Key Insights

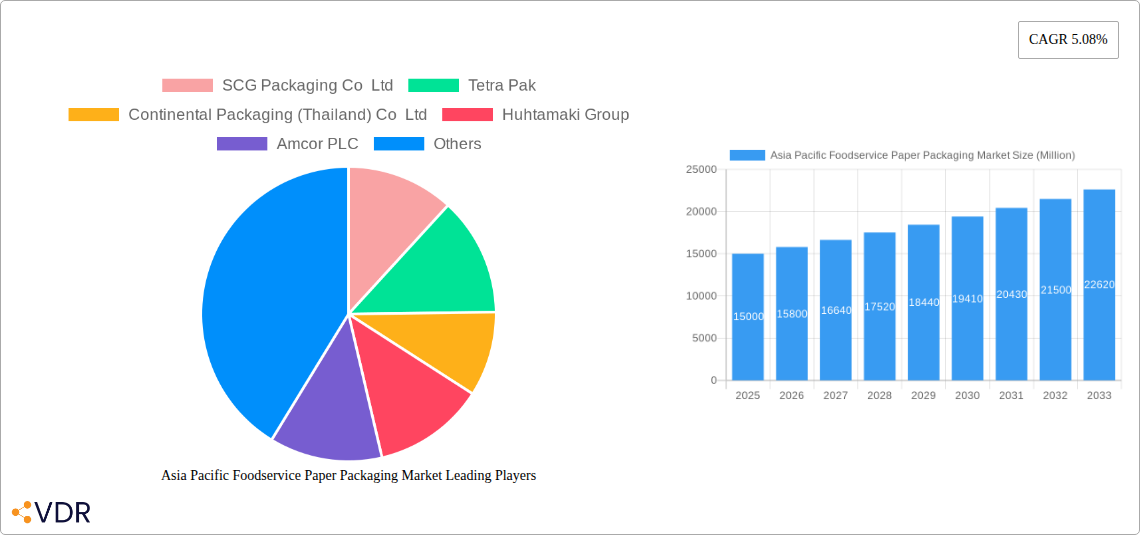

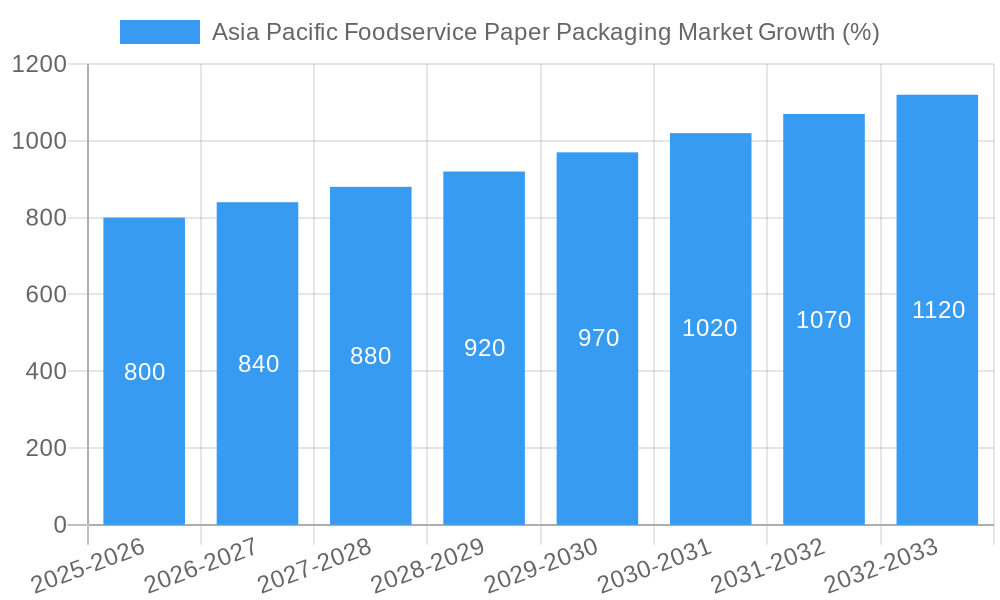

The Asia Pacific foodservice paper packaging market, valued at approximately $XX million in 2025, is projected to experience robust growth, driven by a compound annual growth rate (CAGR) of 5.08% from 2025 to 2033. This expansion is fueled by several key factors. The burgeoning foodservice industry across the region, particularly in countries like China, India, and Japan, is a significant driver. Increasing consumer preference for convenient and eco-friendly packaging options is further bolstering market growth. The rise of quick-service restaurants (QSRs) and the expanding online food delivery sector are also contributing to higher demand. Segment-wise, cups and lids currently hold a significant market share, followed by boxes and cartons. The bakery & confectionery, fruits and vegetables, and dairy products applications dominate the application segment, reflecting changing dietary habits and increased consumption of packaged food items. However, the market faces certain challenges, including fluctuating raw material prices and increasing environmental concerns related to paper waste management. Competitive pressures from alternative packaging materials also pose a threat. Despite these challenges, the long-term outlook for the Asia Pacific foodservice paper packaging market remains positive, with continuous innovation in sustainable packaging solutions expected to drive further growth. Major players such as SCG Packaging, Tetra Pak, and Amcor are strategically investing in capacity expansion and product diversification to capitalize on emerging opportunities.

The projected market size for 2033 can be estimated using the provided CAGR. Given a 2025 value of $XX million (this needs to be replaced with an actual value), and a CAGR of 5.08%, a simple compound interest calculation will yield a projected 2033 market size. Furthermore, regional variations will exist, with China, Japan, and India likely dominating market share due to their large and rapidly growing foodservice sectors. Competitive analysis reveals a landscape dominated by established multinational corporations and regional players, with significant opportunities for both organic growth and mergers & acquisitions. The market is expected to witness a shift towards more sustainable and recyclable packaging materials, aligning with global environmental initiatives and consumer preferences. This will require companies to invest in research and development to offer environmentally responsible solutions that meet the demands of the foodservice industry.

Asia Pacific Foodservice Paper Packaging Market: A Comprehensive Report (2019-2033)

This in-depth report provides a comprehensive analysis of the Asia Pacific foodservice paper packaging market, encompassing market dynamics, growth trends, regional dominance, product landscape, key challenges, emerging opportunities, and key players. The study period covers 2019-2033, with 2025 as the base year and a forecast period of 2025-2033. The report is crucial for businesses, investors, and industry professionals seeking a clear understanding of this dynamic market. Market values are presented in million units.

Asia Pacific Foodservice Paper Packaging Market Dynamics & Structure

The Asia Pacific foodservice paper packaging market is characterized by a moderately consolidated structure, with key players like SCG Packaging Co Ltd, Tetra Pak, and Amcor PLC holding significant market shares. Technological innovation, particularly in sustainable and eco-friendly packaging solutions, is a key driver. Stringent regulatory frameworks, particularly concerning food safety and waste management (as exemplified by India's FSSAI regulations in March 2022), are shaping market practices. The market also faces competition from alternative packaging materials, such as plastics, although growing environmental concerns are increasingly favoring paper-based solutions. The increasing prevalence of quick-service restaurants and the expanding retail sector in the region significantly boosts demand. M&A activity, though not at exceptionally high volumes (estimated at xx deals annually), is strategically shaping the competitive landscape.

- Market Concentration: Moderately Consolidated (xx% market share held by top 5 players).

- Technological Innovation: Focus on sustainable materials, improved barrier properties, and functional designs.

- Regulatory Framework: Stringent food safety and environmental regulations (e.g., FSSAI regulations in India).

- Competitive Substitutes: Plastics and other alternative packaging materials.

- End-User Demographics: Growth driven by rising disposable incomes and changing consumer preferences for convenience.

- M&A Trends: Strategic acquisitions to expand market reach and product portfolio (xx deals annually estimated).

Asia Pacific Foodservice Paper Packaging Market Growth Trends & Insights

The Asia Pacific foodservice paper packaging market is experiencing robust growth, driven by the expanding foodservice industry and increasing consumer demand for convenient and sustainable packaging. The market size is projected to reach xx million units by 2025, with a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). This growth is fueled by several factors, including the rising popularity of quick-service restaurants and online food delivery platforms, as well as the growing preference for eco-friendly packaging options among environmentally conscious consumers. Technological advancements, such as improved barrier coatings and functional designs, are enhancing the performance and appeal of paper-based foodservice packaging. Market penetration is steadily increasing in developing economies, driven by factors such as urbanization and rising disposable incomes.

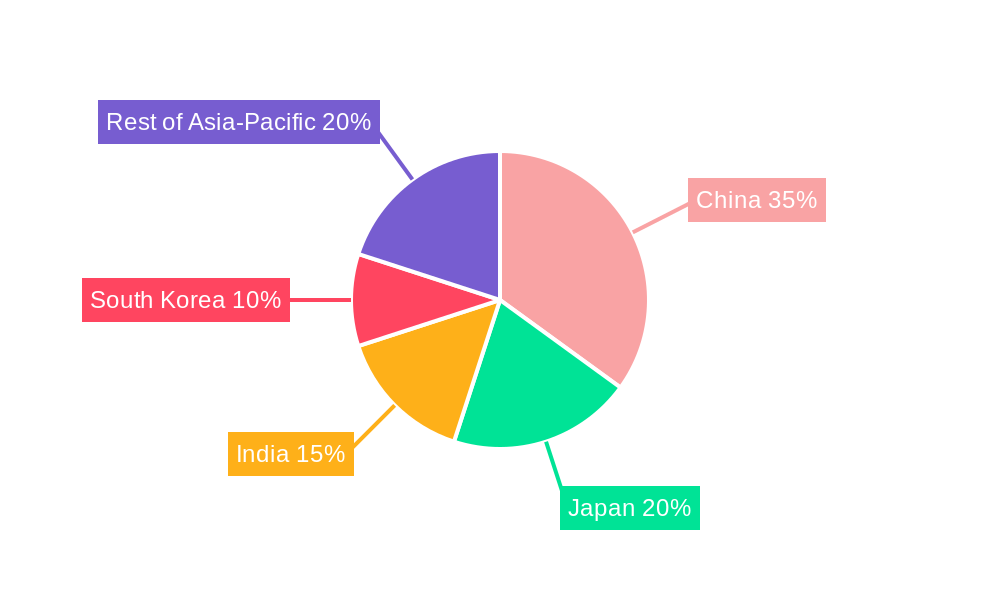

Dominant Regions, Countries, or Segments in Asia Pacific Foodservice Paper Packaging Market

China and India dominate the Asia Pacific foodservice paper packaging market, driven by their large and rapidly growing populations, burgeoning foodservice industries, and expanding retail sectors. Japan and South Korea also hold significant market shares due to their mature economies and developed foodservice infrastructures. Within the segment breakdown:

- By End User: Restaurants (Quick & Full-service based) represent the largest segment, followed by retail establishments.

- By Country: China and India exhibit the highest growth potential.

- By Type: Cups & Lids and Boxes & Cartons constitute the major product types.

- By Application: Beverages, Fruits and Vegetables, and Bakery & Confectionery drive significant demand.

Key drivers include strong economic growth, rapid urbanization, and increasing disposable incomes. China's robust manufacturing base further strengthens its dominance. India's expanding middle class and growing foodservice sector contribute to its significant growth potential.

Asia Pacific Foodservice Paper Packaging Market Product Landscape

The Asia Pacific foodservice paper packaging market offers a diverse range of products, including cups and lids, boxes and cartons, and other specialized packaging solutions tailored to specific food items. Recent innovations include enhanced barrier coatings to improve grease resistance and extend shelf life, eco-friendly materials sourced from sustainable forests, and improved designs for enhanced stacking and transportation efficiency. These innovations cater to the demand for both functionality and environmental sustainability.

Key Drivers, Barriers & Challenges in Asia Pacific Foodservice Paper Packaging Market

Key Drivers:

- Growing foodservice industry

- Increasing consumer preference for convenience and takeaway options.

- Rising demand for sustainable and eco-friendly packaging.

- Technological advancements improving functionality and performance.

Key Challenges:

- Fluctuations in raw material prices (e.g., pulp).

- Competition from alternative packaging materials (plastics).

- Stringent regulatory compliance requirements for food safety and environmental protection.

- Supply chain disruptions (especially following the pandemic and geopolitical events).

Emerging Opportunities in Asia Pacific Foodservice Paper Packaging Market

Significant opportunities exist in expanding into untapped markets within the region, developing innovative packaging solutions for emerging food categories, and catering to the growing demand for customized and personalized packaging. The increasing focus on sustainability presents opportunities for manufacturers offering eco-friendly and biodegradable packaging options. Moreover, the development of smart packaging technologies, incorporating features like tamper evidence and improved traceability, offers exciting growth potential.

Growth Accelerators in the Asia Pacific Foodservice Paper Packaging Market Industry

The Asia Pacific foodservice paper packaging market's long-term growth is accelerated by ongoing technological advancements in sustainable materials and coatings, the strategic consolidation of the industry through mergers and acquisitions, and increasing government support for sustainable packaging initiatives. Expansions into newer markets and successful collaborations between packaging manufacturers and foodservice operators will also drive future growth.

Key Players Shaping the Asia Pacific Foodservice Paper Packaging Market Market

- SCG Packaging Co Ltd

- Tetra Pak

- Continental Packaging (Thailand) Co Ltd

- Huhtamaki Group

- Amcor PLC

- Pura Group

- Oji Holdings Corporation

- International Paper Company

- Toppan Inc

- Sarnti Packaging Co Ltd

Notable Milestones in Asia Pacific Foodservice Paper Packaging Market Sector

- August 2022: Amcor opened a new Innovation Center in Jiangyin, China, accelerating the development of sustainable packaging solutions.

- March 2022: India's FSSAI implemented new regulations to control the use of recycled plastics in food packaging, promoting safer and more sustainable practices.

In-Depth Asia Pacific Foodservice Paper Packaging Market Market Outlook

The Asia Pacific foodservice paper packaging market holds immense future potential, driven by sustained growth in the foodservice sector, increasing consumer demand for convenient and sustainable options, and continuous technological advancements. Strategic partnerships and investments in innovative solutions will be crucial for companies to capitalize on emerging opportunities and secure a strong market position in the years to come. The market is poised for significant expansion, presenting attractive prospects for both established players and new entrants.

Asia Pacific Foodservice Paper Packaging Market Segmentation

-

1. Type

- 1.1. Cups & Lids

- 1.2. Boxes & Cartons

-

2. Application

- 2.1. Fruits and vegetables

- 2.2. Dairy products

- 2.3. Bakery & Confectionery

- 2.4. Beverages

- 2.5. Meat & Poultry

- 2.6. Others

-

3. End User

- 3.1. Restaurants (Quick & Full-service based)

- 3.2. Retail establishments

- 3.3. Institutional

- 3.4. Other End-user Applications

Asia Pacific Foodservice Paper Packaging Market Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. Japan

- 1.3. South Korea

- 1.4. India

- 1.5. Australia

- 1.6. New Zealand

- 1.7. Indonesia

- 1.8. Malaysia

- 1.9. Singapore

- 1.10. Thailand

- 1.11. Vietnam

- 1.12. Philippines

Asia Pacific Foodservice Paper Packaging Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 5.08% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Shift in Consumer Preferences toward Recyclable and Eco-friendly Materials; Online Food Ordering Services are Expected to Drive the Market

- 3.3. Market Restrains

- 3.3.1. Increasing Price Volatility of Raw Materials

- 3.4. Market Trends

- 3.4.1. Online Food Ordering Services are Expected to Drive the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Asia Pacific Foodservice Paper Packaging Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Cups & Lids

- 5.1.2. Boxes & Cartons

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Fruits and vegetables

- 5.2.2. Dairy products

- 5.2.3. Bakery & Confectionery

- 5.2.4. Beverages

- 5.2.5. Meat & Poultry

- 5.2.6. Others

- 5.3. Market Analysis, Insights and Forecast - by End User

- 5.3.1. Restaurants (Quick & Full-service based)

- 5.3.2. Retail establishments

- 5.3.3. Institutional

- 5.3.4. Other End-user Applications

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. China Asia Pacific Foodservice Paper Packaging Market Analysis, Insights and Forecast, 2019-2031

- 7. Japan Asia Pacific Foodservice Paper Packaging Market Analysis, Insights and Forecast, 2019-2031

- 8. India Asia Pacific Foodservice Paper Packaging Market Analysis, Insights and Forecast, 2019-2031

- 9. South Korea Asia Pacific Foodservice Paper Packaging Market Analysis, Insights and Forecast, 2019-2031

- 10. Taiwan Asia Pacific Foodservice Paper Packaging Market Analysis, Insights and Forecast, 2019-2031

- 11. Australia Asia Pacific Foodservice Paper Packaging Market Analysis, Insights and Forecast, 2019-2031

- 12. Rest of Asia-Pacific Asia Pacific Foodservice Paper Packaging Market Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 SCG Packaging Co Ltd

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 Tetra Pak

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 Continental Packaging (Thailand) Co Ltd

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 Huhtamaki Group

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 Amcor PLC

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 Pura Group

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 Oji Holdings Corporation

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 International Paper Company

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 Toppan Inc

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.10 Sarnti Packaging Co Ltd

- 13.2.10.1. Overview

- 13.2.10.2. Products

- 13.2.10.3. SWOT Analysis

- 13.2.10.4. Recent Developments

- 13.2.10.5. Financials (Based on Availability)

- 13.2.1 SCG Packaging Co Ltd

List of Figures

- Figure 1: Asia Pacific Foodservice Paper Packaging Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Asia Pacific Foodservice Paper Packaging Market Share (%) by Company 2024

List of Tables

- Table 1: Asia Pacific Foodservice Paper Packaging Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Asia Pacific Foodservice Paper Packaging Market Revenue Million Forecast, by Type 2019 & 2032

- Table 3: Asia Pacific Foodservice Paper Packaging Market Revenue Million Forecast, by Application 2019 & 2032

- Table 4: Asia Pacific Foodservice Paper Packaging Market Revenue Million Forecast, by End User 2019 & 2032

- Table 5: Asia Pacific Foodservice Paper Packaging Market Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Asia Pacific Foodservice Paper Packaging Market Revenue Million Forecast, by Country 2019 & 2032

- Table 7: China Asia Pacific Foodservice Paper Packaging Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Japan Asia Pacific Foodservice Paper Packaging Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: India Asia Pacific Foodservice Paper Packaging Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: South Korea Asia Pacific Foodservice Paper Packaging Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Taiwan Asia Pacific Foodservice Paper Packaging Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Australia Asia Pacific Foodservice Paper Packaging Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Rest of Asia-Pacific Asia Pacific Foodservice Paper Packaging Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Asia Pacific Foodservice Paper Packaging Market Revenue Million Forecast, by Type 2019 & 2032

- Table 15: Asia Pacific Foodservice Paper Packaging Market Revenue Million Forecast, by Application 2019 & 2032

- Table 16: Asia Pacific Foodservice Paper Packaging Market Revenue Million Forecast, by End User 2019 & 2032

- Table 17: Asia Pacific Foodservice Paper Packaging Market Revenue Million Forecast, by Country 2019 & 2032

- Table 18: China Asia Pacific Foodservice Paper Packaging Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Japan Asia Pacific Foodservice Paper Packaging Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: South Korea Asia Pacific Foodservice Paper Packaging Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: India Asia Pacific Foodservice Paper Packaging Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Australia Asia Pacific Foodservice Paper Packaging Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: New Zealand Asia Pacific Foodservice Paper Packaging Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Indonesia Asia Pacific Foodservice Paper Packaging Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: Malaysia Asia Pacific Foodservice Paper Packaging Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Singapore Asia Pacific Foodservice Paper Packaging Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 27: Thailand Asia Pacific Foodservice Paper Packaging Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: Vietnam Asia Pacific Foodservice Paper Packaging Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 29: Philippines Asia Pacific Foodservice Paper Packaging Market Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Asia Pacific Foodservice Paper Packaging Market?

The projected CAGR is approximately 5.08%.

2. Which companies are prominent players in the Asia Pacific Foodservice Paper Packaging Market?

Key companies in the market include SCG Packaging Co Ltd, Tetra Pak, Continental Packaging (Thailand) Co Ltd, Huhtamaki Group, Amcor PLC, Pura Group, Oji Holdings Corporation, International Paper Company, Toppan Inc, Sarnti Packaging Co Ltd.

3. What are the main segments of the Asia Pacific Foodservice Paper Packaging Market?

The market segments include Type, Application, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Shift in Consumer Preferences toward Recyclable and Eco-friendly Materials; Online Food Ordering Services are Expected to Drive the Market.

6. What are the notable trends driving market growth?

Online Food Ordering Services are Expected to Drive the Market.

7. Are there any restraints impacting market growth?

Increasing Price Volatility of Raw Materials.

8. Can you provide examples of recent developments in the market?

August 2022: Amcor added a new location in Jiangyin, China, to its network of Innovation Centers. Customers in the area now have access to Amcor's expertise through the new facility in China. This speeds up the development of packaging solutions that are better for the environment.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Asia Pacific Foodservice Paper Packaging Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Asia Pacific Foodservice Paper Packaging Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Asia Pacific Foodservice Paper Packaging Market?

To stay informed about further developments, trends, and reports in the Asia Pacific Foodservice Paper Packaging Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence