Key Insights

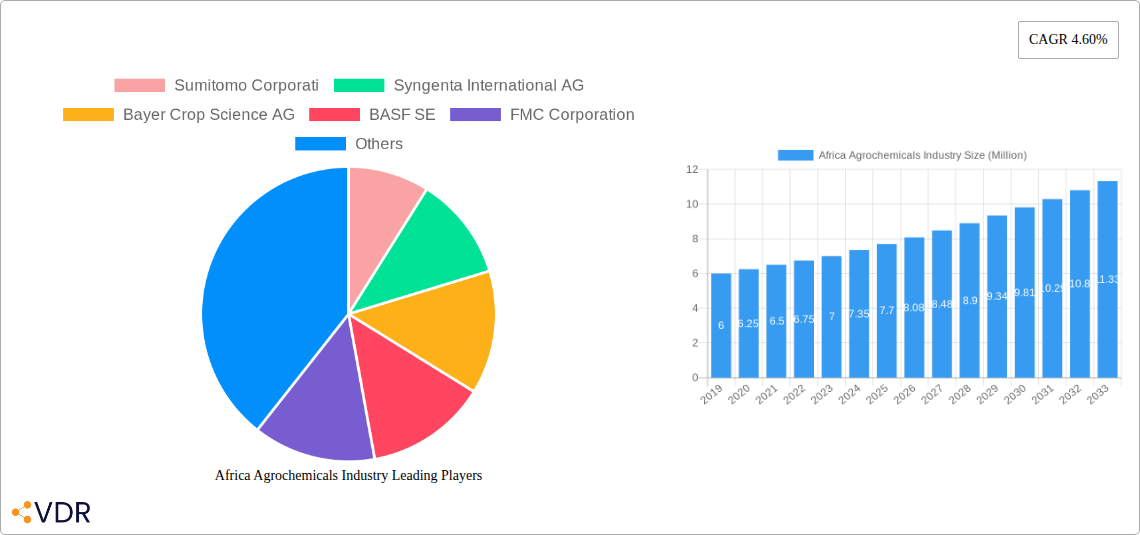

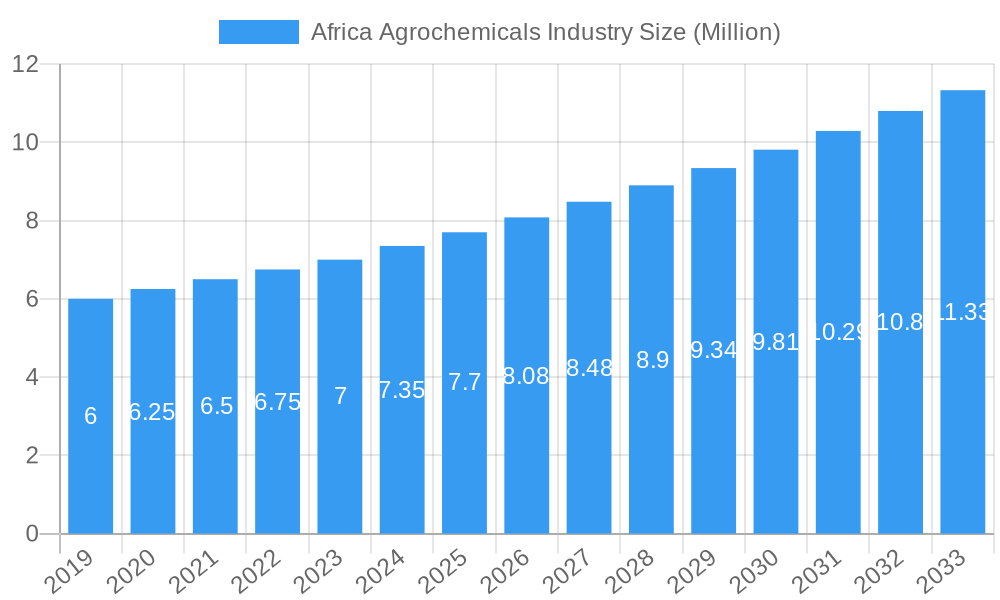

The African agrochemicals market is poised for significant expansion, projected to reach USD 7.70 billion by 2025, with a robust Compound Annual Growth Rate (CAGR) of 4.60% anticipated through 2033. This growth is propelled by a confluence of critical drivers, including the increasing need for enhanced food security across a burgeoning population, the adoption of modern agricultural practices, and a rising awareness among farmers regarding the benefits of crop protection and yield enhancement solutions. Furthermore, government initiatives aimed at modernizing the agricultural sector and fostering foreign investment are creating a more conducive environment for market players. The demand for a diverse range of agrochemicals, from pesticides and herbicides to fertilizers and biostimulants, is set to escalate as farmers strive to maximize their output and improve the quality of their produce. This dynamic landscape presents substantial opportunities for both established global corporations and emerging regional players.

Africa Agrochemicals Industry Market Size (In Million)

Despite the optimistic outlook, certain restraints may temper the pace of growth. These include the high cost of certain agrochemical products, which can be a barrier for smallholder farmers, along with the complex regulatory frameworks that vary across different African nations. Additionally, issues related to inadequate distribution networks and limited access to credit for farmers can pose challenges. Nevertheless, the overarching trend towards sustainable agriculture and the increasing availability of more affordable and environmentally friendly agrochemical solutions are expected to mitigate these concerns. Innovations in product formulations, such as slow-release fertilizers and targeted pest control methods, will play a crucial role in addressing farmer needs and regulatory demands. The market segments, encompassing production, consumption, import/export dynamics, and price trends, are all expected to witness significant activity, reflecting the continent's growing agricultural prowess. Leading companies like Sumitomo Corporation, Syngenta, Bayer Crop Science, BASF SE, and FMC Corporation are actively engaged in this market, developing and distributing a wide array of agrochemical products tailored to the specific needs of African agriculture.

Africa Agrochemicals Industry Company Market Share

This comprehensive report provides an in-depth analysis of the Africa Agrochemicals Industry, forecasting its trajectory from 2019 to 2033, with a base and estimated year of 2025. It delves into market dynamics, growth trends, regional dominance, product landscape, key drivers, barriers, challenges, emerging opportunities, and growth accelerators, offering valuable insights for industry professionals, investors, and policymakers. The report meticulously examines both parent and child markets, presenting all values in millions of units for clarity and ease of comparison.

Africa Agrochemicals Industry Market Dynamics & Structure

The Africa Agrochemicals Industry is characterized by a moderately consolidated market, with global giants like Syngenta International AG, Bayer Crop Science AG, BASF SE, and Corteva Agrisciences holding significant influence. Technological innovation is a key driver, with a growing emphasis on precision agriculture, biopesticides, and sustainable farming solutions. Regulatory frameworks across African nations are evolving, creating both opportunities and challenges for market entry and product registration. Competitive product substitutes, ranging from traditional chemical pesticides to bio-based alternatives, necessitate a nuanced market approach. End-user demographics are diverse, encompassing smallholder farmers to large commercial agricultural operations, each with distinct needs and adoption capacities. Mergers and acquisitions (M&A) trends, while not as pronounced as in developed markets, are observed as companies seek to expand their footprint and product portfolios across the continent.

- Market Concentration: Dominated by key global players, with a gradual emergence of regional players.

- Technological Innovation: Focus on digital farming tools, biological crop protection, and advanced formulation technologies.

- Regulatory Landscape: Nascent but developing, with efforts to harmonize standards and streamline registration processes.

- Competitive Substitutes: Increasing demand for bio-pesticides and integrated pest management (IPM) solutions.

- End-User Demographics: Diverse, requiring tailored product offerings and support.

- M&A Activity: Strategic acquisitions aimed at market penetration and portfolio enhancement.

Africa Agrochemicals Industry Growth Trends & Insights

The Africa Agrochemicals Industry is poised for robust growth, driven by increasing agricultural productivity demands to feed a burgeoning population and rising disposable incomes. The adoption rate of advanced agrochemical solutions is steadily climbing, fueled by greater awareness of their benefits in enhancing crop yields and reducing post-harvest losses. Technological disruptions are transforming the industry, with the integration of data analytics, drone technology for application, and the development of climate-resilient crop protection products. Consumer behavior is shifting towards a demand for safer, more sustainable food production methods, indirectly boosting the market for bio-based and environmentally friendly agrochemicals. The compound annual growth rate (CAGR) for the forecast period is projected at XX%, indicating significant market penetration and expansion.

The market size evolution showcases a consistent upward trend, propelled by several key factors. Government initiatives promoting food security and agricultural modernization play a crucial role. Investments in agricultural research and development are leading to the introduction of more effective and targeted agrochemical solutions. Furthermore, the increasing prevalence of crop diseases and pest infestations, exacerbated by climate change, creates a continuous demand for crop protection products. The growing export potential of African agricultural produce also necessitates higher quality and quantity outputs, further stimulating agrochemical consumption. Market penetration is expected to deepen, particularly in regions with developing agricultural sectors, as farmers gain access to and trust in modern farming inputs. The ongoing digital transformation in agriculture will further enable precision application and monitoring, optimizing resource utilization and enhancing the efficacy of agrochemicals.

Dominant Regions, Countries, or Segments in Africa Agrochemicals Industry

The Consumption Analysis segment is currently the dominant force driving the Africa Agrochemicals Industry, with a substantial market share driven by the continent's vast agricultural land and increasing focus on food security. South Africa consistently emerges as a leading country within the agrochemicals market, owing to its well-established agricultural infrastructure, significant commercial farming operations, and advanced adoption of modern farming practices. Economic policies supportive of the agricultural sector, coupled with significant investments in irrigation and farm mechanization, further bolster its dominance.

- Production Analysis: While production capabilities are growing, they are still developing and often focused on specific segments or formulations. Key production hubs are emerging in countries with strong chemical manufacturing bases.

- Consumption Analysis: This segment leads due to the sheer demand for crop protection and enhancement products across diverse farming systems. It is characterized by a growing appetite for both conventional and increasingly, biological agrochemicals.

- Import Market Analysis (Value & Volume): High import volumes are observed as Africa relies on international suppliers for a wide range of agrochemical products, especially specialized formulations. This segment is crucial for meeting immediate demand and accessing innovative products.

- Export Market Analysis (Value & Volume): While historically lower, the export market is showing promising growth as African countries begin to develop their own niche agrochemical products and formulations for regional and niche international markets.

- Price Trend Analysis: Prices are influenced by global commodity prices, currency fluctuations, and local import duties. There is a gradual trend towards premium pricing for innovative and sustainable solutions.

The dominance of the consumption segment is underscored by the critical need to enhance food production. Economic policies aimed at boosting agricultural output, such as subsidies for inputs and farmer training programs, directly translate into higher agrochemical demand. Infrastructure development, including improved logistics and storage facilities, facilitates the efficient distribution and utilization of these products. The growth potential in this segment remains immense, as a significant portion of arable land is yet to be optimally cultivated, presenting a clear opportunity for sustained agrochemical market expansion.

Africa Agrochemicals Industry Product Landscape

The product landscape in the Africa Agrochemicals Industry is witnessing a significant evolution, with a growing emphasis on innovation and efficacy. Key product categories include herbicides, insecticides, fungicides, and plant growth regulators, with increasing research and development focused on bio-pesticides and integrated pest management solutions. Products like Bayer's Flipper and Serenade are notable for their effectiveness in organic production, complementing conventional offerings. Corteva Agrisciences' Aubaine 518 SC herbicide exemplifies the trend towards targeted solutions for specific crops and weed challenges. The performance metrics of these products are increasingly evaluated not just on yield enhancement but also on environmental impact and farmer safety.

Key Drivers, Barriers & Challenges in Africa Agrochemicals Industry

Key Drivers:

- Growing Food Demand: A rapidly expanding population necessitates increased agricultural output, driving the demand for agrochemicals.

- Government Support: Policies promoting food security and agricultural modernization are significant catalysts.

- Technological Advancements: Introduction of precision agriculture, biopesticides, and digital farming tools enhances efficacy and adoption.

- Climate Change Adaptation: Need for crop protection against evolving pest and disease pressures.

- Foreign Direct Investment: Influx of capital into the agricultural sector, including agrochemical manufacturing and distribution.

Barriers & Challenges:

- Regulatory Hurdles: Complex and varying registration processes across different countries can delay market entry.

- Limited Farmer Education: Low awareness and understanding of optimal product usage and benefits among smallholder farmers.

- Supply Chain Inefficiencies: Poor infrastructure and logistics can lead to availability issues and increased costs.

- Financial Constraints: Limited access to credit for farmers to purchase expensive agrochemical inputs.

- Counterfeit Products: The prevalence of substandard and counterfeit agrochemicals erodes trust and market integrity.

- Environmental Concerns: Growing scrutiny over the environmental impact of chemical pesticides, pushing for sustainable alternatives.

Emerging Opportunities in Africa Agrochemicals Industry

Emerging opportunities in the Africa Agrochemicals Industry lie in the burgeoning demand for biological crop protection solutions, driven by consumer preferences for organic and sustainably produced food. Untapped markets in various sub-Saharan African countries, with their vast agricultural potential and increasing investment, present significant growth avenues. Innovative applications, such as drone-based targeted spraying and smart farming technologies, offer enhanced efficiency and reduced environmental impact. The development of climate-resilient agrochemicals tailored to the specific challenges faced by African agriculture, like drought and heat stress, also presents a lucrative opportunity.

Growth Accelerators in the Africa Agrochemicals Industry Industry

Technological breakthroughs in developing cost-effective and potent biopesticides are key growth accelerators. Strategic partnerships between multinational corporations and local enterprises are crucial for market penetration and navigating regulatory landscapes. Furthermore, expansion strategies focusing on capacity building and farmer training programs will foster greater adoption and utilization of advanced agrochemical solutions, thereby accelerating market growth.

Key Players Shaping the Africa Agrochemicals Industry Market

- Sumitomo Corporation

- Syngenta International AG

- Bayer Crop Science AG

- BASF SE

- FMC Corporation

- Corteva Agrisciences

- UPL

- Yara International

- Nufar

- Adama Agricultural Solutions

Notable Milestones in Africa Agrochemicals Industry Sector

- January 2023: Bayer announced its Partnership with French company M2i Group which will provide Pheromone-based biological Crop Protection products. Bayer will integrate M2i's innovative press application technology into the product to form a digitally enabled solution.

- February 2022: Bayer and Kimitec announced their partnership for the development and commercialization of crop protection Products. Kimitec and Bayer are working together on the development of biological products that will provide a better solution for crop protection.

- February 2022: Bayer launched new products in the crop protection segment called Flipper and Serenade, which provide excellent control options in all organic production and complement Bayer's conventional crop protection.

- March 2022: Corteva Agrisciences launched its latest crop protection solution, Aubaine 518 SC herbicide, to South African wheat farmers to control wheat crop weeds, particularly in regions that experience widespread winter rainfall.

In-Depth Africa Agrochemicals Industry Market Outlook

The future market potential of the Africa Agrochemicals Industry is exceptionally bright, driven by the continuous need for enhanced agricultural productivity and food security. Strategic opportunities abound in the development and widespread adoption of sustainable and biological agrochemical solutions, aligning with global environmental trends and local farmer needs. Continued investment in research and development for climate-resilient products, coupled with robust farmer education initiatives and efficient supply chain development, will solidify Africa's position as a key growth market for agrochemicals. The integration of digital technologies will further optimize application and yield, creating a positive feedback loop for market expansion.

Africa Agrochemicals Industry Segmentation

- 1. Production Analysis

- 2. Consumption Analysis

- 3. Import Market Analysis (Value & Volume)

- 4. Export Market Analysis (Value & Volume)

- 5. Price Trend Analysis

Africa Agrochemicals Industry Segmentation By Geography

-

1. Africa

- 1.1. Nigeria

- 1.2. South Africa

- 1.3. Egypt

- 1.4. Kenya

- 1.5. Ethiopia

- 1.6. Morocco

- 1.7. Ghana

- 1.8. Algeria

- 1.9. Tanzania

- 1.10. Ivory Coast

Africa Agrochemicals Industry Regional Market Share

Geographic Coverage of Africa Agrochemicals Industry

Africa Agrochemicals Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.60% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Production Analysis

- 5.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 5.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 5.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 5.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. Africa

- 6. Africa Agrochemicals Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Production Analysis

- 6.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 6.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 6.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 6.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Sumitomo Corporati

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Syngenta International AG

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Bayer Crop Science AG

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 BASF SE

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 FMC Corporation

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Corteva Agrisciences

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 UPL

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Yara International

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Nufar

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Adama Agricultural Solutions

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Sumitomo Corporati

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Africa Agrochemicals Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Africa Agrochemicals Industry Share (%) by Company 2025

List of Tables

- Table 1: Africa Agrochemicals Industry Revenue Million Forecast, by Production Analysis 2020 & 2033

- Table 2: Africa Agrochemicals Industry Revenue Million Forecast, by Consumption Analysis 2020 & 2033

- Table 3: Africa Agrochemicals Industry Revenue Million Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 4: Africa Agrochemicals Industry Revenue Million Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 5: Africa Agrochemicals Industry Revenue Million Forecast, by Price Trend Analysis 2020 & 2033

- Table 6: Africa Agrochemicals Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 7: Africa Agrochemicals Industry Revenue Million Forecast, by Production Analysis 2020 & 2033

- Table 8: Africa Agrochemicals Industry Revenue Million Forecast, by Consumption Analysis 2020 & 2033

- Table 9: Africa Agrochemicals Industry Revenue Million Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 10: Africa Agrochemicals Industry Revenue Million Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 11: Africa Agrochemicals Industry Revenue Million Forecast, by Price Trend Analysis 2020 & 2033

- Table 12: Africa Agrochemicals Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Nigeria Africa Agrochemicals Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: South Africa Africa Agrochemicals Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Egypt Africa Agrochemicals Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Kenya Africa Agrochemicals Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Ethiopia Africa Agrochemicals Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Morocco Africa Agrochemicals Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Ghana Africa Agrochemicals Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Algeria Africa Agrochemicals Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Tanzania Africa Agrochemicals Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Ivory Coast Africa Agrochemicals Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Africa Agrochemicals Industry?

The projected CAGR is approximately 4.60%.

2. Which companies are prominent players in the Africa Agrochemicals Industry?

Key companies in the market include Sumitomo Corporati, Syngenta International AG, Bayer Crop Science AG, BASF SE, FMC Corporation, Corteva Agrisciences, UPL, Yara International, Nufar, Adama Agricultural Solutions.

3. What are the main segments of the Africa Agrochemicals Industry?

The market segments include Production Analysis, Consumption Analysis, Import Market Analysis (Value & Volume), Export Market Analysis (Value & Volume), Price Trend Analysis.

4. Can you provide details about the market size?

The market size is estimated to be USD 7.70 Million as of 2022.

5. What are some drivers contributing to market growth?

Adoption of Organic and Eco-friendly Farming Practices; Declining Area of Arable Land and Rising Food Security Concerns.

6. What are the notable trends driving market growth?

Growing Food Demand Due to High Population Growth.

7. Are there any restraints impacting market growth?

High Demand for Conventional and Synthetic Products; Lack of Awareness and Other Factors Limiting the Adoption of Agricultural Inoculants.

8. Can you provide examples of recent developments in the market?

January 2023: Bayer announced its Partnership with French company M2i Group which will provide Pheromone-based biological Crop Protection products. Bayer will integrate M2i's innovative press application technology into the product to form a digitally enabled solution.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Africa Agrochemicals Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Africa Agrochemicals Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Africa Agrochemicals Industry?

To stay informed about further developments, trends, and reports in the Africa Agrochemicals Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence