Key Insights

The global Mechanical Tube and Pipe market is poised for substantial growth, projected to reach a market size of approximately $120 billion by 2025, with an estimated Compound Annual Growth Rate (CAGR) of around 6.5% through 2033. This expansion is primarily driven by escalating demand from critical sectors such as solar panel support systems, industrial machinery, and robust infrastructure development, particularly in emerging economies. The increasing adoption of renewable energy, exemplified by the surge in solar power installations, necessitates high-quality mechanical tubes for structural integrity and longevity. Similarly, the ongoing need for advanced manufacturing processes and expansion of industrial facilities worldwide fuels demand for durable and precisely engineered steel tubes. The conveyor belt component sector also contributes significantly, requiring specialized tubes for efficient material handling operations across logistics and mining.

Key trends shaping the mechanical tube and pipe market include a notable shift towards higher-grade and specialized alloy tubes to meet stringent performance requirements in demanding applications. Innovations in manufacturing processes, such as advancements in welding techniques for welded steel tubes and improved material compositions for seamless steel tubes, are enhancing product quality and reducing production costs. However, the market faces certain restraints, including volatility in raw material prices, particularly for steel, which can impact profit margins and pricing strategies for manufacturers. Stringent environmental regulations concerning emissions and waste management in the steel production process also pose compliance challenges and may necessitate capital investments in greener technologies. Despite these challenges, the overall outlook remains positive, with continuous technological advancements and a persistent need for robust mechanical components in diverse industrial landscapes.

Here's a comprehensive, SEO-optimized report description for the Mechanical Tube and Pipe market, designed for immediate use without modification:

This in-depth report provides a critical analysis of the global Mechanical Tube and Pipe market, offering invaluable insights for manufacturers, suppliers, investors, and industry stakeholders. Covering a comprehensive study period from 2019 to 2033, with a base year of 2025 and a forecast period of 2025-2033, this report dissects market dynamics, growth trajectories, and future potential.

The Mechanical Tube and Pipe market is a vital sector underpinning numerous industrial applications, from robust machinery and efficient conveyor belt components to resilient greenhouse structures and innovative solar panel supports. Understanding its intricate structure, key drivers, and emerging opportunities is paramount for strategic planning and competitive advantage. This report delves into both parent and child market segments, providing a holistic view of market evolution.

Our analysis encompasses both seamless steel tubes and welded steel tubes, examining their respective market shares and growth prospects. We also explore the "Others" category for types, ensuring a complete market representation. End-user applications are thoroughly investigated, with a focus on playground equipment and a comprehensive "Others" segment that captures a wide array of industrial uses.

The report leverages extensive data and expert analysis to deliver actionable intelligence, empowering you to navigate the complexities of the mechanical tube and pipe industry.

Mechanical Tube and Pipe Market Dynamics & Structure

The global mechanical tube and pipe market exhibits a moderate concentration, with a mix of large, integrated players and specialized manufacturers. Technological innovation remains a significant driver, particularly in material science, manufacturing processes (e.g., advanced welding techniques, precision forming), and coatings to enhance durability and performance. Regulatory frameworks, encompassing material standards, environmental regulations, and safety certifications, play a crucial role in shaping market entry and product development. Competitive product substitutes, such as alternative materials and engineered components, present a constant challenge, necessitating continuous innovation and cost optimization. End-user demographics are shifting, with a growing demand from infrastructure development, renewable energy projects, and sophisticated manufacturing sectors. Mergers and acquisitions (M&A) are a key feature, with larger entities consolidating market share and acquiring innovative technologies or regional presence.

- Market Concentration: Moderate, with key players holding significant shares.

- Technological Innovation Drivers: Advanced materials, enhanced manufacturing efficiency, and performance coatings.

- Regulatory Frameworks: Strict adherence to international standards and environmental compliance.

- Competitive Product Substitutes: Ongoing threat from alternative materials and engineered solutions.

- End-User Demographics: Growing demand from construction, automotive, energy, and machinery sectors.

- M&A Trends: Strategic acquisitions to expand product portfolios and market reach.

Mechanical Tube and Pipe Growth Trends & Insights

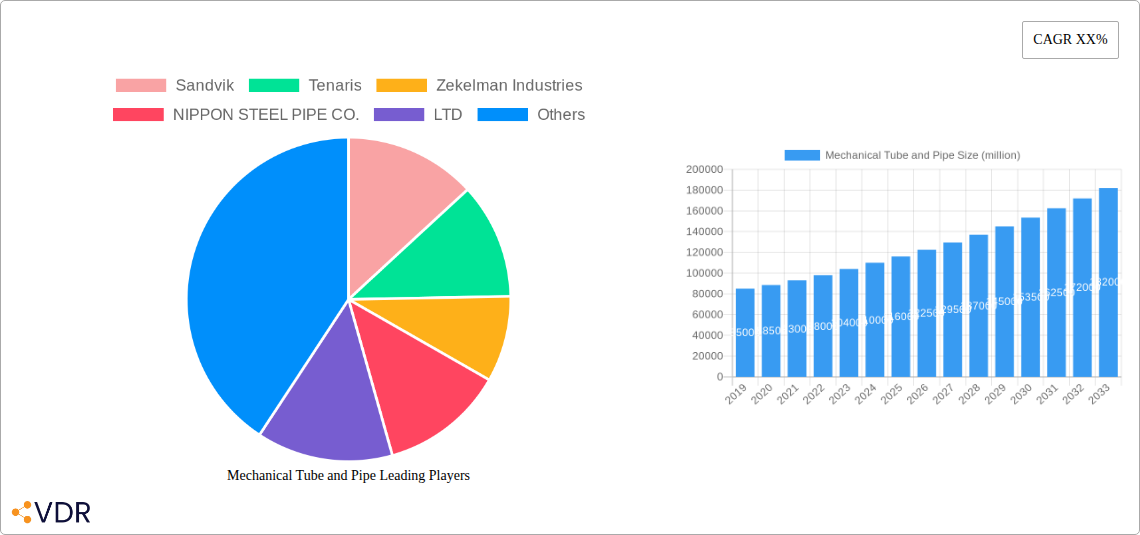

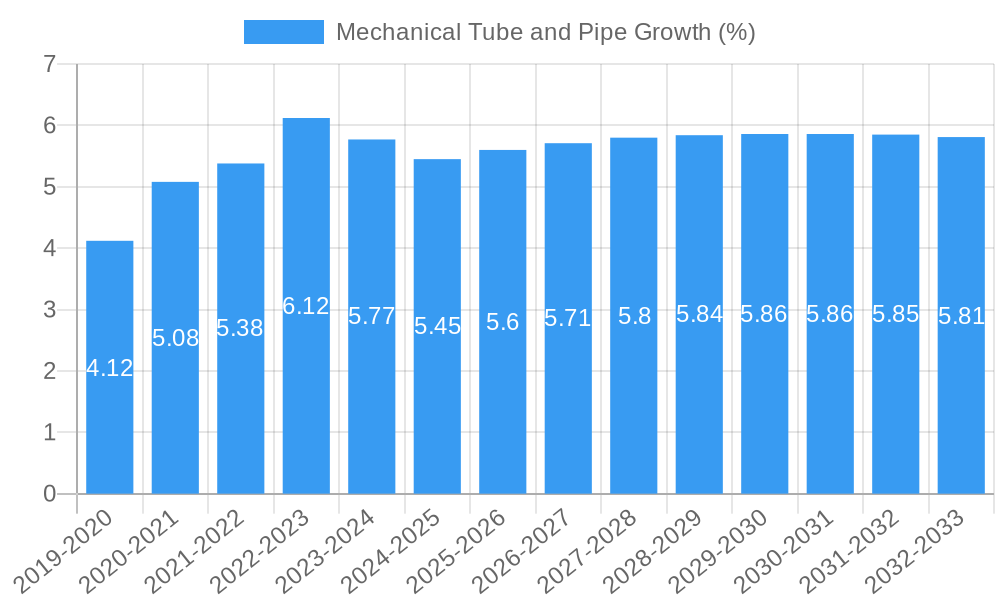

The mechanical tube and pipe market is projected to experience robust growth over the forecast period, driven by increasing industrialization, infrastructure development, and the burgeoning renewable energy sector. The market size evolution is marked by a steady upward trend, reflecting sustained demand across diverse applications. Adoption rates for specialized and high-performance tubes are accelerating as industries seek greater efficiency, durability, and safety. Technological disruptions, such as advancements in automation in manufacturing and the development of novel alloy compositions, are reshaping production capabilities and product offerings. Consumer behavior shifts are evident, with a growing preference for lightweight, high-strength, and sustainable material solutions. The market is anticipated to achieve a Compound Annual Growth Rate (CAGR) of approximately 4.5% during the forecast period. Market penetration is expected to deepen in emerging economies as their manufacturing and construction sectors expand. The total market revenue is estimated to reach $185,500 million by 2033.

- Market Size Evolution: Consistent growth driven by industrial expansion and infrastructure projects.

- Adoption Rates: Increasing demand for specialized tubes and advanced material solutions.

- Technological Disruptions: Automation in manufacturing and development of advanced alloys.

- Consumer Behavior Shifts: Preference for lightweight, high-strength, and sustainable materials.

- CAGR: Estimated at 4.5% for the forecast period.

- Market Penetration: Deepening in emerging economies due to industrialization.

- Total Market Revenue (2033 Estimate): $185,500 million.

Dominant Regions, Countries, or Segments in Mechanical Tube and Pipe

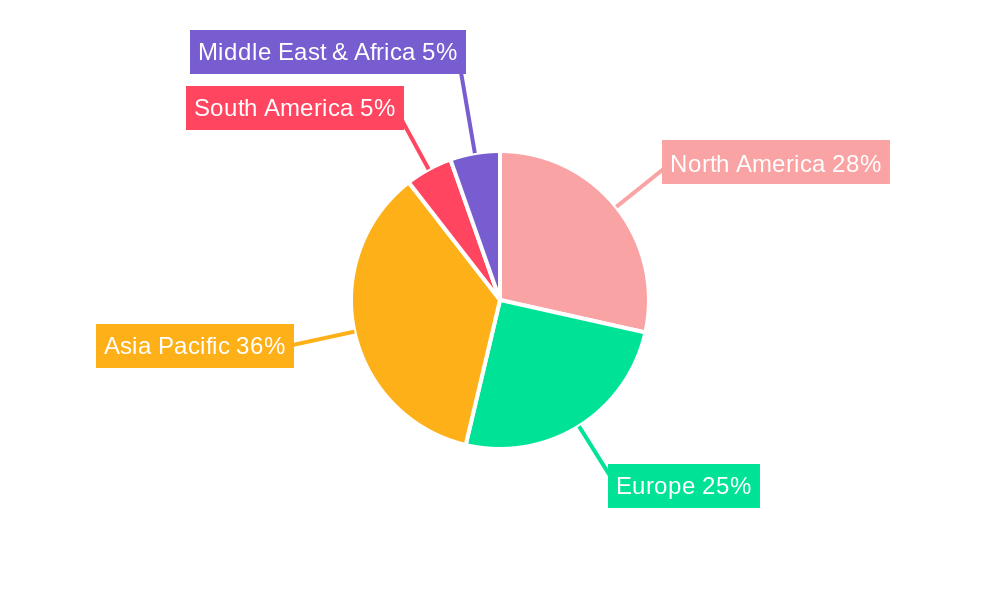

The Machinery application segment is a dominant force in the mechanical tube and pipe market, driven by its pervasive use across various industries, including manufacturing, agriculture, and construction. This segment's dominance stems from the fundamental need for robust and precisely engineered tubing in the construction of industrial equipment, automation systems, and heavy machinery. Key drivers for this segment's growth include ongoing technological advancements in machinery design, a global push for increased manufacturing efficiency, and substantial investments in capital goods. The Asia Pacific region, particularly China and India, stands out as a leading geographical market due to its expansive manufacturing base, significant infrastructure development initiatives, and a growing domestic demand for industrial equipment. Favorable government policies supporting manufacturing and industrial expansion further bolster growth in this region. The market share for the Machinery segment is estimated to be around 35% of the total market value.

- Dominant Application Segment: Machinery, due to its widespread use in industrial equipment and automation.

- Key Drivers for Machinery Segment: Technological advancements in machinery, global manufacturing efficiency initiatives, and capital goods investment.

- Leading Geographical Market: Asia Pacific, driven by strong manufacturing and infrastructure growth.

- Key Countries in Asia Pacific: China and India.

- Dominance Factors in Asia Pacific: Expansive manufacturing base, infrastructure development, and supportive government policies.

- Market Share of Machinery Segment (Estimate): Approximately 35%.

- Growth Potential: High, fueled by ongoing industrialization and automation trends.

Mechanical Tube and Pipe Product Landscape

The mechanical tube and pipe product landscape is characterized by continuous innovation aimed at enhancing performance and expanding application possibilities. Manufacturers are focusing on developing tubes with improved tensile strength, corrosion resistance, and thermal conductivity. Key product innovations include the development of advanced steel alloys for high-temperature applications and the introduction of specialized coatings for enhanced durability in harsh environments. Seamless steel tubes continue to dominate in applications requiring high pressure and precision, while welded steel tubes offer cost-effectiveness and versatility for a broader range of uses. The performance metrics of these products are critical, with a focus on meeting stringent industry standards for dimensional accuracy, material integrity, and load-bearing capacity. Unique selling propositions often lie in tailored solutions, custom fabrication, and superior material properties that cater to specific end-user requirements.

Key Drivers, Barriers & Challenges in Mechanical Tube and Pipe

Key Drivers:

- Infrastructure Development: Global investments in transportation, energy, and construction projects fuel demand for structural and fluid transport tubing.

- Industrial Automation & Machinery: The increasing adoption of automated systems and advanced machinery in manufacturing necessitates high-quality mechanical tubes.

- Renewable Energy Sector Growth: Demand for solar panel supports, wind turbine components, and other energy infrastructure drives growth.

- Automotive Industry Demand: Lightweight and high-strength tubes for vehicle manufacturing, including electric vehicles.

- Technological Advancements: Innovations in material science and manufacturing processes enabling higher performance and specialized applications.

Barriers & Challenges:

- Raw Material Price Volatility: Fluctuations in steel and other alloy prices can impact manufacturing costs and profitability.

- Intense Competition: A fragmented market with numerous players leads to price pressures and margin erosion.

- Stringent Quality and Regulatory Standards: Meeting diverse international and industry-specific standards requires significant investment and compliance efforts.

- Supply Chain Disruptions: Global events and logistical challenges can impact the availability and timely delivery of raw materials and finished products.

- Environmental Regulations: Increasing pressure to adopt sustainable manufacturing practices and reduce carbon footprint.

- Technological Obsolescence: Rapid technological advancements can render existing production facilities and product lines outdated if not continuously upgraded.

Emerging Opportunities in Mechanical Tube and Pipe

Emerging opportunities in the mechanical tube and pipe sector are centered on the increasing demand for specialized, high-performance, and sustainable solutions. The growing focus on energy efficiency and emissions reduction is creating a demand for lightweight tubing in the automotive and aerospace industries. The expansion of renewable energy infrastructure, particularly in solar and wind power, presents significant growth prospects for tubing used in structural supports and energy transmission. Furthermore, the increasing adoption of advanced manufacturing techniques, such as additive manufacturing, for complex tube geometries and customized components, opens new avenues for innovation and niche market development. The trend towards Industry 4.0 and smart factories will also drive demand for tubes used in automated handling systems and sophisticated industrial equipment.

Growth Accelerators in the Mechanical Tube and Pipe Industry

Long-term growth in the mechanical tube and pipe industry will be significantly accelerated by continuous technological breakthroughs in material science, leading to the development of tubes with superior strength-to-weight ratios and enhanced resistance to extreme conditions. Strategic partnerships between raw material suppliers, tube manufacturers, and end-users will foster collaborative innovation and tailor-made solutions, driving market adoption. Market expansion strategies, including tapping into emerging economies with developing industrial bases and focusing on niche applications with high growth potential, will further fuel sustained growth. The circular economy and the increasing emphasis on recycling and sustainable production methods will also act as key growth accelerators, driving the development of eco-friendly manufacturing processes and materials.

Key Players Shaping the Mechanical Tube and Pipe Market

- Sandvik

- Tenaris

- Zekelman Industries

- NIPPON STEEL PIPE CO.,LTD

- U.S. Steel

- ArcelorMittal USA

- Tata Steel

- Salem Tube

- JFE Holdings

- Vallourec

- Nucor

- TimkenSteel

- Mannesmann Stainless Tubes

- Russel Metals

- Atkore

- Cleveland-Cliffs

- Wheatland Tube

- Sharon Tube

- Ryerson

- Valmont Tubing

- Steel Tube Institute

- Industrial Tube and Steel Corporation

- Totten Tubes

- Specialty Pipe & Tube

- Tubular Steel Inc

- EXLTUBE

- T&B Tube

- Harbor Steel

- Wisconsin Steel & Tube

- Nova Steel

Notable Milestones in Mechanical Tube and Pipe Sector

- 2019: Increased investment in advanced welding technologies for higher precision and efficiency.

- 2020: Focus on developing lightweight, high-strength alloys for automotive applications driven by EV growth.

- 2021: Expansion of seamless tube production capacity in emerging markets to meet rising industrial demand.

- 2022: Growing emphasis on sustainable manufacturing practices and reduced carbon footprint in production.

- 2023: Introduction of novel coating technologies to enhance corrosion and wear resistance in harsh environments.

- 2024: Strategic partnerships formed to develop integrated solutions for renewable energy infrastructure.

- 2025 (Estimated): Further advancements in material science leading to tubing for extreme temperature and pressure applications.

- 2026-2033 (Forecast): Continued market growth driven by automation, infrastructure, and specialized applications, with increasing adoption of digital manufacturing.

In-Depth Mechanical Tube and Pipe Market Outlook

- 2019: Increased investment in advanced welding technologies for higher precision and efficiency.

- 2020: Focus on developing lightweight, high-strength alloys for automotive applications driven by EV growth.

- 2021: Expansion of seamless tube production capacity in emerging markets to meet rising industrial demand.

- 2022: Growing emphasis on sustainable manufacturing practices and reduced carbon footprint in production.

- 2023: Introduction of novel coating technologies to enhance corrosion and wear resistance in harsh environments.

- 2024: Strategic partnerships formed to develop integrated solutions for renewable energy infrastructure.

- 2025 (Estimated): Further advancements in material science leading to tubing for extreme temperature and pressure applications.

- 2026-2033 (Forecast): Continued market growth driven by automation, infrastructure, and specialized applications, with increasing adoption of digital manufacturing.

In-Depth Mechanical Tube and Pipe Market Outlook

The future outlook for the mechanical tube and pipe market is exceptionally positive, characterized by sustained growth and evolving opportunities. Key growth accelerators, including relentless technological innovation in material science and manufacturing, will continue to drive the development of high-performance and specialized tubing solutions. Strategic partnerships and market expansion into burgeoning economies will solidify market presence and create new revenue streams. The increasing global emphasis on sustainability and the circular economy will spur the adoption of eco-friendly production methods and materials. The market's trajectory is set to be shaped by ongoing industrial modernization, the expansion of renewable energy infrastructure, and the ever-present demand for robust and reliable components across a multitude of sectors, ensuring a vibrant and dynamic market landscape for years to come.

Mechanical Tube and Pipe Segmentation

-

1. Application

- 1.1. Solar Panel Supports

- 1.2. Conveyor Belt Components

- 1.3. Playground Equipment

- 1.4. Greenhouse Structures

- 1.5. Machinery

- 1.6. Others

-

2. Types

- 2.1. Seamless Steel Tubes

- 2.2. Welded Steel Tubes

- 2.3. Others

Mechanical Tube and Pipe Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Mechanical Tube and Pipe REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Mechanical Tube and Pipe Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Solar Panel Supports

- 5.1.2. Conveyor Belt Components

- 5.1.3. Playground Equipment

- 5.1.4. Greenhouse Structures

- 5.1.5. Machinery

- 5.1.6. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Seamless Steel Tubes

- 5.2.2. Welded Steel Tubes

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Mechanical Tube and Pipe Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Solar Panel Supports

- 6.1.2. Conveyor Belt Components

- 6.1.3. Playground Equipment

- 6.1.4. Greenhouse Structures

- 6.1.5. Machinery

- 6.1.6. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Seamless Steel Tubes

- 6.2.2. Welded Steel Tubes

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Mechanical Tube and Pipe Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Solar Panel Supports

- 7.1.2. Conveyor Belt Components

- 7.1.3. Playground Equipment

- 7.1.4. Greenhouse Structures

- 7.1.5. Machinery

- 7.1.6. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Seamless Steel Tubes

- 7.2.2. Welded Steel Tubes

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Mechanical Tube and Pipe Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Solar Panel Supports

- 8.1.2. Conveyor Belt Components

- 8.1.3. Playground Equipment

- 8.1.4. Greenhouse Structures

- 8.1.5. Machinery

- 8.1.6. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Seamless Steel Tubes

- 8.2.2. Welded Steel Tubes

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Mechanical Tube and Pipe Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Solar Panel Supports

- 9.1.2. Conveyor Belt Components

- 9.1.3. Playground Equipment

- 9.1.4. Greenhouse Structures

- 9.1.5. Machinery

- 9.1.6. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Seamless Steel Tubes

- 9.2.2. Welded Steel Tubes

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Mechanical Tube and Pipe Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Solar Panel Supports

- 10.1.2. Conveyor Belt Components

- 10.1.3. Playground Equipment

- 10.1.4. Greenhouse Structures

- 10.1.5. Machinery

- 10.1.6. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Seamless Steel Tubes

- 10.2.2. Welded Steel Tubes

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Sandvik

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Tenaris

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Zekelman Industries

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 NIPPON STEEL PIPE CO.

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 LTD

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 U.S. Steel

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 ArcelorMittal USA

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Tata Steel

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Salem Tube

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 JFE Holdings

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Vallourec

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Nucor

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 TimkenSteel

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Mannesmann Stainless Tubes

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Russel Metals

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Atkore

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Cleveland-Cliffs

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Wheatland Tube

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Sharon Tube

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Ryerson

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 Valmont Tubing

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 Steel Tube Institute

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.23 Industrial Tube and Steel Corporation

- 11.2.23.1. Overview

- 11.2.23.2. Products

- 11.2.23.3. SWOT Analysis

- 11.2.23.4. Recent Developments

- 11.2.23.5. Financials (Based on Availability)

- 11.2.24 Totten Tubes

- 11.2.24.1. Overview

- 11.2.24.2. Products

- 11.2.24.3. SWOT Analysis

- 11.2.24.4. Recent Developments

- 11.2.24.5. Financials (Based on Availability)

- 11.2.25 Specialty Pipe & Tube

- 11.2.25.1. Overview

- 11.2.25.2. Products

- 11.2.25.3. SWOT Analysis

- 11.2.25.4. Recent Developments

- 11.2.25.5. Financials (Based on Availability)

- 11.2.26 Tubular Steel Inc

- 11.2.26.1. Overview

- 11.2.26.2. Products

- 11.2.26.3. SWOT Analysis

- 11.2.26.4. Recent Developments

- 11.2.26.5. Financials (Based on Availability)

- 11.2.27 EXLTUBE

- 11.2.27.1. Overview

- 11.2.27.2. Products

- 11.2.27.3. SWOT Analysis

- 11.2.27.4. Recent Developments

- 11.2.27.5. Financials (Based on Availability)

- 11.2.28 T&B Tube

- 11.2.28.1. Overview

- 11.2.28.2. Products

- 11.2.28.3. SWOT Analysis

- 11.2.28.4. Recent Developments

- 11.2.28.5. Financials (Based on Availability)

- 11.2.29 Harbor Steel

- 11.2.29.1. Overview

- 11.2.29.2. Products

- 11.2.29.3. SWOT Analysis

- 11.2.29.4. Recent Developments

- 11.2.29.5. Financials (Based on Availability)

- 11.2.30 Wisconsin Steel & Tube

- 11.2.30.1. Overview

- 11.2.30.2. Products

- 11.2.30.3. SWOT Analysis

- 11.2.30.4. Recent Developments

- 11.2.30.5. Financials (Based on Availability)

- 11.2.31 Nova Steel

- 11.2.31.1. Overview

- 11.2.31.2. Products

- 11.2.31.3. SWOT Analysis

- 11.2.31.4. Recent Developments

- 11.2.31.5. Financials (Based on Availability)

- 11.2.1 Sandvik

List of Figures

- Figure 1: Global Mechanical Tube and Pipe Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: Global Mechanical Tube and Pipe Volume Breakdown (K, %) by Region 2024 & 2032

- Figure 3: North America Mechanical Tube and Pipe Revenue (million), by Application 2024 & 2032

- Figure 4: North America Mechanical Tube and Pipe Volume (K), by Application 2024 & 2032

- Figure 5: North America Mechanical Tube and Pipe Revenue Share (%), by Application 2024 & 2032

- Figure 6: North America Mechanical Tube and Pipe Volume Share (%), by Application 2024 & 2032

- Figure 7: North America Mechanical Tube and Pipe Revenue (million), by Types 2024 & 2032

- Figure 8: North America Mechanical Tube and Pipe Volume (K), by Types 2024 & 2032

- Figure 9: North America Mechanical Tube and Pipe Revenue Share (%), by Types 2024 & 2032

- Figure 10: North America Mechanical Tube and Pipe Volume Share (%), by Types 2024 & 2032

- Figure 11: North America Mechanical Tube and Pipe Revenue (million), by Country 2024 & 2032

- Figure 12: North America Mechanical Tube and Pipe Volume (K), by Country 2024 & 2032

- Figure 13: North America Mechanical Tube and Pipe Revenue Share (%), by Country 2024 & 2032

- Figure 14: North America Mechanical Tube and Pipe Volume Share (%), by Country 2024 & 2032

- Figure 15: South America Mechanical Tube and Pipe Revenue (million), by Application 2024 & 2032

- Figure 16: South America Mechanical Tube and Pipe Volume (K), by Application 2024 & 2032

- Figure 17: South America Mechanical Tube and Pipe Revenue Share (%), by Application 2024 & 2032

- Figure 18: South America Mechanical Tube and Pipe Volume Share (%), by Application 2024 & 2032

- Figure 19: South America Mechanical Tube and Pipe Revenue (million), by Types 2024 & 2032

- Figure 20: South America Mechanical Tube and Pipe Volume (K), by Types 2024 & 2032

- Figure 21: South America Mechanical Tube and Pipe Revenue Share (%), by Types 2024 & 2032

- Figure 22: South America Mechanical Tube and Pipe Volume Share (%), by Types 2024 & 2032

- Figure 23: South America Mechanical Tube and Pipe Revenue (million), by Country 2024 & 2032

- Figure 24: South America Mechanical Tube and Pipe Volume (K), by Country 2024 & 2032

- Figure 25: South America Mechanical Tube and Pipe Revenue Share (%), by Country 2024 & 2032

- Figure 26: South America Mechanical Tube and Pipe Volume Share (%), by Country 2024 & 2032

- Figure 27: Europe Mechanical Tube and Pipe Revenue (million), by Application 2024 & 2032

- Figure 28: Europe Mechanical Tube and Pipe Volume (K), by Application 2024 & 2032

- Figure 29: Europe Mechanical Tube and Pipe Revenue Share (%), by Application 2024 & 2032

- Figure 30: Europe Mechanical Tube and Pipe Volume Share (%), by Application 2024 & 2032

- Figure 31: Europe Mechanical Tube and Pipe Revenue (million), by Types 2024 & 2032

- Figure 32: Europe Mechanical Tube and Pipe Volume (K), by Types 2024 & 2032

- Figure 33: Europe Mechanical Tube and Pipe Revenue Share (%), by Types 2024 & 2032

- Figure 34: Europe Mechanical Tube and Pipe Volume Share (%), by Types 2024 & 2032

- Figure 35: Europe Mechanical Tube and Pipe Revenue (million), by Country 2024 & 2032

- Figure 36: Europe Mechanical Tube and Pipe Volume (K), by Country 2024 & 2032

- Figure 37: Europe Mechanical Tube and Pipe Revenue Share (%), by Country 2024 & 2032

- Figure 38: Europe Mechanical Tube and Pipe Volume Share (%), by Country 2024 & 2032

- Figure 39: Middle East & Africa Mechanical Tube and Pipe Revenue (million), by Application 2024 & 2032

- Figure 40: Middle East & Africa Mechanical Tube and Pipe Volume (K), by Application 2024 & 2032

- Figure 41: Middle East & Africa Mechanical Tube and Pipe Revenue Share (%), by Application 2024 & 2032

- Figure 42: Middle East & Africa Mechanical Tube and Pipe Volume Share (%), by Application 2024 & 2032

- Figure 43: Middle East & Africa Mechanical Tube and Pipe Revenue (million), by Types 2024 & 2032

- Figure 44: Middle East & Africa Mechanical Tube and Pipe Volume (K), by Types 2024 & 2032

- Figure 45: Middle East & Africa Mechanical Tube and Pipe Revenue Share (%), by Types 2024 & 2032

- Figure 46: Middle East & Africa Mechanical Tube and Pipe Volume Share (%), by Types 2024 & 2032

- Figure 47: Middle East & Africa Mechanical Tube and Pipe Revenue (million), by Country 2024 & 2032

- Figure 48: Middle East & Africa Mechanical Tube and Pipe Volume (K), by Country 2024 & 2032

- Figure 49: Middle East & Africa Mechanical Tube and Pipe Revenue Share (%), by Country 2024 & 2032

- Figure 50: Middle East & Africa Mechanical Tube and Pipe Volume Share (%), by Country 2024 & 2032

- Figure 51: Asia Pacific Mechanical Tube and Pipe Revenue (million), by Application 2024 & 2032

- Figure 52: Asia Pacific Mechanical Tube and Pipe Volume (K), by Application 2024 & 2032

- Figure 53: Asia Pacific Mechanical Tube and Pipe Revenue Share (%), by Application 2024 & 2032

- Figure 54: Asia Pacific Mechanical Tube and Pipe Volume Share (%), by Application 2024 & 2032

- Figure 55: Asia Pacific Mechanical Tube and Pipe Revenue (million), by Types 2024 & 2032

- Figure 56: Asia Pacific Mechanical Tube and Pipe Volume (K), by Types 2024 & 2032

- Figure 57: Asia Pacific Mechanical Tube and Pipe Revenue Share (%), by Types 2024 & 2032

- Figure 58: Asia Pacific Mechanical Tube and Pipe Volume Share (%), by Types 2024 & 2032

- Figure 59: Asia Pacific Mechanical Tube and Pipe Revenue (million), by Country 2024 & 2032

- Figure 60: Asia Pacific Mechanical Tube and Pipe Volume (K), by Country 2024 & 2032

- Figure 61: Asia Pacific Mechanical Tube and Pipe Revenue Share (%), by Country 2024 & 2032

- Figure 62: Asia Pacific Mechanical Tube and Pipe Volume Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Mechanical Tube and Pipe Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Mechanical Tube and Pipe Volume K Forecast, by Region 2019 & 2032

- Table 3: Global Mechanical Tube and Pipe Revenue million Forecast, by Application 2019 & 2032

- Table 4: Global Mechanical Tube and Pipe Volume K Forecast, by Application 2019 & 2032

- Table 5: Global Mechanical Tube and Pipe Revenue million Forecast, by Types 2019 & 2032

- Table 6: Global Mechanical Tube and Pipe Volume K Forecast, by Types 2019 & 2032

- Table 7: Global Mechanical Tube and Pipe Revenue million Forecast, by Region 2019 & 2032

- Table 8: Global Mechanical Tube and Pipe Volume K Forecast, by Region 2019 & 2032

- Table 9: Global Mechanical Tube and Pipe Revenue million Forecast, by Application 2019 & 2032

- Table 10: Global Mechanical Tube and Pipe Volume K Forecast, by Application 2019 & 2032

- Table 11: Global Mechanical Tube and Pipe Revenue million Forecast, by Types 2019 & 2032

- Table 12: Global Mechanical Tube and Pipe Volume K Forecast, by Types 2019 & 2032

- Table 13: Global Mechanical Tube and Pipe Revenue million Forecast, by Country 2019 & 2032

- Table 14: Global Mechanical Tube and Pipe Volume K Forecast, by Country 2019 & 2032

- Table 15: United States Mechanical Tube and Pipe Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: United States Mechanical Tube and Pipe Volume (K) Forecast, by Application 2019 & 2032

- Table 17: Canada Mechanical Tube and Pipe Revenue (million) Forecast, by Application 2019 & 2032

- Table 18: Canada Mechanical Tube and Pipe Volume (K) Forecast, by Application 2019 & 2032

- Table 19: Mexico Mechanical Tube and Pipe Revenue (million) Forecast, by Application 2019 & 2032

- Table 20: Mexico Mechanical Tube and Pipe Volume (K) Forecast, by Application 2019 & 2032

- Table 21: Global Mechanical Tube and Pipe Revenue million Forecast, by Application 2019 & 2032

- Table 22: Global Mechanical Tube and Pipe Volume K Forecast, by Application 2019 & 2032

- Table 23: Global Mechanical Tube and Pipe Revenue million Forecast, by Types 2019 & 2032

- Table 24: Global Mechanical Tube and Pipe Volume K Forecast, by Types 2019 & 2032

- Table 25: Global Mechanical Tube and Pipe Revenue million Forecast, by Country 2019 & 2032

- Table 26: Global Mechanical Tube and Pipe Volume K Forecast, by Country 2019 & 2032

- Table 27: Brazil Mechanical Tube and Pipe Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Brazil Mechanical Tube and Pipe Volume (K) Forecast, by Application 2019 & 2032

- Table 29: Argentina Mechanical Tube and Pipe Revenue (million) Forecast, by Application 2019 & 2032

- Table 30: Argentina Mechanical Tube and Pipe Volume (K) Forecast, by Application 2019 & 2032

- Table 31: Rest of South America Mechanical Tube and Pipe Revenue (million) Forecast, by Application 2019 & 2032

- Table 32: Rest of South America Mechanical Tube and Pipe Volume (K) Forecast, by Application 2019 & 2032

- Table 33: Global Mechanical Tube and Pipe Revenue million Forecast, by Application 2019 & 2032

- Table 34: Global Mechanical Tube and Pipe Volume K Forecast, by Application 2019 & 2032

- Table 35: Global Mechanical Tube and Pipe Revenue million Forecast, by Types 2019 & 2032

- Table 36: Global Mechanical Tube and Pipe Volume K Forecast, by Types 2019 & 2032

- Table 37: Global Mechanical Tube and Pipe Revenue million Forecast, by Country 2019 & 2032

- Table 38: Global Mechanical Tube and Pipe Volume K Forecast, by Country 2019 & 2032

- Table 39: United Kingdom Mechanical Tube and Pipe Revenue (million) Forecast, by Application 2019 & 2032

- Table 40: United Kingdom Mechanical Tube and Pipe Volume (K) Forecast, by Application 2019 & 2032

- Table 41: Germany Mechanical Tube and Pipe Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: Germany Mechanical Tube and Pipe Volume (K) Forecast, by Application 2019 & 2032

- Table 43: France Mechanical Tube and Pipe Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: France Mechanical Tube and Pipe Volume (K) Forecast, by Application 2019 & 2032

- Table 45: Italy Mechanical Tube and Pipe Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Italy Mechanical Tube and Pipe Volume (K) Forecast, by Application 2019 & 2032

- Table 47: Spain Mechanical Tube and Pipe Revenue (million) Forecast, by Application 2019 & 2032

- Table 48: Spain Mechanical Tube and Pipe Volume (K) Forecast, by Application 2019 & 2032

- Table 49: Russia Mechanical Tube and Pipe Revenue (million) Forecast, by Application 2019 & 2032

- Table 50: Russia Mechanical Tube and Pipe Volume (K) Forecast, by Application 2019 & 2032

- Table 51: Benelux Mechanical Tube and Pipe Revenue (million) Forecast, by Application 2019 & 2032

- Table 52: Benelux Mechanical Tube and Pipe Volume (K) Forecast, by Application 2019 & 2032

- Table 53: Nordics Mechanical Tube and Pipe Revenue (million) Forecast, by Application 2019 & 2032

- Table 54: Nordics Mechanical Tube and Pipe Volume (K) Forecast, by Application 2019 & 2032

- Table 55: Rest of Europe Mechanical Tube and Pipe Revenue (million) Forecast, by Application 2019 & 2032

- Table 56: Rest of Europe Mechanical Tube and Pipe Volume (K) Forecast, by Application 2019 & 2032

- Table 57: Global Mechanical Tube and Pipe Revenue million Forecast, by Application 2019 & 2032

- Table 58: Global Mechanical Tube and Pipe Volume K Forecast, by Application 2019 & 2032

- Table 59: Global Mechanical Tube and Pipe Revenue million Forecast, by Types 2019 & 2032

- Table 60: Global Mechanical Tube and Pipe Volume K Forecast, by Types 2019 & 2032

- Table 61: Global Mechanical Tube and Pipe Revenue million Forecast, by Country 2019 & 2032

- Table 62: Global Mechanical Tube and Pipe Volume K Forecast, by Country 2019 & 2032

- Table 63: Turkey Mechanical Tube and Pipe Revenue (million) Forecast, by Application 2019 & 2032

- Table 64: Turkey Mechanical Tube and Pipe Volume (K) Forecast, by Application 2019 & 2032

- Table 65: Israel Mechanical Tube and Pipe Revenue (million) Forecast, by Application 2019 & 2032

- Table 66: Israel Mechanical Tube and Pipe Volume (K) Forecast, by Application 2019 & 2032

- Table 67: GCC Mechanical Tube and Pipe Revenue (million) Forecast, by Application 2019 & 2032

- Table 68: GCC Mechanical Tube and Pipe Volume (K) Forecast, by Application 2019 & 2032

- Table 69: North Africa Mechanical Tube and Pipe Revenue (million) Forecast, by Application 2019 & 2032

- Table 70: North Africa Mechanical Tube and Pipe Volume (K) Forecast, by Application 2019 & 2032

- Table 71: South Africa Mechanical Tube and Pipe Revenue (million) Forecast, by Application 2019 & 2032

- Table 72: South Africa Mechanical Tube and Pipe Volume (K) Forecast, by Application 2019 & 2032

- Table 73: Rest of Middle East & Africa Mechanical Tube and Pipe Revenue (million) Forecast, by Application 2019 & 2032

- Table 74: Rest of Middle East & Africa Mechanical Tube and Pipe Volume (K) Forecast, by Application 2019 & 2032

- Table 75: Global Mechanical Tube and Pipe Revenue million Forecast, by Application 2019 & 2032

- Table 76: Global Mechanical Tube and Pipe Volume K Forecast, by Application 2019 & 2032

- Table 77: Global Mechanical Tube and Pipe Revenue million Forecast, by Types 2019 & 2032

- Table 78: Global Mechanical Tube and Pipe Volume K Forecast, by Types 2019 & 2032

- Table 79: Global Mechanical Tube and Pipe Revenue million Forecast, by Country 2019 & 2032

- Table 80: Global Mechanical Tube and Pipe Volume K Forecast, by Country 2019 & 2032

- Table 81: China Mechanical Tube and Pipe Revenue (million) Forecast, by Application 2019 & 2032

- Table 82: China Mechanical Tube and Pipe Volume (K) Forecast, by Application 2019 & 2032

- Table 83: India Mechanical Tube and Pipe Revenue (million) Forecast, by Application 2019 & 2032

- Table 84: India Mechanical Tube and Pipe Volume (K) Forecast, by Application 2019 & 2032

- Table 85: Japan Mechanical Tube and Pipe Revenue (million) Forecast, by Application 2019 & 2032

- Table 86: Japan Mechanical Tube and Pipe Volume (K) Forecast, by Application 2019 & 2032

- Table 87: South Korea Mechanical Tube and Pipe Revenue (million) Forecast, by Application 2019 & 2032

- Table 88: South Korea Mechanical Tube and Pipe Volume (K) Forecast, by Application 2019 & 2032

- Table 89: ASEAN Mechanical Tube and Pipe Revenue (million) Forecast, by Application 2019 & 2032

- Table 90: ASEAN Mechanical Tube and Pipe Volume (K) Forecast, by Application 2019 & 2032

- Table 91: Oceania Mechanical Tube and Pipe Revenue (million) Forecast, by Application 2019 & 2032

- Table 92: Oceania Mechanical Tube and Pipe Volume (K) Forecast, by Application 2019 & 2032

- Table 93: Rest of Asia Pacific Mechanical Tube and Pipe Revenue (million) Forecast, by Application 2019 & 2032

- Table 94: Rest of Asia Pacific Mechanical Tube and Pipe Volume (K) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Mechanical Tube and Pipe?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the Mechanical Tube and Pipe?

Key companies in the market include Sandvik, Tenaris, Zekelman Industries, NIPPON STEEL PIPE CO., LTD, U.S. Steel, ArcelorMittal USA, Tata Steel, Salem Tube, JFE Holdings, Vallourec, Nucor, TimkenSteel, Mannesmann Stainless Tubes, Russel Metals, Atkore, Cleveland-Cliffs, Wheatland Tube, Sharon Tube, Ryerson, Valmont Tubing, Steel Tube Institute, Industrial Tube and Steel Corporation, Totten Tubes, Specialty Pipe & Tube, Tubular Steel Inc, EXLTUBE, T&B Tube, Harbor Steel, Wisconsin Steel & Tube, Nova Steel.

3. What are the main segments of the Mechanical Tube and Pipe?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Mechanical Tube and Pipe," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Mechanical Tube and Pipe report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Mechanical Tube and Pipe?

To stay informed about further developments, trends, and reports in the Mechanical Tube and Pipe, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence