Key Insights

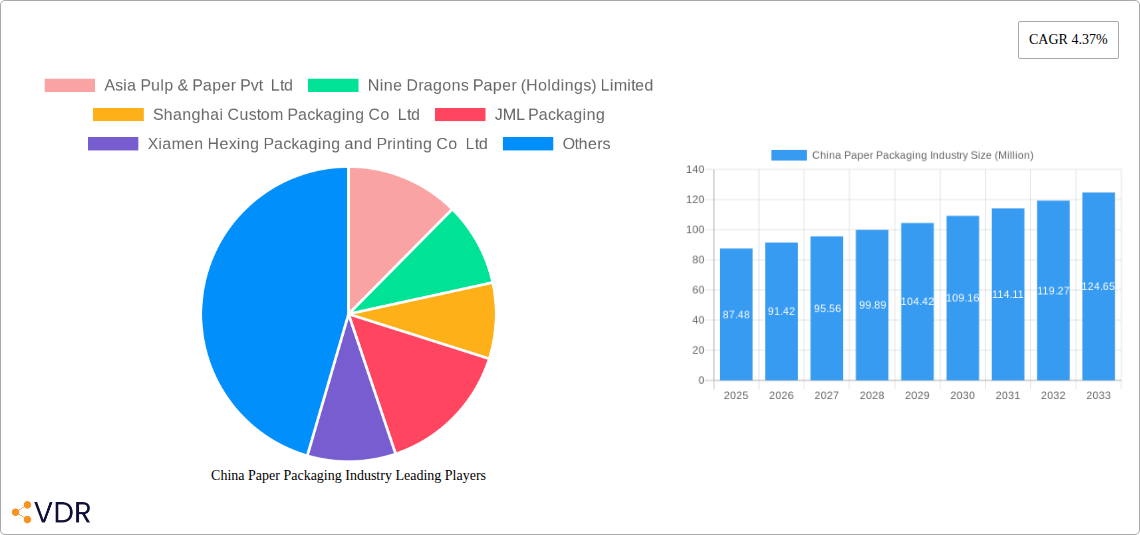

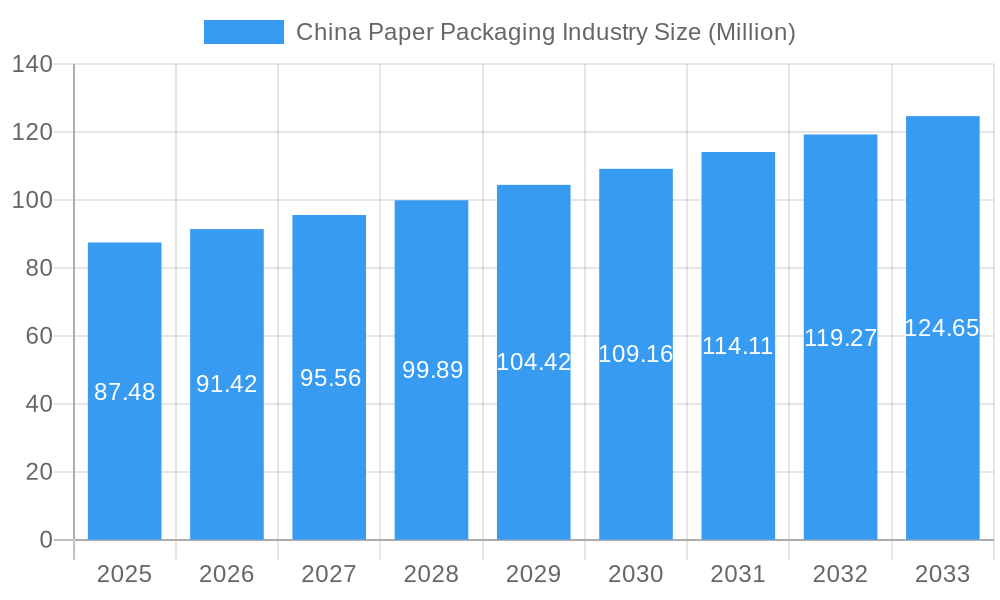

The China paper packaging market, valued at $87.48 million in 2025, is projected to experience robust growth, driven by a burgeoning e-commerce sector fueling demand for corrugated boxes and folding cartons. The rising disposable incomes and changing consumer lifestyles within China contribute significantly to this expansion. The food and beverage industry, a major consumer of paper packaging, is expected to remain a key driver, along with the healthcare and personal care sectors showing increased adoption of sustainable packaging solutions. While increasing raw material costs and environmental regulations pose challenges, technological advancements in printing and packaging design are mitigating these restraints. Segmentation analysis reveals that corrugated boxes hold the largest market share among product types, reflecting their versatility and cost-effectiveness. Key players like Asia Pulp & Paper, Nine Dragons Paper, and Mondi Group are strategically investing in capacity expansion and innovation to meet the growing demand. The forecast period of 2025-2033 anticipates a steady growth trajectory fueled by continued economic expansion and a rising middle class in China, demanding convenient and aesthetically pleasing packaging.

China Paper Packaging Industry Market Size (In Million)

The CAGR of 4.37% indicates a consistent market expansion throughout the forecast period. However, the market will need to navigate evolving consumer preferences towards sustainable and eco-friendly packaging materials. Companies are responding by increasing the use of recycled materials and exploring biodegradable alternatives. Competitive pressures are likely to intensify, demanding continuous innovation in product design and manufacturing processes to maintain market share. Government initiatives promoting sustainable practices will likely play a crucial role in shaping the industry's future trajectory, encouraging investments in environmentally sound packaging solutions. Regional variations within China might also influence market growth, with certain provinces experiencing higher growth rates than others based on economic development and industrial concentration. Overall, the China paper packaging market is poised for continued expansion, presenting significant opportunities for existing and new market entrants.

China Paper Packaging Industry Company Market Share

China Paper Packaging Industry: A Comprehensive Market Report (2019-2033)

This in-depth report provides a comprehensive analysis of the China paper packaging industry, encompassing market dynamics, growth trends, key players, and future outlook. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report offers invaluable insights for industry professionals, investors, and strategic decision-makers. The report segments the market by end-user industry (Food, Beverage, Healthcare, Personal Care, Household Care, Electrical Products, Other End-user Industries) and product type (Folding Cartons, Corrugated Boxes, Other Product Types), providing granular data for informed analysis.

China Paper Packaging Industry Market Dynamics & Structure

The Chinese paper packaging market is a dynamic landscape shaped by several interconnected factors. Market concentration is moderate, with a few dominant players alongside numerous smaller firms. Technological innovation, particularly in sustainable and automated packaging solutions, is a key driver. Stringent environmental regulations are pushing the industry towards eco-friendly materials and processes, creating both challenges and opportunities. The rise of e-commerce fuels demand for efficient packaging, while competitive pressures from substitute materials like plastic remain significant. M&A activity is moderate; xx deals were recorded between 2019 and 2024, with xx% involving international players seeking access to the vast Chinese market. End-user demographics are shifting towards younger, more environmentally conscious consumers, influencing packaging preferences.

- Market Concentration: Moderate, with top 5 players holding xx% market share in 2024.

- Technological Innovation: Focus on automation, sustainable materials (FSC certified paper), and smart packaging solutions.

- Regulatory Framework: Increasingly stringent environmental regulations favoring sustainable packaging.

- Competitive Substitutes: Plastic packaging poses a significant competitive threat.

- M&A Trends: Moderate activity, with xx deals recorded between 2019 and 2024.

China Paper Packaging Industry Growth Trends & Insights

The China paper packaging market experienced significant growth during the historical period (2019-2024), with a CAGR of xx%. This growth is primarily driven by the expanding e-commerce sector, rising consumer spending, and increasing demand from various end-user industries. The market size reached xx million units in 2024 and is projected to reach xx million units by 2033, exhibiting a CAGR of xx% during the forecast period (2025-2033). Technological disruptions, such as the adoption of advanced printing techniques and automation in packaging lines, are further accelerating market growth. Consumer behavior shifts towards sustainable and convenient packaging are influencing product development and market dynamics. Market penetration of sustainable packaging solutions is increasing at xx% annually.

Dominant Regions, Countries, or Segments in China Paper Packaging Industry

The coastal regions of China, particularly Guangdong, Jiangsu, and Zhejiang provinces, dominate the paper packaging market due to their well-established manufacturing bases and proximity to major consumption centers. Within end-user industries, the Food and Beverage sector holds the largest market share (xx%), driven by high demand for packaging solutions for processed foods, beverages, and snacks. The Corrugated Boxes segment leads in terms of product type, accounting for xx% of the market in 2024, due to its widespread use in e-commerce and industrial packaging.

- Key Drivers (Food & Beverage Segment): Rising disposable incomes, changing dietary habits, and growth of the processed food industry.

- Key Drivers (Coastal Regions): Strong industrial infrastructure, access to raw materials, and proximity to major markets.

- Market Share (2024): Food & Beverage (xx%), Corrugated Boxes (xx%).

- Growth Potential: High growth potential is expected in the Healthcare and Personal Care segments, driven by increasing health consciousness and premiumization.

China Paper Packaging Industry Product Landscape

The paper packaging industry in China offers a diverse range of products, including folding cartons, corrugated boxes, and other specialized packaging solutions. Folding cartons are widely used for premium products, emphasizing aesthetics and brand appeal. Corrugated boxes dominate in terms of volume, owing to their strength and cost-effectiveness. Recent innovations focus on eco-friendly materials, such as recycled paper and biodegradable coatings, coupled with advanced printing technologies for enhanced branding and consumer engagement. Smart packaging solutions with embedded sensors and traceability features are also emerging.

Key Drivers, Barriers & Challenges in China Paper Packaging Industry

Key Drivers:

- Rapid growth of e-commerce and online retail.

- Rising demand from various end-user industries.

- Increasing consumer preference for sustainable packaging.

- Government support for the development of eco-friendly industries.

Key Challenges:

- Fluctuations in raw material prices (pulp, paperboard).

- Intense competition from substitute materials (plastics).

- Environmental regulations and sustainability concerns.

- Supply chain disruptions and logistical challenges. These challenges impacted production by an estimated xx% in 2022.

Emerging Opportunities in China Paper Packaging Industry

Emerging opportunities lie in sustainable packaging solutions, including biodegradable and compostable materials. The growing demand for personalized and customized packaging offers significant potential for innovation. Evolving consumer preferences towards convenience and tamper-evident packaging create new product development opportunities. Untapped markets exist in rural areas and smaller cities, where demand for affordable yet quality packaging is increasing.

Growth Accelerators in the China Paper Packaging Industry Industry

Technological advancements in printing and automation are major growth catalysts. Strategic partnerships between packaging companies and brands will facilitate the adoption of innovative packaging solutions. Expansion into new markets, both domestically and internationally, presents significant growth opportunities. The increasing focus on sustainable practices, aligning with government policies, is also a key accelerator.

Key Players Shaping the China Paper Packaging Industry Market

- Asia Pulp & Paper Pvt Ltd

- Nine Dragons Paper (Holdings) Limited

- Shanghai Custom Packaging Co Ltd

- JML Packaging

- Xiamen Hexing Packaging and Printing Co Ltd

- Mondi Group

- Rengo Co Ltd

- SIG Combibloc Group

- Dongguan Vision Paper Products Co Ltd

- Belpa

- Shanghai DE Printed Box

- Suneco Box Co Ltd

Notable Milestones in China Paper Packaging Industry Sector

- December 2023: Mars China launches Snickers bars with FSC-certified paper packaging, signifying a shift towards sustainable materials.

- August 2023: Sichuan Huaqiao Fenghuang Paper installs Voith Group's XcelLine packaging paper machine, boosting production capacity and efficiency.

In-Depth China Paper Packaging Industry Market Outlook

The future of the China paper packaging industry is bright, driven by sustained growth in e-commerce, increasing consumer spending, and a growing emphasis on sustainability. Strategic investments in technology, sustainable materials, and innovative packaging solutions will be crucial for success. The market's long-term potential is significant, offering substantial opportunities for both domestic and international players. The focus on eco-friendly practices and circular economy models will shape the industry's trajectory in the coming years.

China Paper Packaging Industry Segmentation

-

1. Product Type

- 1.1. Folding Cartons

- 1.2. Corrugated Boxes

- 1.3. Other Product Types

-

2. End-user Industry

- 2.1. Food

- 2.2. Beverage

- 2.3. Healthcare

- 2.4. Personal Care

- 2.5. Household Care

- 2.6. Electrical Products

- 2.7. Other End-user Industries

China Paper Packaging Industry Segmentation By Geography

- 1. China

China Paper Packaging Industry Regional Market Share

Geographic Coverage of China Paper Packaging Industry

China Paper Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.37% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Folding Cartons

- 5.1.2. Corrugated Boxes

- 5.1.3. Other Product Types

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Food

- 5.2.2. Beverage

- 5.2.3. Healthcare

- 5.2.4. Personal Care

- 5.2.5. Household Care

- 5.2.6. Electrical Products

- 5.2.7. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. China

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. China Paper Packaging Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Folding Cartons

- 6.1.2. Corrugated Boxes

- 6.1.3. Other Product Types

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Food

- 6.2.2. Beverage

- 6.2.3. Healthcare

- 6.2.4. Personal Care

- 6.2.5. Household Care

- 6.2.6. Electrical Products

- 6.2.7. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Asia Pulp & Paper Pvt Ltd

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Nine Dragons Paper (Holdings) Limited

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Shanghai Custom Packaging Co Ltd

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 JML Packaging

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Xiamen Hexing Packaging and Printing Co Ltd

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Mondi Group

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Rengo Co Ltd

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 SIG Combibloc Group

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Dongguan Vision Paper Products Co Ltd

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Belpa

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Shanghai DE Printed Box

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Suneco Box Co Ltd

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.1 Asia Pulp & Paper Pvt Ltd

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China Paper Packaging Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: China Paper Packaging Industry Share (%) by Company 2025

List of Tables

- Table 1: China Paper Packaging Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 2: China Paper Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 3: China Paper Packaging Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: China Paper Packaging Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 5: China Paper Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 6: China Paper Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Paper Packaging Industry?

The projected CAGR is approximately 4.37%.

2. Which companies are prominent players in the China Paper Packaging Industry?

Key companies in the market include Asia Pulp & Paper Pvt Ltd, Nine Dragons Paper (Holdings) Limited, Shanghai Custom Packaging Co Ltd, JML Packaging, Xiamen Hexing Packaging and Printing Co Ltd, Mondi Group, Rengo Co Ltd, SIG Combibloc Group, Dongguan Vision Paper Products Co Ltd, Belpa, Shanghai DE Printed Box, Suneco Box Co Ltd.

3. What are the main segments of the China Paper Packaging Industry?

The market segments include Product Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 87.48 Million as of 2022.

5. What are some drivers contributing to market growth?

Growth in E-commerce Sales in China; Rising Demand from the Food-service Sector; Growing Consumer Awareness on Paper Packaging; Recycling Initiatives Involving Closed-loop Systems to Aid Market Adoption of Paper Packaging-based Materials.

6. What are the notable trends driving market growth?

Corrugated Boxes Holds Largest Market Share in the Product Type Segment.

7. Are there any restraints impacting market growth?

Recycling. Raw Material Supply Chain Management. and Challenges in the Paper Packaging Industry; Effects of Deforestation on Paper Packaging; Increasing Raw Material Costs and Outsourcing.

8. Can you provide examples of recent developments in the market?

December 2023: Mars China unveiled the launch of the new Snickers low GI dark chocolate cereal bars that use paper for the outer box covering material. The new Snickers bar outer packaging box is made of FSC-certified paper, which would help Mars China reduce its reliance on plastic and promote sustainable forest management.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Paper Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Paper Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Paper Packaging Industry?

To stay informed about further developments, trends, and reports in the China Paper Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence