Key Insights

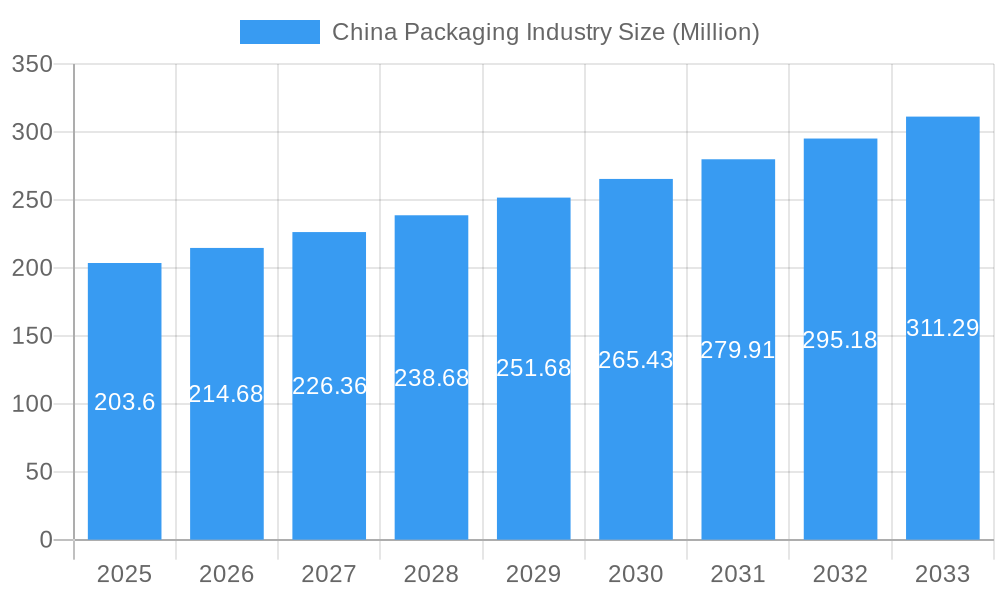

The China packaging industry, valued at $203.60 million in 2025, is experiencing robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of 5.22% from 2025 to 2033. This expansion is driven by several key factors. Firstly, the burgeoning e-commerce sector in China fuels a significant demand for efficient and protective packaging solutions for online deliveries. Secondly, rising consumer spending and changing lifestyles contribute to increased demand for packaged food and beverages, beauty products, and pharmaceuticals. Stringent government regulations promoting sustainable packaging practices are also influencing market dynamics, pushing companies towards eco-friendly materials like paper and biodegradable alternatives. Finally, advancements in packaging technology, including intelligent packaging solutions and improved barrier properties, offer enhanced product preservation and consumer experience, driving market growth.

China Packaging Industry Market Size (In Million)

However, challenges persist. Fluctuations in raw material prices, particularly for plastics and metals, pose a significant risk to profitability. The industry also faces increasing pressure to reduce its environmental footprint, necessitating investments in sustainable practices and materials. Intense competition among domestic and international players further complicates the market landscape, requiring companies to adopt innovative strategies to maintain their market share. Segmentation analysis reveals a dominance of plastic packaging, followed by paper and other materials. The food and beverage sector remains the largest end-user, but growth is also evident in healthcare, beauty, and industrial sectors. Key players like Amcor PLC, Mondi PLC, and Tetra Pak International SA are strategically positioned to capitalize on these growth opportunities, though the presence of numerous smaller, regional players indicates a highly competitive market requiring robust market strategies.

China Packaging Industry Company Market Share

China Packaging Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the dynamic China packaging industry, encompassing market size, growth trends, competitive landscape, and future outlook. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report is an invaluable resource for industry professionals, investors, and strategic decision-makers. The report leverages extensive data analysis to provide actionable insights across various segments, including packaging materials (plastic, paper, glass, foam, metal), packaging layers (primary, secondary, tertiary), and end-user industries (food & beverage, healthcare & pharmaceutical, beauty & personal care, industrial, and others). Key players like Daklapack Group, Transpak Inc, Sealed Air Corporation, Jiangyin Aluminum Foil Packaging East Asia Co Ltd, Plastipak Holdings Inc, Amcor PLC, Mondi PLC, Wipak Group, Guangzhou Yifeng Printing & Packaging Co Ltd, and Tetra Pak International SA are analyzed, offering a complete picture of this lucrative market. The report's quantitative and qualitative insights illuminate market dynamics, growth drivers, and potential challenges, providing a crucial roadmap for success in the competitive China packaging landscape. The market size is projected at xx Million units by 2025.

China Packaging Industry Market Dynamics & Structure

The China packaging industry is characterized by a dynamic and intricate ecosystem, shaped by a confluence of driving forces. Market concentration remains at a moderate level, fostering a competitive landscape where established multinational corporations coexist with a vibrant array of agile domestic players. A significant catalyst for the industry's evolution is technological innovation, increasingly steered by a dual imperative: to address pressing sustainability concerns and to cater to the ever-shifting preferences of discerning consumers. Furthermore, a robust and evolving regulatory framework, particularly concerning material recyclability and the stringent demands of food safety, profoundly influences industry operations and strategic decision-making. The meteoric rise of e-commerce, coupled with profound shifts in consumer lifestyles, has ignited a surge in demand for highly specialized and functional packaging solutions, presenting both substantial opportunities for growth and complex operational challenges. Concurrently, a palpable shift away from traditional packaging materials towards advanced, eco-friendly alternatives is rapidly gaining momentum. This period has also seen heightened merger and acquisition (M&A) activity, underscoring a clear trend towards industry consolidation and strategic expansion, with a notable figure of [Insert Specific Number Here] major deals recorded between 2019 and 2024.

- Market Concentration: A balanced mix exists between large multinational corporations and numerous smaller, dynamic domestic enterprises, indicating a moderately competitive market.

- Technological Innovation: The pursuit of sustainability, epitomized by the development and adoption of biodegradable and recyclable materials, alongside the sophisticated demands of the e-commerce sector, are primary drivers of technological advancement.

- Regulatory Framework: Strict governmental regulations governing material recyclability, waste management, and ensuring rigorous food safety standards play a crucial role in shaping industry practices.

- Competitive Product Substitutes: The market is experiencing a pronounced trend towards the adoption of innovative and environmentally responsible materials, increasingly substituting conventional options.

- End-User Demographics: Evolving consumer behaviors are increasingly favoring packaging that offers convenience, enhanced functionality, and demonstrably sustainable attributes.

- M&A Trends: The period between 2019 and 2024 witnessed [Insert Specific Number Here] significant merger and acquisition deals, signaling a robust trend of industry consolidation and strategic growth initiatives.

China Packaging Industry Growth Trends & Insights

The Chinese packaging market has demonstrated exceptional growth trajectories in recent years. This robust expansion is predominantly propelled by the phenomenal surge in e-commerce, the steady increase in disposable incomes across the population, and the escalating demand for conveniently packaged consumer goods. The market size has seen a substantial increase, expanding from an estimated [Insert Previous Year's Market Size] Million units in 2019 to [Insert Current Year's Market Size] Million units in 2024, reflecting an impressive Compound Annual Growth Rate (CAGR) of [Insert CAGR Percentage]%. The integration of sustainable packaging solutions is experiencing a notable acceleration, largely driven by supportive government policies and a heightened consumer awareness regarding environmental impact. Technological disruptions, including significant advancements in automated packaging processes and the development of intelligent, "smart" packaging, are fundamentally transforming operational efficiencies and product value propositions. A discernible shift in consumer purchasing habits, leaning towards premium quality and convenience-oriented packaging, presents both significant growth opportunities and strategic considerations. Projections indicate continued strong growth, fueled by the expanding middle-class demographic, ongoing urbanization, and persistent innovation in packaging technologies. The market is anticipated to reach an impressive [Insert Future Year's Market Size] Million units by 2033, with a projected CAGR of [Insert Future CAGR Percentage]% during the forecast period (2025-2033). Furthermore, the market penetration of sustainable packaging is expected to reach a significant [Insert Sustainable Packaging Penetration Percentage]% by 2033.

Dominant Regions, Countries, or Segments in China Packaging Industry

The coastal regions of China, particularly the Yangtze River Delta and the Pearl River Delta, are the dominant regions for packaging production and consumption. Within packaging materials, plastic packaging holds the largest market share, followed by paper and metal. However, the share of sustainable materials like paper and biodegradable plastics is growing rapidly. In terms of packaging layers, the primary layer segment dominates, accounting for the largest share of the market. The food and beverage industry is the largest end-user segment, followed by healthcare and pharmaceuticals. This dominance is driven by several factors including strong economic growth in these regions, well-established infrastructure, and a high concentration of manufacturing and processing facilities. Government policies supporting economic development and infrastructure investments further contribute to this regional dominance.

- Key Drivers: Strong economic growth in coastal regions, well-developed infrastructure, high concentration of manufacturing and processing facilities, government support for economic development and infrastructure investments.

- Dominant Segments: Plastic packaging materials, primary layer packaging, food and beverage end-user industry.

China Packaging Industry Product Landscape

The China packaging industry offers a wide array of products tailored to various end-user needs. Innovation is driven by factors such as sustainability concerns, convenience, and enhanced product protection. Product advancements include the use of biodegradable materials, smart packaging with embedded sensors, and modified atmosphere packaging (MAP) technologies. These innovations aim to improve product shelf life, reduce environmental impact, and enhance consumer experience. The market also witnesses a rise in customized packaging solutions catering to specific brand requirements and consumer preferences.

Key Drivers, Barriers & Challenges in China Packaging Industry

Key Drivers: The primary engines propelling growth in the China packaging industry include the sustained rise in disposable incomes, the continued expansion and sophistication of the e-commerce sector, and a growing overall demand for packaged goods across various consumer categories. Government initiatives actively promoting sustainable packaging solutions and the relentless pace of technological advancements in both packaging materials and processing techniques also serve as significant growth accelerators. For instance, the government's resolute emphasis on mitigating plastic waste is a direct impetus for the widespread adoption of eco-friendly and biodegradable alternatives.

Challenges & Restraints: The industry navigates several significant challenges, including the inherent volatility of raw material prices, intense market competition, the complex and often evolving landscape of regulatory compliance, and the persistent threat of supply chain disruptions, such as transportation bottlenecks. A critical balancing act for manufacturers lies in reconciling cost-effectiveness with the increasingly vital imperative of sustainability. For example, the impact of logistical disruptions on the availability and pricing of essential packaging materials can be substantial, with an estimated impact affecting approximately [Insert Percentage of Manufacturers Affected]% of manufacturers.

Emerging Opportunities in China Packaging Industry

Emerging trends reveal significant opportunities. The growing demand for sustainable and eco-friendly packaging presents a vast market for biodegradable and compostable materials. The rise of e-commerce is driving the need for innovative packaging solutions that ensure product safety and convenience during shipping. The increasing adoption of smart packaging technologies, integrated with sensors for tracking and monitoring, offers immense potential. Furthermore, tailored packaging solutions designed to meet specific consumer preferences and brand requirements are emerging as significant growth areas.

Growth Accelerators in the China Packaging Industry

Transformative breakthroughs in materials science, leading to the development of novel and high-performance packaging materials, alongside significant advancements in packaging automation technologies, are pivotal growth accelerators for the industry. The establishment of strategic partnerships between packaging manufacturers and leading brand owners is crucial for co-creating innovative and sustainable packaging solutions that resonate with market demands and drive expansion. Furthermore, proactive government initiatives designed to encourage the use of eco-friendly packaging options and to promote effective waste reduction strategies cultivate a highly supportive ecosystem for industry growth. The strategic expansion into emerging markets and the diversification of product portfolios also play a significant role in accelerating the industry's upward trajectory.

Key Players Shaping the China Packaging Industry Market

- Daklapack Group

- Transpak Inc

- Sealed Air Corporation

- Jiangyin Aluminum Foil Packaging East Asia Co Ltd

- Plastipak Holdings Inc

- Amcor PLC

- Mondi PLC

- Wipak Group

- Guangzhou Yifeng Printing & Packaging Co Ltd

- Tetra Pak International SA

Notable Milestones in China Packaging Industry Sector

- August 2022: Nippon Paint China and BASF jointly launched eco-friendly industrial packaging for Nippon Paint's dry-mixed mortar products, utilizing BASF's water-based barrier coatings. This signifies a shift towards sustainable packaging in the industrial sector.

- March 2022: Datwyler's acquisition of Yantai Xinhui Packing strengthens its pharmaceutical packaging capabilities in China, expanding its manufacturing capacity and local market reach.

In-Depth China Packaging Industry Market Outlook

The China packaging industry is poised for sustained growth, driven by technological advancements, rising consumer demand, and a supportive regulatory environment. Strategic opportunities lie in developing and commercializing sustainable packaging solutions, investing in automation and smart packaging technologies, and capitalizing on the booming e-commerce sector. The market's future success hinges on adapting to evolving consumer preferences, enhancing supply chain resilience, and navigating evolving regulatory landscapes. The potential for market expansion is significant, with continued growth anticipated across various segments and regions.

China Packaging Industry Segmentation

-

1. Packaging Material

- 1.1. Plastic

- 1.2. Paper

- 1.3. Glass

- 1.4. Metal

- 1.5. Other Packaging Material

-

2. Types of Packaging

- 2.1. Primary Packaging

- 2.2. Secondary Packaging

- 2.3. Tertiary Packaging

-

3. End-user Industry

- 3.1. Food and Beverage

- 3.2. Healthcare and Pharmaceutical

- 3.3. Beauty and Personal Care

- 3.4. Industrial

- 3.5. Other End-user Industries

China Packaging Industry Segmentation By Geography

- 1. China

China Packaging Industry Regional Market Share

Geographic Coverage of China Packaging Industry

China Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.22% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Packaging Material

- 5.1.1. Plastic

- 5.1.2. Paper

- 5.1.3. Glass

- 5.1.4. Metal

- 5.1.5. Other Packaging Material

- 5.2. Market Analysis, Insights and Forecast - by Types of Packaging

- 5.2.1. Primary Packaging

- 5.2.2. Secondary Packaging

- 5.2.3. Tertiary Packaging

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. Food and Beverage

- 5.3.2. Healthcare and Pharmaceutical

- 5.3.3. Beauty and Personal Care

- 5.3.4. Industrial

- 5.3.5. Other End-user Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. China

- 5.1. Market Analysis, Insights and Forecast - by Packaging Material

- 6. China Packaging Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Packaging Material

- 6.1.1. Plastic

- 6.1.2. Paper

- 6.1.3. Glass

- 6.1.4. Metal

- 6.1.5. Other Packaging Material

- 6.2. Market Analysis, Insights and Forecast - by Types of Packaging

- 6.2.1. Primary Packaging

- 6.2.2. Secondary Packaging

- 6.2.3. Tertiary Packaging

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. Food and Beverage

- 6.3.2. Healthcare and Pharmaceutical

- 6.3.3. Beauty and Personal Care

- 6.3.4. Industrial

- 6.3.5. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Packaging Material

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Daklapack Group

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Transpak Inc

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Sealed Air Corporation*List Not Exhaustive

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Jiangyin Aluminum Foil Packaging East Asia Co Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Plastipak Holdings Inc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Amcor PLC

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Mondi PLC

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Wipak Group

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Guangzhou Yifeng Printing & Packaging Co Ltd

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Tetra Pak International SA

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Daklapack Group

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China Packaging Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: China Packaging Industry Share (%) by Company 2025

List of Tables

- Table 1: China Packaging Industry Revenue Million Forecast, by Packaging Material 2020 & 2033

- Table 2: China Packaging Industry Revenue Million Forecast, by Types of Packaging 2020 & 2033

- Table 3: China Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 4: China Packaging Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: China Packaging Industry Revenue Million Forecast, by Packaging Material 2020 & 2033

- Table 6: China Packaging Industry Revenue Million Forecast, by Types of Packaging 2020 & 2033

- Table 7: China Packaging Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 8: China Packaging Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Packaging Industry?

The projected CAGR is approximately 5.22%.

2. Which companies are prominent players in the China Packaging Industry?

Key companies in the market include Daklapack Group, Transpak Inc, Sealed Air Corporation*List Not Exhaustive, Jiangyin Aluminum Foil Packaging East Asia Co Ltd, Plastipak Holdings Inc, Amcor PLC, Mondi PLC, Wipak Group, Guangzhou Yifeng Printing & Packaging Co Ltd, Tetra Pak International SA.

3. What are the main segments of the China Packaging Industry?

The market segments include Packaging Material, Types of Packaging, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 203.60 Million as of 2022.

5. What are some drivers contributing to market growth?

Rise of E-commerce Giants; Increasing Demand for Longer Shelf Life of Packaged Goods.

6. What are the notable trends driving market growth?

Plastic Packaging is Expected to Witness a Slow Growth Owing to Ban on Plastics.

7. Are there any restraints impacting market growth?

Strict Rules and Regulations in the Packaging Industry; Environmental Concerns Restricting the Market Growth.

8. Can you provide examples of recent developments in the market?

August 2022: Nippon Paint China, a prominent coatings producer, and BASF jointly introduced eco-friendly industrial packaging, which Nippon Paint's dry-mixed mortar series products have since embraced. The innovative packaging material for Nippon Paint's construction dry mortar products is commercialized, using water-based acrylic dispersion Joncryl High-Performance Barrier (HPB) from BASF as the barrier material. China will be the first country where BASF's water-based barrier coatings are employed in industrial packaging.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Packaging Industry?

To stay informed about further developments, trends, and reports in the China Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence