million units.

Passenger Vehicle Industry Market Dynamics & Structure

The global passenger vehicle industry is characterized by a moderate to high market concentration, with a few dominant players holding significant market share. Technological innovation, particularly in electrification and autonomous driving, serves as a primary driver, pushing manufacturers to invest heavily in R&D. Stringent regulatory frameworks, aimed at reducing emissions and enhancing safety, are shaping product development and market entry strategies. The competitive landscape includes traditional internal combustion engine (ICE) vehicles, a rapidly growing segment of hybrid and electric vehicles (HEVs, PHEVs, BEVs, FCEVs), and emerging alternative fuel vehicles (CNG, LPG).

- Market Concentration: Dominated by key automotive giants, with strategic M&A activity consolidating market power.

- Technological Innovation: Driven by advancements in battery technology, artificial intelligence for autonomous systems, and lightweight materials.

- Regulatory Frameworks: Emission standards (e.g., Euro 7, CAFE standards) and safety regulations are increasingly influential.

- Competitive Product Substitutes: Growing competition from EVs, shared mobility services, and public transportation in urban centers.

- End-User Demographics: Shifting preferences towards SUVs, crossovers, and eco-friendly vehicles, influenced by generational trends and environmental awareness.

- M&A Trends: Consolidation of smaller players and strategic alliances to share R&D costs and expand market reach. For example, the period saw increased consolidation in component suppliers and EV startups.

Passenger Vehicle Industry Growth Trends & Insights

The passenger vehicle industry is poised for significant evolution, driven by a confluence of technological advancements, shifting consumer preferences, and supportive government policies. The historical period (2019–2024) witnessed a nuanced recovery from global disruptions, with an increasing focus on sustainable mobility solutions. The base year (2025) represents a critical juncture, with the industry accelerating its transition towards cleaner propulsion systems and advanced technological integration.

The forecast period (2025–2033) is anticipated to be marked by robust growth, primarily fueled by the escalating adoption of electric vehicles (EVs) and plug-in hybrid electric vehicles (PHEVs). Market penetration of battery electric vehicles (BEVs) is projected to surge as battery costs decline, charging infrastructure expands, and range anxiety diminishes. Hybrid electric vehicles (HEVs) will continue to serve as a crucial transitional technology, appealing to a broader consumer base seeking fuel efficiency without the immediate commitment to full electrification. Fuel cell electric vehicles (FCEVs), while still a niche segment, are expected to see incremental growth, particularly in regions with robust hydrogen infrastructure development.

Technological disruptions are not limited to propulsion. Advances in artificial intelligence and sensor technology are driving the development of sophisticated Advanced Driver-Assistance Systems (ADAS) and paving the way for greater levels of vehicle autonomy. Consumer behavior is also undergoing a significant shift, with a growing emphasis on sustainability, connectivity, and personalized in-car experiences. This has led to increased demand for connected car features, over-the-air updates, and intuitive user interfaces. The rise of subscription-based ownership models and the growing popularity of ride-sharing platforms will also influence market dynamics, potentially altering traditional sales volumes and ownership patterns.

The increasing demand for Sports Utility Vehicles (SUVs) and Crossovers across all propulsion types, from gasoline and diesel to hybrid and electric powertrains, underscores a persistent consumer preference for versatility and space. Hatchbacks and Sedans will continue to hold significant market share, particularly in urban environments and for budget-conscious consumers, but their growth trajectory may be moderated by the SUV trend. The industry's ability to navigate supply chain complexities, semiconductor shortages, and evolving geopolitical landscapes will be critical in realizing its full growth potential. The overall Compound Annual Growth Rate (CAGR) for the passenger vehicle market is projected to be approximately 4.5% from 2025 to 2033.

Dominant Regions, Countries, or Segments in Passenger Vehicle Industry

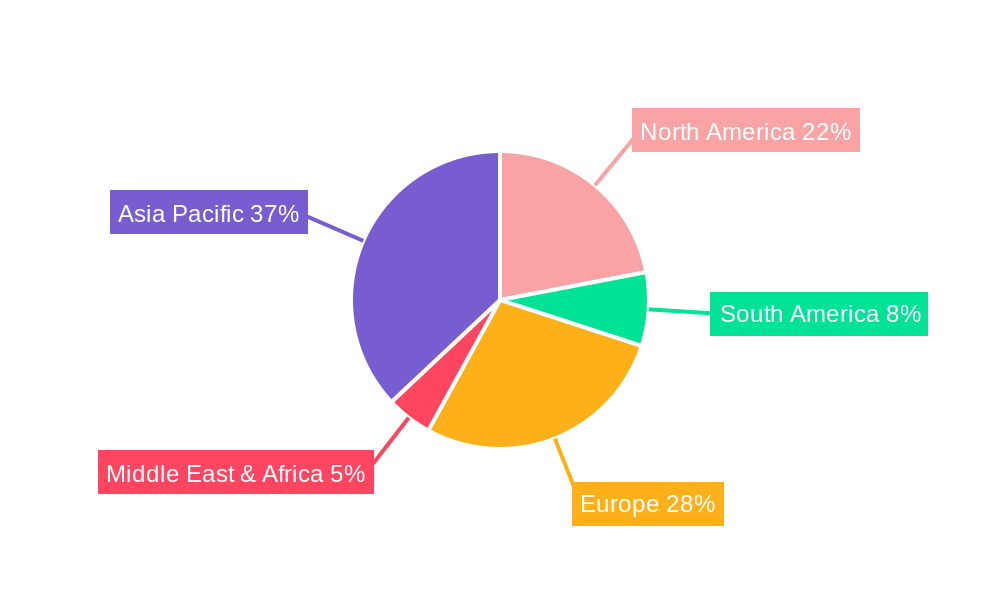

The global passenger vehicle industry is experiencing a dynamic shift in its dominant regions and segments, driven by diverse economic policies, technological adoption rates, and evolving consumer demands.

Dominant Regions:

- Asia-Pacific: This region, particularly China, is the undisputed leader in passenger vehicle sales and production. Its dominance is fueled by a massive domestic market, strong government support for electric vehicle adoption, and significant investments by both local and international manufacturers. The growth in electric vehicle sales in China is unprecedented, driven by favorable subsidies, an expanding charging infrastructure, and a wide array of affordable EV models. The region's burgeoning middle class and rapid urbanization also contribute to sustained demand for passenger cars.

- Europe: Europe is a strong contender, characterized by its stringent emission regulations and a proactive approach towards electrification. Countries like Germany, France, and the UK are leading the charge in the adoption of hybrid and electric vehicles. The EU's ambitious climate targets and the phasing out of internal combustion engine vehicles are significant growth accelerators. The demand for premium and performance-oriented vehicles also remains strong in this region.

- North America: While historically dominated by gasoline-powered vehicles, North America is witnessing a rapid acceleration in the adoption of electric vehicles, particularly in the United States. Government incentives, the growing popularity of electric SUVs and trucks, and the expansion of charging networks are key drivers. The region's large consumer base and the presence of major automotive manufacturers ensure its continued significance.

Dominant Segments:

Vehicle Configuration:

- Sports Utility Vehicle (SUV): The SUV segment continues its reign across all propulsion types, appealing to a broad demographic due to its perceived versatility, higher driving position, and cargo capacity. Its market share is expected to remain dominant through the forecast period.

- Passenger Cars (Hatchback, Sedan): These segments will continue to be crucial, especially in urban areas and for cost-conscious consumers. Hatchbacks are likely to maintain popularity in compact city cars, while sedans will cater to traditional buyers and executive segments.

Propulsion Type:

- Hybrid and Electric Vehicles (HEV, PHEV, BEV, FCEV): This category is the primary growth engine for the industry.

- Battery Electric Vehicles (BEV): Expected to experience the highest growth rate, driven by declining battery costs, expanding charging infrastructure, and increasing model availability across all vehicle types. Key markets like China and Europe are leading this transition.

- Plug-in Hybrid Electric Vehicles (PHEV): Will continue to be a significant segment, offering a bridge for consumers transitioning to full electric mobility, providing electric range for daily commutes and the flexibility of gasoline engines for longer journeys.

- Hybrid Electric Vehicles (HEV): Will remain a substantial part of the market, particularly in regions where EV infrastructure is still developing, offering improved fuel efficiency over traditional ICE vehicles.

- Internal Combustion Engine (ICE):

- Gasoline: Will continue to hold a significant market share, especially in emerging markets and for consumers who prioritize lower upfront costs. However, its growth is projected to slow down considerably.

- Diesel: Its market share is expected to decline in most developed regions due to stricter emission regulations and environmental concerns, though it may retain some presence in commercial applications and specific markets.

- CNG and LPG: These alternative fuels will likely see niche growth in specific markets and for fleet applications where regulatory incentives or fuel price advantages exist.

- Hybrid and Electric Vehicles (HEV, PHEV, BEV, FCEV): This category is the primary growth engine for the industry.

Passenger Vehicle Industry Product Landscape

The passenger vehicle industry is currently defined by a surge in innovative product offerings, with a strong emphasis on electrification and advanced technology. Sports Utility Vehicles (SUVs) and Crossovers are leading this transformation, available in a wide array of hybrid and electric configurations. Battery Electric Vehicles (BEVs) are at the forefront, featuring enhanced battery ranges, faster charging capabilities, and sophisticated thermal management systems. Key product innovations include the introduction of all-wheel-drive electric variants, such as the Mustang Mach-E, equipped with standard heated seats and steering wheels, enhancing user comfort and performance in diverse conditions. The integration of advanced driver-assistance systems (ADAS) and intuitive infotainment platforms is becoming standard across most new models, offering enhanced safety and connectivity.

Key Drivers, Barriers & Challenges in Passenger Vehicle Industry

Key Drivers:

- Technological Advancements: Rapid innovation in battery technology, electric powertrains, autonomous driving systems, and connectivity features is a primary catalyst.

- Environmental Regulations & Government Incentives: Stringent emission standards and supportive policies for electric vehicles (tax credits, subsidies) are significantly accelerating adoption.

- Growing Consumer Environmental Awareness: Increasing public concern over climate change is driving demand for sustainable mobility solutions.

- Decreasing Battery Costs: Declining production costs of batteries are making electric vehicles more affordable and competitive.

Barriers & Challenges:

- Supply Chain Disruptions: Ongoing shortages of critical components, particularly semiconductors, continue to impact production volumes and lead times.

- Charging Infrastructure Gaps: The availability and reliability of public charging infrastructure remain a concern in many regions, hindering widespread EV adoption.

- High Upfront Cost of EVs: While decreasing, the initial purchase price of electric vehicles can still be a deterrent for a significant portion of consumers.

- Grid Capacity and Renewable Energy Integration: The increasing demand for electricity from EVs necessitates upgrades to power grids and a greater reliance on renewable energy sources.

- Geopolitical Instability: Global events can impact raw material availability and pricing, as well as disrupt manufacturing and logistics.

Emerging Opportunities in Passenger Vehicle Industry

Emerging opportunities within the passenger vehicle industry lie in the expansion of electric vehicle ecosystems, the development of smart city mobility solutions, and the growing demand for personalized and sustainable transportation. The increasing focus on circular economy principles presents opportunities in battery recycling and sustainable material sourcing. Furthermore, the untapped potential in emerging markets, where EV adoption is still nascent but poised for rapid growth, offers significant expansion avenues. The evolution of autonomous driving technology opens doors for new mobility-as-a-service (MaaS) models and on-demand transportation solutions, catering to changing urban lifestyles.

Growth Accelerators in the Passenger Vehicle Industry Industry

Several catalysts are poised to accelerate long-term growth in the passenger vehicle industry. Significant investments in battery gigafactories and the development of next-generation battery chemistries promise to further reduce costs and improve performance. Strategic partnerships between automotive manufacturers, technology companies, and energy providers are crucial for developing integrated mobility solutions and robust charging networks. The continued refinement of autonomous driving technology, coupled with regulatory progress, will unlock new revenue streams and redefine personal mobility. Market expansion into underserved regions and the introduction of innovative business models, such as flexible subscription services, will also drive sustained growth.

Key Players Shaping the Passenger Vehicle Industry Market

- Bayerische Motoren Werke AG

- Nissan Motor Co Ltd

- General Motors Company

- Volkswagen A

- Daimler AG (Mercedes-Benz AG)

- Hyundai Motor Company

- Kia Corporation

- Toyota Motor Corporation

- Honda Motor Co Ltd

- Ford Motor Company

Notable Milestones in Passenger Vehicle Industry Sector

- December 2023: Ford introduces the Mustang Mach-E with electric all-wheel drive, standard heated seats, and steering wheel.

- December 2023: Hyundai Motor unveils "Strategy 2025," committing KRW 61.1 trillion in R&D for future technology, aiming to electrify the majority of new vehicles by 2030 in key markets and by 2035 in emerging markets.

- December 2023: Toyota debuts the Corolla GR-S in Brazil, featuring a 2.0-liter Dynamic Force Atkinson flex cycle engine producing 177 horsepower on ethanol and 169 horsepower on gasoline.

In-Depth Passenger Vehicle Industry Market Outlook

The passenger vehicle industry is on an accelerated path of transformation, with electrification and technological integration forming the bedrock of its future. The market outlook is exceptionally positive, driven by a global commitment to sustainability and the continuous evolution of automotive technology. The projected growth from 2025 to 2033 indicates a significant shift towards Battery Electric Vehicles (BEVs) and Plug-in Hybrid Electric Vehicles (PHEVs), supported by government initiatives and decreasing battery costs. Strategic collaborations, advancements in autonomous driving, and the development of comprehensive charging infrastructures are set to redefine mobility. Emerging markets present substantial untapped potential, promising further expansion and innovation. The industry's resilience and adaptability to evolving consumer preferences and regulatory landscapes will be key to realizing its full growth potential.

Passenger Vehicle Industry Segmentation

-

1. Vehicle Configuration

-

1.1. Passenger Cars

- 1.1.1. Hatchback

- 1.1.2. Sedan

- 1.1.3. Sports Utility Vehicle

-

1.1. Passenger Cars

-

2. Propulsion Type

-

2.1. Hybrid and Electric Vehicles

-

2.1.1. By Fuel Category

- 2.1.1.1. BEV

- 2.1.1.2. FCEV

- 2.1.1.3. HEV

- 2.1.1.4. PHEV

-

2.1.1. By Fuel Category

-

2.2. ICE

- 2.2.1. CNG

- 2.2.2. Diesel

- 2.2.3. Gasoline

- 2.2.4. LPG

-

2.1. Hybrid and Electric Vehicles

Passenger Vehicle Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Passenger Vehicle Industry Regional Market Share

Geographic Coverage of Passenger Vehicle Industry

Passenger Vehicle Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.24% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Configuration

- 5.1.1. Passenger Cars

- 5.1.1.1. Hatchback

- 5.1.1.2. Sedan

- 5.1.1.3. Sports Utility Vehicle

- 5.1.1. Passenger Cars

- 5.2. Market Analysis, Insights and Forecast - by Propulsion Type

- 5.2.1. Hybrid and Electric Vehicles

- 5.2.1.1. By Fuel Category

- 5.2.1.1.1. BEV

- 5.2.1.1.2. FCEV

- 5.2.1.1.3. HEV

- 5.2.1.1.4. PHEV

- 5.2.1.1. By Fuel Category

- 5.2.2. ICE

- 5.2.2.1. CNG

- 5.2.2.2. Diesel

- 5.2.2.3. Gasoline

- 5.2.2.4. LPG

- 5.2.1. Hybrid and Electric Vehicles

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Configuration

- 6. Global Passenger Vehicle Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Configuration

- 6.1.1. Passenger Cars

- 6.1.1.1. Hatchback

- 6.1.1.2. Sedan

- 6.1.1.3. Sports Utility Vehicle

- 6.1.1. Passenger Cars

- 6.2. Market Analysis, Insights and Forecast - by Propulsion Type

- 6.2.1. Hybrid and Electric Vehicles

- 6.2.1.1. By Fuel Category

- 6.2.1.1.1. BEV

- 6.2.1.1.2. FCEV

- 6.2.1.1.3. HEV

- 6.2.1.1.4. PHEV

- 6.2.1.1. By Fuel Category

- 6.2.2. ICE

- 6.2.2.1. CNG

- 6.2.2.2. Diesel

- 6.2.2.3. Gasoline

- 6.2.2.4. LPG

- 6.2.1. Hybrid and Electric Vehicles

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Configuration

- 7. North America Passenger Vehicle Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Vehicle Configuration

- 7.1.1. Passenger Cars

- 7.1.1.1. Hatchback

- 7.1.1.2. Sedan

- 7.1.1.3. Sports Utility Vehicle

- 7.1.1. Passenger Cars

- 7.2. Market Analysis, Insights and Forecast - by Propulsion Type

- 7.2.1. Hybrid and Electric Vehicles

- 7.2.1.1. By Fuel Category

- 7.2.1.1.1. BEV

- 7.2.1.1.2. FCEV

- 7.2.1.1.3. HEV

- 7.2.1.1.4. PHEV

- 7.2.1.1. By Fuel Category

- 7.2.2. ICE

- 7.2.2.1. CNG

- 7.2.2.2. Diesel

- 7.2.2.3. Gasoline

- 7.2.2.4. LPG

- 7.2.1. Hybrid and Electric Vehicles

- 7.1. Market Analysis, Insights and Forecast - by Vehicle Configuration

- 8. South America Passenger Vehicle Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Vehicle Configuration

- 8.1.1. Passenger Cars

- 8.1.1.1. Hatchback

- 8.1.1.2. Sedan

- 8.1.1.3. Sports Utility Vehicle

- 8.1.1. Passenger Cars

- 8.2. Market Analysis, Insights and Forecast - by Propulsion Type

- 8.2.1. Hybrid and Electric Vehicles

- 8.2.1.1. By Fuel Category

- 8.2.1.1.1. BEV

- 8.2.1.1.2. FCEV

- 8.2.1.1.3. HEV

- 8.2.1.1.4. PHEV

- 8.2.1.1. By Fuel Category

- 8.2.2. ICE

- 8.2.2.1. CNG

- 8.2.2.2. Diesel

- 8.2.2.3. Gasoline

- 8.2.2.4. LPG

- 8.2.1. Hybrid and Electric Vehicles

- 8.1. Market Analysis, Insights and Forecast - by Vehicle Configuration

- 9. Europe Passenger Vehicle Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Vehicle Configuration

- 9.1.1. Passenger Cars

- 9.1.1.1. Hatchback

- 9.1.1.2. Sedan

- 9.1.1.3. Sports Utility Vehicle

- 9.1.1. Passenger Cars

- 9.2. Market Analysis, Insights and Forecast - by Propulsion Type

- 9.2.1. Hybrid and Electric Vehicles

- 9.2.1.1. By Fuel Category

- 9.2.1.1.1. BEV

- 9.2.1.1.2. FCEV

- 9.2.1.1.3. HEV

- 9.2.1.1.4. PHEV

- 9.2.1.1. By Fuel Category

- 9.2.2. ICE

- 9.2.2.1. CNG

- 9.2.2.2. Diesel

- 9.2.2.3. Gasoline

- 9.2.2.4. LPG

- 9.2.1. Hybrid and Electric Vehicles

- 9.1. Market Analysis, Insights and Forecast - by Vehicle Configuration

- 10. Middle East & Africa Passenger Vehicle Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Vehicle Configuration

- 10.1.1. Passenger Cars

- 10.1.1.1. Hatchback

- 10.1.1.2. Sedan

- 10.1.1.3. Sports Utility Vehicle

- 10.1.1. Passenger Cars

- 10.2. Market Analysis, Insights and Forecast - by Propulsion Type

- 10.2.1. Hybrid and Electric Vehicles

- 10.2.1.1. By Fuel Category

- 10.2.1.1.1. BEV

- 10.2.1.1.2. FCEV

- 10.2.1.1.3. HEV

- 10.2.1.1.4. PHEV

- 10.2.1.1. By Fuel Category

- 10.2.2. ICE

- 10.2.2.1. CNG

- 10.2.2.2. Diesel

- 10.2.2.3. Gasoline

- 10.2.2.4. LPG

- 10.2.1. Hybrid and Electric Vehicles

- 10.1. Market Analysis, Insights and Forecast - by Vehicle Configuration

- 11. Asia Pacific Passenger Vehicle Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Vehicle Configuration

- 11.1.1. Passenger Cars

- 11.1.1.1. Hatchback

- 11.1.1.2. Sedan

- 11.1.1.3. Sports Utility Vehicle

- 11.1.1. Passenger Cars

- 11.2. Market Analysis, Insights and Forecast - by Propulsion Type

- 11.2.1. Hybrid and Electric Vehicles

- 11.2.1.1. By Fuel Category

- 11.2.1.1.1. BEV

- 11.2.1.1.2. FCEV

- 11.2.1.1.3. HEV

- 11.2.1.1.4. PHEV

- 11.2.1.1. By Fuel Category

- 11.2.2. ICE

- 11.2.2.1. CNG

- 11.2.2.2. Diesel

- 11.2.2.3. Gasoline

- 11.2.2.4. LPG

- 11.2.1. Hybrid and Electric Vehicles

- 11.1. Market Analysis, Insights and Forecast - by Vehicle Configuration

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Bayerische Motoren Werke AG

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Nissan Motor Co Ltd

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 General Motors Company

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Volkswagen A

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Daimler AG (Mercedes-Benz AG)

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Hyundai Motor Company

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Kia Corporation

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Toyota Motor Corporation

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Honda Motor Co Ltd

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Ford Motor Company

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Bayerische Motoren Werke AG

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Passenger Vehicle Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Passenger Vehicle Industry Revenue (billion), by Vehicle Configuration 2025 & 2033

- Figure 3: North America Passenger Vehicle Industry Revenue Share (%), by Vehicle Configuration 2025 & 2033

- Figure 4: North America Passenger Vehicle Industry Revenue (billion), by Propulsion Type 2025 & 2033

- Figure 5: North America Passenger Vehicle Industry Revenue Share (%), by Propulsion Type 2025 & 2033

- Figure 6: North America Passenger Vehicle Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Passenger Vehicle Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Passenger Vehicle Industry Revenue (billion), by Vehicle Configuration 2025 & 2033

- Figure 9: South America Passenger Vehicle Industry Revenue Share (%), by Vehicle Configuration 2025 & 2033

- Figure 10: South America Passenger Vehicle Industry Revenue (billion), by Propulsion Type 2025 & 2033

- Figure 11: South America Passenger Vehicle Industry Revenue Share (%), by Propulsion Type 2025 & 2033

- Figure 12: South America Passenger Vehicle Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Passenger Vehicle Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Passenger Vehicle Industry Revenue (billion), by Vehicle Configuration 2025 & 2033

- Figure 15: Europe Passenger Vehicle Industry Revenue Share (%), by Vehicle Configuration 2025 & 2033

- Figure 16: Europe Passenger Vehicle Industry Revenue (billion), by Propulsion Type 2025 & 2033

- Figure 17: Europe Passenger Vehicle Industry Revenue Share (%), by Propulsion Type 2025 & 2033

- Figure 18: Europe Passenger Vehicle Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Passenger Vehicle Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Passenger Vehicle Industry Revenue (billion), by Vehicle Configuration 2025 & 2033

- Figure 21: Middle East & Africa Passenger Vehicle Industry Revenue Share (%), by Vehicle Configuration 2025 & 2033

- Figure 22: Middle East & Africa Passenger Vehicle Industry Revenue (billion), by Propulsion Type 2025 & 2033

- Figure 23: Middle East & Africa Passenger Vehicle Industry Revenue Share (%), by Propulsion Type 2025 & 2033

- Figure 24: Middle East & Africa Passenger Vehicle Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Passenger Vehicle Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Passenger Vehicle Industry Revenue (billion), by Vehicle Configuration 2025 & 2033

- Figure 27: Asia Pacific Passenger Vehicle Industry Revenue Share (%), by Vehicle Configuration 2025 & 2033

- Figure 28: Asia Pacific Passenger Vehicle Industry Revenue (billion), by Propulsion Type 2025 & 2033

- Figure 29: Asia Pacific Passenger Vehicle Industry Revenue Share (%), by Propulsion Type 2025 & 2033

- Figure 30: Asia Pacific Passenger Vehicle Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Passenger Vehicle Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Passenger Vehicle Industry Revenue billion Forecast, by Vehicle Configuration 2020 & 2033

- Table 2: Global Passenger Vehicle Industry Revenue billion Forecast, by Propulsion Type 2020 & 2033

- Table 3: Global Passenger Vehicle Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Passenger Vehicle Industry Revenue billion Forecast, by Vehicle Configuration 2020 & 2033

- Table 5: Global Passenger Vehicle Industry Revenue billion Forecast, by Propulsion Type 2020 & 2033

- Table 6: Global Passenger Vehicle Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Passenger Vehicle Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Passenger Vehicle Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Passenger Vehicle Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Passenger Vehicle Industry Revenue billion Forecast, by Vehicle Configuration 2020 & 2033

- Table 11: Global Passenger Vehicle Industry Revenue billion Forecast, by Propulsion Type 2020 & 2033

- Table 12: Global Passenger Vehicle Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Passenger Vehicle Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Passenger Vehicle Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Passenger Vehicle Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Passenger Vehicle Industry Revenue billion Forecast, by Vehicle Configuration 2020 & 2033

- Table 17: Global Passenger Vehicle Industry Revenue billion Forecast, by Propulsion Type 2020 & 2033

- Table 18: Global Passenger Vehicle Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Passenger Vehicle Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Passenger Vehicle Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Passenger Vehicle Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Passenger Vehicle Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Passenger Vehicle Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Passenger Vehicle Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Passenger Vehicle Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Passenger Vehicle Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Passenger Vehicle Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Passenger Vehicle Industry Revenue billion Forecast, by Vehicle Configuration 2020 & 2033

- Table 29: Global Passenger Vehicle Industry Revenue billion Forecast, by Propulsion Type 2020 & 2033

- Table 30: Global Passenger Vehicle Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Passenger Vehicle Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Passenger Vehicle Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Passenger Vehicle Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Passenger Vehicle Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Passenger Vehicle Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Passenger Vehicle Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Passenger Vehicle Industry Revenue billion Forecast, by Vehicle Configuration 2020 & 2033

- Table 38: Global Passenger Vehicle Industry Revenue billion Forecast, by Propulsion Type 2020 & 2033

- Table 39: Global Passenger Vehicle Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Passenger Vehicle Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Passenger Vehicle Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Passenger Vehicle Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Passenger Vehicle Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Passenger Vehicle Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Passenger Vehicle Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Passenger Vehicle Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Passenger Vehicle Industry?

The projected CAGR is approximately 11.24%.

2. Which companies are prominent players in the Passenger Vehicle Industry?

Key companies in the market include Bayerische Motoren Werke AG, Nissan Motor Co Ltd, General Motors Company, Volkswagen A, Daimler AG (Mercedes-Benz AG), Hyundai Motor Company, Kia Corporation, Toyota Motor Corporation, Honda Motor Co Ltd, Ford Motor Company.

3. What are the main segments of the Passenger Vehicle Industry?

The market segments include Vehicle Configuration, Propulsion Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 11.37 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Travel and Tourism Industry is Driving the Car Rental Market.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Increasing Popularity of Ride-Sharing Services Pose Challenges for the Conventional Car Rental Market.

8. Can you provide examples of recent developments in the market?

December 2023: Mustang Mach-E is avaiable with electric all-wheel drive and has standard heated seats and steering wheel.December 2023: Hyundai Motor unveiled its "Strategy 2025" blueprint, outlining KRW 61.1 trillion in investments for future technology research and development (R&D) until 2025. The goal is to electrify the majority of new vehicles in key markets such as Korea, the United States, China, and Europe by 2030, with emerging markets such as India and Brazil following suit by 2035.December 2023: Toyota debuts the Corolla GR-S in Brazil. Its 2.0-liter Dynamic Force Atkinson flex cycle engine generates 177 horsepower when running on ethanol and 169 horsepower when running on gasoline, with 21.4 kgfm of torque in both cases.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Passenger Vehicle Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Passenger Vehicle Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Passenger Vehicle Industry?

To stay informed about further developments, trends, and reports in the Passenger Vehicle Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence