Key Insights

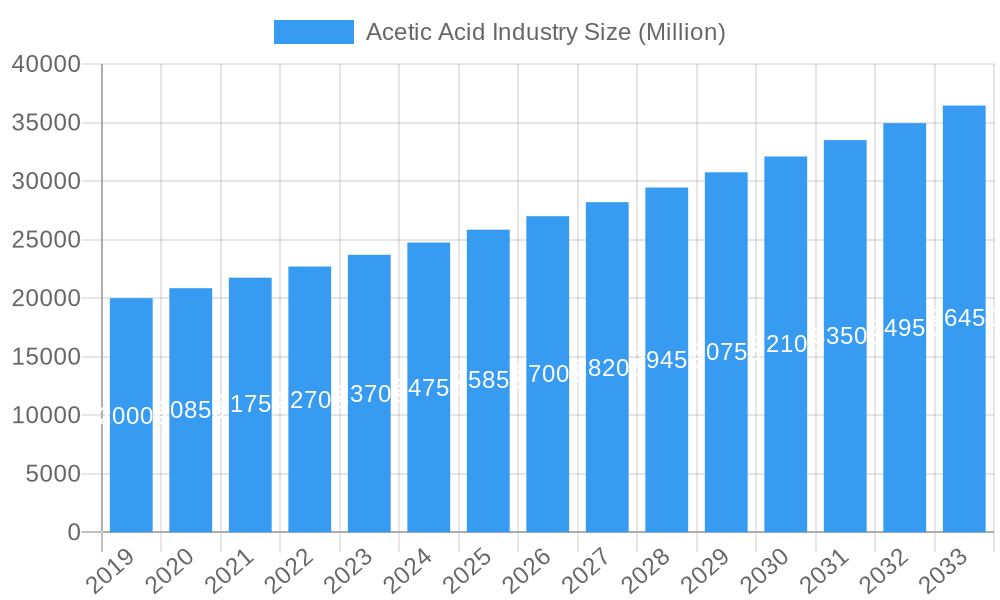

The global Acetic Acid market is projected to reach $2.6 billion by 2025, with an anticipated Compound Annual Growth Rate (CAGR) of 4.56% through 2033. This growth is primarily driven by escalating demand for acetic acid derivatives such as Vinyl Acetate Monomer (VAM) and Purified Terephthalic Acid (PTA), crucial for plastics, polymers, and textile manufacturing. The expanding paints and coatings sector, coupled with the food and beverage industry's sustained use of acetic acid for preservation and flavoring, further strengthens market demand. Medical applications, including pharmaceutical formulations, also contribute to its growing utility. Emerging trends like the development of sustainable bio-based acetic acid production and its increasing adoption in industrializing economies with rising consumer spending are key market shapers.

Acetic Acid Industry Market Size (In Billion)

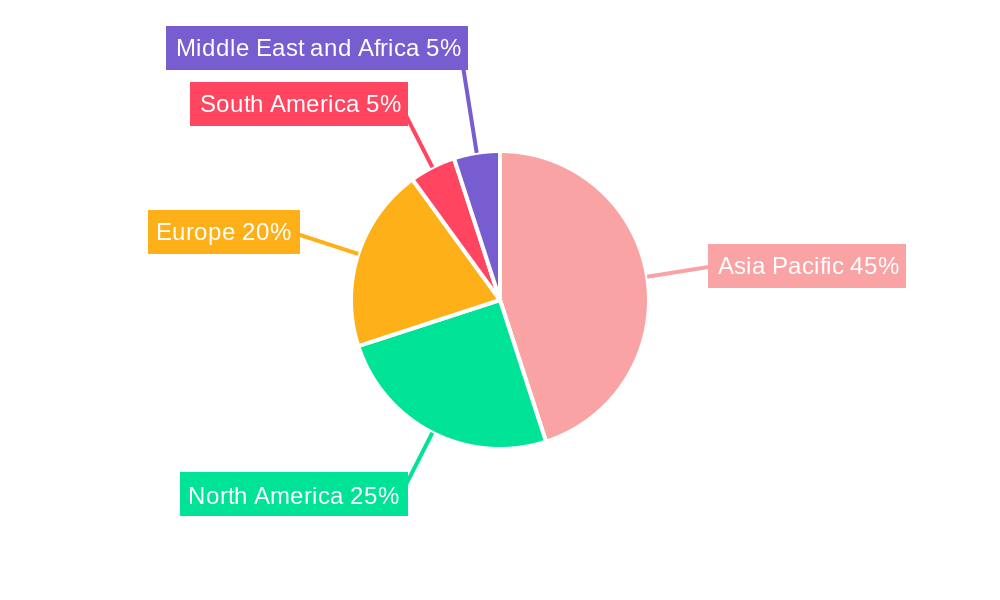

Market challenges include raw material price volatility, particularly for methanol and carbon monoxide, affecting production costs and profitability. Stringent environmental regulations for production and disposal necessitate investment in cleaner technologies. Despite these obstacles, the broad application base and continuous innovation in production and application development forecast a positive market outlook. The Asia Pacific region, led by China and India, is expected to maintain dominance due to rapid industrialization and significant consumption in textiles and plastics. North America and Europe remain significant markets, driven by established industries and a focus on specialty chemical applications.

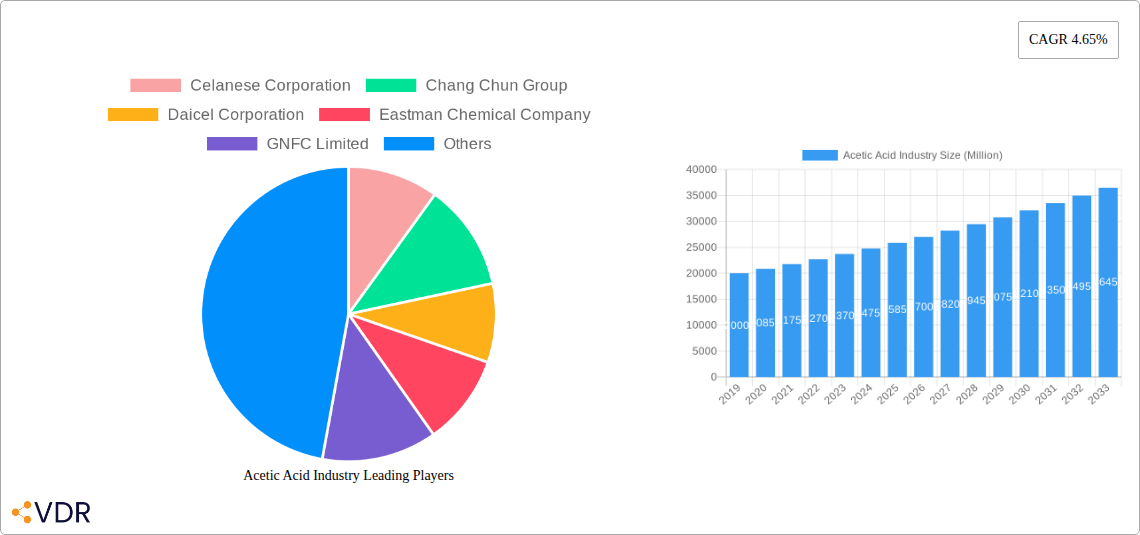

Acetic Acid Industry Company Market Share

Acetic Acid Industry Report: Global Market Analysis & Future Outlook (2019-2033)

This comprehensive report delivers an in-depth analysis of the global Acetic Acid Industry, meticulously examining market dynamics, growth trends, regional dominance, product landscape, and future opportunities. Covering the period from 2019 to 2033, with a base and estimated year of 2025, this report offers invaluable insights for stakeholders seeking to navigate and capitalize on the evolving chemical market. The analysis leverages quantitative data, including market share percentages and CAGR, alongside qualitative factors, to provide a robust understanding of this vital industrial sector. We explore the intricate parent and child market relationships that define the Acetic Acid value chain, from raw material sourcing to diverse end-user applications, ensuring a holistic perspective.

Acetic Acid Industry Market Dynamics & Structure

The global Acetic Acid Industry exhibits a moderately concentrated market structure, with a few key players dominating production. Technological innovation is primarily driven by process optimization for efficiency and sustainability, alongside the development of novel applications. Regulatory frameworks, particularly concerning environmental impact and safety, play a crucial role in shaping market operations and investment decisions. Competitive product substitutes are limited for core acetic acid applications, though alternative production routes for derivatives can introduce indirect competition. End-user demographics are diverse, spanning industrial manufacturing, consumer goods, and agriculture. Merger and acquisition (M&A) trends reflect a strategic consolidation to gain market share, secure feedstock, and expand geographical reach. For instance, recent M&A activities have focused on integrating upstream feedstock capabilities with downstream derivative production to enhance supply chain resilience.

- Market Concentration: Characterized by the presence of leading global chemical manufacturers, with the top 5-7 companies holding a significant market share.

- Technological Innovation Drivers: Focus on cost reduction through catalyst development, energy efficiency improvements, and exploring bio-based acetic acid production.

- Regulatory Frameworks: Stringent environmental regulations (e.g., emissions control, waste management) and chemical safety standards significantly influence operational costs and investment.

- Competitive Product Substitutes: While direct substitutes are rare for acetic acid itself, alternative chemicals can fulfill specific derivative functions in certain applications.

- End-User Demographics: Broad consumer base including industries such as textiles, plastics, adhesives, paints, and food and beverages.

- M&A Trends: Strategic acquisitions to enhance vertical integration, expand product portfolios, and enter high-growth regional markets. The volume of M&A deals in the past five years indicates a trend towards consolidation and market leadership.

Acetic Acid Industry Growth Trends & Insights

The Acetic Acid Industry is projected for robust growth, driven by increasing demand from its diverse application segments and expanding global industrialization. The market size evolution is a testament to the indispensable nature of acetic acid and its derivatives in numerous manufacturing processes. Adoption rates for improved production technologies, focusing on sustainability and cost-effectiveness, are steadily increasing. Technological disruptions, such as the exploration of carbon capture and utilization (CCU) technologies for acetic acid synthesis, are beginning to shape future production paradigms, aiming for lower carbon footprints. Consumer behavior shifts, particularly the growing preference for eco-friendly products, are indirectly influencing the demand for acetic acid derivatives used in sustainable materials and processes.

The global Acetic Acid market is on a steady upward trajectory, with a projected Compound Annual Growth Rate (CAGR) of approximately 4.5% during the forecast period. The market size, valued at an estimated $XX billion in 2025, is expected to reach $XX billion by 2033. This growth is underpinned by the escalating demand from key downstream industries like plastics and polymers, and adhesives, paints, and coatings. Vinyl Acetate Monomer (VAM), a primary derivative, continues to be a major demand driver due to its extensive use in producing polyvinyl acetate (PVA) and polyvinyl alcohol (PVOH), essential for adhesives, textiles, and paper coatings. The increasing focus on sustainable infrastructure projects globally is also bolstering the demand for VAM-based products.

Purified Terephthalic Acid (PTA), another significant derivative, is closely linked to the polyester fiber and PET resin markets. The burgeoning textile industry in emerging economies and the continuous demand for PET packaging solutions for food and beverages are key contributors to PTA’s market penetration. Ethyl Acetate, widely used as a solvent in paints, coatings, and inks, benefits from the expansion of the construction and automotive sectors, which rely heavily on these finishing products. Acetic Anhydride, crucial for cellulose acetate production (used in cigarette filters and textiles) and pharmaceuticals, exhibits stable growth driven by these established applications.

Furthermore, the “Other Derivatives” segment, encompassing products like methyl acetate and specialty esters, is witnessing innovation and niche market growth, catering to specific industrial needs. The shift towards greener solvents and bio-based chemical alternatives also presents an opportunity, although traditional petrochemical routes remain dominant. The adoption of advanced manufacturing techniques, including digitalization and AI-driven process optimization, is enhancing production efficiency and contributing to market growth by reducing operational costs and waste. The report analyzes these trends with granular detail, providing a forward-looking perspective on the Acetic Acid industry's expansion and adaptation to global economic and environmental shifts.

Dominant Regions, Countries, or Segments in Acetic Acid Industry

The global Acetic Acid Industry is significantly influenced by the dominance of Asia-Pacific, particularly China, as a manufacturing hub and a major consumer of chemical products. Within the derivative segments, Vinyl Acetate Monomer (VAM) consistently emerges as the leading driver of market growth. Its extensive application in the production of polymers, adhesives, and coatings positions it at the forefront of industrial demand. The burgeoning construction and automotive industries in emerging economies, coupled with the persistent need for consumer goods that utilize VAM-based products, contribute to its sustained market leadership. Economic policies in these regions, often focused on industrial expansion and infrastructure development, further bolster VAM consumption.

Purified Terephthalic Acid (PTA) is another powerful segment, heavily reliant on the massive textile and packaging industries. The demand for polyester fibers for clothing and home furnishings, alongside the ubiquitous use of PET in beverage bottles and food containers, ensures PTA’s significant market share. Countries with large textile manufacturing bases, such as India and Southeast Asian nations, are key consumption centers for PTA. The growth potential of this segment is directly tied to population growth and rising disposable incomes in these regions, which translate to increased demand for apparel and packaged goods.

Ethyl Acetate finds strong traction in the Paints, and Coatings and Adhesives segments. The global expansion of infrastructure projects, coupled with the automotive industry's continuous need for high-quality finishes, fuels the demand for ethyl acetate as a versatile solvent. The increasing awareness and adoption of water-based and low-VOC (Volatile Organic Compound) coatings are creating new opportunities and driving innovation within this segment, although traditional solvent-based applications remain substantial.

The Textile application segment, directly consuming acetic acid derivatives like acetic anhydride for cellulose acetate production, exhibits steady growth. The demand for acetate fabrics, known for their drape and lustrous appearance, particularly in women's fashion, contributes to this segment's importance. The Medical segment, while smaller in volume, represents a high-value application for acetic acid and its derivatives in pharmaceutical synthesis and sterilization processes, indicating a niche but critical area of growth.

Dominant Derivative: Vinyl Acetate Monomer (VAM):

- Drivers: Extensive use in polyvinyl acetate (PVA) and polyvinyl alcohol (PVOH) for adhesives, textiles, paper coatings, and construction materials.

- Market Share: Holds the largest share among acetic acid derivatives due to its broad application spectrum.

- Growth Potential: Strong growth linked to infrastructure development and consumer goods manufacturing in emerging economies.

Dominant Application: Plastics and Polymers:

- Drivers: Acetic acid is a precursor to key monomers like VAM, essential for polymer production.

- Market Share: A significant end-use market for acetic acid and its derivatives.

- Growth Potential: Aligned with the global demand for plastics in packaging, automotive, and construction sectors.

Key Regional Dominance: Asia-Pacific:

- Drivers: Robust manufacturing capabilities, large consumer base, and supportive government policies in countries like China.

- Market Share: Accounts for the largest share of global acetic acid production and consumption.

- Growth Potential: Continues to be the primary growth engine for the acetic acid industry.

Emerging Application Trends: Increasing demand for acetic acid derivatives in eco-friendly paints and coatings, and sustainable textile manufacturing processes.

Acetic Acid Industry Product Landscape

The Acetic Acid Industry's product landscape is characterized by a range of essential derivatives and direct applications. Vinyl Acetate Monomer (VAM) stands out for its critical role in producing polymers like PVA and PVOH, vital for adhesives, textiles, and paper. Purified Terephthalic Acid (PTA) is indispensable for the polyester industry, driving the production of fibers and PET resins for packaging. Ethyl Acetate serves as a widely used solvent in paints, coatings, and inks, while Acetic Anhydride is crucial for cellulose acetate production in textiles and pharmaceuticals. Innovations focus on improving the purity of these derivatives and developing more sustainable production methods, aligning with global environmental initiatives. The performance metrics of these products are continuously being optimized for enhanced efficiency and reduced environmental impact in their respective application areas.

Key Drivers, Barriers & Challenges in Acetic Acid Industry

The Acetic Acid Industry is propelled by several key drivers. The fundamental and growing demand for its derivatives across plastics, polymers, textiles, and adhesives fuels its expansion. Technological advancements in production processes, leading to increased efficiency and cost-effectiveness, are also significant catalysts. Government initiatives promoting industrial growth and infrastructure development in emerging economies further boost demand.

However, the industry faces notable barriers and challenges. Fluctuations in the prices of key raw materials, particularly methanol and natural gas, can impact profitability. Stringent environmental regulations concerning emissions and waste disposal necessitate significant capital investment in compliance technologies. Supply chain disruptions, exacerbated by geopolitical events, can affect the availability and cost of raw materials and finished products. Intense competition among global players also puts pressure on profit margins.

Key Drivers:

- Robust Demand from Downstream Industries: Essential for plastics, polymers, textiles, adhesives, and food industries.

- Technological Advancements: Improved production efficiency, catalyst development, and process optimization.

- Growing Industrialization in Emerging Economies: Increased manufacturing and infrastructure development.

Barriers & Challenges:

- Raw Material Price Volatility: Dependence on methanol and natural gas markets.

- Stringent Environmental Regulations: Increased operational costs and compliance requirements.

- Supply Chain Vulnerabilities: Risks associated with global logistics and geopolitical stability.

- Intense Market Competition: Pressure on pricing and margins.

Emerging Opportunities in Acetic Acid Industry

Emerging opportunities in the Acetic Acid Industry lie in the increasing demand for bio-based and sustainable acetic acid production routes, driven by growing environmental consciousness and regulatory pressures. The development of novel applications for acetic acid derivatives in high-performance materials and specialty chemicals presents a significant growth avenue. Furthermore, the expansion of the pharmaceutical and medical sectors continues to create opportunities for high-purity acetic acid and its derivatives. Untapped markets in developing regions with rapidly industrializing economies also offer substantial potential for market penetration and growth.

Growth Accelerators in the Acetic Acid Industry Industry

Several factors are accelerating the growth of the Acetic Acid Industry. Technological breakthroughs in catalysis and process engineering are leading to more efficient and environmentally friendly production methods, reducing costs and enhancing competitiveness. Strategic partnerships and joint ventures between established chemical companies and emerging players are fostering innovation and market expansion. The increasing adoption of digital technologies for supply chain management and production optimization is also contributing to operational efficiency and market responsiveness. Furthermore, targeted investments in high-growth application segments, such as biodegradable polymers and advanced adhesives, are opening new avenues for market expansion.

Key Players Shaping the Acetic Acid Industry Market

- Celanese Corporation

- Chang Chun Group

- Daicel Corporation

- Eastman Chemical Company

- GNFC Limited

- INEOS

- Jiangsu SOPO (Group) Co Ltd

- Kingboard Holdings Limited

- LyondellBasell Industries Holdings BV

- Mitsubishi Chemical Corporation

- PetroChina Company Limited

- Sabic

- Shandong Hualu-Hengsheng Chemical Co Ltd

- Shanghai Huayi Holding Group Co Ltd

- Sipchem Company

- Svensk Etanolkemi AB (SEKAB)

- Tanfac Industries Ltd

- Yankuang Group

Notable Milestones in Acetic Acid Industry Sector

- January 2023: Kingboard Holdings Limited announced that its unit, Hebei Kingboard Energy Development Co., Ltd., plans to submit the "Environmental Impact Report of Hebei Kingboard Energy Development Co., Ltd. Acetic Acid Expansion and Transformation Project" for approval, signaling a commitment to capacity expansion and process improvement.

- June 2022: Hebei Kingboard Energy Development Co., Ltd. announced the commencement of construction for an acetic acid facility with a capacity of 29,80 tons per year. This CNY 23.20 billion (USD 3.6 billion) project, integrated with a 35,20 tons/year carbon capture and recycling initiative, aims to establish a high-value-added carbon neutrality demonstration park for innovative chemical materials and promote low-carbon development.

In-Depth Acetic Acid Industry Market Outlook

The future of the Acetic Acid Industry is marked by sustained growth and strategic evolution. Driven by the persistent demand from its core applications, the market is poised for further expansion, particularly in rapidly developing regions. Innovations in sustainable production technologies, including bio-based routes and advanced carbon capture, are expected to reshape the industry's environmental footprint and offer new competitive advantages. Strategic investments in research and development for novel derivative applications in high-growth sectors such as advanced materials, pharmaceuticals, and sustainable packaging will be crucial for unlocking future market potential. Collaborations and partnerships will play a pivotal role in navigating complex regulatory landscapes and achieving economies of scale, ensuring a resilient and prosperous future for the Acetic Acid industry.

Acetic Acid Industry Segmentation

-

1. Derivative

- 1.1. Vinyl Acetate Monomer (VAM)

- 1.2. Purified Terephthalic Acid (PTA)

- 1.3. Ethyl Acetate

- 1.4. Acetic Anhydride

- 1.5. Other Derivatives

-

2. Application

- 2.1. Plastics and Polymers

- 2.2. Food and Beverage

- 2.3. Adhesives, Paints, and Coatings

- 2.4. Textile

- 2.5. Medical

- 2.6. Other Applications

Acetic Acid Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. Italy

- 3.4. France

- 3.5. Rest of Europe

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. Saudi Arabia

- 5.2. South Africa

- 5.3. Rest of Middle East and Africa

Acetic Acid Industry Regional Market Share

Geographic Coverage of Acetic Acid Industry

Acetic Acid Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.56% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Derivative

- 5.1.1. Vinyl Acetate Monomer (VAM)

- 5.1.2. Purified Terephthalic Acid (PTA)

- 5.1.3. Ethyl Acetate

- 5.1.4. Acetic Anhydride

- 5.1.5. Other Derivatives

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Plastics and Polymers

- 5.2.2. Food and Beverage

- 5.2.3. Adhesives, Paints, and Coatings

- 5.2.4. Textile

- 5.2.5. Medical

- 5.2.6. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Asia Pacific

- 5.3.2. North America

- 5.3.3. Europe

- 5.3.4. South America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Derivative

- 6. Global Acetic Acid Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Derivative

- 6.1.1. Vinyl Acetate Monomer (VAM)

- 6.1.2. Purified Terephthalic Acid (PTA)

- 6.1.3. Ethyl Acetate

- 6.1.4. Acetic Anhydride

- 6.1.5. Other Derivatives

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Plastics and Polymers

- 6.2.2. Food and Beverage

- 6.2.3. Adhesives, Paints, and Coatings

- 6.2.4. Textile

- 6.2.5. Medical

- 6.2.6. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Derivative

- 7. Asia Pacific Acetic Acid Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Derivative

- 7.1.1. Vinyl Acetate Monomer (VAM)

- 7.1.2. Purified Terephthalic Acid (PTA)

- 7.1.3. Ethyl Acetate

- 7.1.4. Acetic Anhydride

- 7.1.5. Other Derivatives

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Plastics and Polymers

- 7.2.2. Food and Beverage

- 7.2.3. Adhesives, Paints, and Coatings

- 7.2.4. Textile

- 7.2.5. Medical

- 7.2.6. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by Derivative

- 8. North America Acetic Acid Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Derivative

- 8.1.1. Vinyl Acetate Monomer (VAM)

- 8.1.2. Purified Terephthalic Acid (PTA)

- 8.1.3. Ethyl Acetate

- 8.1.4. Acetic Anhydride

- 8.1.5. Other Derivatives

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Plastics and Polymers

- 8.2.2. Food and Beverage

- 8.2.3. Adhesives, Paints, and Coatings

- 8.2.4. Textile

- 8.2.5. Medical

- 8.2.6. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by Derivative

- 9. Europe Acetic Acid Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Derivative

- 9.1.1. Vinyl Acetate Monomer (VAM)

- 9.1.2. Purified Terephthalic Acid (PTA)

- 9.1.3. Ethyl Acetate

- 9.1.4. Acetic Anhydride

- 9.1.5. Other Derivatives

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Plastics and Polymers

- 9.2.2. Food and Beverage

- 9.2.3. Adhesives, Paints, and Coatings

- 9.2.4. Textile

- 9.2.5. Medical

- 9.2.6. Other Applications

- 9.1. Market Analysis, Insights and Forecast - by Derivative

- 10. South America Acetic Acid Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Derivative

- 10.1.1. Vinyl Acetate Monomer (VAM)

- 10.1.2. Purified Terephthalic Acid (PTA)

- 10.1.3. Ethyl Acetate

- 10.1.4. Acetic Anhydride

- 10.1.5. Other Derivatives

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Plastics and Polymers

- 10.2.2. Food and Beverage

- 10.2.3. Adhesives, Paints, and Coatings

- 10.2.4. Textile

- 10.2.5. Medical

- 10.2.6. Other Applications

- 10.1. Market Analysis, Insights and Forecast - by Derivative

- 11. Middle East and Africa Acetic Acid Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Derivative

- 11.1.1. Vinyl Acetate Monomer (VAM)

- 11.1.2. Purified Terephthalic Acid (PTA)

- 11.1.3. Ethyl Acetate

- 11.1.4. Acetic Anhydride

- 11.1.5. Other Derivatives

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Plastics and Polymers

- 11.2.2. Food and Beverage

- 11.2.3. Adhesives, Paints, and Coatings

- 11.2.4. Textile

- 11.2.5. Medical

- 11.2.6. Other Applications

- 11.1. Market Analysis, Insights and Forecast - by Derivative

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Celanese Corporation

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Chang Chun Group

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Daicel Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Eastman Chemical Company

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 GNFC Limited

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 INEOS

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Jiangsu SOPO (Group) Co Ltd

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Kingboard Holdings Limited

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 LyondellBasell Industries Holdings BV

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Mitsubishi Chemical Corporation

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 PetroChina Company Limited

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Sabic

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Shandong Hualu-Hengsheng Chemical Co Ltd

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Shanghai Huayi Holding Group Co Ltd

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Sipchem Company

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Svensk Etanolkemi AB (SEKAB)

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Tanfac Industries Ltd

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 Yankuang Group*List Not Exhaustive

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.1 Celanese Corporation

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Acetic Acid Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Asia Pacific Acetic Acid Industry Revenue (billion), by Derivative 2025 & 2033

- Figure 3: Asia Pacific Acetic Acid Industry Revenue Share (%), by Derivative 2025 & 2033

- Figure 4: Asia Pacific Acetic Acid Industry Revenue (billion), by Application 2025 & 2033

- Figure 5: Asia Pacific Acetic Acid Industry Revenue Share (%), by Application 2025 & 2033

- Figure 6: Asia Pacific Acetic Acid Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: Asia Pacific Acetic Acid Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: North America Acetic Acid Industry Revenue (billion), by Derivative 2025 & 2033

- Figure 9: North America Acetic Acid Industry Revenue Share (%), by Derivative 2025 & 2033

- Figure 10: North America Acetic Acid Industry Revenue (billion), by Application 2025 & 2033

- Figure 11: North America Acetic Acid Industry Revenue Share (%), by Application 2025 & 2033

- Figure 12: North America Acetic Acid Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: North America Acetic Acid Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Acetic Acid Industry Revenue (billion), by Derivative 2025 & 2033

- Figure 15: Europe Acetic Acid Industry Revenue Share (%), by Derivative 2025 & 2033

- Figure 16: Europe Acetic Acid Industry Revenue (billion), by Application 2025 & 2033

- Figure 17: Europe Acetic Acid Industry Revenue Share (%), by Application 2025 & 2033

- Figure 18: Europe Acetic Acid Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Acetic Acid Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: South America Acetic Acid Industry Revenue (billion), by Derivative 2025 & 2033

- Figure 21: South America Acetic Acid Industry Revenue Share (%), by Derivative 2025 & 2033

- Figure 22: South America Acetic Acid Industry Revenue (billion), by Application 2025 & 2033

- Figure 23: South America Acetic Acid Industry Revenue Share (%), by Application 2025 & 2033

- Figure 24: South America Acetic Acid Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: South America Acetic Acid Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Acetic Acid Industry Revenue (billion), by Derivative 2025 & 2033

- Figure 27: Middle East and Africa Acetic Acid Industry Revenue Share (%), by Derivative 2025 & 2033

- Figure 28: Middle East and Africa Acetic Acid Industry Revenue (billion), by Application 2025 & 2033

- Figure 29: Middle East and Africa Acetic Acid Industry Revenue Share (%), by Application 2025 & 2033

- Figure 30: Middle East and Africa Acetic Acid Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Middle East and Africa Acetic Acid Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Acetic Acid Industry Revenue billion Forecast, by Derivative 2020 & 2033

- Table 2: Global Acetic Acid Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 3: Global Acetic Acid Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Acetic Acid Industry Revenue billion Forecast, by Derivative 2020 & 2033

- Table 5: Global Acetic Acid Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 6: Global Acetic Acid Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: China Acetic Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: India Acetic Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Japan Acetic Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: South Korea Acetic Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Rest of Asia Pacific Acetic Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Global Acetic Acid Industry Revenue billion Forecast, by Derivative 2020 & 2033

- Table 13: Global Acetic Acid Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 14: Global Acetic Acid Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 15: United States Acetic Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada Acetic Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Mexico Acetic Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Global Acetic Acid Industry Revenue billion Forecast, by Derivative 2020 & 2033

- Table 19: Global Acetic Acid Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 20: Global Acetic Acid Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 21: Germany Acetic Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: United Kingdom Acetic Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Italy Acetic Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: France Acetic Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Rest of Europe Acetic Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Global Acetic Acid Industry Revenue billion Forecast, by Derivative 2020 & 2033

- Table 27: Global Acetic Acid Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 28: Global Acetic Acid Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 29: Brazil Acetic Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Argentina Acetic Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Rest of South America Acetic Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Global Acetic Acid Industry Revenue billion Forecast, by Derivative 2020 & 2033

- Table 33: Global Acetic Acid Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 34: Global Acetic Acid Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 35: Saudi Arabia Acetic Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: South Africa Acetic Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Rest of Middle East and Africa Acetic Acid Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Acetic Acid Industry?

The projected CAGR is approximately 4.56%.

2. Which companies are prominent players in the Acetic Acid Industry?

Key companies in the market include Celanese Corporation, Chang Chun Group, Daicel Corporation, Eastman Chemical Company, GNFC Limited, INEOS, Jiangsu SOPO (Group) Co Ltd, Kingboard Holdings Limited, LyondellBasell Industries Holdings BV, Mitsubishi Chemical Corporation, PetroChina Company Limited, Sabic, Shandong Hualu-Hengsheng Chemical Co Ltd, Shanghai Huayi Holding Group Co Ltd, Sipchem Company, Svensk Etanolkemi AB (SEKAB), Tanfac Industries Ltd, Yankuang Group*List Not Exhaustive.

3. What are the main segments of the Acetic Acid Industry?

The market segments include Derivative, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.6 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Vinyl Acetate Monomer (VAM); Increasing Demand from the Textile and Packaging Industry; Increasing Use of Ester Solvents in the Paints and Coating Industry.

6. What are the notable trends driving market growth?

Increasing Applications in the Adhesives. Paints. and Coatings Industry.

7. Are there any restraints impacting market growth?

Increasing Demand for Vinyl Acetate Monomer (VAM); Increasing Demand from the Textile and Packaging Industry; Increasing Use of Ester Solvents in the Paints and Coating Industry.

8. Can you provide examples of recent developments in the market?

January 2023: Kingboard Holdings Limited announced that the company's unit, Hebei Kingboard Energy Development Co., Ltd., plans to submit the "Environmental Impact Report of Hebei Kingboard Energy Development Co., Ltd. Acetic Acid Expansion and Transformation Project" for approval, and the entire content of the environmental impact study is accessible.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Acetic Acid Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Acetic Acid Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Acetic Acid Industry?

To stay informed about further developments, trends, and reports in the Acetic Acid Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence