Key Insights

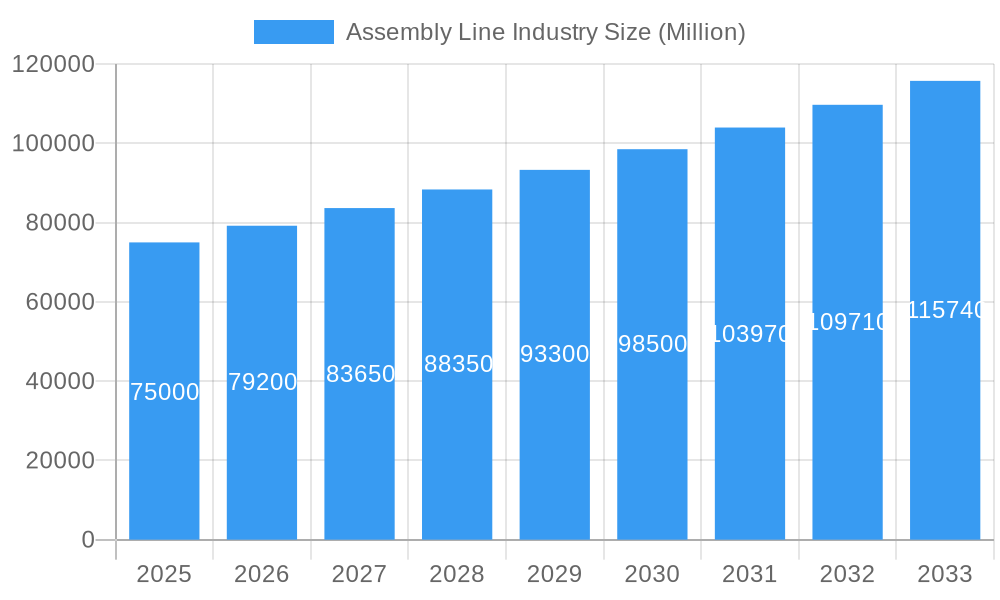

The global Assembly Line Industry is projected for substantial growth, expected to reach a market size of $307.15 billion by 2025. The industry anticipates a Compound Annual Growth Rate (CAGR) of 7.85% from 2025 to 2033. This expansion is largely attributed to the rising adoption of automation in manufacturing, driven by the imperative for enhanced efficiency, superior product quality, and reduced operational expenses. Key catalysts include the widespread embrace of Industry 4.0 principles, smart factory implementations, and the integration of cutting-edge technologies such as robotics, artificial intelligence (AI), and the Internet of Things (IoT) into assembly operations. Moreover, the increasing complexity of products across automotive, electronics, and medical device sectors necessitates advanced and adaptable assembly line solutions.

Assembly Line Industry Market Size (In Billion)

Emerging trends shaping the industry include the proliferation of collaborative robots (cobots) for improved human-robot synergy, the development of modular and flexible assembly line designs to cater to diverse product portfolios, and a growing emphasis on sustainability through efficient resource management and waste minimization. Potential challenges, such as significant upfront investments in advanced automation, the requirement for a skilled workforce proficient in operating and maintaining sophisticated systems, and cybersecurity risks associated with interconnected factories, may influence the adoption rate in certain market segments. The market is segmented by type into Manual Assembly Lines, Semi-automated Assembly Lines, and Fully Automated Assembly Lines, with Fully Automated Assembly Lines exhibiting the most significant growth momentum. Leading end-user segments include Automotive, Industrial Manufacturing, and Electronics and Semiconductors, while the Medical & Pharmaceutical sector presents considerable growth potential due to stringent quality mandates.

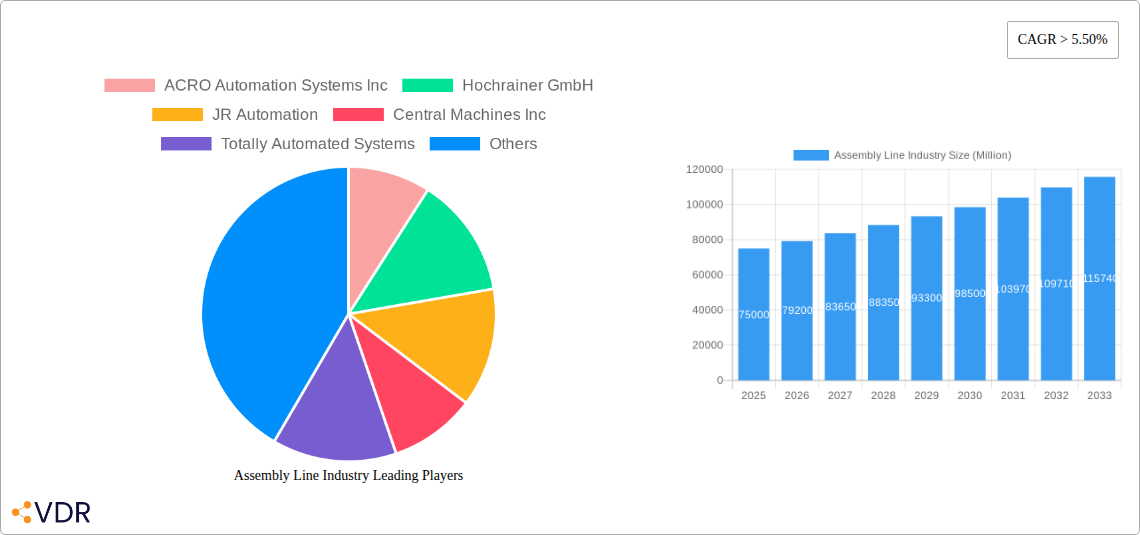

Assembly Line Industry Company Market Share

Assembly Line Industry: Comprehensive Market Analysis & Forecast (2019-2033)

This in-depth report provides a comprehensive analysis of the global Assembly Line Industry, covering market dynamics, growth trends, regional dominance, product innovations, key players, and emerging opportunities. With a detailed forecast period from 2025 to 2033, this report offers actionable insights for stakeholders seeking to navigate and capitalize on the evolving landscape of automated and manual assembly solutions. We delve into the parent market of Industrial Automation and the child market of Robotics in Manufacturing, providing a holistic view of the assembly line ecosystem.

Assembly Line Industry Market Dynamics & Structure

The global Assembly Line Industry is characterized by a moderate level of market concentration, with key players investing heavily in technological innovation and strategic mergers and acquisitions to expand their global footprint. The primary drivers of technological innovation include advancements in robotics, artificial intelligence (AI), the Internet of Things (IoT) for enhanced connectivity and data analytics, and sophisticated vision systems for quality control. Regulatory frameworks, while varied by region, are increasingly focusing on workplace safety, efficiency standards, and environmental sustainability, influencing the adoption of specific assembly line types. Competitive product substitutes, such as advanced manufacturing techniques like 3D printing and modular production systems, are emerging, posing a challenge to traditional assembly line models, particularly in niche applications. End-user demographics are shifting, with a growing demand for customized products and shorter production cycles, necessitating more flexible and agile assembly line solutions. Mergers and acquisitions (M&A) trends are prominent, with larger integrators acquiring smaller, specialized technology providers to enhance their service offerings and market reach. For instance, the consolidation under the JR Automation brand, uniting five divisional brands, signifies a strategic move towards streamlined operations and a unified market presence.

- Market Concentration: Moderate, with a few large integrators and numerous specialized providers.

- Technological Innovation Drivers: AI, IoT, advanced robotics, machine vision.

- Regulatory Frameworks: Focus on safety, efficiency, and sustainability.

- Competitive Product Substitutes: 3D printing, modular production.

- End-User Demographics: Demand for customization and faster production cycles.

- M&A Trends: Strategic acquisitions to enhance capabilities and market reach.

Assembly Line Industry Growth Trends & Insights

The Assembly Line Industry is poised for significant growth driven by increasing industrialization, the relentless pursuit of operational efficiency, and the imperative to enhance product quality across various sectors. The base year 2025 estimates the market size at approximately $XX,XXX million units, with a projected Compound Annual Growth Rate (CAGR) of XX.X% during the forecast period of 2025–2033. This robust growth is fueled by the accelerating adoption of automation in manufacturing processes, particularly in emerging economies seeking to bridge technological gaps and improve competitiveness. Technological disruptions, such as the integration of collaborative robots (cobots) and AI-powered quality inspection systems, are reshaping assembly line capabilities, enabling greater flexibility and precision. Consumer behavior shifts towards personalized products and faster delivery times are compelling manufacturers to invest in adaptable assembly line configurations. The historical period from 2019–2024 witnessed a steady expansion, despite global economic fluctuations, underscoring the intrinsic demand for efficient production solutions. The market penetration of fully automated assembly lines is expected to surge, capturing a larger share from manual and semi-automated systems as the cost-benefit analysis becomes increasingly favorable for businesses. The integration of digital twin technology for simulation and optimization of assembly lines is also a key trend enhancing efficiency and reducing downtime.

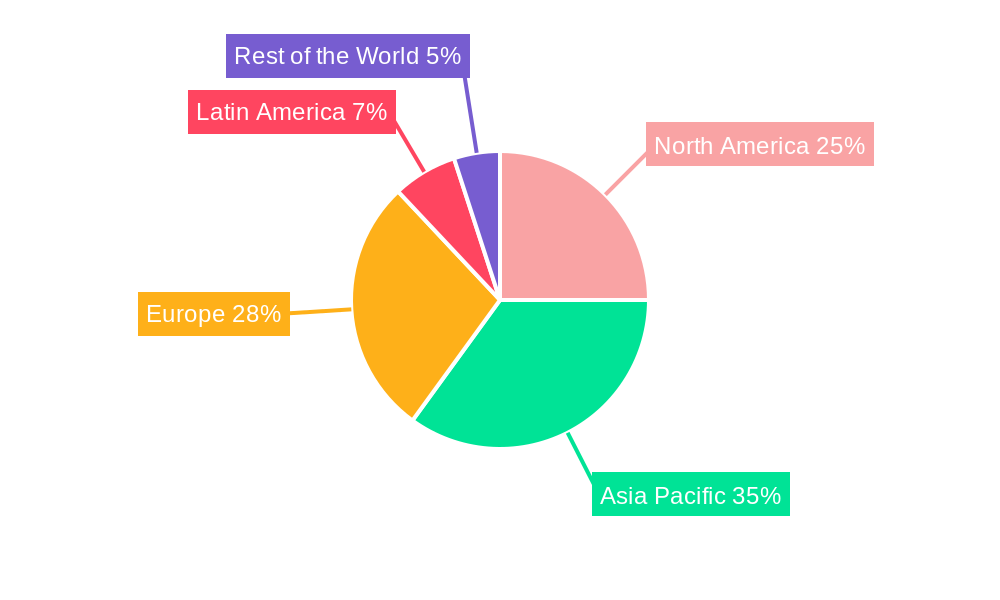

Dominant Regions, Countries, or Segments in Assembly Line Industry

The Automotive segment is consistently a dominant force within the Assembly Line Industry, driven by the sector's high production volumes, complex manufacturing processes, and continuous innovation in vehicle design and technology. This segment accounts for an estimated XX% of the global assembly line market share in 2025. The region of Asia Pacific is expected to lead global market growth, propelled by rapid industrialization in countries like China and India, significant investments in manufacturing infrastructure, and a strong government focus on technological advancement. The country of China alone represents a substantial portion of this regional dominance, acting as both a major consumer and producer of assembly line solutions.

Dominant Segment: Automotive

- Key Drivers: High production volumes, demand for advanced safety features, electric vehicle (EV) production growth, stringent quality control requirements.

- Market Share (Automotive Segment): Estimated at XX% in 2025.

- Growth Potential: Continued expansion driven by new vehicle launches and evolving manufacturing techniques.

Dominant Region: Asia Pacific

- Key Drivers: Rapid industrialization, government support for manufacturing, growing middle class, increasing FDI in manufacturing sectors, expansion of electronics and automotive hubs.

- Market Share (Asia Pacific Region): Estimated to reach XX% of the global market by 2033.

- Growth Potential: High, fueled by continued economic development and adoption of advanced manufacturing technologies.

Dominant Country: China

- Key Drivers: World's largest manufacturing base, significant government incentives for automation, robust domestic demand, key player in global supply chains for electronics and automotive components.

- Market Share (China Country): Estimated to represent XX% of the Asia Pacific market.

- Growth Potential: Sustained growth driven by Industry 4.0 initiatives and smart factory implementations.

The Fully Automated Assembly Lines segment is projected to experience the highest growth rate, driven by the increasing need for precision, speed, and cost reduction in mass production environments. The Industrial Manufacturing end-user segment also plays a crucial role, with its diverse applications across various sub-sectors contributing significantly to market expansion.

Assembly Line Industry Product Landscape

The product landscape of the Assembly Line Industry is evolving rapidly, with innovations focused on enhancing flexibility, efficiency, and intelligence. Key product developments include the integration of advanced robotics, such as collaborative robots (cobots) that can work alongside human operators, and sophisticated AI-driven vision systems for real-time quality inspection and defect detection. Modular assembly line designs are gaining traction, allowing for quick reconfiguration to accommodate different product variants and production volumes. Furthermore, the incorporation of IoT sensors and data analytics platforms enables predictive maintenance, real-time performance monitoring, and optimized production scheduling. These advancements are critical for meeting the increasing demand for customized products and shorter lead times across industries like automotive, electronics, and medical devices. The performance metrics that manufacturers prioritize include throughput, uptime, accuracy, and energy efficiency, all of which are being continuously improved through these technological advancements.

Key Drivers, Barriers & Challenges in Assembly Line Industry

The Assembly Line Industry is propelled by several key drivers. The ever-increasing demand for operational efficiency and cost reduction in manufacturing is a primary catalyst. Advancements in robotics, AI, and IoT are enabling more sophisticated and adaptable automation solutions. Government initiatives promoting industrial automation and smart manufacturing further bolster market growth. The need for enhanced product quality and precision, particularly in sectors like automotive and medical devices, also drives adoption.

However, significant barriers and challenges exist. The substantial initial investment required for advanced assembly line automation can be prohibitive for small and medium-sized enterprises (SMEs). A shortage of skilled labor capable of operating, maintaining, and programming these complex systems presents a critical hurdle. Cybersecurity concerns related to interconnected automated systems also pose a risk. Supply chain disruptions, as seen in recent global events, can impact the availability of critical components, while evolving regulatory landscapes can add complexity to implementation. Competitive pressures and the need for continuous innovation to stay ahead also present challenges.

Emerging Opportunities in Assembly Line Industry

Emerging opportunities within the Assembly Line Industry lie in the increasing adoption of automation in niche and high-growth sectors. The Medical & Pharmaceutical industry presents a significant untapped market, driven by the demand for sterile, high-precision assembly of medical devices and pharmaceuticals, where strict regulatory compliance is paramount. The "Industry 5.0" paradigm, emphasizing human-robot collaboration and personalization, opens avenues for more intuitive and adaptive assembly line solutions that prioritize human well-being and creativity. Furthermore, the growing trend of reshoring manufacturing activities in developed economies, coupled with the need for localized, flexible production, creates demand for advanced, agile assembly line systems. The development of AI-powered predictive analytics for assembly line optimization and defect prevention offers a substantial opportunity for service providers.

Growth Accelerators in the Assembly Line Industry Industry

Several key catalysts are accelerating long-term growth in the Assembly Line Industry. Technological breakthroughs in areas such as machine learning for process optimization, advanced sensor technology for real-time monitoring, and next-generation robotics are continuously enhancing the capabilities and efficiency of assembly lines. Strategic partnerships between technology providers, system integrators, and end-users are crucial for developing tailored solutions and facilitating wider adoption. Market expansion strategies, particularly the focus on developing economies and emerging industrial hubs, are opening up new revenue streams and driving global demand. The increasing integration of simulation and digital twin technologies to de-risk and optimize line design and operation before physical implementation also acts as a significant growth accelerator, reducing implementation time and costs.

Key Players Shaping the Assembly Line Industry Market

- ACRO Automation Systems Inc

- Hochrainer GmbH

- JR Automation

- Central Machines Inc

- Totally Automated Systems

- Fusion Systems Group

- Adescor Inc

- Gemtec GmbH

- Markone Control Systems

- Eriez Manufacturing Co

- NEVMAT Australia PTY LTD

- RNA Automation

- UMD Automated Systems

- Mondragon Assembly

- Hitachi Power Solutions Co Ltd

- MechTech Automation Group

- RG-Luma Automation

- BBS Automation

- SITEC Industrietechnologie GmbH

Notable Milestones in Assembly Line Industry Sector

- May 2021: Mondragon Assembly expands into the USA market with a new subsidiary in Chicago, aiming to provide closer and personalized service to American customers.

- August 2021: JR Automation, a subsidiary of Hitachi, Ltd., announces the unification of its five divisional brands (JR Automation, Esys Automation, Setpoint, FSA Technologies, and PSB Technologies) under a single corporate identity, JR Automation, to streamline operations and enhance market presence.

In-Depth Assembly Line Industry Market Outlook

The Assembly Line Industry outlook remains exceptionally positive, fueled by ongoing industrial transformation and the persistent demand for optimized production processes. Growth accelerators such as advancements in AI, robotics, and the adoption of Industry 4.0 principles are creating more intelligent, flexible, and efficient assembly lines. Strategic partnerships and market expansion into burgeoning industrial regions will continue to drive demand. The increasing focus on sustainability and worker well-being within manufacturing environments will also shape the development of new assembly line technologies. The ongoing evolution of the automotive sector, particularly the shift towards electric vehicles, and the expanding needs of the medical and pharmaceutical industries present significant opportunities for innovation and market penetration. Consequently, the market is projected for sustained robust growth, offering substantial potential for stakeholders to invest and innovate.

Assembly Line Industry Segmentation

-

1. Type

- 1.1. Manual Assembly Lines

- 1.2. Semi-automated Assembly Lines

- 1.3. Fully Automated Assembly Lines

-

2. End-user

- 2.1. Automotive

- 2.2. Industrial Manufacturing

- 2.3. Electronics and Semiconductors

- 2.4. Medical & Pharmaceutical

- 2.5. Others

Assembly Line Industry Segmentation By Geography

- 1. North America

- 2. Asia Pacific

- 3. Europe

- 4. Latin America

- 5. Rest of the World

Assembly Line Industry Regional Market Share

Geographic Coverage of Assembly Line Industry

Assembly Line Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.85% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Manual Assembly Lines

- 5.1.2. Semi-automated Assembly Lines

- 5.1.3. Fully Automated Assembly Lines

- 5.2. Market Analysis, Insights and Forecast - by End-user

- 5.2.1. Automotive

- 5.2.2. Industrial Manufacturing

- 5.2.3. Electronics and Semiconductors

- 5.2.4. Medical & Pharmaceutical

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Asia Pacific

- 5.3.3. Europe

- 5.3.4. Latin America

- 5.3.5. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Assembly Line Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Manual Assembly Lines

- 6.1.2. Semi-automated Assembly Lines

- 6.1.3. Fully Automated Assembly Lines

- 6.2. Market Analysis, Insights and Forecast - by End-user

- 6.2.1. Automotive

- 6.2.2. Industrial Manufacturing

- 6.2.3. Electronics and Semiconductors

- 6.2.4. Medical & Pharmaceutical

- 6.2.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Assembly Line Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Manual Assembly Lines

- 7.1.2. Semi-automated Assembly Lines

- 7.1.3. Fully Automated Assembly Lines

- 7.2. Market Analysis, Insights and Forecast - by End-user

- 7.2.1. Automotive

- 7.2.2. Industrial Manufacturing

- 7.2.3. Electronics and Semiconductors

- 7.2.4. Medical & Pharmaceutical

- 7.2.5. Others

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Asia Pacific Assembly Line Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Manual Assembly Lines

- 8.1.2. Semi-automated Assembly Lines

- 8.1.3. Fully Automated Assembly Lines

- 8.2. Market Analysis, Insights and Forecast - by End-user

- 8.2.1. Automotive

- 8.2.2. Industrial Manufacturing

- 8.2.3. Electronics and Semiconductors

- 8.2.4. Medical & Pharmaceutical

- 8.2.5. Others

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Europe Assembly Line Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Manual Assembly Lines

- 9.1.2. Semi-automated Assembly Lines

- 9.1.3. Fully Automated Assembly Lines

- 9.2. Market Analysis, Insights and Forecast - by End-user

- 9.2.1. Automotive

- 9.2.2. Industrial Manufacturing

- 9.2.3. Electronics and Semiconductors

- 9.2.4. Medical & Pharmaceutical

- 9.2.5. Others

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Latin America Assembly Line Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Manual Assembly Lines

- 10.1.2. Semi-automated Assembly Lines

- 10.1.3. Fully Automated Assembly Lines

- 10.2. Market Analysis, Insights and Forecast - by End-user

- 10.2.1. Automotive

- 10.2.2. Industrial Manufacturing

- 10.2.3. Electronics and Semiconductors

- 10.2.4. Medical & Pharmaceutical

- 10.2.5. Others

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Rest of the World Assembly Line Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Manual Assembly Lines

- 11.1.2. Semi-automated Assembly Lines

- 11.1.3. Fully Automated Assembly Lines

- 11.2. Market Analysis, Insights and Forecast - by End-user

- 11.2.1. Automotive

- 11.2.2. Industrial Manufacturing

- 11.2.3. Electronics and Semiconductors

- 11.2.4. Medical & Pharmaceutical

- 11.2.5. Others

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 ACRO Automation Systems Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Hochrainer GmbH

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 JR Automation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Central Machines Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Totally Automated Systems

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Fusion Systems Group

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Adescor Inc

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Gemtec GmbH

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Markone Control Systems

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Eriez Manufacturing Co

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 NEVMAT Australia PTY LTD

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 RNA Automation

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 UMD Automated Systems

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Mondragon Assembly

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Hitachi Power Solutions Co Ltd

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 MechTech Automation Group

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 RG-Luma Automation

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 BBS Automation

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.19 SITEC Industrietechnologie GmbH**List Not Exhaustive

- 12.1.19.1. Company Overview

- 12.1.19.2. Products

- 12.1.19.3. Company Financials

- 12.1.19.4. SWOT Analysis

- 12.1.1 ACRO Automation Systems Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Assembly Line Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Assembly Line Industry Revenue (billion), by Type 2025 & 2033

- Figure 3: North America Assembly Line Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America Assembly Line Industry Revenue (billion), by End-user 2025 & 2033

- Figure 5: North America Assembly Line Industry Revenue Share (%), by End-user 2025 & 2033

- Figure 6: North America Assembly Line Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Assembly Line Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Asia Pacific Assembly Line Industry Revenue (billion), by Type 2025 & 2033

- Figure 9: Asia Pacific Assembly Line Industry Revenue Share (%), by Type 2025 & 2033

- Figure 10: Asia Pacific Assembly Line Industry Revenue (billion), by End-user 2025 & 2033

- Figure 11: Asia Pacific Assembly Line Industry Revenue Share (%), by End-user 2025 & 2033

- Figure 12: Asia Pacific Assembly Line Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Asia Pacific Assembly Line Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Assembly Line Industry Revenue (billion), by Type 2025 & 2033

- Figure 15: Europe Assembly Line Industry Revenue Share (%), by Type 2025 & 2033

- Figure 16: Europe Assembly Line Industry Revenue (billion), by End-user 2025 & 2033

- Figure 17: Europe Assembly Line Industry Revenue Share (%), by End-user 2025 & 2033

- Figure 18: Europe Assembly Line Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Assembly Line Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Latin America Assembly Line Industry Revenue (billion), by Type 2025 & 2033

- Figure 21: Latin America Assembly Line Industry Revenue Share (%), by Type 2025 & 2033

- Figure 22: Latin America Assembly Line Industry Revenue (billion), by End-user 2025 & 2033

- Figure 23: Latin America Assembly Line Industry Revenue Share (%), by End-user 2025 & 2033

- Figure 24: Latin America Assembly Line Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Latin America Assembly Line Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Rest of the World Assembly Line Industry Revenue (billion), by Type 2025 & 2033

- Figure 27: Rest of the World Assembly Line Industry Revenue Share (%), by Type 2025 & 2033

- Figure 28: Rest of the World Assembly Line Industry Revenue (billion), by End-user 2025 & 2033

- Figure 29: Rest of the World Assembly Line Industry Revenue Share (%), by End-user 2025 & 2033

- Figure 30: Rest of the World Assembly Line Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Rest of the World Assembly Line Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Assembly Line Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Global Assembly Line Industry Revenue billion Forecast, by End-user 2020 & 2033

- Table 3: Global Assembly Line Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Assembly Line Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 5: Global Assembly Line Industry Revenue billion Forecast, by End-user 2020 & 2033

- Table 6: Global Assembly Line Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Global Assembly Line Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 8: Global Assembly Line Industry Revenue billion Forecast, by End-user 2020 & 2033

- Table 9: Global Assembly Line Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Global Assembly Line Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 11: Global Assembly Line Industry Revenue billion Forecast, by End-user 2020 & 2033

- Table 12: Global Assembly Line Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Global Assembly Line Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 14: Global Assembly Line Industry Revenue billion Forecast, by End-user 2020 & 2033

- Table 15: Global Assembly Line Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Global Assembly Line Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 17: Global Assembly Line Industry Revenue billion Forecast, by End-user 2020 & 2033

- Table 18: Global Assembly Line Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Assembly Line Industry?

The projected CAGR is approximately 7.85%.

2. Which companies are prominent players in the Assembly Line Industry?

Key companies in the market include ACRO Automation Systems Inc, Hochrainer GmbH, JR Automation, Central Machines Inc, Totally Automated Systems, Fusion Systems Group, Adescor Inc, Gemtec GmbH, Markone Control Systems, Eriez Manufacturing Co, NEVMAT Australia PTY LTD, RNA Automation, UMD Automated Systems, Mondragon Assembly, Hitachi Power Solutions Co Ltd, MechTech Automation Group, RG-Luma Automation, BBS Automation, SITEC Industrietechnologie GmbH**List Not Exhaustive.

3. What are the main segments of the Assembly Line Industry?

The market segments include Type, End-user.

4. Can you provide details about the market size?

The market size is estimated to be USD 307.15 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Demand from Electric Vehicle Companies Driving the Market.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

May 2021: Mondragon Assembly is expanding into the USA market. The opening of a new subsidiary in Chicago will enable Mondragon Assembly to provide a closer and personalized service to the customers in the country.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Assembly Line Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Assembly Line Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Assembly Line Industry?

To stay informed about further developments, trends, and reports in the Assembly Line Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence