Key Insights

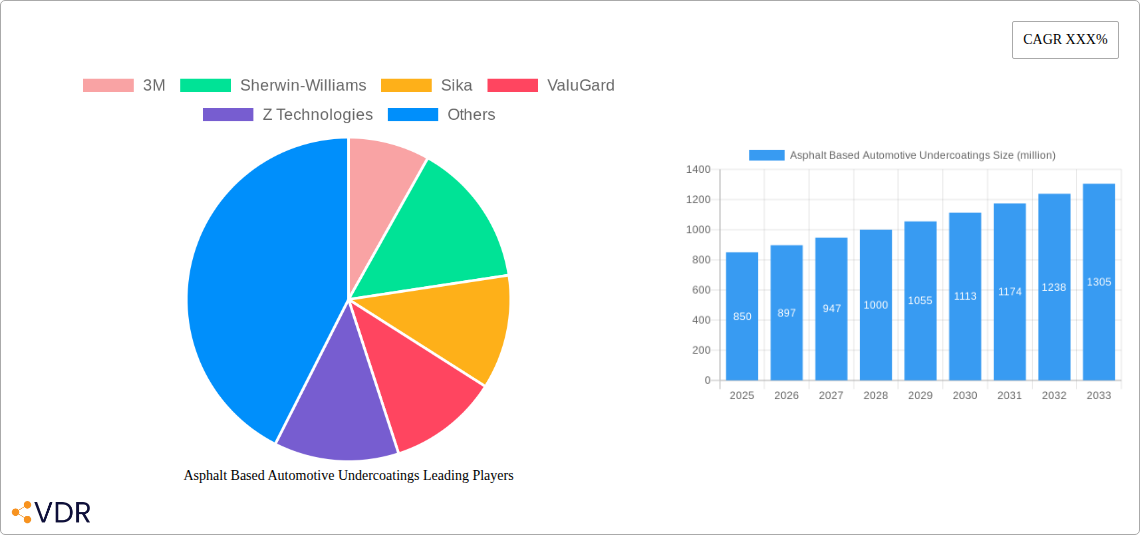

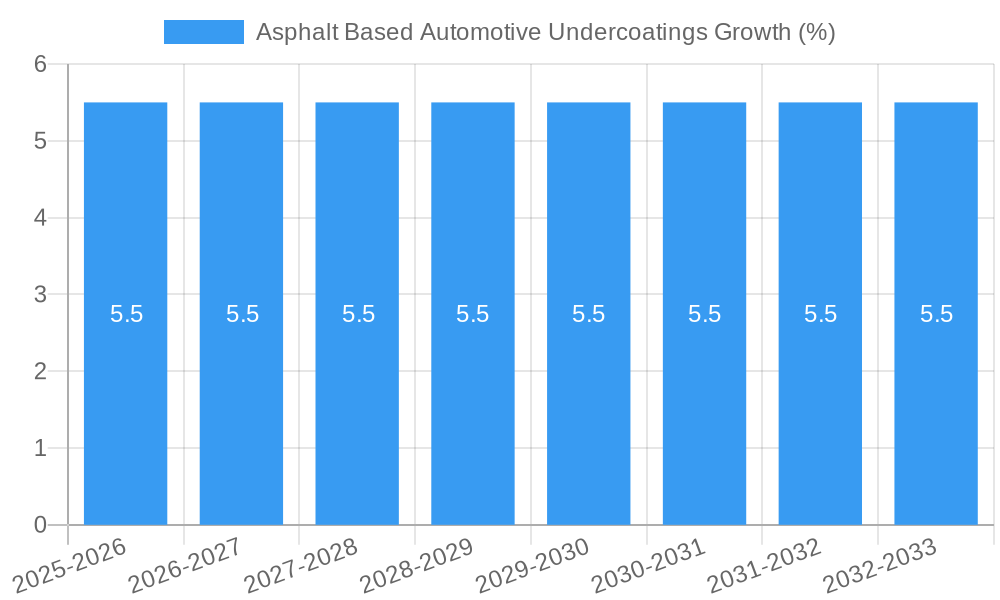

The global asphalt-based automotive undercoatings market is poised for robust expansion, projected to reach an estimated $850 million by 2025. This growth trajectory is underpinned by a Compound Annual Growth Rate (CAGR) of approximately 5.5% during the forecast period of 2025-2033. The increasing production of both passenger cars and commercial vehicles worldwide serves as a primary driver for this market. As manufacturers prioritize vehicle longevity, corrosion resistance, and noise reduction, the demand for effective undercoatings continues to surge. The inherent protective properties of asphalt-based formulations, offering excellent adhesion, durability, and resistance to abrasion and environmental factors, make them a preferred choice for automotive OEMs and the aftermarket. Furthermore, rising consumer awareness regarding vehicle maintenance and the desire to preserve resale value are contributing to the sustained demand for these protective coatings.

The market's expansion is further propelled by technological advancements in asphalt-based undercoating formulations, leading to improved application processes and enhanced performance characteristics. Innovations are focusing on developing eco-friendlier and low-VOC (Volatile Organic Compound) options to comply with increasingly stringent environmental regulations. While the market demonstrates strong growth, certain restraints, such as the emergence of alternative undercoating materials and the potential for raw material price volatility, warrant attention. However, the cost-effectiveness and proven efficacy of asphalt-based undercoatings are expected to maintain their competitive edge. The market segmentation highlights a significant share for applications in passenger cars, followed by commercial vehicles. Geographically, the Asia Pacific region, particularly China and India, is expected to witness the fastest growth due to its burgeoning automotive manufacturing sector and increasing disposable incomes.

Asphalt Based Automotive Undercoatings Market: Comprehensive Industry Analysis (2019-2033)

This in-depth report provides a definitive analysis of the global Asphalt Based Automotive Undercoatings Market, offering critical insights for stakeholders from 2019 to 2033. With a base year of 2025, this study delves into market dynamics, growth trends, regional dominance, product innovation, key drivers, barriers, opportunities, and the competitive landscape. Leveraging extensive primary and secondary research, this report equips you with actionable intelligence to navigate and capitalize on the evolving automotive undercoating sector.

Asphalt Based Automotive Undercoatings Market Dynamics & Structure

The global Asphalt Based Automotive Undercoatings Market exhibits a moderately consolidated structure, with leading players like 3M, Sherwin-Williams, and Sika holding significant market share. Technological innovation is primarily driven by the demand for enhanced durability, corrosion resistance, and sound dampening properties in automotive vehicles. Regulatory frameworks, particularly those concerning VOC emissions, are increasingly influencing product development towards water-based alternatives, although solvent-based formulations remain dominant due to performance characteristics. Competitive product substitutes, such as rubberized undercoatings and polymer-based coatings, present a consistent challenge, forcing manufacturers to innovate and optimize asphalt-based offerings. End-user demographics are shifting, with a growing demand for premium undercoatings in the passenger car segment, driven by increased vehicle personalization and a desire for extended vehicle lifespan. The commercial vehicle segment, on the other hand, emphasizes cost-effectiveness and robust protection against harsh environmental conditions. Merger and acquisition (M&A) trends are moderate, often focusing on expanding geographical reach or acquiring niche technological capabilities.

- Market Concentration: Moderate, with a few key global players and several regional manufacturers.

- Technological Innovation Drivers: Enhanced corrosion resistance, superior sound deadening, improved application efficiency, and stricter environmental compliance.

- Regulatory Frameworks: Focus on reducing volatile organic compound (VOC) emissions, driving innovation in low-VOC and water-based asphalt undercoatings.

- Competitive Product Substitutes: Rubberized undercoatings, polyurethane coatings, epoxy coatings, and advanced polymer-based solutions.

- End-User Demographics: Increasing demand for premium, high-performance undercoatings from passenger car owners and a focus on durability and cost-efficiency for commercial vehicle operators.

- M&A Trends: Strategic acquisitions for market penetration, technology integration, and portfolio expansion.

Asphalt Based Automotive Undercoatings Growth Trends & Insights

The Asphalt Based Automotive Undercoatings Market is poised for steady growth, projected to reach USD 3,500 million by 2033, expanding from an estimated USD 2,800 million in 2025. This growth trajectory is underpinned by a compound annual growth rate (CAGR) of approximately 3.5% during the forecast period of 2025–2033. Adoption rates of advanced asphalt undercoatings are steadily increasing as automotive manufacturers prioritize vehicle longevity and passenger comfort. Technological disruptions, such as the development of faster-curing formulations and enhanced adhesion properties, are further stimulating market penetration. Consumer behavior shifts are also playing a crucial role, with a heightened awareness of the importance of underbody protection against rust, corrosion, and road debris. This awareness, coupled with the growing demand for SUVs and off-road vehicles, which are more exposed to harsh conditions, is a significant market driver. The aftermarket segment continues to be a substantial contributor, as vehicle owners seek to maintain and protect their investments. The increasing complexity of vehicle underbodies and the need for specialized protection solutions are driving demand for high-performance asphalt undercoatings. Furthermore, the growing emphasis on noise, vibration, and harshness (NVH) reduction in vehicles is propelling the adoption of asphalt undercoatings for their acoustic insulation properties.

Dominant Regions, Countries, or Segments in Asphalt Based Automotive Undercoatings

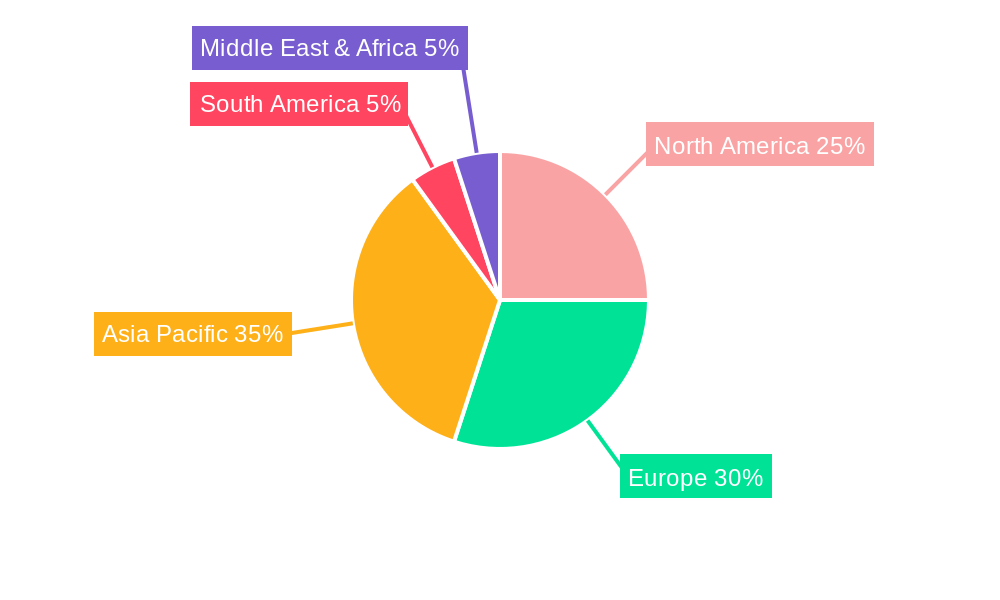

The Passenger Car segment is currently the dominant force in the Asphalt Based Automotive Undercoatings Market, driven by higher production volumes and a greater emphasis on aesthetics and long-term vehicle value. This segment is estimated to hold a 65% market share in 2025. North America and Europe are leading regions, primarily due to stringent automotive industry standards, high disposable incomes, and a strong aftermarket demand for vehicle protection. The Commercial Vehicle segment is also experiencing robust growth, driven by the increasing global trade and the need for durable undercoatings to withstand demanding operational conditions. Asia Pacific, particularly China and India, represents the fastest-growing regional market, fueled by the expansion of their automotive manufacturing bases and a rising middle class demanding more reliable vehicles.

- Dominant Application Segment: Passenger Car, accounting for an estimated USD 1,820 million in 2025.

- Key Drivers: High vehicle production volumes, increasing demand for premium features, and a focus on vehicle longevity and resale value.

- Growth Potential: Continues to be a primary market, with steady demand from both OEM and aftermarket sectors.

- Dominant Region: North America, with an estimated market size of USD 980 million in 2025.

- Key Drivers: Mature automotive market, stringent quality standards, strong OEM presence, and a significant aftermarket.

- Growth Potential: Stable growth, driven by fleet upgrades and aftermarket demand.

- Leading Country: United States, estimated at USD 700 million in 2025.

- Key Drivers: Robust automotive manufacturing, extensive vehicle parc, and high consumer spending on vehicle maintenance.

- Dominant Type: Solvent-Based undercoatings, projected to account for 70% of the market in 2025, valued at USD 1,960 million.

- Key Drivers: Superior adhesion, excellent durability, and proven performance in diverse environmental conditions.

- Growth Potential: While facing regulatory pressure, it remains the preferred choice for many demanding applications.

Asphalt Based Automotive Undercoatings Product Landscape

The Asphalt Based Automotive Undercoatings Market is characterized by continuous product innovation focused on enhancing performance and application efficiency. Manufacturers are actively developing formulations with improved UV resistance, superior adhesion to various substrates, and faster drying times. Advanced asphalt undercoatings now offer enhanced rust inhibition, robust sound dampening capabilities, and excellent resistance to impacts from stones and road debris. Unique selling propositions often revolve around eco-friendly formulations, such as low-VOC or water-based asphalt undercoatings, that meet evolving environmental regulations without compromising protective qualities. Technological advancements include the integration of advanced additives for enhanced durability and the development of specialized undercoatings for specific vehicle types and operational environments.

Key Drivers, Barriers & Challenges in Asphalt Based Automotive Undercoatings

Key Drivers:

- Increasing Demand for Vehicle Longevity: Growing consumer awareness and desire for extended vehicle lifespan are driving demand for protective undercoatings.

- Stringent Environmental Regulations: Evolving regulations on emissions are pushing innovation towards water-based and low-VOC asphalt undercoatings.

- Growth in Automotive Production: Expansion of the global automotive industry, particularly in emerging economies, directly translates to increased demand for undercoatings.

- Aftermarket Demand for Protection: Vehicle owners increasingly invest in aftermarket undercoatings to protect their vehicles from corrosion and damage.

- Demand for Noise Reduction: The focus on NVH improvement in vehicles boosts the appeal of asphalt undercoatings for their sound-dampening properties.

Barriers & Challenges:

- Availability and Price Volatility of Raw Materials: Fluctuations in asphalt and other key raw material prices can impact production costs and profitability.

- Competition from Substitute Products: Advancements in rubberized, polymer, and ceramic undercoatings offer alternatives that challenge asphalt-based solutions.

- Strict Environmental Regulations: While driving innovation, compliance with VOC emission standards can increase R&D costs and necessitate reformulation.

- Economic Downturns and Reduced Vehicle Sales: A slowdown in the automotive sector directly affects the demand for undercoatings.

- Complexity of Application Processes: Certain undercoatings may require specialized application equipment and skilled labor, potentially increasing overall costs.

Emerging Opportunities in Asphalt Based Automotive Undercoatings

Emerging opportunities in the Asphalt Based Automotive Undercoatings Market lie in the development of advanced, eco-friendly formulations that cater to the growing demand for sustainable automotive solutions. The electrification of vehicles presents a unique opportunity, as EV underbodies require specialized protection against battery pack heat and moisture ingress. Untapped markets in regions with rapidly expanding automotive industries, such as Southeast Asia and parts of Africa, offer significant growth potential. Furthermore, innovations in DIY-friendly asphalt undercoating products for the aftermarket segment can tap into a growing base of proactive vehicle owners seeking convenient protection solutions. The integration of smart functionalities, such as self-healing properties or integrated sensors for early corrosion detection, also represents a frontier for innovation.

Growth Accelerators in the Asphalt Based Automotive Undercoatings Industry

The Asphalt Based Automotive Undercoatings Industry is experiencing significant growth acceleration through several key catalysts. Technological breakthroughs in material science are leading to the development of undercoatings with superior performance characteristics, including enhanced corrosion resistance and improved sound dampening, meeting the evolving demands of vehicle manufacturers. Strategic partnerships between undercoating manufacturers and automotive OEMs are crucial for early integration of advanced solutions into vehicle designs and production lines. Market expansion strategies, particularly focusing on emerging economies with burgeoning automotive sectors, are opening up new avenues for growth. The increasing emphasis on electric vehicles (EVs) also acts as a significant accelerator, as these vehicles require specialized underbody protection for battery systems and thermal management, creating a new segment for asphalt undercoatings.

Key Players Shaping the Asphalt Based Automotive Undercoatings Market

- 3M

- Sherwin-Williams

- Sika

- ValuGard

- Z Technologies

- KBS Coatings

- Seymour Paint

- MOTIP

- Dominion Sure Seal

Notable Milestones in Asphalt Based Automotive Undercoatings Sector

- 2021: Introduction of advanced low-VOC solvent-based undercoatings by major players, aligning with stricter environmental regulations.

- 2022: Increased R&D focus on water-based asphalt undercoatings offering comparable performance to solvent-based alternatives.

- 2023: Development of specialized undercoatings for electric vehicle battery protection, addressing unique thermal and moisture management needs.

- 2024: Strategic acquisitions by larger chemical companies to enhance their portfolio in the automotive coatings sector, including undercoatings.

- 2025 (estimated): Launch of new formulations with enhanced self-healing properties for improved durability and extended lifespan.

In-Depth Asphalt Based Automotive Undercoatings Market Outlook

The future outlook for the Asphalt Based Automotive Undercoatings Market is strongly positive, driven by sustained demand for vehicle protection, longevity, and comfort. Growth accelerators, including technological advancements in eco-friendly formulations and specialized applications for electric vehicles, are poised to shape market expansion. Strategic collaborations and market penetration into emerging economies will further fuel this growth. The industry's ability to adapt to evolving regulatory landscapes and consumer preferences for sustainable and high-performance products will be critical in capitalizing on future market potential. The increasing focus on vehicle lifecycle management and preventative maintenance will continue to position asphalt undercoatings as essential components in automotive manufacturing and aftermarket services.

Asphalt Based Automotive Undercoatings Segmentation

-

1. Application

- 1.1. Passenger Car

- 1.2. Commercial Vehicle

-

2. Type

- 2.1. Water-Based

- 2.2. Solvent-Based

Asphalt Based Automotive Undercoatings Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Asphalt Based Automotive Undercoatings REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XXX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Asphalt Based Automotive Undercoatings Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Passenger Car

- 5.1.2. Commercial Vehicle

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Water-Based

- 5.2.2. Solvent-Based

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Asphalt Based Automotive Undercoatings Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Passenger Car

- 6.1.2. Commercial Vehicle

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Water-Based

- 6.2.2. Solvent-Based

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Asphalt Based Automotive Undercoatings Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Passenger Car

- 7.1.2. Commercial Vehicle

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Water-Based

- 7.2.2. Solvent-Based

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Asphalt Based Automotive Undercoatings Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Passenger Car

- 8.1.2. Commercial Vehicle

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Water-Based

- 8.2.2. Solvent-Based

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Asphalt Based Automotive Undercoatings Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Passenger Car

- 9.1.2. Commercial Vehicle

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Water-Based

- 9.2.2. Solvent-Based

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Asphalt Based Automotive Undercoatings Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Passenger Car

- 10.1.2. Commercial Vehicle

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Water-Based

- 10.2.2. Solvent-Based

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 3M

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Sherwin-Williams

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Sika

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 ValuGard

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Z Technologies

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 KBS Coatings

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Seymour Paint

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 MOTIP

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Dominion Sure Seal

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.1 3M

List of Figures

- Figure 1: Global Asphalt Based Automotive Undercoatings Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: Global Asphalt Based Automotive Undercoatings Volume Breakdown (K, %) by Region 2024 & 2032

- Figure 3: North America Asphalt Based Automotive Undercoatings Revenue (million), by Application 2024 & 2032

- Figure 4: North America Asphalt Based Automotive Undercoatings Volume (K), by Application 2024 & 2032

- Figure 5: North America Asphalt Based Automotive Undercoatings Revenue Share (%), by Application 2024 & 2032

- Figure 6: North America Asphalt Based Automotive Undercoatings Volume Share (%), by Application 2024 & 2032

- Figure 7: North America Asphalt Based Automotive Undercoatings Revenue (million), by Type 2024 & 2032

- Figure 8: North America Asphalt Based Automotive Undercoatings Volume (K), by Type 2024 & 2032

- Figure 9: North America Asphalt Based Automotive Undercoatings Revenue Share (%), by Type 2024 & 2032

- Figure 10: North America Asphalt Based Automotive Undercoatings Volume Share (%), by Type 2024 & 2032

- Figure 11: North America Asphalt Based Automotive Undercoatings Revenue (million), by Country 2024 & 2032

- Figure 12: North America Asphalt Based Automotive Undercoatings Volume (K), by Country 2024 & 2032

- Figure 13: North America Asphalt Based Automotive Undercoatings Revenue Share (%), by Country 2024 & 2032

- Figure 14: North America Asphalt Based Automotive Undercoatings Volume Share (%), by Country 2024 & 2032

- Figure 15: South America Asphalt Based Automotive Undercoatings Revenue (million), by Application 2024 & 2032

- Figure 16: South America Asphalt Based Automotive Undercoatings Volume (K), by Application 2024 & 2032

- Figure 17: South America Asphalt Based Automotive Undercoatings Revenue Share (%), by Application 2024 & 2032

- Figure 18: South America Asphalt Based Automotive Undercoatings Volume Share (%), by Application 2024 & 2032

- Figure 19: South America Asphalt Based Automotive Undercoatings Revenue (million), by Type 2024 & 2032

- Figure 20: South America Asphalt Based Automotive Undercoatings Volume (K), by Type 2024 & 2032

- Figure 21: South America Asphalt Based Automotive Undercoatings Revenue Share (%), by Type 2024 & 2032

- Figure 22: South America Asphalt Based Automotive Undercoatings Volume Share (%), by Type 2024 & 2032

- Figure 23: South America Asphalt Based Automotive Undercoatings Revenue (million), by Country 2024 & 2032

- Figure 24: South America Asphalt Based Automotive Undercoatings Volume (K), by Country 2024 & 2032

- Figure 25: South America Asphalt Based Automotive Undercoatings Revenue Share (%), by Country 2024 & 2032

- Figure 26: South America Asphalt Based Automotive Undercoatings Volume Share (%), by Country 2024 & 2032

- Figure 27: Europe Asphalt Based Automotive Undercoatings Revenue (million), by Application 2024 & 2032

- Figure 28: Europe Asphalt Based Automotive Undercoatings Volume (K), by Application 2024 & 2032

- Figure 29: Europe Asphalt Based Automotive Undercoatings Revenue Share (%), by Application 2024 & 2032

- Figure 30: Europe Asphalt Based Automotive Undercoatings Volume Share (%), by Application 2024 & 2032

- Figure 31: Europe Asphalt Based Automotive Undercoatings Revenue (million), by Type 2024 & 2032

- Figure 32: Europe Asphalt Based Automotive Undercoatings Volume (K), by Type 2024 & 2032

- Figure 33: Europe Asphalt Based Automotive Undercoatings Revenue Share (%), by Type 2024 & 2032

- Figure 34: Europe Asphalt Based Automotive Undercoatings Volume Share (%), by Type 2024 & 2032

- Figure 35: Europe Asphalt Based Automotive Undercoatings Revenue (million), by Country 2024 & 2032

- Figure 36: Europe Asphalt Based Automotive Undercoatings Volume (K), by Country 2024 & 2032

- Figure 37: Europe Asphalt Based Automotive Undercoatings Revenue Share (%), by Country 2024 & 2032

- Figure 38: Europe Asphalt Based Automotive Undercoatings Volume Share (%), by Country 2024 & 2032

- Figure 39: Middle East & Africa Asphalt Based Automotive Undercoatings Revenue (million), by Application 2024 & 2032

- Figure 40: Middle East & Africa Asphalt Based Automotive Undercoatings Volume (K), by Application 2024 & 2032

- Figure 41: Middle East & Africa Asphalt Based Automotive Undercoatings Revenue Share (%), by Application 2024 & 2032

- Figure 42: Middle East & Africa Asphalt Based Automotive Undercoatings Volume Share (%), by Application 2024 & 2032

- Figure 43: Middle East & Africa Asphalt Based Automotive Undercoatings Revenue (million), by Type 2024 & 2032

- Figure 44: Middle East & Africa Asphalt Based Automotive Undercoatings Volume (K), by Type 2024 & 2032

- Figure 45: Middle East & Africa Asphalt Based Automotive Undercoatings Revenue Share (%), by Type 2024 & 2032

- Figure 46: Middle East & Africa Asphalt Based Automotive Undercoatings Volume Share (%), by Type 2024 & 2032

- Figure 47: Middle East & Africa Asphalt Based Automotive Undercoatings Revenue (million), by Country 2024 & 2032

- Figure 48: Middle East & Africa Asphalt Based Automotive Undercoatings Volume (K), by Country 2024 & 2032

- Figure 49: Middle East & Africa Asphalt Based Automotive Undercoatings Revenue Share (%), by Country 2024 & 2032

- Figure 50: Middle East & Africa Asphalt Based Automotive Undercoatings Volume Share (%), by Country 2024 & 2032

- Figure 51: Asia Pacific Asphalt Based Automotive Undercoatings Revenue (million), by Application 2024 & 2032

- Figure 52: Asia Pacific Asphalt Based Automotive Undercoatings Volume (K), by Application 2024 & 2032

- Figure 53: Asia Pacific Asphalt Based Automotive Undercoatings Revenue Share (%), by Application 2024 & 2032

- Figure 54: Asia Pacific Asphalt Based Automotive Undercoatings Volume Share (%), by Application 2024 & 2032

- Figure 55: Asia Pacific Asphalt Based Automotive Undercoatings Revenue (million), by Type 2024 & 2032

- Figure 56: Asia Pacific Asphalt Based Automotive Undercoatings Volume (K), by Type 2024 & 2032

- Figure 57: Asia Pacific Asphalt Based Automotive Undercoatings Revenue Share (%), by Type 2024 & 2032

- Figure 58: Asia Pacific Asphalt Based Automotive Undercoatings Volume Share (%), by Type 2024 & 2032

- Figure 59: Asia Pacific Asphalt Based Automotive Undercoatings Revenue (million), by Country 2024 & 2032

- Figure 60: Asia Pacific Asphalt Based Automotive Undercoatings Volume (K), by Country 2024 & 2032

- Figure 61: Asia Pacific Asphalt Based Automotive Undercoatings Revenue Share (%), by Country 2024 & 2032

- Figure 62: Asia Pacific Asphalt Based Automotive Undercoatings Volume Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Asphalt Based Automotive Undercoatings Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Asphalt Based Automotive Undercoatings Volume K Forecast, by Region 2019 & 2032

- Table 3: Global Asphalt Based Automotive Undercoatings Revenue million Forecast, by Application 2019 & 2032

- Table 4: Global Asphalt Based Automotive Undercoatings Volume K Forecast, by Application 2019 & 2032

- Table 5: Global Asphalt Based Automotive Undercoatings Revenue million Forecast, by Type 2019 & 2032

- Table 6: Global Asphalt Based Automotive Undercoatings Volume K Forecast, by Type 2019 & 2032

- Table 7: Global Asphalt Based Automotive Undercoatings Revenue million Forecast, by Region 2019 & 2032

- Table 8: Global Asphalt Based Automotive Undercoatings Volume K Forecast, by Region 2019 & 2032

- Table 9: Global Asphalt Based Automotive Undercoatings Revenue million Forecast, by Application 2019 & 2032

- Table 10: Global Asphalt Based Automotive Undercoatings Volume K Forecast, by Application 2019 & 2032

- Table 11: Global Asphalt Based Automotive Undercoatings Revenue million Forecast, by Type 2019 & 2032

- Table 12: Global Asphalt Based Automotive Undercoatings Volume K Forecast, by Type 2019 & 2032

- Table 13: Global Asphalt Based Automotive Undercoatings Revenue million Forecast, by Country 2019 & 2032

- Table 14: Global Asphalt Based Automotive Undercoatings Volume K Forecast, by Country 2019 & 2032

- Table 15: United States Asphalt Based Automotive Undercoatings Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: United States Asphalt Based Automotive Undercoatings Volume (K) Forecast, by Application 2019 & 2032

- Table 17: Canada Asphalt Based Automotive Undercoatings Revenue (million) Forecast, by Application 2019 & 2032

- Table 18: Canada Asphalt Based Automotive Undercoatings Volume (K) Forecast, by Application 2019 & 2032

- Table 19: Mexico Asphalt Based Automotive Undercoatings Revenue (million) Forecast, by Application 2019 & 2032

- Table 20: Mexico Asphalt Based Automotive Undercoatings Volume (K) Forecast, by Application 2019 & 2032

- Table 21: Global Asphalt Based Automotive Undercoatings Revenue million Forecast, by Application 2019 & 2032

- Table 22: Global Asphalt Based Automotive Undercoatings Volume K Forecast, by Application 2019 & 2032

- Table 23: Global Asphalt Based Automotive Undercoatings Revenue million Forecast, by Type 2019 & 2032

- Table 24: Global Asphalt Based Automotive Undercoatings Volume K Forecast, by Type 2019 & 2032

- Table 25: Global Asphalt Based Automotive Undercoatings Revenue million Forecast, by Country 2019 & 2032

- Table 26: Global Asphalt Based Automotive Undercoatings Volume K Forecast, by Country 2019 & 2032

- Table 27: Brazil Asphalt Based Automotive Undercoatings Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Brazil Asphalt Based Automotive Undercoatings Volume (K) Forecast, by Application 2019 & 2032

- Table 29: Argentina Asphalt Based Automotive Undercoatings Revenue (million) Forecast, by Application 2019 & 2032

- Table 30: Argentina Asphalt Based Automotive Undercoatings Volume (K) Forecast, by Application 2019 & 2032

- Table 31: Rest of South America Asphalt Based Automotive Undercoatings Revenue (million) Forecast, by Application 2019 & 2032

- Table 32: Rest of South America Asphalt Based Automotive Undercoatings Volume (K) Forecast, by Application 2019 & 2032

- Table 33: Global Asphalt Based Automotive Undercoatings Revenue million Forecast, by Application 2019 & 2032

- Table 34: Global Asphalt Based Automotive Undercoatings Volume K Forecast, by Application 2019 & 2032

- Table 35: Global Asphalt Based Automotive Undercoatings Revenue million Forecast, by Type 2019 & 2032

- Table 36: Global Asphalt Based Automotive Undercoatings Volume K Forecast, by Type 2019 & 2032

- Table 37: Global Asphalt Based Automotive Undercoatings Revenue million Forecast, by Country 2019 & 2032

- Table 38: Global Asphalt Based Automotive Undercoatings Volume K Forecast, by Country 2019 & 2032

- Table 39: United Kingdom Asphalt Based Automotive Undercoatings Revenue (million) Forecast, by Application 2019 & 2032

- Table 40: United Kingdom Asphalt Based Automotive Undercoatings Volume (K) Forecast, by Application 2019 & 2032

- Table 41: Germany Asphalt Based Automotive Undercoatings Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: Germany Asphalt Based Automotive Undercoatings Volume (K) Forecast, by Application 2019 & 2032

- Table 43: France Asphalt Based Automotive Undercoatings Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: France Asphalt Based Automotive Undercoatings Volume (K) Forecast, by Application 2019 & 2032

- Table 45: Italy Asphalt Based Automotive Undercoatings Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Italy Asphalt Based Automotive Undercoatings Volume (K) Forecast, by Application 2019 & 2032

- Table 47: Spain Asphalt Based Automotive Undercoatings Revenue (million) Forecast, by Application 2019 & 2032

- Table 48: Spain Asphalt Based Automotive Undercoatings Volume (K) Forecast, by Application 2019 & 2032

- Table 49: Russia Asphalt Based Automotive Undercoatings Revenue (million) Forecast, by Application 2019 & 2032

- Table 50: Russia Asphalt Based Automotive Undercoatings Volume (K) Forecast, by Application 2019 & 2032

- Table 51: Benelux Asphalt Based Automotive Undercoatings Revenue (million) Forecast, by Application 2019 & 2032

- Table 52: Benelux Asphalt Based Automotive Undercoatings Volume (K) Forecast, by Application 2019 & 2032

- Table 53: Nordics Asphalt Based Automotive Undercoatings Revenue (million) Forecast, by Application 2019 & 2032

- Table 54: Nordics Asphalt Based Automotive Undercoatings Volume (K) Forecast, by Application 2019 & 2032

- Table 55: Rest of Europe Asphalt Based Automotive Undercoatings Revenue (million) Forecast, by Application 2019 & 2032

- Table 56: Rest of Europe Asphalt Based Automotive Undercoatings Volume (K) Forecast, by Application 2019 & 2032

- Table 57: Global Asphalt Based Automotive Undercoatings Revenue million Forecast, by Application 2019 & 2032

- Table 58: Global Asphalt Based Automotive Undercoatings Volume K Forecast, by Application 2019 & 2032

- Table 59: Global Asphalt Based Automotive Undercoatings Revenue million Forecast, by Type 2019 & 2032

- Table 60: Global Asphalt Based Automotive Undercoatings Volume K Forecast, by Type 2019 & 2032

- Table 61: Global Asphalt Based Automotive Undercoatings Revenue million Forecast, by Country 2019 & 2032

- Table 62: Global Asphalt Based Automotive Undercoatings Volume K Forecast, by Country 2019 & 2032

- Table 63: Turkey Asphalt Based Automotive Undercoatings Revenue (million) Forecast, by Application 2019 & 2032

- Table 64: Turkey Asphalt Based Automotive Undercoatings Volume (K) Forecast, by Application 2019 & 2032

- Table 65: Israel Asphalt Based Automotive Undercoatings Revenue (million) Forecast, by Application 2019 & 2032

- Table 66: Israel Asphalt Based Automotive Undercoatings Volume (K) Forecast, by Application 2019 & 2032

- Table 67: GCC Asphalt Based Automotive Undercoatings Revenue (million) Forecast, by Application 2019 & 2032

- Table 68: GCC Asphalt Based Automotive Undercoatings Volume (K) Forecast, by Application 2019 & 2032

- Table 69: North Africa Asphalt Based Automotive Undercoatings Revenue (million) Forecast, by Application 2019 & 2032

- Table 70: North Africa Asphalt Based Automotive Undercoatings Volume (K) Forecast, by Application 2019 & 2032

- Table 71: South Africa Asphalt Based Automotive Undercoatings Revenue (million) Forecast, by Application 2019 & 2032

- Table 72: South Africa Asphalt Based Automotive Undercoatings Volume (K) Forecast, by Application 2019 & 2032

- Table 73: Rest of Middle East & Africa Asphalt Based Automotive Undercoatings Revenue (million) Forecast, by Application 2019 & 2032

- Table 74: Rest of Middle East & Africa Asphalt Based Automotive Undercoatings Volume (K) Forecast, by Application 2019 & 2032

- Table 75: Global Asphalt Based Automotive Undercoatings Revenue million Forecast, by Application 2019 & 2032

- Table 76: Global Asphalt Based Automotive Undercoatings Volume K Forecast, by Application 2019 & 2032

- Table 77: Global Asphalt Based Automotive Undercoatings Revenue million Forecast, by Type 2019 & 2032

- Table 78: Global Asphalt Based Automotive Undercoatings Volume K Forecast, by Type 2019 & 2032

- Table 79: Global Asphalt Based Automotive Undercoatings Revenue million Forecast, by Country 2019 & 2032

- Table 80: Global Asphalt Based Automotive Undercoatings Volume K Forecast, by Country 2019 & 2032

- Table 81: China Asphalt Based Automotive Undercoatings Revenue (million) Forecast, by Application 2019 & 2032

- Table 82: China Asphalt Based Automotive Undercoatings Volume (K) Forecast, by Application 2019 & 2032

- Table 83: India Asphalt Based Automotive Undercoatings Revenue (million) Forecast, by Application 2019 & 2032

- Table 84: India Asphalt Based Automotive Undercoatings Volume (K) Forecast, by Application 2019 & 2032

- Table 85: Japan Asphalt Based Automotive Undercoatings Revenue (million) Forecast, by Application 2019 & 2032

- Table 86: Japan Asphalt Based Automotive Undercoatings Volume (K) Forecast, by Application 2019 & 2032

- Table 87: South Korea Asphalt Based Automotive Undercoatings Revenue (million) Forecast, by Application 2019 & 2032

- Table 88: South Korea Asphalt Based Automotive Undercoatings Volume (K) Forecast, by Application 2019 & 2032

- Table 89: ASEAN Asphalt Based Automotive Undercoatings Revenue (million) Forecast, by Application 2019 & 2032

- Table 90: ASEAN Asphalt Based Automotive Undercoatings Volume (K) Forecast, by Application 2019 & 2032

- Table 91: Oceania Asphalt Based Automotive Undercoatings Revenue (million) Forecast, by Application 2019 & 2032

- Table 92: Oceania Asphalt Based Automotive Undercoatings Volume (K) Forecast, by Application 2019 & 2032

- Table 93: Rest of Asia Pacific Asphalt Based Automotive Undercoatings Revenue (million) Forecast, by Application 2019 & 2032

- Table 94: Rest of Asia Pacific Asphalt Based Automotive Undercoatings Volume (K) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Asphalt Based Automotive Undercoatings?

The projected CAGR is approximately XXX%.

2. Which companies are prominent players in the Asphalt Based Automotive Undercoatings?

Key companies in the market include 3M, Sherwin-Williams, Sika, ValuGard, Z Technologies, KBS Coatings, Seymour Paint, MOTIP, Dominion Sure Seal.

3. What are the main segments of the Asphalt Based Automotive Undercoatings?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Asphalt Based Automotive Undercoatings," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Asphalt Based Automotive Undercoatings report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Asphalt Based Automotive Undercoatings?

To stay informed about further developments, trends, and reports in the Asphalt Based Automotive Undercoatings, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence