Key Insights

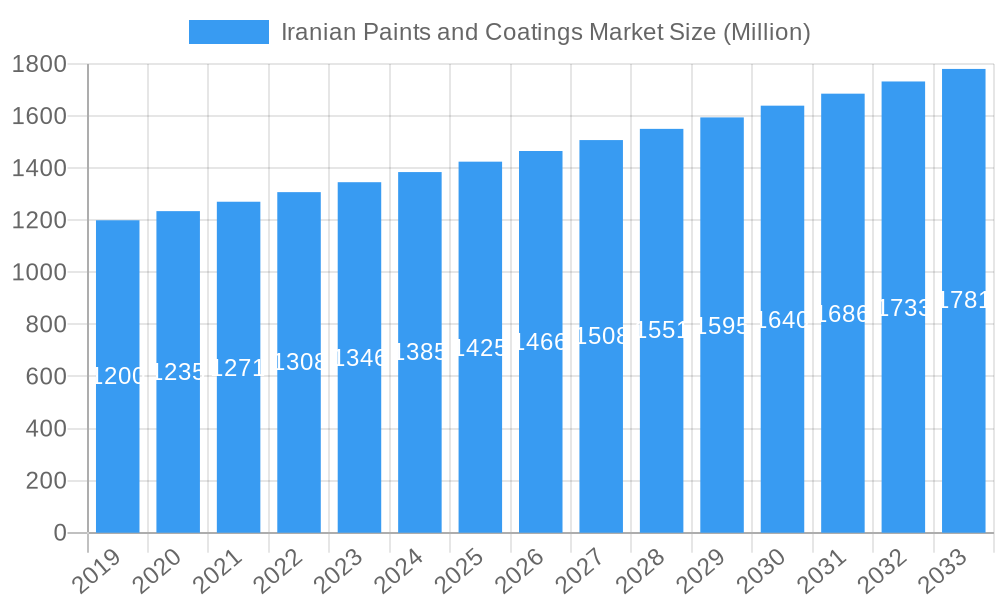

The Iranian paints and coatings market is poised for steady growth, with a projected Compound Annual Growth Rate (CAGR) of 2.89% between 2019 and 2033. This expansion is driven by robust demand across various end-user industries. The Architectural segment is a significant contributor, fueled by ongoing construction and renovation projects across Iran. The Automotive sector also plays a crucial role, with increasing domestic vehicle production and a growing demand for high-quality protective and decorative coatings. Furthermore, the Industrial Coatings segment, encompassing applications in manufacturing, machinery, and infrastructure, is expected to witness sustained demand as Iran's industrial base continues to develop. The Wood and Packaging sectors, while smaller, also present opportunities for growth as consumer spending and manufacturing activities evolve.

Iranian Paints and Coatings Market Market Size (In Billion)

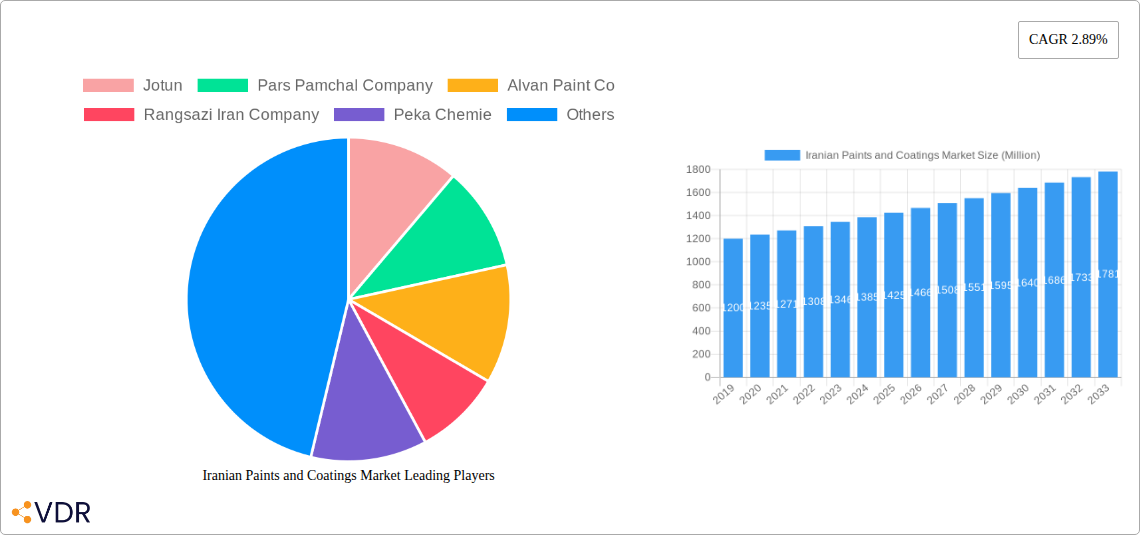

Technological advancements are shaping the market landscape, with a notable shift towards Water-borne coatings due to increasing environmental regulations and a growing consumer preference for eco-friendly products. Solvent-borne coatings, while still prevalent, are expected to see a gradual decline in market share. In terms of resin types, Acrylic and Alkyd coatings are likely to dominate, owing to their versatility and cost-effectiveness. Polyurethane and Epoxy coatings will see increasing adoption in demanding applications requiring enhanced durability and chemical resistance. Key players like Jotun, Pars Pamchal Company, Alvan Paint Co, Rangsazi Iran Company, Peka Chemie, Ronass Chemical Producing Co, Ranguin Co, and Saba Shimi Arya are actively competing, focusing on product innovation, sustainability, and expanding their distribution networks to capture market share. The market is primarily concentrated within Iran, with significant potential for further penetration and diversification across its various industrial and consumer segments.

Iranian Paints and Coatings Market Company Market Share

This comprehensive report delves into the dynamic Iranian Paints and Coatings Market, providing an in-depth analysis of market dynamics, growth trends, key players, and future opportunities. Covering the study period from 2019 to 2033, with a base year of 2025, this report offers critical insights for industry professionals navigating the evolving landscape of paint and coating solutions in Iran. We meticulously examine various resin types, technologies, and end-user industries, presenting all values in Million units for clarity and precision.

Iranian Paints and Coatings Market Market Dynamics & Structure

The Iranian paints and coatings market is characterized by a moderately concentrated structure, with a few dominant players alongside a significant number of smaller manufacturers. Technological innovation is a key driver, particularly in the development of eco-friendly and high-performance coatings. Regulatory frameworks, while evolving, play a crucial role in shaping product standards and environmental compliance. Competitive product substitutes, ranging from traditional paints to advanced functional coatings, influence market penetration and demand. End-user demographics, heavily influenced by the construction and automotive sectors, dictate consumption patterns. Mergers and acquisitions (M&A) activity, while not as robust as in mature markets, is gradually increasing as companies seek to expand their market reach and product portfolios.

- Market Concentration: The market is dominated by a mix of local stalwarts and international brands, with the top 5 companies estimated to hold approximately 45% of the market share.

- Technological Innovation Drivers: Demand for durable, low-VOC (Volatile Organic Compounds) coatings, driven by environmental awareness and stricter regulations, is pushing innovation in water-borne technologies and specialized resin formulations.

- Regulatory Frameworks: Government initiatives promoting energy efficiency in buildings and stricter emission standards for vehicles are influencing the adoption of advanced coating technologies.

- Competitive Product Substitutes: The availability of both standard and premium paint options, alongside specialized coatings for industrial applications, creates a dynamic competitive environment.

- End-User Demographics: A growing middle class and increasing urbanization fuel demand for decorative paints, while the automotive and industrial sectors drive the need for protective and functional coatings.

- M&A Trends: Limited but increasing M&A activity aims to consolidate market share and acquire technological capabilities, with an estimated 2-3 significant deals anticipated within the forecast period.

Iranian Paints and Coatings Market Growth Trends & Insights

The Iranian paints and coatings market is poised for substantial growth, driven by a confluence of economic recovery, infrastructure development, and increasing consumer demand for aesthetic and protective solutions. The market size evolution is projected to showcase a consistent upward trajectory, with an estimated Compound Annual Growth Rate (CAGR) of approximately 7.2% over the forecast period. Adoption rates for advanced coating technologies, particularly water-borne formulations, are expected to surge as environmental consciousness and regulatory pressures intensify. Technological disruptions, such as the integration of smart coatings with self-healing or antimicrobial properties, are beginning to emerge and are anticipated to gain traction. Consumer behavior shifts are evident, with a growing preference for aesthetically pleasing, durable, and sustainable paint options in residential and commercial applications. The automotive sector's resurgence, coupled with ongoing construction projects, will further fuel the demand for specialized industrial and architectural coatings.

The market's expansion is underpinned by robust demand from the architectural segment, which consistently represents the largest share due to ongoing urbanization and renovation activities. The automotive industry, recovering from previous slowdowns, is a significant contributor, with an increasing need for OEM and refinish coatings. Industrial coatings, encompassing a broad range of applications from machinery to infrastructure, also exhibit strong growth potential, driven by manufacturing sector expansion and maintenance requirements. The packaging sector is experiencing a steady rise, fueled by the growth of the food and beverage industry and the demand for protective and attractive packaging solutions. Wood coatings are witnessing a healthy demand, propelled by the furniture industry and the rising popularity of interior design trends.

Dominant Regions, Countries, or Segments in Iranian Paints and Coatings Market

The Iranian paints and coatings market exhibits distinct dominance across various segments, driven by specific economic, infrastructural, and demographic factors. Within the Resin Type segmentation, Acrylic and Alkyd resins currently hold the lion's share, accounting for an estimated combined market share of 60%. This dominance is attributed to their versatility, cost-effectiveness, and widespread application in architectural and general industrial coatings. Polyurethane coatings are steadily gaining ground, particularly in industrial and automotive applications, due to their superior durability and chemical resistance, projected to capture 18% of the market by 2033. Epoxy resins are crucial for protective coatings in demanding industrial environments, holding approximately 15% of the market, with significant potential in infrastructure projects. Polyester resins cater to specialized applications, contributing around 7% to the market.

In terms of Technology, Solvent-borne coatings, historically dominant due to their ease of application and fast drying times, are gradually being complemented and, in some segments, surpassed by Water-borne technologies. The market share of solvent-borne coatings is estimated at 55% in the base year 2025, but it is projected to decrease as environmental regulations tighten and consumer preferences shift towards greener alternatives. Water-borne coatings are anticipated to grow at a CAGR of 9.5%, reaching an estimated market share of 45% by 2033. This shift is driven by their lower VOC emissions and improved health and safety profiles.

The End-user Industry landscape clearly demonstrates the Architectural segment as the most dominant, representing an estimated 40% of the total market. This is propelled by Iran's ongoing urbanization, a growing population, and substantial investment in residential and commercial construction. The Industrial Coatings segment is the second largest, estimated at 25%, fueled by manufacturing growth, infrastructure development, and the need for protective coatings in various heavy industries. The Automotive sector, including both OEM and refinish markets, accounts for approximately 15%, with recovery in vehicle production and a growing aftermarket boosting demand. The Wood coatings segment holds about 10%, driven by the furniture industry and interior design trends. Transportation coatings (excluding automotive, such as marine and rail) represent 5%, while Packaging coatings, influenced by the food and beverage industry, contribute another 5%.

- Dominant Resin Type: Acrylic and Alkyd resins are leading due to their widespread use and cost-effectiveness.

- Dominant Technology: Solvent-borne currently leads but water-borne technologies are experiencing rapid growth due to environmental concerns.

- Dominant End-User Industry: Architectural coatings drive the market, followed by Industrial and Automotive segments.

- Key Drivers of Dominance: Urbanization, infrastructure projects, manufacturing expansion, and a growing middle class are key factors.

Iranian Paints and Coatings Market Product Landscape

The Iranian paints and coatings market is characterized by a diverse and evolving product landscape, catering to a wide array of aesthetic and functional requirements. Product innovations are increasingly focused on enhancing durability, performance, and environmental sustainability. Key innovations include the development of low-VOC and zero-VOC paints, advanced anti-corrosive coatings for industrial applications, and specialized decorative paints offering enhanced textures and finishes. The introduction of self-cleaning and antimicrobial coatings for architectural and healthcare settings represents a significant technological advancement. Performance metrics such as UV resistance, chemical resistance, adhesion strength, and drying time are continuously being optimized across product categories.

Key Drivers, Barriers & Challenges in Iranian Paints and Coatings Market

Key Drivers: The Iranian paints and coatings market is primarily propelled by robust demand from the construction sector, driven by urbanization and infrastructure development projects. The automotive industry's recovery and increasing vehicle production also contribute significantly. Technological advancements, leading to the development of eco-friendly and high-performance coatings, are creating new market opportunities. Government initiatives promoting industrial growth and import substitution further bolster domestic manufacturing.

Key Barriers & Challenges: A significant barrier is the reliance on imported raw materials, leading to price volatility and supply chain disruptions. Fluctuations in currency exchange rates also impact import costs and profitability. Stringent regulatory frameworks regarding VOC emissions, while driving innovation, can also pose compliance challenges for smaller manufacturers. Intense competition from both local and international players, coupled with price sensitivity in certain market segments, presents ongoing competitive pressures. Economic sanctions can also impact access to advanced technologies and specialized raw materials.

Emerging Opportunities in Iranian Paints and Coatings Market

Emerging opportunities in the Iranian paints and coatings market lie in the growing demand for specialized functional coatings, such as anti-corrosive coatings for the oil and gas sector and protective coatings for renewable energy infrastructure. The increasing consumer awareness regarding environmental sustainability is driving the market for water-borne and bio-based coatings. Furthermore, untapped potential exists in niche applications like marine coatings and coatings for the electronics industry. The government's focus on developing domestic manufacturing capabilities also presents opportunities for local players to innovate and expand their product portfolios.

Growth Accelerators in the Iranian Paints and Coatings Market Industry

Long-term growth in the Iranian paints and coatings market is being accelerated by ongoing investments in infrastructure development, including housing, transportation networks, and industrial facilities. Technological breakthroughs in resin chemistry and pigment technology are enabling the creation of more durable, eco-friendly, and high-performance coatings, expanding their applicability. Strategic partnerships and collaborations between local manufacturers and international technology providers are facilitating the transfer of advanced know-how and product development. Market expansion strategies focusing on underserved regions and emerging end-user industries will further contribute to sustained growth.

Key Players Shaping the Iranian Paints and Coatings Market Market

- Jotun

- Pars Pamchal Company

- Alvan Paint Co

- Rangsazi Iran Company

- Peka Chemie

- Ronass Chemical Producing Co

- Ranguin Co

- Saba Shimi Arya

Notable Milestones in Iranian Paints and Coatings Market Sector

- 2022: Launch of a new range of low-VOC architectural paints by a leading domestic manufacturer, responding to growing environmental concerns.

- 2023: Significant investment in advanced production technology by an industrial coatings specialist to enhance product quality and efficiency.

- 2024: Introduction of innovative anti-corrosive coatings with extended lifespan for infrastructure projects.

- 2024: Increased focus on research and development for bio-based and sustainable coating solutions.

- 2025 (Estimated): Expected introduction of smart coatings with self-healing properties in select industrial applications.

In-Depth Iranian Paints and Coatings Market Market Outlook

The future outlook for the Iranian paints and coatings market is highly promising, driven by sustained economic recovery, significant infrastructure investments, and a growing emphasis on sustainable and high-performance solutions. The market is expected to witness accelerated growth, fueled by technological advancements, strategic partnerships, and the increasing demand for specialized coatings across diverse end-user industries. Expansion into niche markets and a continued shift towards environmentally friendly products will define the trajectory of this dynamic sector.

Iranian Paints and Coatings Market Segmentation

-

1. Resin Type

- 1.1. Acrylic

- 1.2. Alkyd

- 1.3. Polyurethane

- 1.4. Epoxy

- 1.5. Polyester

- 1.6. Other Resin Types

-

2. Technology

- 2.1. Water-borne

- 2.2. Solvent-borne

-

3. End-user Industry

- 3.1. Architectural

- 3.2. Automotive

- 3.3. Wood

- 3.4. Industrial Coatings

- 3.5. Transportation

- 3.6. Packaging

Iranian Paints and Coatings Market Segmentation By Geography

- 1. Iran

Iranian Paints and Coatings Market Regional Market Share

Geographic Coverage of Iranian Paints and Coatings Market

Iranian Paints and Coatings Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.89% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Resin Type

- 5.1.1. Acrylic

- 5.1.2. Alkyd

- 5.1.3. Polyurethane

- 5.1.4. Epoxy

- 5.1.5. Polyester

- 5.1.6. Other Resin Types

- 5.2. Market Analysis, Insights and Forecast - by Technology

- 5.2.1. Water-borne

- 5.2.2. Solvent-borne

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. Architectural

- 5.3.2. Automotive

- 5.3.3. Wood

- 5.3.4. Industrial Coatings

- 5.3.5. Transportation

- 5.3.6. Packaging

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Iran

- 5.1. Market Analysis, Insights and Forecast - by Resin Type

- 6. Iranian Paints and Coatings Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Resin Type

- 6.1.1. Acrylic

- 6.1.2. Alkyd

- 6.1.3. Polyurethane

- 6.1.4. Epoxy

- 6.1.5. Polyester

- 6.1.6. Other Resin Types

- 6.2. Market Analysis, Insights and Forecast - by Technology

- 6.2.1. Water-borne

- 6.2.2. Solvent-borne

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. Architectural

- 6.3.2. Automotive

- 6.3.3. Wood

- 6.3.4. Industrial Coatings

- 6.3.5. Transportation

- 6.3.6. Packaging

- 6.1. Market Analysis, Insights and Forecast - by Resin Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Jotun

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Pars Pamchal Company

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Alvan Paint Co

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Rangsazi Iran Company

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Peka Chemie

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Ronass Chemical Producing Co

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Ranguin Co

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Saba Shimi Arya

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.1 Jotun

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Iranian Paints and Coatings Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Iranian Paints and Coatings Market Share (%) by Company 2025

List of Tables

- Table 1: Iranian Paints and Coatings Market Revenue Million Forecast, by Resin Type 2020 & 2033

- Table 2: Iranian Paints and Coatings Market Volume K Tons Forecast, by Resin Type 2020 & 2033

- Table 3: Iranian Paints and Coatings Market Revenue Million Forecast, by Technology 2020 & 2033

- Table 4: Iranian Paints and Coatings Market Volume K Tons Forecast, by Technology 2020 & 2033

- Table 5: Iranian Paints and Coatings Market Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 6: Iranian Paints and Coatings Market Volume K Tons Forecast, by End-user Industry 2020 & 2033

- Table 7: Iranian Paints and Coatings Market Revenue Million Forecast, by Region 2020 & 2033

- Table 8: Iranian Paints and Coatings Market Volume K Tons Forecast, by Region 2020 & 2033

- Table 9: Iranian Paints and Coatings Market Revenue Million Forecast, by Resin Type 2020 & 2033

- Table 10: Iranian Paints and Coatings Market Volume K Tons Forecast, by Resin Type 2020 & 2033

- Table 11: Iranian Paints and Coatings Market Revenue Million Forecast, by Technology 2020 & 2033

- Table 12: Iranian Paints and Coatings Market Volume K Tons Forecast, by Technology 2020 & 2033

- Table 13: Iranian Paints and Coatings Market Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 14: Iranian Paints and Coatings Market Volume K Tons Forecast, by End-user Industry 2020 & 2033

- Table 15: Iranian Paints and Coatings Market Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Iranian Paints and Coatings Market Volume K Tons Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Iranian Paints and Coatings Market?

The projected CAGR is approximately 2.89%.

2. Which companies are prominent players in the Iranian Paints and Coatings Market?

Key companies in the market include Jotun, Pars Pamchal Company, Alvan Paint Co, Rangsazi Iran Company, Peka Chemie, Ronass Chemical Producing Co, Ranguin Co, Saba Shimi Arya.

3. What are the main segments of the Iranian Paints and Coatings Market?

The market segments include Resin Type, Technology, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Government Measures to Boost Construction Activities for the Middle-class Population; Increasing Exports of Iranian Furniture; Other Drivers.

6. What are the notable trends driving market growth?

Acrylic Resins to Dominate the Market.

7. Are there any restraints impacting market growth?

The Conflict between the United States and Iran; Stringent Environmental Regulations Related to VOCs; Other Restraints.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Iranian Paints and Coatings Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Iranian Paints and Coatings Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Iranian Paints and Coatings Market?

To stay informed about further developments, trends, and reports in the Iranian Paints and Coatings Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence