Key Insights

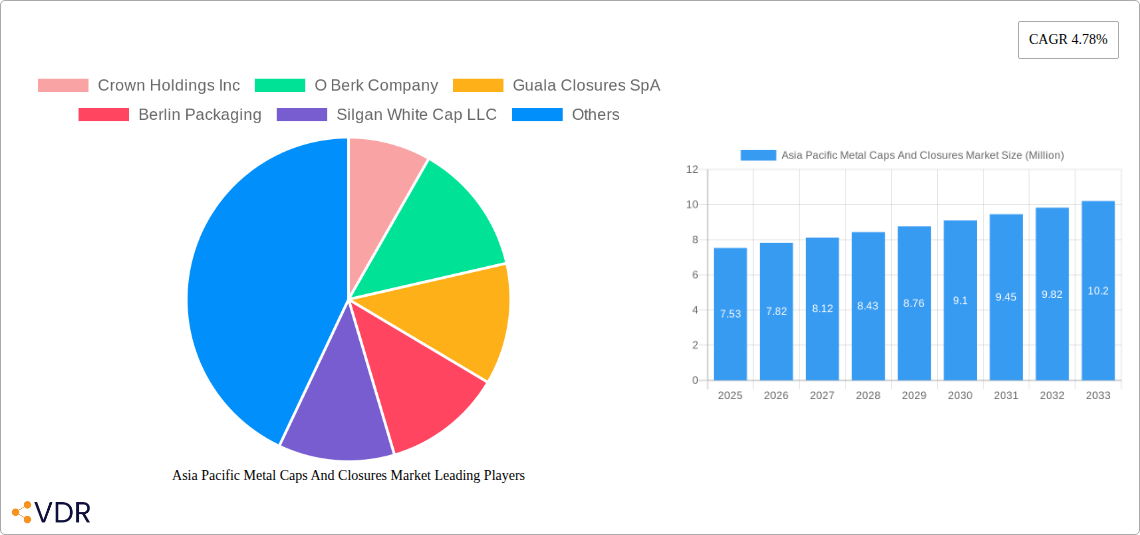

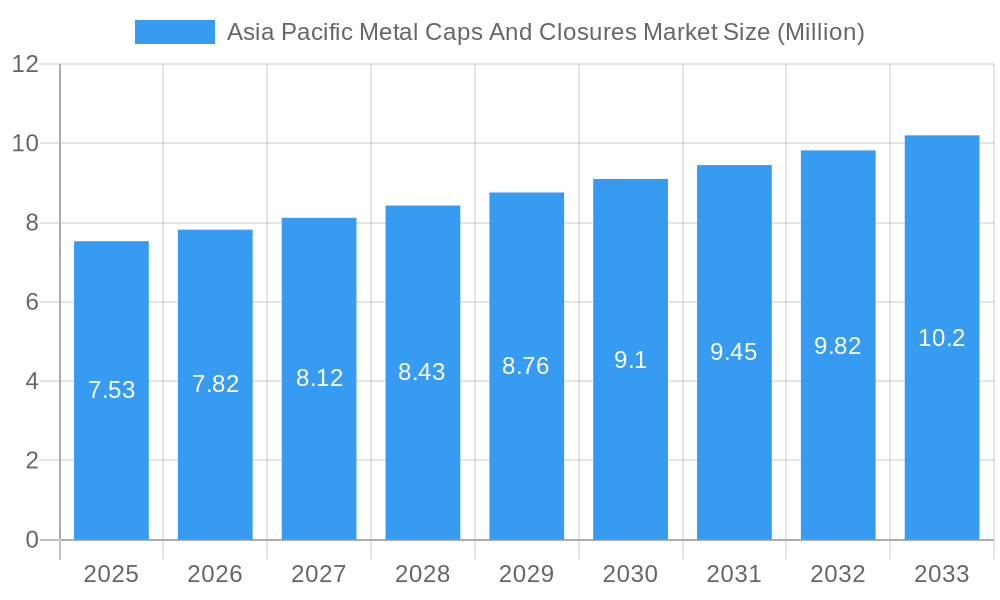

The Asia Pacific metal caps and closures market is poised for substantial growth, projected to reach a market size of approximately USD 7.53 million with a robust Compound Annual Growth Rate (CAGR) of 4.78% over the forecast period of 2025-2033. This expansion is fueled by the increasing demand from key end-user industries, particularly the beverage sector, encompassing both alcoholic and non-alcoholic drinks. The burgeoning middle class in countries like China and India, coupled with evolving consumer preferences for convenience and product integrity, directly drives the need for secure and reliable metal closures. Furthermore, the pharmaceutical industry's consistent growth, amplified by an aging population and increased healthcare spending, adds significant momentum to market demand. The personal care segment also contributes, driven by the popularity of premium and travel-sized products requiring durable packaging solutions.

Asia Pacific Metal Caps And Closures Market Market Size (In Million)

The market's dynamics are characterized by distinct material types, with aluminum and steel dominating production, offering a balance of cost-effectiveness and performance. Crown caps and screw caps represent the most prevalent closure types, catering to a wide array of product applications. However, emerging trends such as the development of innovative tamper-evident closures and sustainable material options are shaping the competitive landscape. While the market exhibits strong growth drivers, potential restraints may include fluctuations in raw material prices, particularly for aluminum and steel, which could impact manufacturing costs. Additionally, increasing regulatory scrutiny concerning packaging materials and a growing consumer preference for eco-friendly alternatives, though an opportunity for innovation, could pose challenges for traditional metal closure manufacturers if they fail to adapt. The Asia Pacific region, with its vast consumer base and expanding industrial sectors, is expected to be the primary growth engine for this market.

Asia Pacific Metal Caps And Closures Market Company Market Share

This in-depth report offers a detailed analysis of the Asia Pacific Metal Caps and Closures Market, a critical segment within the broader packaging industry. Spanning from 2019 to 2033, with a base year of 2025, this study provides crucial insights into market dynamics, growth trends, competitive landscape, and future outlook for stakeholders. The report meticulously examines parent and child market segments, utilizing high-traffic keywords to ensure maximum visibility for industry professionals seeking to understand the evolution of aluminum and steel caps and closures across diverse end-user industries.

Asia Pacific Metal Caps And Closures Market Market Dynamics & Structure

The Asia Pacific metal caps and closures market is characterized by moderate concentration, with a growing emphasis on technological innovation and sustainability. Key drivers include increasing demand from the food and beverage sectors, coupled with rising disposable incomes across emerging economies. Regulatory frameworks, particularly those pertaining to food safety and environmental standards, are progressively shaping manufacturing processes and material choices. While competition from alternative packaging materials like plastic and glass exists, the inherent durability, recyclability, and barrier properties of metal closures maintain their strong market position. End-user demographics are shifting, with a greater demand for convenient and aesthetically appealing packaging solutions. Mergers and acquisitions (M&A) activity is on the rise as companies seek to expand their regional presence and product portfolios. For instance, the increasing adoption of advanced coating technologies and improved sealing mechanisms represents a significant innovation driver. Barriers to entry include high initial capital investment for manufacturing facilities and the need for specialized expertise in metal forming and finishing.

- Market Concentration: Moderate, with a few dominant global players and a growing number of regional manufacturers.

- Technological Innovation Drivers: Advancements in material science, barrier coatings, and tamper-evident features.

- Regulatory Frameworks: Strict adherence to food safety standards (e.g., FDA, EFSA equivalents), environmental regulations regarding recyclability and waste reduction.

- Competitive Product Substitutes: Plastic caps, glass stoppers, corks, and alternative closure systems.

- End-User Demographics: Growing middle class, urbanization, and a demand for premium and convenient packaged goods.

- M&A Trends: Strategic acquisitions to gain market share, access new technologies, and expand geographical reach.

Asia Pacific Metal Caps And Closures Market Growth Trends & Insights

The Asia Pacific metal caps and closures market is poised for robust growth, driven by several key trends. The market size is projected to witness a substantial expansion driven by increasing consumption in rapidly developing economies and the persistent demand for safe, secure, and visually appealing packaging. Adoption rates for advanced metal closure solutions, particularly those offering enhanced tamper-evidence and extended shelf-life properties, are on an upward trajectory. Technological disruptions, such as the development of lighter-weight yet equally strong aluminum alloys and improved internal coatings, are further enhancing the performance and sustainability of these products. Consumer behavior shifts, including a growing preference for sustainably sourced and recyclable packaging, are compelling manufacturers to invest in eco-friendly production processes and materials. The increasing industrialization and a rising middle class across the region are fueling demand across a spectrum of end-user industries. The market penetration of specialized metal closures for niche applications is also expected to rise. The estimated market size in 2025 is projected to be approximately 75,200 million units, with a projected Compound Annual Growth Rate (CAGR) of 4.5% from 2025 to 2033.

Dominant Regions, Countries, or Segments in Asia Pacific Metal Caps And Closures Market

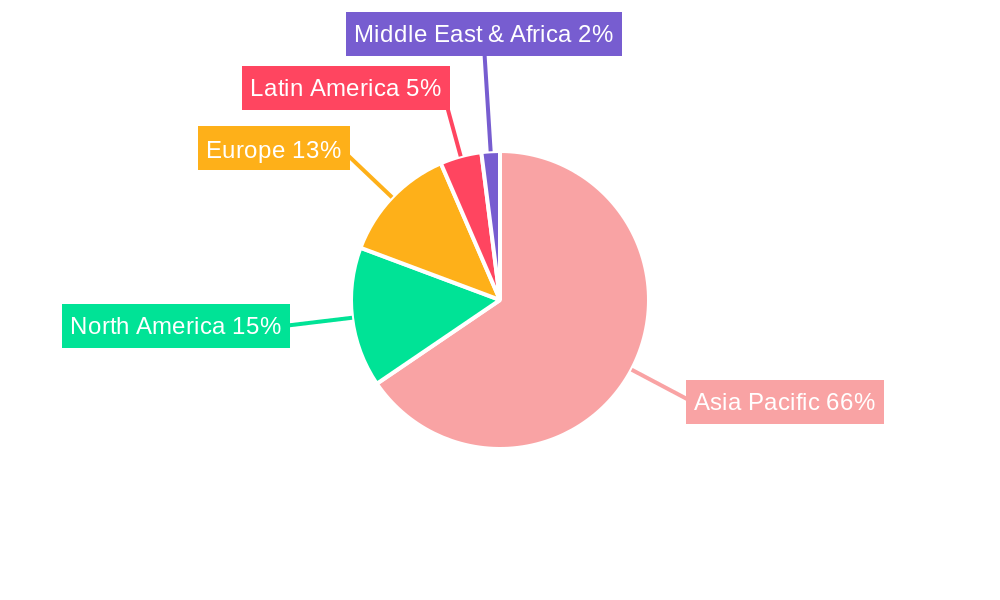

The Asia Pacific Metal Caps and Closures Market exhibits significant regional dominance, with China emerging as the leading country and the Food and Beverages segments, particularly non-alcoholic beverages, showcasing the highest growth potential. China's expansive manufacturing base, coupled with its massive domestic consumption of packaged goods, positions it at the forefront. The country's substantial investments in industrial infrastructure and favorable government policies supporting manufacturing exports further bolster its leadership. The dominance within the Material Type segment is shared between Aluminum and Steel. Aluminum closures are increasingly favored for beverage applications due to their lightweight nature and recyclability, while steel remains a strong contender for food and pharmaceutical packaging due to its robustness and cost-effectiveness.

Within Closures Type, Screw Caps are experiencing the most rapid growth, driven by their convenience and widespread adoption across various industries. Crown caps remain significant for the beer and beverage industry, while twist metal caps are also prevalent. The End-user Industry landscape is dominated by Food and Beverages. The non-alcoholic beverage sector, including juices, carbonated drinks, and water, represents a colossal demand driver. The alcoholic beverage segment also contributes significantly. The Pharmaceuticals sector, driven by the need for sterile and tamper-evident packaging, and the Personal Care industry, with its focus on aesthetic appeal and product preservation, are also crucial growth areas.

- Leading Country: China, driven by manufacturing prowess and vast domestic consumption.

- Dominant End-user Industries: Food and Beverages (especially non-alcoholic), followed by Pharmaceuticals and Personal Care.

- Key Drivers of Dominance:

- Economic Policies: Government support for manufacturing, trade agreements, and investment incentives in China and Southeast Asia.

- Infrastructure Development: Robust logistics networks, port facilities, and industrial zones facilitating production and distribution.

- Consumer Demand: Growing middle class, urbanization, and increasing per capita consumption of packaged goods.

- Technological Adoption: Increasing use of advanced manufacturing techniques and innovative closure designs.

- Market Share: China accounts for an estimated 40% of the Asia Pacific market, with the Food & Beverage segment holding over 60% share.

Asia Pacific Metal Caps And Closures Market Product Landscape

The product landscape of the Asia Pacific metal caps and closures market is dynamic, marked by continuous innovation aimed at enhancing functionality, sustainability, and aesthetic appeal. Manufacturers are actively developing lighter-weight aluminum and steel closures that maintain robust sealing capabilities, reducing material consumption and transportation costs. Advanced internal coatings are being deployed to improve product compatibility and extend shelf life, particularly for sensitive food and beverage products. Tamper-evident features, such as tear-off bands and induction seals, are increasingly integrated to assure product integrity and consumer safety. The trend towards decorative printing and specialized finishes on closures is also gaining momentum, enabling brand differentiation and premiumization in the competitive consumer goods market.

Key Drivers, Barriers & Challenges in Asia Pacific Metal Caps And Closures Market

Key Drivers: The primary forces propelling the Asia Pacific metal caps and closures market include the escalating demand for packaged food and beverages, driven by population growth and urbanization. Technological advancements in material science and manufacturing processes are enabling the production of more efficient, lighter-weight, and sustainable closures. Favorable government initiatives promoting domestic manufacturing and export growth in countries like China and India also play a crucial role. The increasing consumer preference for premium, safe, and convenient packaging solutions further fuels market expansion.

Barriers & Challenges: Despite the growth prospects, the market faces several challenges. Fluctuations in raw material prices, particularly for aluminum and steel, can impact profit margins. Stringent environmental regulations and the growing emphasis on recyclability necessitate continuous investment in sustainable production technologies. Intense competition from alternative packaging materials and established players can also exert downward pressure on pricing. Supply chain disruptions, exacerbated by geopolitical factors and logistics constraints, pose a significant operational hurdle.

Emerging Opportunities in Asia Pacific Metal Caps And Closures Market

Emerging opportunities in the Asia Pacific metal caps and closures market lie in the growing demand for specialized closures in niche applications. The expanding pharmaceutical sector, particularly for generic drugs and over-the-counter medications, presents a significant opportunity for tamper-evident and child-resistant closures. Furthermore, the rise of the e-commerce sector is creating a demand for robust and secure closures that can withstand the rigors of online distribution. The increasing consumer consciousness regarding health and wellness is also driving demand for closures that offer superior barrier properties and preserve the freshness of products like functional beverages and health supplements.

Growth Accelerators in the Asia Pacific Metal Caps And Closures Market Industry

Catalysts driving long-term growth in the Asia Pacific metal caps and closures market are multi-faceted. Technological breakthroughs in forming and coating processes are enabling the development of thinner yet stronger metal closures, leading to cost savings and reduced environmental impact. Strategic partnerships between raw material suppliers, manufacturers, and end-user brands are fostering innovation and supply chain resilience. Market expansion strategies, including the establishment of local manufacturing facilities in high-growth economies and the development of customized closure solutions for diverse regional preferences, are key accelerators. The increasing focus on circular economy principles and enhanced recyclability of metal packaging will also continue to drive investment and market adoption.

Key Players Shaping the Asia Pacific Metal Caps And Closures Market Market

- Crown Holdings Inc.

- O Berk Company

- Guala Closures SpA

- Berlin Packaging

- Silgan White Cap LLC

- Sonoco Products Company

- Alupac India

- Nippon Closures Co Ltd

- ACTEGA (A member of ALTANA)

- UA Packaging

Notable Milestones in Asia Pacific Metal Caps And Closures Market Sector

- April 2024: Vedanta Aluminium, a leading Indian aluminum producer, announced its expansion plans to become a top 3 global player, including a new 1.5 MTPA expansion at its Lanjigarh alumina refinery, increasing its capacity from 2 MTPA to 3.5 MTPA as part of a broader strategy to reach 5 MTPA, catering to increasing demands from industries like packaging and construction.

- July 2023: Crown Holdings Inc. extended its sustainability program, Twentyby30, by expanding its Aluminum Stewardship Initiative (ASI) certifications in Asia-Pacific. Its beverage packaging plants in Nong Khae and Crown TCP, Thailand, received ASI Performance Standard certification, bringing the total number of certified Crown facilities to 12.

In-Depth Asia Pacific Metal Caps And Closures Market Market Outlook

The Asia Pacific metal caps and closures market is set for sustained growth, driven by an unwavering demand from the food and beverage sectors and increasing adoption across pharmaceuticals and personal care. The continuous pursuit of lightweight, sustainable, and high-performance closure solutions will remain a central theme. Strategic investments in advanced manufacturing technologies and the expansion of production capacities in emerging economies will be crucial for market leaders. The integration of smart features and enhanced recyclability will further shape the market’s trajectory. Industry players are expected to focus on innovation that addresses both consumer convenience and environmental responsibility, thereby solidifying the long-term market potential and unlocking new strategic opportunities within this dynamic sector.

Asia Pacific Metal Caps And Closures Market Segmentation

-

1. Material Type

- 1.1. Aluminum

- 1.2. Steel

-

2. Closures Type

- 2.1. Crown Caps

- 2.2. Screw Caps

- 2.3. Twist Metal Caps

- 2.4. Other Closure Types

-

3. End-user Industry

- 3.1. Food

-

3.2. Beverages

- 3.2.1. Alcoholic

- 3.2.2. Non-alcoholic

- 3.3. Pharmaceuticals

- 3.4. Personal Care

- 3.5. Other End-user Industries

Asia Pacific Metal Caps And Closures Market Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. Japan

- 1.3. South Korea

- 1.4. India

- 1.5. Australia

- 1.6. New Zealand

- 1.7. Indonesia

- 1.8. Malaysia

- 1.9. Singapore

- 1.10. Thailand

- 1.11. Vietnam

- 1.12. Philippines

Asia Pacific Metal Caps And Closures Market Regional Market Share

Geographic Coverage of Asia Pacific Metal Caps And Closures Market

Asia Pacific Metal Caps And Closures Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.78% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 5.1.1. Aluminum

- 5.1.2. Steel

- 5.2. Market Analysis, Insights and Forecast - by Closures Type

- 5.2.1. Crown Caps

- 5.2.2. Screw Caps

- 5.2.3. Twist Metal Caps

- 5.2.4. Other Closure Types

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. Food

- 5.3.2. Beverages

- 5.3.2.1. Alcoholic

- 5.3.2.2. Non-alcoholic

- 5.3.3. Pharmaceuticals

- 5.3.4. Personal Care

- 5.3.5. Other End-user Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 6. Asia Pacific Metal Caps And Closures Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 6.1.1. Aluminum

- 6.1.2. Steel

- 6.2. Market Analysis, Insights and Forecast - by Closures Type

- 6.2.1. Crown Caps

- 6.2.2. Screw Caps

- 6.2.3. Twist Metal Caps

- 6.2.4. Other Closure Types

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. Food

- 6.3.2. Beverages

- 6.3.2.1. Alcoholic

- 6.3.2.2. Non-alcoholic

- 6.3.3. Pharmaceuticals

- 6.3.4. Personal Care

- 6.3.5. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Crown Holdings Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 O Berk Company

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Guala Closures SpA

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Berlin Packaging

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Silgan White Cap LLC

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Sonoco Products Company

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Alupac India

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Nippon Closures Co Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 ACTEGA (A member of ALTANA)

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 UA Packaging7 2 INVESTMENT ANALYSIS7 3 FUTURE OF THE MARKE

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Crown Holdings Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Asia Pacific Metal Caps And Closures Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Asia Pacific Metal Caps And Closures Market Share (%) by Company 2025

List of Tables

- Table 1: Asia Pacific Metal Caps And Closures Market Revenue Million Forecast, by Material Type 2020 & 2033

- Table 2: Asia Pacific Metal Caps And Closures Market Volume Billion Forecast, by Material Type 2020 & 2033

- Table 3: Asia Pacific Metal Caps And Closures Market Revenue Million Forecast, by Closures Type 2020 & 2033

- Table 4: Asia Pacific Metal Caps And Closures Market Volume Billion Forecast, by Closures Type 2020 & 2033

- Table 5: Asia Pacific Metal Caps And Closures Market Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 6: Asia Pacific Metal Caps And Closures Market Volume Billion Forecast, by End-user Industry 2020 & 2033

- Table 7: Asia Pacific Metal Caps And Closures Market Revenue Million Forecast, by Region 2020 & 2033

- Table 8: Asia Pacific Metal Caps And Closures Market Volume Billion Forecast, by Region 2020 & 2033

- Table 9: Asia Pacific Metal Caps And Closures Market Revenue Million Forecast, by Material Type 2020 & 2033

- Table 10: Asia Pacific Metal Caps And Closures Market Volume Billion Forecast, by Material Type 2020 & 2033

- Table 11: Asia Pacific Metal Caps And Closures Market Revenue Million Forecast, by Closures Type 2020 & 2033

- Table 12: Asia Pacific Metal Caps And Closures Market Volume Billion Forecast, by Closures Type 2020 & 2033

- Table 13: Asia Pacific Metal Caps And Closures Market Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 14: Asia Pacific Metal Caps And Closures Market Volume Billion Forecast, by End-user Industry 2020 & 2033

- Table 15: Asia Pacific Metal Caps And Closures Market Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Asia Pacific Metal Caps And Closures Market Volume Billion Forecast, by Country 2020 & 2033

- Table 17: China Asia Pacific Metal Caps And Closures Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: China Asia Pacific Metal Caps And Closures Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 19: Japan Asia Pacific Metal Caps And Closures Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Japan Asia Pacific Metal Caps And Closures Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 21: South Korea Asia Pacific Metal Caps And Closures Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: South Korea Asia Pacific Metal Caps And Closures Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 23: India Asia Pacific Metal Caps And Closures Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: India Asia Pacific Metal Caps And Closures Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 25: Australia Asia Pacific Metal Caps And Closures Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Australia Asia Pacific Metal Caps And Closures Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 27: New Zealand Asia Pacific Metal Caps And Closures Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: New Zealand Asia Pacific Metal Caps And Closures Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 29: Indonesia Asia Pacific Metal Caps And Closures Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Indonesia Asia Pacific Metal Caps And Closures Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 31: Malaysia Asia Pacific Metal Caps And Closures Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Malaysia Asia Pacific Metal Caps And Closures Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 33: Singapore Asia Pacific Metal Caps And Closures Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Singapore Asia Pacific Metal Caps And Closures Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 35: Thailand Asia Pacific Metal Caps And Closures Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Thailand Asia Pacific Metal Caps And Closures Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 37: Vietnam Asia Pacific Metal Caps And Closures Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Vietnam Asia Pacific Metal Caps And Closures Market Volume (Billion) Forecast, by Application 2020 & 2033

- Table 39: Philippines Asia Pacific Metal Caps And Closures Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 40: Philippines Asia Pacific Metal Caps And Closures Market Volume (Billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Asia Pacific Metal Caps And Closures Market?

The projected CAGR is approximately 4.78%.

2. Which companies are prominent players in the Asia Pacific Metal Caps And Closures Market?

Key companies in the market include Crown Holdings Inc, O Berk Company, Guala Closures SpA, Berlin Packaging, Silgan White Cap LLC, Sonoco Products Company, Alupac India, Nippon Closures Co Ltd, ACTEGA (A member of ALTANA), UA Packaging7 2 INVESTMENT ANALYSIS7 3 FUTURE OF THE MARKE.

3. What are the main segments of the Asia Pacific Metal Caps And Closures Market?

The market segments include Material Type, Closures Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 7.53 Million as of 2022.

5. What are some drivers contributing to market growth?

Increased Demand for Innovative Solutions from Various End Users; Superior Properties Compared to Other Closure Materials.

6. What are the notable trends driving market growth?

A Considerable Portion of the Market is Anticipated to be Held by Aluminum.

7. Are there any restraints impacting market growth?

Increased Demand for Innovative Solutions from Various End Users; Superior Properties Compared to Other Closure Materials.

8. Can you provide examples of recent developments in the market?

April 2024: Vedanta Aluminium, India's leading aluminum producer, marked a significant stride in its expansion endeavors, aiming to secure a spot among the top 3 global players. The company, with a current capacity of 3 million tonnes per annum (MTPA), unveiled plans to bolster its vertical integration, a move underscored by the successful launch of a new 1.5 MTPA expansion at its alumina refinery in Lanjigarh, Odisha. This expansion elevates the refinery's capacity from 2 MTPA to 3.5 MTPA. Notably, this 1.5 MTPA increment is just a segment of Vedanta's broader strategy to elevate the Lanjigarh refinery's nameplate capacity from 2 MTPA to 5 MTPA, aligning with its escalating aluminum production demands from a range of industries, including packaging and construction.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Asia Pacific Metal Caps And Closures Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Asia Pacific Metal Caps And Closures Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Asia Pacific Metal Caps And Closures Market?

To stay informed about further developments, trends, and reports in the Asia Pacific Metal Caps And Closures Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence