Key Insights

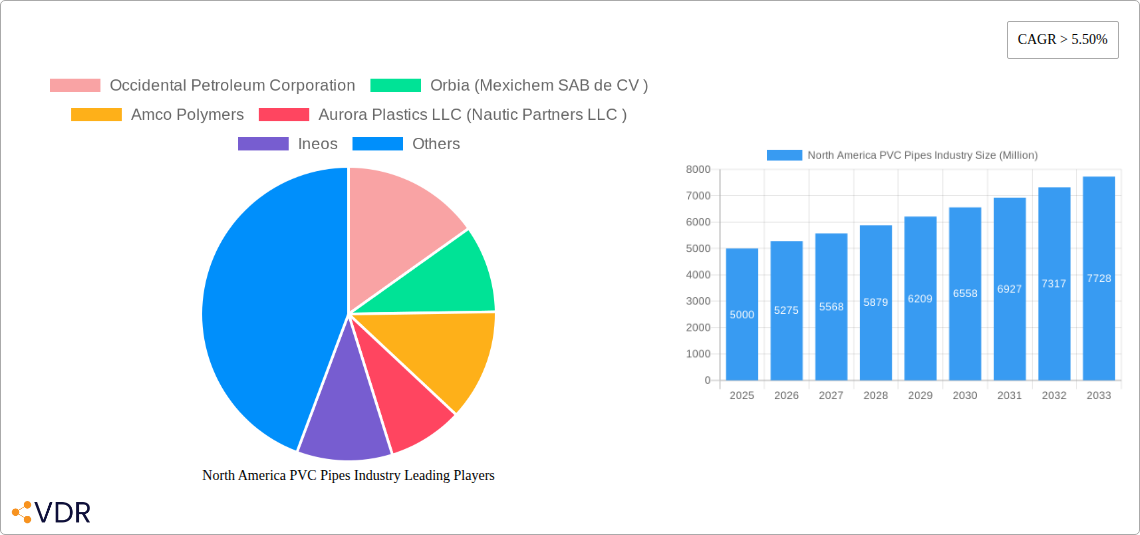

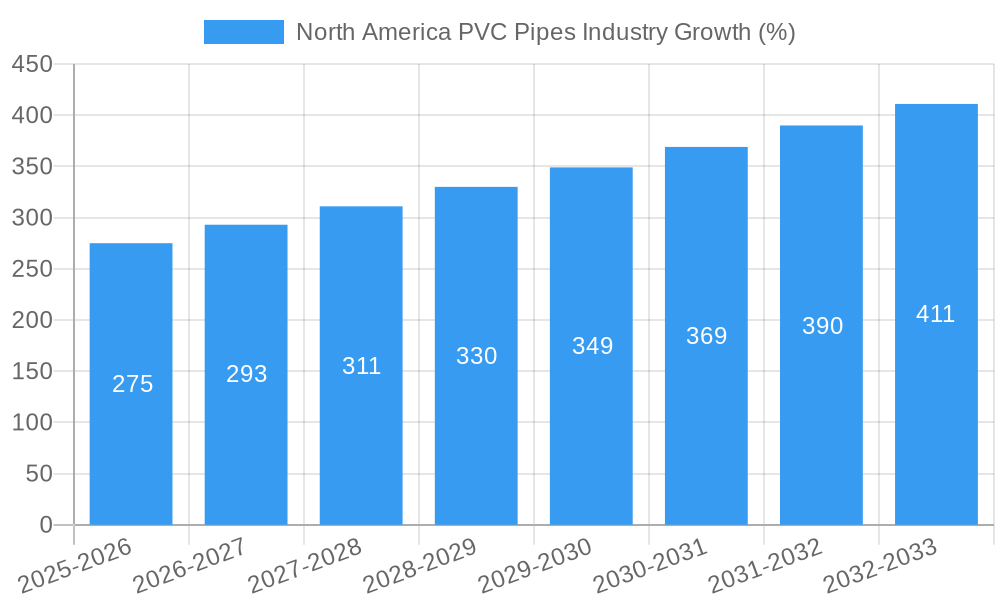

The North American PVC pipes market, valued at approximately $X billion in 2025 (estimated based on global market size and regional distribution), is projected to experience robust growth with a Compound Annual Growth Rate (CAGR) exceeding 5.5% from 2025 to 2033. This expansion is fueled by several key drivers. The burgeoning construction sector, particularly residential and infrastructure development, significantly boosts demand for PVC pipes due to their durability, cost-effectiveness, and ease of installation. Furthermore, increasing government investments in water infrastructure projects across the United States, Canada, and Mexico are contributing to market growth. Growing adoption of PVC pipes in the agricultural irrigation sector is adding to the demand. However, the market faces challenges like fluctuating raw material prices (primarily PVC resin) and environmental concerns surrounding PVC's manufacturing process and disposal. Stringent environmental regulations and the increasing popularity of eco-friendly alternatives are potential restraints to growth. The market is segmented by product type (rigid, flexible, low-smoke, chlorinated), application (pipes & fittings, films & sheets, etc.), and end-user industry (healthcare, automotive, building & construction etc.). Major players like Occidental Petroleum, Orbia, Ineos, and Formosa Plastics are strategically positioned to capitalize on market opportunities through innovation, expansion, and mergers and acquisitions. The North American region's strong economic performance and continued infrastructure investment solidify the market's positive outlook for the forecast period.

The competitive landscape is characterized by both large multinational corporations and regional players. These companies are actively engaged in expanding their product portfolios to meet specific market needs, investing in research and development to improve product performance and sustainability, and focusing on strengthening their distribution networks to enhance market reach. Strategic partnerships and collaborations are also becoming increasingly prevalent, contributing to market consolidation and the emergence of more innovative solutions. The future of the North American PVC pipes market hinges on the successful navigation of environmental regulations, material price volatility, and the growing adoption of sustainable alternatives, ensuring continued growth while addressing ecological concerns. Technological advancements in PVC pipe production and the exploration of recycled PVC are promising avenues for mitigating environmental impact and enhancing market sustainability.

North America PVC Pipes Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the North America PVC Pipes industry, encompassing market dynamics, growth trends, key players, and future outlook. The study period covers 2019-2033, with 2025 as the base and estimated year. This report is essential for industry professionals, investors, and strategic decision-makers seeking a thorough understanding of this dynamic market. The report delves into various segments including Product Types (Rigid PVC, Non-clear Rigid PVC, Flexible PVC, Non-clear Flexible PVC, Low-smoke PVC, Chlorinated PVC) and Applications (Pipes and Fittings, Films and Sheets, Wires and Cables, Bottles, Profiles, Hoses and Tubings, Other Applications) across key end-user industries.

North America PVC Pipes Industry Market Dynamics & Structure

The North American PVC pipes market is characterized by a moderately concentrated structure with several major players holding significant market share. Technological innovation, particularly in sustainable and high-performance PVC formulations, is a key driver. Stringent regulatory frameworks concerning material safety and environmental impact significantly influence market dynamics. Competition from alternative materials like polyethylene (PE) and cross-linked polyethylene (PEX) necessitates continuous product differentiation. End-user demographics, especially in the building and construction sector, are critical factors influencing demand. The market has witnessed several mergers and acquisitions (M&A) activities in recent years, reflecting industry consolidation and strategic expansion.

- Market Concentration: The top 5 players hold approximately xx% of the market share in 2025 (estimated).

- Technological Innovation: Focus on bio-based PVC and improved material properties are driving innovation.

- Regulatory Landscape: Stringent environmental regulations are shaping product development and manufacturing processes.

- Competitive Substitutes: PE and PEX pipes present competitive pressure, requiring enhanced performance and cost-effectiveness from PVC manufacturers.

- M&A Activity: xx M&A deals were recorded in the period 2019-2024.

North America PVC Pipes Industry Growth Trends & Insights

The North American PVC pipes market experienced a xx Million units CAGR during the historical period (2019-2024), driven by robust growth in the construction sector and increasing demand for water infrastructure improvements. Market penetration of PVC pipes remains high across various applications. Technological advancements, such as the development of bio-based PVC, are further accelerating growth, while consumer preference for sustainable building materials adds another positive factor. The market is expected to continue its growth trajectory, with a projected CAGR of xx Million units during the forecast period (2025-2033). However, fluctuating raw material prices and economic uncertainties could potentially impact growth rates.

Dominant Regions, Countries, or Segments in North America PVC Pipes Industry

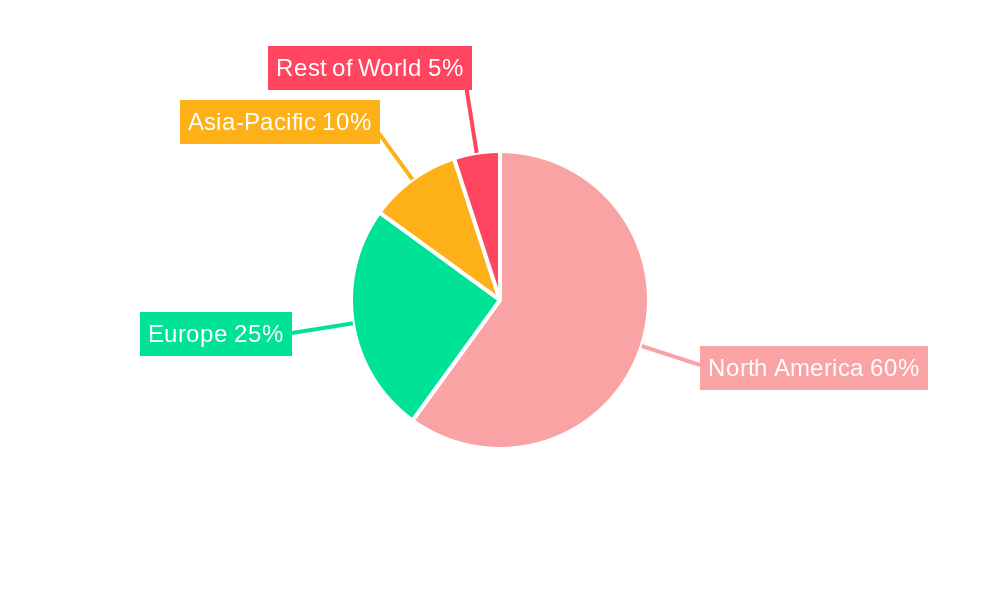

The building and construction sector is the dominant end-user industry for PVC pipes, accounting for approximately xx% of the market in 2025 (estimated). Within product types, rigid PVC dominates due to its strength and durability, holding approximately xx% of market share. The United States constitutes the largest regional market, followed by Canada and Mexico. Growth is primarily driven by government infrastructure projects, rising housing construction, and renovation activities.

- Key Growth Drivers: Strong construction activity in the U.S., government infrastructure investment, and increasing adoption of sustainable materials.

- Dominant Segments: Rigid PVC pipes in the building and construction sector, followed by pipes and fittings applications.

- Regional Dominance: The United States holds the largest market share driven by significant construction and infrastructure development.

North America PVC Pipes Industry Product Landscape

The PVC pipes market showcases a range of products catering to diverse applications. Innovation focuses on enhancing material properties like impact resistance, durability, and sustainability. Bio-based PVC is gaining traction, offering environmentally friendly alternatives. Product differentiation strategies center around specialized formulations for specific applications (e.g., high-pressure pipes, corrosion-resistant pipes). Performance metrics emphasize strength, longevity, and cost-effectiveness.

Key Drivers, Barriers & Challenges in North America PVC Pipes Industry

Key Drivers: Robust growth in the construction industry, increasing demand for water infrastructure upgrades, and government support for sustainable building materials. Technological advancements, specifically in bio-based PVC, create new market opportunities.

Challenges: Fluctuations in raw material prices (e.g., PVC resin), stringent environmental regulations, and competition from substitute materials pose significant hurdles. Supply chain disruptions can lead to production delays and increased costs. These challenges can result in a xx% reduction in projected growth in adverse conditions (estimated).

Emerging Opportunities in North America PVC Pipes Industry

Emerging opportunities lie in the growing demand for sustainable and eco-friendly PVC pipes, expansion into untapped markets within the infrastructure sector, and development of innovative applications in specialized sectors like industrial piping systems. The rising focus on water conservation and efficient irrigation systems presents significant growth potential for PVC pipes in agriculture and landscaping.

Growth Accelerators in the North America PVC Pipes Industry

Technological breakthroughs in PVC formulation, particularly bio-based and recycled content, will drive market growth. Strategic partnerships between manufacturers and end-users to develop innovative solutions and expansion into developing regional markets will further propel the industry's growth.

Key Players Shaping the North America PVC Pipes Industry Market

- Occidental Petroleum Corporation

- Orbia (Mexichem SAB de CV)

- Amco Polymers

- Aurora Plastics LLC (Nautic Partners LLC)

- Ineos

- SABIC

- LG Chem

- Shin-Etsu Chemical Co Ltd

- Formosa Plastics Corporation

- Westlake Corporation

Notable Milestones in North America PVC Pipes Industry Sector

- December 2022: Wavin launches bio-based drinking water solutions, signifying a shift towards sustainable PVC production.

- August 2022: Aurora Plastics expands operations, increasing rigid PVC production capacity by over 100 million pounds.

In-Depth North America PVC Pipes Industry Market Outlook

The future of the North American PVC pipes market appears bright, driven by continued infrastructure development and the growing demand for sustainable building materials. Strategic investments in research and development, coupled with a focus on product innovation and sustainability, will be critical for success. Companies that leverage technological advancements and adapt to changing regulatory landscapes are poised to capture significant market share in the coming years. The market is projected to reach xx Million units by 2033.

North America PVC Pipes Industry Segmentation

-

1. Product Type

-

1.1. Rigid PVC

- 1.1.1. Clear Rigid PVC

- 1.1.2. Non-clear Rigid PVC

-

1.2. Flexible PVC

- 1.2.1. Clear Flexible PVC

- 1.2.2. Non-clear Flexible PVC

- 1.3. Low-smoke PVC

- 1.4. Chlorinated PVC

-

1.1. Rigid PVC

-

2. Application

- 2.1. Pipes and Fittings

- 2.2. Films and Sheets

- 2.3. Wires and Cables

- 2.4. Bottles

- 2.5. Profiles, Hoses, and Tubings

- 2.6. Other Applications

-

3. End-user Industry

- 3.1. Healthcare

- 3.2. Automotive

- 3.3. Electrical and Electronics

- 3.4. Packaging

- 3.5. Footwear

- 3.6. Building and Construction

- 3.7. Other End-user Industries

-

4. Geography

- 4.1. United States

- 4.2. Canada

- 4.3. Mexico

North America PVC Pipes Industry Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Mexico

North America PVC Pipes Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 5.50% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Application in the Healthcare and Medical Devices Industries; Rising Demand from the Construction Industry

- 3.3. Market Restrains

- 3.3.1. Hazardous Impact on Humans and the Environment; Other Restraints

- 3.4. Market Trends

- 3.4.1. Growing Demand from the Construction Industry

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. North America PVC Pipes Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Rigid PVC

- 5.1.1.1. Clear Rigid PVC

- 5.1.1.2. Non-clear Rigid PVC

- 5.1.2. Flexible PVC

- 5.1.2.1. Clear Flexible PVC

- 5.1.2.2. Non-clear Flexible PVC

- 5.1.3. Low-smoke PVC

- 5.1.4. Chlorinated PVC

- 5.1.1. Rigid PVC

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Pipes and Fittings

- 5.2.2. Films and Sheets

- 5.2.3. Wires and Cables

- 5.2.4. Bottles

- 5.2.5. Profiles, Hoses, and Tubings

- 5.2.6. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. Healthcare

- 5.3.2. Automotive

- 5.3.3. Electrical and Electronics

- 5.3.4. Packaging

- 5.3.5. Footwear

- 5.3.6. Building and Construction

- 5.3.7. Other End-user Industries

- 5.4. Market Analysis, Insights and Forecast - by Geography

- 5.4.1. United States

- 5.4.2. Canada

- 5.4.3. Mexico

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. United States

- 5.5.2. Canada

- 5.5.3. Mexico

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. United States North America PVC Pipes Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Rigid PVC

- 6.1.1.1. Clear Rigid PVC

- 6.1.1.2. Non-clear Rigid PVC

- 6.1.2. Flexible PVC

- 6.1.2.1. Clear Flexible PVC

- 6.1.2.2. Non-clear Flexible PVC

- 6.1.3. Low-smoke PVC

- 6.1.4. Chlorinated PVC

- 6.1.1. Rigid PVC

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Pipes and Fittings

- 6.2.2. Films and Sheets

- 6.2.3. Wires and Cables

- 6.2.4. Bottles

- 6.2.5. Profiles, Hoses, and Tubings

- 6.2.6. Other Applications

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. Healthcare

- 6.3.2. Automotive

- 6.3.3. Electrical and Electronics

- 6.3.4. Packaging

- 6.3.5. Footwear

- 6.3.6. Building and Construction

- 6.3.7. Other End-user Industries

- 6.4. Market Analysis, Insights and Forecast - by Geography

- 6.4.1. United States

- 6.4.2. Canada

- 6.4.3. Mexico

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Canada North America PVC Pipes Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Rigid PVC

- 7.1.1.1. Clear Rigid PVC

- 7.1.1.2. Non-clear Rigid PVC

- 7.1.2. Flexible PVC

- 7.1.2.1. Clear Flexible PVC

- 7.1.2.2. Non-clear Flexible PVC

- 7.1.3. Low-smoke PVC

- 7.1.4. Chlorinated PVC

- 7.1.1. Rigid PVC

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Pipes and Fittings

- 7.2.2. Films and Sheets

- 7.2.3. Wires and Cables

- 7.2.4. Bottles

- 7.2.5. Profiles, Hoses, and Tubings

- 7.2.6. Other Applications

- 7.3. Market Analysis, Insights and Forecast - by End-user Industry

- 7.3.1. Healthcare

- 7.3.2. Automotive

- 7.3.3. Electrical and Electronics

- 7.3.4. Packaging

- 7.3.5. Footwear

- 7.3.6. Building and Construction

- 7.3.7. Other End-user Industries

- 7.4. Market Analysis, Insights and Forecast - by Geography

- 7.4.1. United States

- 7.4.2. Canada

- 7.4.3. Mexico

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. Mexico North America PVC Pipes Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Rigid PVC

- 8.1.1.1. Clear Rigid PVC

- 8.1.1.2. Non-clear Rigid PVC

- 8.1.2. Flexible PVC

- 8.1.2.1. Clear Flexible PVC

- 8.1.2.2. Non-clear Flexible PVC

- 8.1.3. Low-smoke PVC

- 8.1.4. Chlorinated PVC

- 8.1.1. Rigid PVC

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Pipes and Fittings

- 8.2.2. Films and Sheets

- 8.2.3. Wires and Cables

- 8.2.4. Bottles

- 8.2.5. Profiles, Hoses, and Tubings

- 8.2.6. Other Applications

- 8.3. Market Analysis, Insights and Forecast - by End-user Industry

- 8.3.1. Healthcare

- 8.3.2. Automotive

- 8.3.3. Electrical and Electronics

- 8.3.4. Packaging

- 8.3.5. Footwear

- 8.3.6. Building and Construction

- 8.3.7. Other End-user Industries

- 8.4. Market Analysis, Insights and Forecast - by Geography

- 8.4.1. United States

- 8.4.2. Canada

- 8.4.3. Mexico

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. United States North America PVC Pipes Industry Analysis, Insights and Forecast, 2019-2031

- 10. Canada North America PVC Pipes Industry Analysis, Insights and Forecast, 2019-2031

- 11. Mexico North America PVC Pipes Industry Analysis, Insights and Forecast, 2019-2031

- 12. Competitive Analysis

- 12.1. Market Share Analysis 2024

- 12.2. Company Profiles

- 12.2.1 Occidental Petroleum Corporation

- 12.2.1.1. Overview

- 12.2.1.2. Products

- 12.2.1.3. SWOT Analysis

- 12.2.1.4. Recent Developments

- 12.2.1.5. Financials (Based on Availability)

- 12.2.2 Orbia (Mexichem SAB de CV )

- 12.2.2.1. Overview

- 12.2.2.2. Products

- 12.2.2.3. SWOT Analysis

- 12.2.2.4. Recent Developments

- 12.2.2.5. Financials (Based on Availability)

- 12.2.3 Amco Polymers

- 12.2.3.1. Overview

- 12.2.3.2. Products

- 12.2.3.3. SWOT Analysis

- 12.2.3.4. Recent Developments

- 12.2.3.5. Financials (Based on Availability)

- 12.2.4 Aurora Plastics LLC (Nautic Partners LLC )

- 12.2.4.1. Overview

- 12.2.4.2. Products

- 12.2.4.3. SWOT Analysis

- 12.2.4.4. Recent Developments

- 12.2.4.5. Financials (Based on Availability)

- 12.2.5 Ineos

- 12.2.5.1. Overview

- 12.2.5.2. Products

- 12.2.5.3. SWOT Analysis

- 12.2.5.4. Recent Developments

- 12.2.5.5. Financials (Based on Availability)

- 12.2.6 SABIC

- 12.2.6.1. Overview

- 12.2.6.2. Products

- 12.2.6.3. SWOT Analysis

- 12.2.6.4. Recent Developments

- 12.2.6.5. Financials (Based on Availability)

- 12.2.7 LG Chem

- 12.2.7.1. Overview

- 12.2.7.2. Products

- 12.2.7.3. SWOT Analysis

- 12.2.7.4. Recent Developments

- 12.2.7.5. Financials (Based on Availability)

- 12.2.8 Shin-Etsu Chemical Co Ltd

- 12.2.8.1. Overview

- 12.2.8.2. Products

- 12.2.8.3. SWOT Analysis

- 12.2.8.4. Recent Developments

- 12.2.8.5. Financials (Based on Availability)

- 12.2.9 Formosa Plastics Corporation

- 12.2.9.1. Overview

- 12.2.9.2. Products

- 12.2.9.3. SWOT Analysis

- 12.2.9.4. Recent Developments

- 12.2.9.5. Financials (Based on Availability)

- 12.2.10 Westlake Corporation

- 12.2.10.1. Overview

- 12.2.10.2. Products

- 12.2.10.3. SWOT Analysis

- 12.2.10.4. Recent Developments

- 12.2.10.5. Financials (Based on Availability)

- 12.2.1 Occidental Petroleum Corporation

List of Figures

- Figure 1: North America PVC Pipes Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: North America PVC Pipes Industry Share (%) by Company 2024

List of Tables

- Table 1: North America PVC Pipes Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: North America PVC Pipes Industry Volume K Tons Forecast, by Region 2019 & 2032

- Table 3: North America PVC Pipes Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 4: North America PVC Pipes Industry Volume K Tons Forecast, by Product Type 2019 & 2032

- Table 5: North America PVC Pipes Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 6: North America PVC Pipes Industry Volume K Tons Forecast, by Application 2019 & 2032

- Table 7: North America PVC Pipes Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 8: North America PVC Pipes Industry Volume K Tons Forecast, by End-user Industry 2019 & 2032

- Table 9: North America PVC Pipes Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 10: North America PVC Pipes Industry Volume K Tons Forecast, by Geography 2019 & 2032

- Table 11: North America PVC Pipes Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 12: North America PVC Pipes Industry Volume K Tons Forecast, by Region 2019 & 2032

- Table 13: North America PVC Pipes Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 14: North America PVC Pipes Industry Volume K Tons Forecast, by Country 2019 & 2032

- Table 15: United States North America PVC Pipes Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: United States North America PVC Pipes Industry Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 17: Canada North America PVC Pipes Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Canada North America PVC Pipes Industry Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 19: Mexico North America PVC Pipes Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Mexico North America PVC Pipes Industry Volume (K Tons) Forecast, by Application 2019 & 2032

- Table 21: North America PVC Pipes Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 22: North America PVC Pipes Industry Volume K Tons Forecast, by Product Type 2019 & 2032

- Table 23: North America PVC Pipes Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 24: North America PVC Pipes Industry Volume K Tons Forecast, by Application 2019 & 2032

- Table 25: North America PVC Pipes Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 26: North America PVC Pipes Industry Volume K Tons Forecast, by End-user Industry 2019 & 2032

- Table 27: North America PVC Pipes Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 28: North America PVC Pipes Industry Volume K Tons Forecast, by Geography 2019 & 2032

- Table 29: North America PVC Pipes Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 30: North America PVC Pipes Industry Volume K Tons Forecast, by Country 2019 & 2032

- Table 31: North America PVC Pipes Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 32: North America PVC Pipes Industry Volume K Tons Forecast, by Product Type 2019 & 2032

- Table 33: North America PVC Pipes Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 34: North America PVC Pipes Industry Volume K Tons Forecast, by Application 2019 & 2032

- Table 35: North America PVC Pipes Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 36: North America PVC Pipes Industry Volume K Tons Forecast, by End-user Industry 2019 & 2032

- Table 37: North America PVC Pipes Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 38: North America PVC Pipes Industry Volume K Tons Forecast, by Geography 2019 & 2032

- Table 39: North America PVC Pipes Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 40: North America PVC Pipes Industry Volume K Tons Forecast, by Country 2019 & 2032

- Table 41: North America PVC Pipes Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 42: North America PVC Pipes Industry Volume K Tons Forecast, by Product Type 2019 & 2032

- Table 43: North America PVC Pipes Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 44: North America PVC Pipes Industry Volume K Tons Forecast, by Application 2019 & 2032

- Table 45: North America PVC Pipes Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 46: North America PVC Pipes Industry Volume K Tons Forecast, by End-user Industry 2019 & 2032

- Table 47: North America PVC Pipes Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 48: North America PVC Pipes Industry Volume K Tons Forecast, by Geography 2019 & 2032

- Table 49: North America PVC Pipes Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 50: North America PVC Pipes Industry Volume K Tons Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America PVC Pipes Industry?

The projected CAGR is approximately > 5.50%.

2. Which companies are prominent players in the North America PVC Pipes Industry?

Key companies in the market include Occidental Petroleum Corporation, Orbia (Mexichem SAB de CV ), Amco Polymers, Aurora Plastics LLC (Nautic Partners LLC ), Ineos, SABIC, LG Chem, Shin-Etsu Chemical Co Ltd, Formosa Plastics Corporation, Westlake Corporation.

3. What are the main segments of the North America PVC Pipes Industry?

The market segments include Product Type, Application, End-user Industry, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Application in the Healthcare and Medical Devices Industries; Rising Demand from the Construction Industry.

6. What are the notable trends driving market growth?

Growing Demand from the Construction Industry.

7. Are there any restraints impacting market growth?

Hazardous Impact on Humans and the Environment; Other Restraints.

8. Can you provide examples of recent developments in the market?

December 2022: Wavin, a division of Orbia's Building and Infrastructure company, introduced a portfolio of bio-based drinking water solutions to provide water utilities and infrastructure contractors with a cutting-edge sustainable product line. The new products from Wavin are made with a biobased PVC that substitutes ethylene with an alternative bio-ethylene derived from a biomass waste stream and uses vegetable oil.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America PVC Pipes Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America PVC Pipes Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America PVC Pipes Industry?

To stay informed about further developments, trends, and reports in the North America PVC Pipes Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence