Key Insights

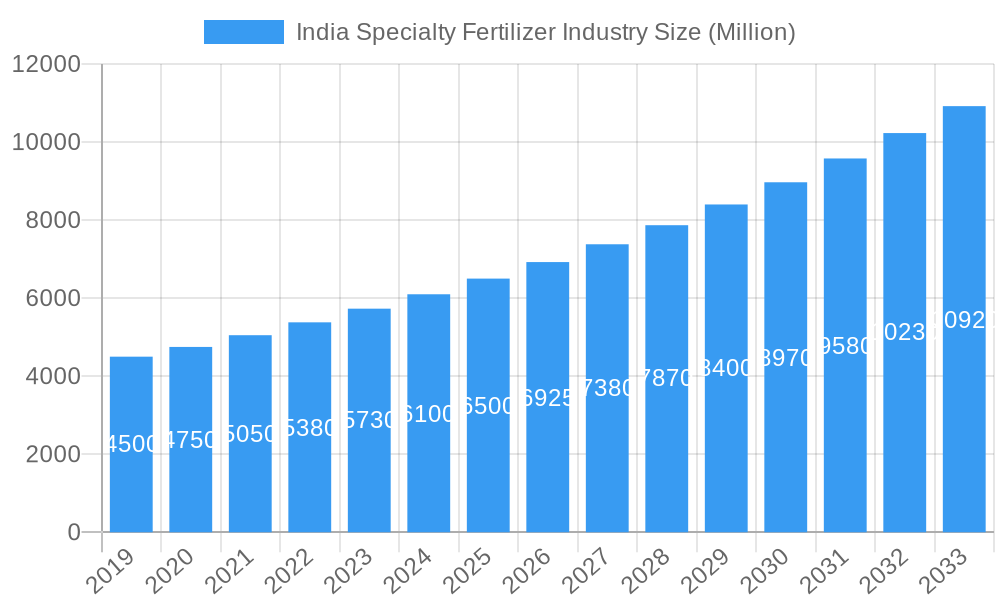

India's specialty fertilizer market is projected for significant growth, with an estimated market size of 39.9 billion by 2025, expanding at a Compound Annual Growth Rate (CAGR) of 6.3%. This expansion is driven by the increasing adoption of advanced agricultural practices focused on enhancing crop yield and quality, alongside growing farmer awareness of tailored nutrient solutions. Government initiatives promoting agricultural productivity and sustainability, coupled with favorable policies, further support this growth. Key drivers include the demand for high-efficiency fertilizers that minimize nutrient loss and environmental impact, the cultivation of high-value crops requiring specific nutrient profiles, and the adoption of precision agriculture. Emerging trends like water-soluble fertilizers, controlled-release fertilizers, and biostimulants are fostering more sustainable and effective soil and plant nutrition management.

India Specialty Fertilizer Industry Market Size (In Billion)

Potential restraints to market expansion include the higher cost of specialty fertilizers compared to conventional options, which can be a barrier for small farmers, and limited awareness of application techniques within a segment of the farming community. However, continuous efforts by market players to educate farmers, introduce cost-effective solutions, and expand distribution networks are expected to mitigate these challenges. The market is characterized by intense competition, with global and domestic players vying for market share. Strategic collaborations, mergers, and acquisitions are anticipated as companies seek to broaden product portfolios and geographical reach. India's dynamic agricultural needs and technological advancements present a fertile ground for innovation and sustained growth in the specialty fertilizer sector.

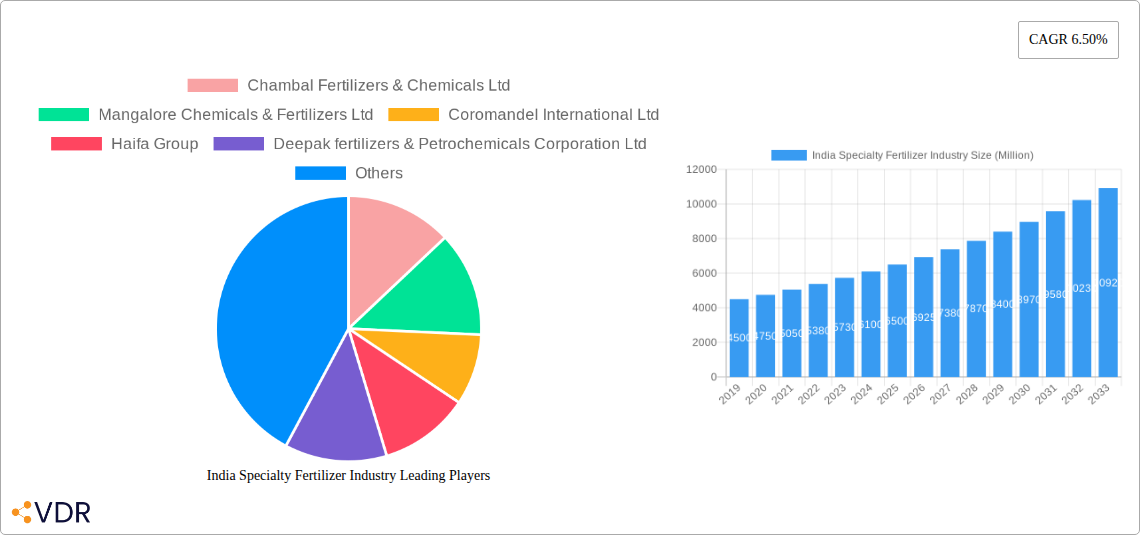

India Specialty Fertilizer Industry Company Market Share

This report provides a detailed analysis of the India Specialty Fertilizer Industry, covering market dynamics, growth trends, regional dominance, product landscape, key drivers, challenges, and future opportunities. Research for the period 2019-2033, with a base year of 2025, offers critical insights for stakeholders. The analysis includes production, consumption, import/export markets, and price trends, with values presented in billion units. We meticulously examine parent and child market segments for a holistic understanding of India's specialty fertilizer ecosystem.

India Specialty Fertilizer Industry Market Dynamics & Structure

The India Specialty Fertilizer Industry is characterized by a moderate level of market concentration, with a few key players holding significant market share, while a growing number of smaller entities contribute to a dynamic competitive landscape. Technological innovation is a primary driver, fueled by the increasing adoption of precision agriculture, enhanced nutrient use efficiency, and the demand for sustainable farming practices. Regulatory frameworks, while evolving to support agricultural advancement, also influence market entry and product development. Competitive product substitutes include conventional fertilizers and organic alternatives, necessitating continuous innovation in specialty fertilizer formulations. End-user demographics are diverse, ranging from large-scale commercial farms to smallholder farmers, each with distinct needs and purchasing behaviors. Mergers and acquisitions (M&A) trends are observed as companies seek to expand their product portfolios, market reach, and technological capabilities. For instance, strategic partnerships, like Coromandel International's collaboration with Agrinos, highlight this trend, aiming to broaden offerings in plant nutrition. The industry faces innovation barriers related to the cost of R&D, farmer education on advanced nutrient management, and the long gestation periods for product development and market acceptance.

- Market Concentration: Moderately concentrated, with increasing fragmentation due to new entrants.

- Technological Innovation Drivers: Precision farming, enhanced nutrient use efficiency, climate-resilient agriculture.

- Regulatory Frameworks: Government policies promoting sustainable agriculture, subsidies for innovative inputs.

- Competitive Product Substitutes: Conventional NPK fertilizers, organic manures, biostimulants.

- End-User Demographics: Commercial agribusiness, progressive farmers, smallholder farmers adopting new technologies.

- M&A Trends: Strategic alliances and acquisitions to enhance product breadth and market access.

India Specialty Fertilizer Industry Growth Trends & Insights

The India Specialty Fertilizer Industry is poised for substantial growth, driven by a confluence of factors including an escalating demand for enhanced crop yields, improved soil health, and sustainable agricultural practices. Market size evolution is projected to be robust, with a significant compound annual growth rate (CAGR) anticipated over the forecast period. Adoption rates for specialty fertilizers are on a steady rise, as Indian farmers increasingly recognize their benefits in optimizing nutrient delivery and minimizing environmental impact. Technological disruptions, such as the development and application of nanotechnology-based fertilizers by entities like IFFCO, are revolutionizing nutrient management, promising higher efficiency and reduced application rates. These innovations are pivotal in addressing the challenges of low nutrient use efficiency and soil degradation prevalent in Indian agriculture. Consumer behavior shifts are also playing a crucial role, with a growing awareness among farmers about the long-term economic and environmental benefits of using tailored nutrient solutions over generic fertilizers. This shift is influenced by educational initiatives, government support for precision farming, and the increasing profitability demonstrated by farmers who adopt these advanced inputs. Market penetration of specialty fertilizers, though still nascent in some segments, is accelerating, particularly in regions with intensive agriculture and higher farmer incomes. The increasing focus on horticultural crops and high-value agricultural produce further fuels the demand for specialized nutrient formulations that cater to specific crop requirements and growth stages. The overall market is transitioning from a volume-driven approach to a value-driven one, emphasizing the superior performance and environmental sustainability of specialty fertilizers.

Dominant Regions, Countries, or Segments in India Specialty Fertilizer Industry

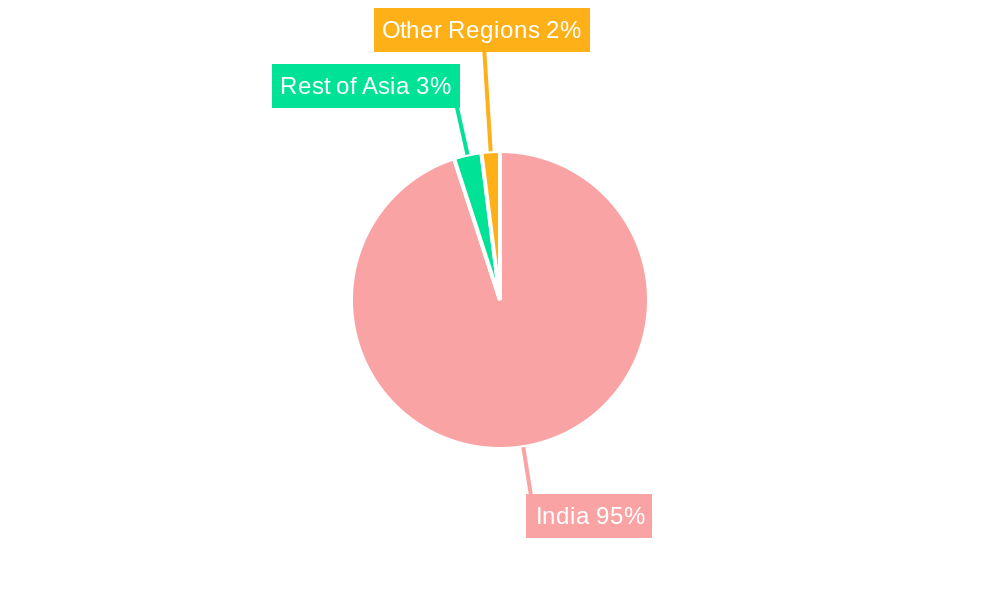

The Consumption Analysis segment is currently the dominant force driving growth within the India Specialty Fertilizer Industry, reflecting the direct demand from the agricultural sector. Major agricultural states in India, such as Punjab, Haryana, Uttar Pradesh, Maharashtra, and Gujarat, emerge as key consumption hubs. These regions are characterized by intensive farming practices, a higher proportion of high-value crops, and greater farmer awareness and adoption of advanced agricultural technologies. The economic policies in these states, often focused on agricultural modernization and farmer welfare, further stimulate the demand for specialty fertilizers. Infrastructure development, including improved irrigation facilities and better access to agricultural extension services, also plays a crucial role in facilitating the adoption of these inputs.

- Key Drivers in Dominant Consumption Regions:

- Intensive Agriculture & High-Value Crops: Leading to greater demand for tailored nutrient solutions.

- Farmer Awareness & Adoption: Increased understanding of the benefits of specialty fertilizers.

- Government Initiatives: Subsidies and support for modern farming practices and inputs.

- Infrastructure Development: Improved irrigation and logistics networks.

- Growing Agri-Business Sector: Commercial farms adopting advanced nutrient management.

The Production Analysis segment is also crucial, with significant manufacturing capacities concentrated in states with good access to raw materials, established chemical industries, and proximity to major agricultural markets. Companies like Chambal Fertilizers & Chemicals Ltd and Coromandel International Ltd have substantial production facilities that cater to both domestic and, to some extent, export markets. The growth potential in this segment is linked to the increasing domestic demand and the government's 'Make in India' initiative, encouraging local manufacturing of agricultural inputs.

- Key Drivers in Dominant Production Regions:

- Raw Material Availability: Proximity to sources of key fertilizer ingredients.

- Industrial Infrastructure: Well-developed chemical and industrial zones.

- Skilled Labor Force: Availability of technical expertise.

- Logistics and Connectivity: Efficient transportation networks for raw materials and finished goods.

The Import Market Analysis is significant for specialized products and raw materials not readily available domestically, with Gujarat, Maharashtra, and Tamil Nadu being major entry points due to their port infrastructure. Conversely, the Export Market Analysis, while currently smaller, shows potential for growth, particularly for niche specialty fertilizers where Indian manufacturers develop a competitive edge. Price Trend Analysis is influenced by global commodity prices, domestic demand-supply dynamics, and government policies, with specialty fertilizers generally commanding premium pricing due to their enhanced efficacy and formulation.

India Specialty Fertilizer Industry Product Landscape

The product landscape of the India Specialty Fertilizer Industry is characterized by a rapid evolution driven by innovation and the need for precise crop nutrition. Key product categories include water-soluble fertilizers, controlled-release fertilizers, micronutrient fertilizers, liquid fertilizers, and biostimulants. These products offer enhanced nutrient use efficiency, reduced environmental impact, and tailored solutions for specific crops and soil conditions. Unique selling propositions lie in their advanced formulations, such as nano-fertilizers, which ensure better nutrient absorption and reduced wastage, and slow-release fertilizers that provide sustained nutrition over the crop cycle. Technological advancements like the development of products from polyhalite, as pioneered by ICL Fertilizers, exemplify the industry's commitment to balanced and targeted crop feeding. The application of these specialty fertilizers spans across a wide range of crops, from staple grains to fruits, vegetables, and plantation crops, contributing to improved yield quality and quantity.

Key Drivers, Barriers & Challenges in India Specialty Fertilizer Industry

Key Drivers: The India Specialty Fertilizer Industry is propelled by several potent drivers. A primary catalyst is the escalating demand for increased agricultural productivity to meet the food security needs of a growing population. The imperative for sustainable agriculture and environmental protection also fuels the adoption of specialty fertilizers, which minimize nutrient runoff and greenhouse gas emissions. Government initiatives promoting precision farming and subsidies for advanced agricultural inputs further accelerate market growth. Technological innovations, particularly in areas like nanotechnology and controlled-release formulations, offer superior efficacy and efficiency, making them attractive to farmers. Furthermore, the rising disposable incomes of farmers and their increasing awareness of the economic benefits of improved crop yields and quality are significant drivers.

Barriers & Challenges: Despite the strong growth trajectory, the industry faces considerable barriers and challenges. The high cost of specialty fertilizers compared to conventional alternatives remains a significant restraint for many smallholder farmers. Inadequate farmer education and awareness about the proper application and benefits of these advanced products hinder widespread adoption. The complex regulatory landscape and lengthy approval processes for new formulations can also pose challenges. Supply chain inefficiencies, particularly in reaching remote agricultural regions, can impact product availability and cost. Intense competition from established players and the threat of counterfeit products further complicate the market.

Emerging Opportunities in India Specialty Fertilizer Industry

Emerging opportunities in the India Specialty Fertilizer Industry are multifaceted, driven by evolving agricultural practices and consumer preferences. The burgeoning demand for organic and bio-fertilizers presents a significant avenue for growth, aligning with global trends towards sustainable agriculture. The expansion of protected cultivation and precision agriculture techniques in horticulture, floriculture, and high-value crop segments offers substantial potential for customized specialty fertilizer solutions. Furthermore, the increasing adoption of fertigation and foliar application methods by farmers creates a strong market for water-soluble and liquid specialty fertilizers. The development of customized nutrient blends tailored to specific regional soil types and crop needs also represents an untapped market segment.

Growth Accelerators in the India Specialty Fertilizer Industry Industry

Several key accelerators are poised to propel the long-term growth of the India Specialty Fertilizer Industry. Technological breakthroughs in nutrient delivery systems, including advanced controlled-release mechanisms and enhanced nano-fertilizer formulations, will be crucial. Strategic partnerships between domestic and international players, facilitating technology transfer and expanding market reach, will act as significant catalysts. The government's continued focus on agricultural modernization, coupled with favorable policy support and increased R&D investments, will further stimulate innovation and adoption. Market expansion strategies, focusing on underserved regions and the development of affordable specialty fertilizer solutions for smallholder farmers, will be vital for sustained growth.

Key Players Shaping the India Specialty Fertilizer Industry Market

- Chambal Fertilizers & Chemicals Ltd

- Mangalore Chemicals & Fertilizers Ltd

- Coromandel International Ltd

- Haifa Group

- Deepak fertilizers & Petrochemicals Corporation Ltd

- Indian Farmers Fertiliser Cooperative Limited

- Grupa Azoty S A (Compo Expert)

- Yara International AS

- ICL Group Ltd

- Sociedad Quimica y Minera de Chile SA

Notable Milestones in India Specialty Fertilizer Industry Sector

- November 2019: IFFCO Launches its Nano Technology based Products nano nitrogen, nano zinc and nano copper for on-field trials as part of its efforts to cut fertilizer usage and boost farmers' income.

- February 2019: Coromandel International announced a strategic partnership with Agrinos. The partnership allows Coromandel to widen its product offerings of complete plant nutrition solutions, organic fertilizers, and specialty nutrients. Coromandel, in partnership with Agrinos, will offer growers high-technology inputs under the brand name ARITHRI.

- November 2018: ICL Fertilizers developed a new line of premium fertilizers that help farmers feed their crops precisely. Polysulphate, ICLPotashpluS, and ICLPKpluS are manufactured from polyhalite, a mineral extracted at the ICL mine in Boulby, United Kingdom, to meet the agricultural need for balanced, targeted nutrition.

In-Depth India Specialty Fertilizer Industry Market Outlook

The India Specialty Fertilizer Industry is set to witness a period of robust expansion, driven by an unwavering focus on enhancing agricultural productivity and sustainability. Future market potential lies in the widespread adoption of precision agriculture technologies and the development of climate-resilient nutrient solutions. Strategic opportunities include the expansion of product portfolios to include more bio-based and organic inputs, catering to the growing demand for eco-friendly farming. Furthermore, leveraging advancements in digital agriculture and data analytics will enable the creation of highly customized fertilizer recommendations, optimizing crop health and farmer profitability. The industry's outlook is strongly positive, with continued innovation and supportive policies expected to accelerate its growth trajectory.

India Specialty Fertilizer Industry Segmentation

- 1. Production Analysis

- 2. Consumption Analysis

- 3. Import Market Analysis (Value & Volume)

- 4. Export Market Analysis (Value & Volume)

- 5. Price Trend Analysis

India Specialty Fertilizer Industry Segmentation By Geography

- 1. India

India Specialty Fertilizer Industry Regional Market Share

Geographic Coverage of India Specialty Fertilizer Industry

India Specialty Fertilizer Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Production Analysis

- 5.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 5.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 5.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 5.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. India

- 6. India Specialty Fertilizer Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Production Analysis

- 6.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 6.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 6.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 6.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Chambal Fertilizers & Chemicals Ltd

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Mangalore Chemicals & Fertilizers Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Coromandel International Ltd

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Haifa Group

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Deepak fertilizers & Petrochemicals Corporation Ltd

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Indian Farmers Fertiliser Cooperative Limited

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Grupa Azoty S A (Compo Expert)

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Yara International AS

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 ICL Group Ltd

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Sociedad Quimica y Minera de Chile SA

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Chambal Fertilizers & Chemicals Ltd

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: India Specialty Fertilizer Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: India Specialty Fertilizer Industry Share (%) by Company 2025

List of Tables

- Table 1: India Specialty Fertilizer Industry Revenue billion Forecast, by Production Analysis 2020 & 2033

- Table 2: India Specialty Fertilizer Industry Revenue billion Forecast, by Consumption Analysis 2020 & 2033

- Table 3: India Specialty Fertilizer Industry Revenue billion Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 4: India Specialty Fertilizer Industry Revenue billion Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 5: India Specialty Fertilizer Industry Revenue billion Forecast, by Price Trend Analysis 2020 & 2033

- Table 6: India Specialty Fertilizer Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 7: India Specialty Fertilizer Industry Revenue billion Forecast, by Production Analysis 2020 & 2033

- Table 8: India Specialty Fertilizer Industry Revenue billion Forecast, by Consumption Analysis 2020 & 2033

- Table 9: India Specialty Fertilizer Industry Revenue billion Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 10: India Specialty Fertilizer Industry Revenue billion Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 11: India Specialty Fertilizer Industry Revenue billion Forecast, by Price Trend Analysis 2020 & 2033

- Table 12: India Specialty Fertilizer Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the India Specialty Fertilizer Industry?

The projected CAGR is approximately 6.3%.

2. Which companies are prominent players in the India Specialty Fertilizer Industry?

Key companies in the market include Chambal Fertilizers & Chemicals Ltd, Mangalore Chemicals & Fertilizers Ltd, Coromandel International Ltd, Haifa Group, Deepak fertilizers & Petrochemicals Corporation Ltd, Indian Farmers Fertiliser Cooperative Limited, Grupa Azoty S A (Compo Expert), Yara International AS, ICL Group Ltd, Sociedad Quimica y Minera de Chile SA.

3. What are the main segments of the India Specialty Fertilizer Industry?

The market segments include Production Analysis, Consumption Analysis, Import Market Analysis (Value & Volume), Export Market Analysis (Value & Volume), Price Trend Analysis.

4. Can you provide details about the market size?

The market size is estimated to be USD 39.9 billion as of 2022.

5. What are some drivers contributing to market growth?

Shortage of Skilled Labor; Government Support to Enhance Farm Mechanization.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Heavy Initial Procurement Cost and High Expenditure on Maintenance.

8. Can you provide examples of recent developments in the market?

November 2019: IFFCO Launches its Nano Technology based Products nano nitrogen, nano zinc and nano copper for on- field trials as part of its efforts to cut United Statesge of chemical fertilisers and boost farmers' income.February 2019: Coromandel International announced a strategic partnership with Agrinos. The partnership allows Coromandel to widen its product offerings of complete plant nutrition solutions, organic fertilizers, and specialty nutrients. Coromandel, in partnership with Agrinos, will offer growers high-technology inputs under the brand name ARITHRI.November 2018: ICL Fertilizers developed a new line of premium fertilizers that help farmers feed their crops precisely. Polysulphate, ICLPotashpluS, and ICLPKpluS are manufactured from polyhalite, a mineral extracted at the ICL mine in Boulby, United Kingdom, to meet the agricultural need for balanced, targeted nutrition.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "India Specialty Fertilizer Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the India Specialty Fertilizer Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the India Specialty Fertilizer Industry?

To stay informed about further developments, trends, and reports in the India Specialty Fertilizer Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence