Key Insights

The European bioplastics market is projected for substantial growth, anticipated to reach $0.67 million by 2025, with a Compound Annual Growth Rate (CAGR) of 17.96% through 2033. This expansion is driven by heightened consumer environmental awareness and supportive regulatory policies advocating for sustainable materials. Key growth factors include rising demand for eco-friendly packaging, especially in flexible and rigid applications, where bioplastics offer a compelling alternative to petroleum-based plastics. The automotive industry's focus on reducing its carbon footprint, coupled with expanding uses in agriculture and horticulture, presents significant market opportunities. Product innovations, notably in Polylactic Acid (PLA) and Polyhydroxyalkanoates (PHA), are improving performance and cost-competitiveness.

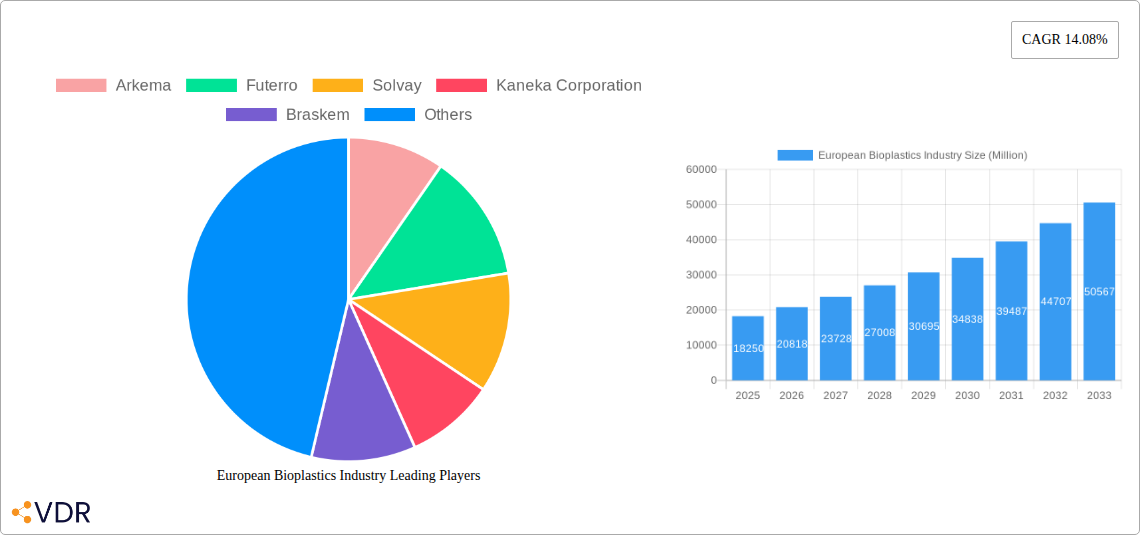

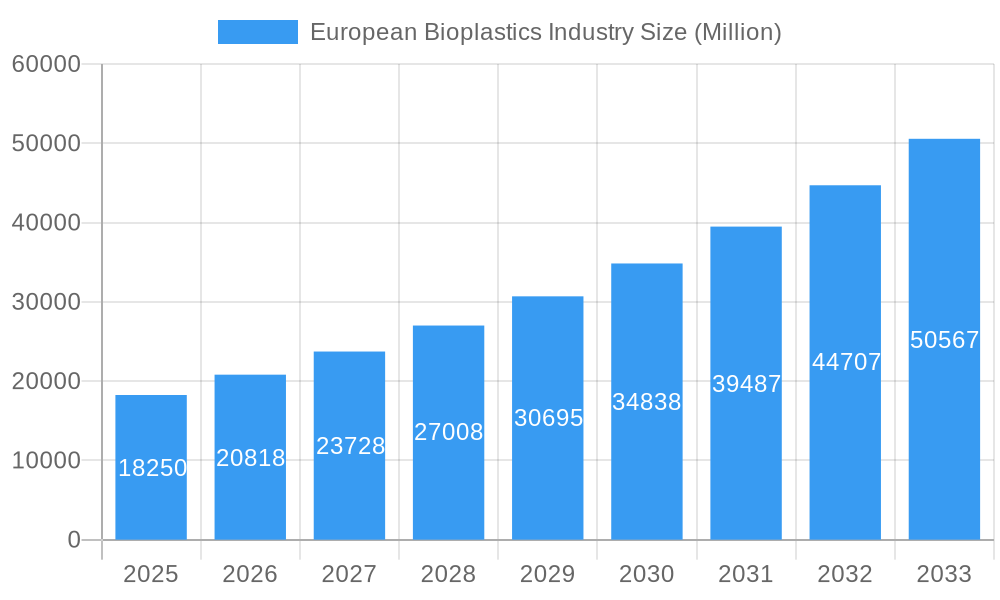

European Bioplastics Industry Market Size (In Million)

Challenges include the initial higher production costs for certain bioplastics and the requirement for comprehensive composting infrastructure for biodegradable variants. However, the shift towards a circular economy and the development of bio-based non-biodegradable alternatives, such as bio-polyethylene terephthalate, are mitigating these issues. Leading companies are investing in R&D, capacity expansion, and strategic collaborations to accelerate market penetration. Europe's strong environmental policies and consumer preference for sustainable products position it as a leading market.

European Bioplastics Industry Company Market Share

Unlocking the Future of Sustainable Materials: European Bioplastics Industry Market Report 2019-2033

Dive deep into the dynamic European Bioplastics Industry with our comprehensive market report. Explore growth trajectories, key players, and transformative innovations driving the shift towards sustainable polymers. This report is your definitive guide to understanding the parent and child markets, from raw material sourcing to end-use applications, providing critical insights for strategic decision-making.

European Bioplastics Industry Market Dynamics & Structure

The European bioplastics market is characterized by a growing but still moderately concentrated landscape, driven by increasing regulatory pressure for sustainable alternatives and significant technological advancements in polymer science. Innovation remains a critical differentiator, with a focus on improving biodegradability, performance, and cost-effectiveness of bio-based materials. Key drivers include ambitious EU targets for plastic reduction and circular economy principles, which foster investment in research and development. However, barriers such as the higher cost of some bioplastics compared to conventional petrochemicals and the need for improved end-of-life infrastructure present ongoing challenges. Competitive product substitutes from both conventional plastics and other emerging materials necessitate continuous innovation and strategic market positioning. End-user demographics are increasingly influenced by consumer demand for eco-friendly products, particularly in packaging and consumer goods. Merger and acquisition (M&A) trends are anticipated to accelerate as larger chemical companies seek to bolster their sustainable portfolios and smaller innovators aim for scalability.

- Market Concentration: Moderate, with key players establishing significant footholds.

- Technological Innovation: Driven by material science advancements in biodegradability and performance.

- Regulatory Frameworks: Strong push from EU policies promoting circularity and waste reduction.

- Competitive Substitutes: Ongoing competition from conventional plastics and advanced recycling technologies.

- End-User Demographics: Growing consumer preference for sustainable products impacting purchasing decisions.

- M&A Trends: Expected to increase as companies consolidate their positions and expand capabilities.

European Bioplastics Industry Growth Trends & Insights

The European bioplastics industry is poised for substantial expansion, driven by a confluence of evolving consumer consciousness, stringent environmental regulations, and continuous technological innovation. This report leverages extensive data to present a 600-word analysis of market size evolution, adoption rates, technological disruptions, and shifts in consumer behavior. The market is witnessing an accelerated growth trajectory, with projected Compound Annual Growth Rates (CAGRs) indicating a significant increase in market penetration across various applications. Technological advancements are not only improving the performance characteristics of bioplastics but also driving down production costs, making them increasingly competitive with traditional petroleum-based polymers. Consumer demand for sustainable products is a powerful catalyst, compelling manufacturers and brands to integrate bioplastic solutions into their product offerings. This shift is further amplified by corporate sustainability initiatives and a growing awareness of the environmental impact of single-use plastics. The industry's ability to innovate, particularly in developing high-performance biodegradable materials and scalable bio-based non-biodegradable alternatives, will be crucial in capturing market share. Furthermore, the development of robust collection and composting infrastructure will play a pivotal role in realizing the full potential of biodegradable bioplastics, thereby enhancing their adoption rates and contributing to a more circular economy. The forecast period is expected to be a transformative era, where bioplastics transition from niche alternatives to mainstream materials across diverse sectors.

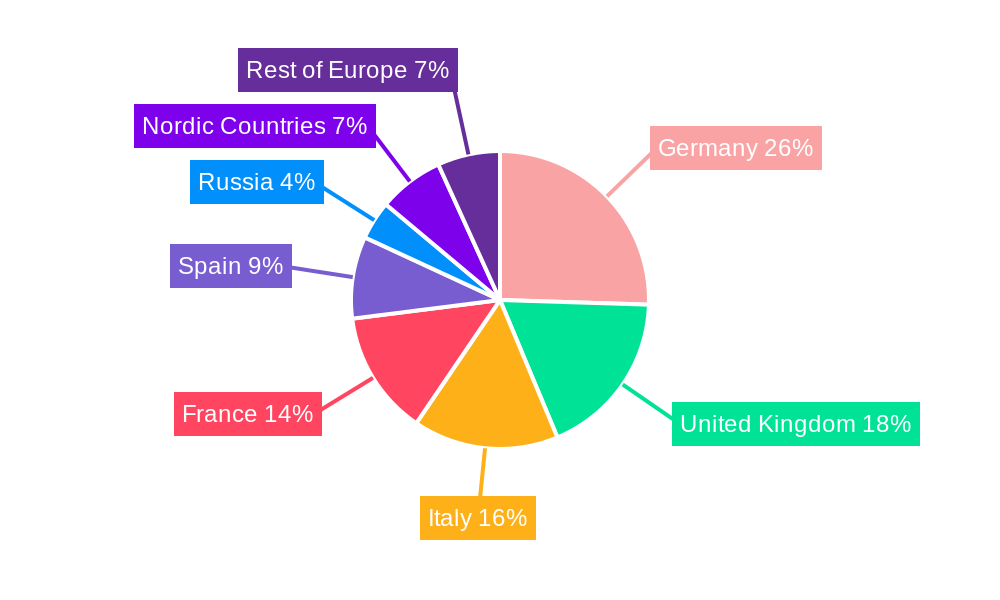

Dominant Regions, Countries, or Segments in European Bioplastics Industry

Within the European bioplastics industry, Germany emerges as a dominant force, leading in both production capacity and market adoption. This leadership is underpinned by a robust industrial base, strong government support for sustainable technologies, and a highly consumer-conscious market demanding eco-friendly products. The Bio-based Biodegradables segment, particularly Polylactic Acid (PLA) and Polyester (PBS, PBAT, and PCL), is experiencing significant growth, driven by their widespread application in flexible and rigid packaging, as well as in agriculture and horticulture. The increasing demand for compostable packaging solutions, spurred by stringent waste management regulations, directly fuels the expansion of these biodegradable categories.

- Germany's Leadership: Supported by proactive environmental policies, substantial R&D investments, and a strong domestic market for sustainable goods.

- Dominant Product Type: Bio-based Biodegradables, with PLA and PBS/PBAT/PCL leading due to their versatility in packaging and agricultural films.

- Key Application Drivers:

- Flexible Packaging: Consumer goods, food, and beverage packaging are major adopters due to sustainability demands.

- Rigid Packaging: Growth in reusable and compostable containers for food and cosmetics.

- Agriculture and Horticulture: Biodegradable mulch films and planters contributing to reduced soil contamination.

- Regulatory Influence: EU directives on single-use plastics and waste reduction are creating a favorable environment for biodegradable bioplastics.

- Technological Advancements: Innovations in PLA production and the development of higher-performance PBAT formulations are expanding application possibilities.

- Market Share: Germany holds a significant share of the European bioplastics market, followed by France and Italy.

- Growth Potential: High growth potential is observed in countries with ambitious sustainability targets and strong consumer engagement, such as the Netherlands and Scandinavian nations.

The Bio-based Non-biodegradables segment, especially Bio-polyethylene Terephthalate (Bio-PET), also shows considerable traction, particularly for applications where durability and recyclability are paramount, such as beverage bottles and automotive components. The integration of bio-based feedstocks into existing polymer chains allows for a "drop-in" solution that leverages established recycling infrastructure, presenting a compelling value proposition.

European Bioplastics Industry Product Landscape

The European bioplastics industry is showcasing a vibrant product landscape characterized by continuous innovation in both bio-based biodegradable and non-biodegradable polymers. Polylactic Acid (PLA) remains a cornerstone, offering excellent transparency and printability for packaging, while Polyhydroxyalkanoates (PHA) are gaining traction for their enhanced biodegradability in diverse environments and superior barrier properties in specialized films. Among bio-based non-biodegradables, Bio-PET and bio-polyamides are increasingly sought after for their performance parity with conventional counterparts, enabling sustainable solutions in demanding sectors like automotive and electronics. Performance metrics such as tensile strength, heat resistance, and moisture barrier capabilities are steadily improving through advanced polymerization techniques and additive technologies, making bioplastics viable for an expanding range of applications. The focus on sustainable sourcing of feedstocks and the development of novel bio-based monomers are key differentiators driving adoption and expanding the product portfolio to meet diverse industry needs.

Key Drivers, Barriers & Challenges in European Bioplastics Industry

The European bioplastics industry is propelled by strong drivers including increasing environmental awareness and consumer demand for sustainable products, stringent government regulations promoting circular economy principles and plastic waste reduction, and ongoing technological advancements leading to improved material performance and cost-competitiveness.

- Drivers:

- Consumer demand for eco-friendly alternatives.

- Supportive EU policies and regulations on sustainability and waste management.

- Technological innovation in material science and production processes.

- Corporate sustainability goals and brand commitments.

Conversely, significant barriers and challenges persist. These include the higher production costs of some bioplastics compared to their petrochemical counterparts, the need for enhanced end-of-life infrastructure for proper disposal and industrial composting, and potential competition from advanced recycling technologies for conventional plastics. Supply chain complexities and feedstock availability can also pose challenges.

- Barriers & Challenges:

- Higher cost of production for certain bioplastics.

- Inadequate collection and composting infrastructure.

- Feedstock availability and land use concerns.

- Competition from conventional plastics and advanced recycling.

- Consumer confusion regarding biodegradability and compostability.

Emerging Opportunities in European Bioplastics Industry

Emerging opportunities in the European bioplastics industry are predominantly centered around the development of high-performance, fully compostable materials for challenging applications, such as medical devices and advanced food packaging with extended shelf life. The growing focus on a truly circular economy is spurring innovation in bio-based materials that are not only compostable but also designed for easier integration into existing recycling streams. Untapped markets in the textiles and electronics sectors, driven by brand commitments to reduce their environmental footprint, represent significant growth potential. Furthermore, evolving consumer preferences for transparency in product origin and sustainability credentials are creating a demand for certified bio-based and biodegradable materials, offering a premium market segment. The increasing investment in research and development for novel bio-monomers and bio-polymers with enhanced properties will continue to unlock new application areas and drive market expansion.

Growth Accelerators in the European Bioplastics Industry Industry

The long-term growth of the European bioplastics industry is being significantly accelerated by breakthroughs in enzyme-based recycling technologies that can efficiently break down and regenerate bioplastic materials. Strategic partnerships between chemical manufacturers, end-users, and waste management companies are crucial for developing robust collection and composting infrastructure, thereby increasing the practical viability of biodegradable bioplastics. Market expansion strategies focused on educating consumers and businesses about the benefits and proper disposal of bioplastics will further drive adoption. Investment in scaling up production capacities for key biopolymers like PLA and PHA, coupled with policy support for bio-based materials, are also critical accelerators, making these sustainable alternatives more accessible and economically attractive across a wider range of industries.

Key Players Shaping the European Bioplastics Industry Market

- Arkema

- Futerro

- Solvay

- Kaneka Corporation

- Braskem

- Mitsubishi Chemical Corporation

- Maccaferri Industrial Group

- Corbion

- BASF SE

- Toray International Inc

- Trinseo

- Dow

- Novamont SpA

- Natureworks LLC

- Danimer Scientific

Notable Milestones in European Bioplastics Industry Sector

- February 2022: Carbios and Indorama Ventures announced their partnership for bio-recycled PET in France with a processing capacity estimated at 50,000 tons.

In-Depth European Bioplastics Industry Market Outlook

The future outlook for the European bioplastics industry is exceptionally promising, driven by a synergistic combination of innovation, policy, and market demand. Growth accelerators such as advanced enzymatic recycling technologies and the increasing focus on a circular economy will foster a more sustainable lifecycle for bioplastic materials. Strategic collaborations are vital for establishing comprehensive end-of-life solutions, including improved collection systems and industrial composting facilities, which are critical for the widespread adoption of biodegradable variants. As production capacities for key biopolymers expand and supportive policies continue to be implemented, bioplastics will become increasingly competitive and accessible for diverse industrial applications. This will not only solidify their position as viable alternatives to conventional plastics but also open new avenues for growth in sectors actively seeking to reduce their environmental impact and enhance their sustainability credentials.

European Bioplastics Industry Segmentation

-

1. Product Type

-

1.1. Bio-based Biodegradables

- 1.1.1. Starch-based

- 1.1.2. Polylactic Acid (PLA)

- 1.1.3. Polyhydroxyalkanoates (PHA)

- 1.1.4. Polyester (PBS, PBAT, and PCL)

- 1.1.5. Other Bio-based Biodegradables

-

1.2. Bio-based Non-biodegradables

- 1.2.1. Bio-polyethylene Terephthalate

- 1.2.2. Bio-polyamides

- 1.2.3. Bio-polytrimethylene Terephthalate

- 1.2.4. Other Bio-based Non-biodegradables

-

1.1. Bio-based Biodegradables

-

2. Application

- 2.1. Flexible Packaging

- 2.2. Rigid Packaging

- 2.3. Automotive and Assembly Operations

- 2.4. Agriculture and Horticulture

- 2.5. Construction

- 2.6. Textiles

- 2.7. Electrical and Electronics

- 2.8. Other Applications

European Bioplastics Industry Segmentation By Geography

- 1. Germany

- 2. United Kingdom

- 3. Italy

- 4. France

- 5. Spain

- 6. Russia

- 7. Nordic Countries

- 8. Rest of Europe

European Bioplastics Industry Regional Market Share

Geographic Coverage of European Bioplastics Industry

European Bioplastics Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 17.98% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Bio-based Biodegradables

- 5.1.1.1. Starch-based

- 5.1.1.2. Polylactic Acid (PLA)

- 5.1.1.3. Polyhydroxyalkanoates (PHA)

- 5.1.1.4. Polyester (PBS, PBAT, and PCL)

- 5.1.1.5. Other Bio-based Biodegradables

- 5.1.2. Bio-based Non-biodegradables

- 5.1.2.1. Bio-polyethylene Terephthalate

- 5.1.2.2. Bio-polyamides

- 5.1.2.3. Bio-polytrimethylene Terephthalate

- 5.1.2.4. Other Bio-based Non-biodegradables

- 5.1.1. Bio-based Biodegradables

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Flexible Packaging

- 5.2.2. Rigid Packaging

- 5.2.3. Automotive and Assembly Operations

- 5.2.4. Agriculture and Horticulture

- 5.2.5. Construction

- 5.2.6. Textiles

- 5.2.7. Electrical and Electronics

- 5.2.8. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Germany

- 5.3.2. United Kingdom

- 5.3.3. Italy

- 5.3.4. France

- 5.3.5. Spain

- 5.3.6. Russia

- 5.3.7. Nordic Countries

- 5.3.8. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. European Bioplastics Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Bio-based Biodegradables

- 6.1.1.1. Starch-based

- 6.1.1.2. Polylactic Acid (PLA)

- 6.1.1.3. Polyhydroxyalkanoates (PHA)

- 6.1.1.4. Polyester (PBS, PBAT, and PCL)

- 6.1.1.5. Other Bio-based Biodegradables

- 6.1.2. Bio-based Non-biodegradables

- 6.1.2.1. Bio-polyethylene Terephthalate

- 6.1.2.2. Bio-polyamides

- 6.1.2.3. Bio-polytrimethylene Terephthalate

- 6.1.2.4. Other Bio-based Non-biodegradables

- 6.1.1. Bio-based Biodegradables

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Flexible Packaging

- 6.2.2. Rigid Packaging

- 6.2.3. Automotive and Assembly Operations

- 6.2.4. Agriculture and Horticulture

- 6.2.5. Construction

- 6.2.6. Textiles

- 6.2.7. Electrical and Electronics

- 6.2.8. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Germany European Bioplastics Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Bio-based Biodegradables

- 7.1.1.1. Starch-based

- 7.1.1.2. Polylactic Acid (PLA)

- 7.1.1.3. Polyhydroxyalkanoates (PHA)

- 7.1.1.4. Polyester (PBS, PBAT, and PCL)

- 7.1.1.5. Other Bio-based Biodegradables

- 7.1.2. Bio-based Non-biodegradables

- 7.1.2.1. Bio-polyethylene Terephthalate

- 7.1.2.2. Bio-polyamides

- 7.1.2.3. Bio-polytrimethylene Terephthalate

- 7.1.2.4. Other Bio-based Non-biodegradables

- 7.1.1. Bio-based Biodegradables

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Flexible Packaging

- 7.2.2. Rigid Packaging

- 7.2.3. Automotive and Assembly Operations

- 7.2.4. Agriculture and Horticulture

- 7.2.5. Construction

- 7.2.6. Textiles

- 7.2.7. Electrical and Electronics

- 7.2.8. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. United Kingdom European Bioplastics Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Bio-based Biodegradables

- 8.1.1.1. Starch-based

- 8.1.1.2. Polylactic Acid (PLA)

- 8.1.1.3. Polyhydroxyalkanoates (PHA)

- 8.1.1.4. Polyester (PBS, PBAT, and PCL)

- 8.1.1.5. Other Bio-based Biodegradables

- 8.1.2. Bio-based Non-biodegradables

- 8.1.2.1. Bio-polyethylene Terephthalate

- 8.1.2.2. Bio-polyamides

- 8.1.2.3. Bio-polytrimethylene Terephthalate

- 8.1.2.4. Other Bio-based Non-biodegradables

- 8.1.1. Bio-based Biodegradables

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Flexible Packaging

- 8.2.2. Rigid Packaging

- 8.2.3. Automotive and Assembly Operations

- 8.2.4. Agriculture and Horticulture

- 8.2.5. Construction

- 8.2.6. Textiles

- 8.2.7. Electrical and Electronics

- 8.2.8. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Italy European Bioplastics Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Bio-based Biodegradables

- 9.1.1.1. Starch-based

- 9.1.1.2. Polylactic Acid (PLA)

- 9.1.1.3. Polyhydroxyalkanoates (PHA)

- 9.1.1.4. Polyester (PBS, PBAT, and PCL)

- 9.1.1.5. Other Bio-based Biodegradables

- 9.1.2. Bio-based Non-biodegradables

- 9.1.2.1. Bio-polyethylene Terephthalate

- 9.1.2.2. Bio-polyamides

- 9.1.2.3. Bio-polytrimethylene Terephthalate

- 9.1.2.4. Other Bio-based Non-biodegradables

- 9.1.1. Bio-based Biodegradables

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Flexible Packaging

- 9.2.2. Rigid Packaging

- 9.2.3. Automotive and Assembly Operations

- 9.2.4. Agriculture and Horticulture

- 9.2.5. Construction

- 9.2.6. Textiles

- 9.2.7. Electrical and Electronics

- 9.2.8. Other Applications

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. France European Bioplastics Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. Bio-based Biodegradables

- 10.1.1.1. Starch-based

- 10.1.1.2. Polylactic Acid (PLA)

- 10.1.1.3. Polyhydroxyalkanoates (PHA)

- 10.1.1.4. Polyester (PBS, PBAT, and PCL)

- 10.1.1.5. Other Bio-based Biodegradables

- 10.1.2. Bio-based Non-biodegradables

- 10.1.2.1. Bio-polyethylene Terephthalate

- 10.1.2.2. Bio-polyamides

- 10.1.2.3. Bio-polytrimethylene Terephthalate

- 10.1.2.4. Other Bio-based Non-biodegradables

- 10.1.1. Bio-based Biodegradables

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Flexible Packaging

- 10.2.2. Rigid Packaging

- 10.2.3. Automotive and Assembly Operations

- 10.2.4. Agriculture and Horticulture

- 10.2.5. Construction

- 10.2.6. Textiles

- 10.2.7. Electrical and Electronics

- 10.2.8. Other Applications

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. Spain European Bioplastics Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 11.1.1. Bio-based Biodegradables

- 11.1.1.1. Starch-based

- 11.1.1.2. Polylactic Acid (PLA)

- 11.1.1.3. Polyhydroxyalkanoates (PHA)

- 11.1.1.4. Polyester (PBS, PBAT, and PCL)

- 11.1.1.5. Other Bio-based Biodegradables

- 11.1.2. Bio-based Non-biodegradables

- 11.1.2.1. Bio-polyethylene Terephthalate

- 11.1.2.2. Bio-polyamides

- 11.1.2.3. Bio-polytrimethylene Terephthalate

- 11.1.2.4. Other Bio-based Non-biodegradables

- 11.1.1. Bio-based Biodegradables

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Flexible Packaging

- 11.2.2. Rigid Packaging

- 11.2.3. Automotive and Assembly Operations

- 11.2.4. Agriculture and Horticulture

- 11.2.5. Construction

- 11.2.6. Textiles

- 11.2.7. Electrical and Electronics

- 11.2.8. Other Applications

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 12. Russia European Bioplastics Industry Analysis, Insights and Forecast, 2021-2033

- 12.1. Market Analysis, Insights and Forecast - by Product Type

- 12.1.1. Bio-based Biodegradables

- 12.1.1.1. Starch-based

- 12.1.1.2. Polylactic Acid (PLA)

- 12.1.1.3. Polyhydroxyalkanoates (PHA)

- 12.1.1.4. Polyester (PBS, PBAT, and PCL)

- 12.1.1.5. Other Bio-based Biodegradables

- 12.1.2. Bio-based Non-biodegradables

- 12.1.2.1. Bio-polyethylene Terephthalate

- 12.1.2.2. Bio-polyamides

- 12.1.2.3. Bio-polytrimethylene Terephthalate

- 12.1.2.4. Other Bio-based Non-biodegradables

- 12.1.1. Bio-based Biodegradables

- 12.2. Market Analysis, Insights and Forecast - by Application

- 12.2.1. Flexible Packaging

- 12.2.2. Rigid Packaging

- 12.2.3. Automotive and Assembly Operations

- 12.2.4. Agriculture and Horticulture

- 12.2.5. Construction

- 12.2.6. Textiles

- 12.2.7. Electrical and Electronics

- 12.2.8. Other Applications

- 12.1. Market Analysis, Insights and Forecast - by Product Type

- 13. Nordic Countries European Bioplastics Industry Analysis, Insights and Forecast, 2021-2033

- 13.1. Market Analysis, Insights and Forecast - by Product Type

- 13.1.1. Bio-based Biodegradables

- 13.1.1.1. Starch-based

- 13.1.1.2. Polylactic Acid (PLA)

- 13.1.1.3. Polyhydroxyalkanoates (PHA)

- 13.1.1.4. Polyester (PBS, PBAT, and PCL)

- 13.1.1.5. Other Bio-based Biodegradables

- 13.1.2. Bio-based Non-biodegradables

- 13.1.2.1. Bio-polyethylene Terephthalate

- 13.1.2.2. Bio-polyamides

- 13.1.2.3. Bio-polytrimethylene Terephthalate

- 13.1.2.4. Other Bio-based Non-biodegradables

- 13.1.1. Bio-based Biodegradables

- 13.2. Market Analysis, Insights and Forecast - by Application

- 13.2.1. Flexible Packaging

- 13.2.2. Rigid Packaging

- 13.2.3. Automotive and Assembly Operations

- 13.2.4. Agriculture and Horticulture

- 13.2.5. Construction

- 13.2.6. Textiles

- 13.2.7. Electrical and Electronics

- 13.2.8. Other Applications

- 13.1. Market Analysis, Insights and Forecast - by Product Type

- 14. Rest of Europe European Bioplastics Industry Analysis, Insights and Forecast, 2021-2033

- 14.1. Market Analysis, Insights and Forecast - by Product Type

- 14.1.1. Bio-based Biodegradables

- 14.1.1.1. Starch-based

- 14.1.1.2. Polylactic Acid (PLA)

- 14.1.1.3. Polyhydroxyalkanoates (PHA)

- 14.1.1.4. Polyester (PBS, PBAT, and PCL)

- 14.1.1.5. Other Bio-based Biodegradables

- 14.1.2. Bio-based Non-biodegradables

- 14.1.2.1. Bio-polyethylene Terephthalate

- 14.1.2.2. Bio-polyamides

- 14.1.2.3. Bio-polytrimethylene Terephthalate

- 14.1.2.4. Other Bio-based Non-biodegradables

- 14.1.1. Bio-based Biodegradables

- 14.2. Market Analysis, Insights and Forecast - by Application

- 14.2.1. Flexible Packaging

- 14.2.2. Rigid Packaging

- 14.2.3. Automotive and Assembly Operations

- 14.2.4. Agriculture and Horticulture

- 14.2.5. Construction

- 14.2.6. Textiles

- 14.2.7. Electrical and Electronics

- 14.2.8. Other Applications

- 14.1. Market Analysis, Insights and Forecast - by Product Type

- 15. Competitive Analysis

- 15.1. Company Profiles

- 15.1.1 Arkema

- 15.1.1.1. Company Overview

- 15.1.1.2. Products

- 15.1.1.3. Company Financials

- 15.1.1.4. SWOT Analysis

- 15.1.2 Futerro

- 15.1.2.1. Company Overview

- 15.1.2.2. Products

- 15.1.2.3. Company Financials

- 15.1.2.4. SWOT Analysis

- 15.1.3 Solvay

- 15.1.3.1. Company Overview

- 15.1.3.2. Products

- 15.1.3.3. Company Financials

- 15.1.3.4. SWOT Analysis

- 15.1.4 Kaneka Corporation

- 15.1.4.1. Company Overview

- 15.1.4.2. Products

- 15.1.4.3. Company Financials

- 15.1.4.4. SWOT Analysis

- 15.1.5 Braskem

- 15.1.5.1. Company Overview

- 15.1.5.2. Products

- 15.1.5.3. Company Financials

- 15.1.5.4. SWOT Analysis

- 15.1.6 Mitsubishi Chemical Corporation

- 15.1.6.1. Company Overview

- 15.1.6.2. Products

- 15.1.6.3. Company Financials

- 15.1.6.4. SWOT Analysis

- 15.1.7 Maccaferri Industrial Group

- 15.1.7.1. Company Overview

- 15.1.7.2. Products

- 15.1.7.3. Company Financials

- 15.1.7.4. SWOT Analysis

- 15.1.8 Corbion

- 15.1.8.1. Company Overview

- 15.1.8.2. Products

- 15.1.8.3. Company Financials

- 15.1.8.4. SWOT Analysis

- 15.1.9 BASF SE

- 15.1.9.1. Company Overview

- 15.1.9.2. Products

- 15.1.9.3. Company Financials

- 15.1.9.4. SWOT Analysis

- 15.1.10 Toray International Inc

- 15.1.10.1. Company Overview

- 15.1.10.2. Products

- 15.1.10.3. Company Financials

- 15.1.10.4. SWOT Analysis

- 15.1.11 Trinseo

- 15.1.11.1. Company Overview

- 15.1.11.2. Products

- 15.1.11.3. Company Financials

- 15.1.11.4. SWOT Analysis

- 15.1.12 Dow

- 15.1.12.1. Company Overview

- 15.1.12.2. Products

- 15.1.12.3. Company Financials

- 15.1.12.4. SWOT Analysis

- 15.1.13 Novamont SpA

- 15.1.13.1. Company Overview

- 15.1.13.2. Products

- 15.1.13.3. Company Financials

- 15.1.13.4. SWOT Analysis

- 15.1.14 Natureworks LLC

- 15.1.14.1. Company Overview

- 15.1.14.2. Products

- 15.1.14.3. Company Financials

- 15.1.14.4. SWOT Analysis

- 15.1.15 Danimer Scientific

- 15.1.15.1. Company Overview

- 15.1.15.2. Products

- 15.1.15.3. Company Financials

- 15.1.15.4. SWOT Analysis

- 15.1.1 Arkema

- 15.2. Market Entropy

- 15.2.1 Company's Key Areas Served

- 15.2.2 Recent Developments

- 15.3. Company Market Share Analysis 2025

- 15.3.1 Top 5 Companies Market Share Analysis

- 15.3.2 Top 3 Companies Market Share Analysis

- 15.4. List of Potential Customers

- 16. Research Methodology

List of Figures

- Figure 1: European Bioplastics Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: European Bioplastics Industry Share (%) by Company 2025

List of Tables

- Table 1: European Bioplastics Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 2: European Bioplastics Industry Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 3: European Bioplastics Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 4: European Bioplastics Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 5: European Bioplastics Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: European Bioplastics Industry Volume K Tons Forecast, by Region 2020 & 2033

- Table 7: European Bioplastics Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 8: European Bioplastics Industry Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 9: European Bioplastics Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 10: European Bioplastics Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 11: European Bioplastics Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 12: European Bioplastics Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 13: European Bioplastics Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 14: European Bioplastics Industry Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 15: European Bioplastics Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 16: European Bioplastics Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 17: European Bioplastics Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 18: European Bioplastics Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 19: European Bioplastics Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 20: European Bioplastics Industry Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 21: European Bioplastics Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 22: European Bioplastics Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 23: European Bioplastics Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 24: European Bioplastics Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 25: European Bioplastics Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 26: European Bioplastics Industry Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 27: European Bioplastics Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 28: European Bioplastics Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 29: European Bioplastics Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 30: European Bioplastics Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 31: European Bioplastics Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 32: European Bioplastics Industry Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 33: European Bioplastics Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 34: European Bioplastics Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 35: European Bioplastics Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 36: European Bioplastics Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 37: European Bioplastics Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 38: European Bioplastics Industry Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 39: European Bioplastics Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 40: European Bioplastics Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 41: European Bioplastics Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 42: European Bioplastics Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 43: European Bioplastics Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 44: European Bioplastics Industry Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 45: European Bioplastics Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 46: European Bioplastics Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 47: European Bioplastics Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 48: European Bioplastics Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 49: European Bioplastics Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 50: European Bioplastics Industry Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 51: European Bioplastics Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 52: European Bioplastics Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 53: European Bioplastics Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 54: European Bioplastics Industry Volume K Tons Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the European Bioplastics Industry?

The projected CAGR is approximately 17.98%.

2. Which companies are prominent players in the European Bioplastics Industry?

Key companies in the market include Arkema, Futerro, Solvay, Kaneka Corporation, Braskem, Mitsubishi Chemical Corporation, Maccaferri Industrial Group, Corbion, BASF SE, Toray International Inc, Trinseo, Dow, Novamont SpA, Natureworks LLC, Danimer Scientific.

3. What are the main segments of the European Bioplastics Industry?

The market segments include Product Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 9.54 billion as of 2022.

5. What are some drivers contributing to market growth?

Environmental Factors Encouraging a Paradigm Shift; Growing Demand for Bioplastics in Flexible Packaging; Other Drivers.

6. What are the notable trends driving market growth?

Flexible Packaging Expected to Dominate the Market.

7. Are there any restraints impacting market growth?

Availability of Cheaper Alternatives; Other Restraints.

8. Can you provide examples of recent developments in the market?

February 2022: Carbios and Indorama Ventures announced their partnership for bio-recycled PET in France with a processing capacity estimated at 50,000 tons.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "European Bioplastics Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the European Bioplastics Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the European Bioplastics Industry?

To stay informed about further developments, trends, and reports in the European Bioplastics Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence