Key Insights

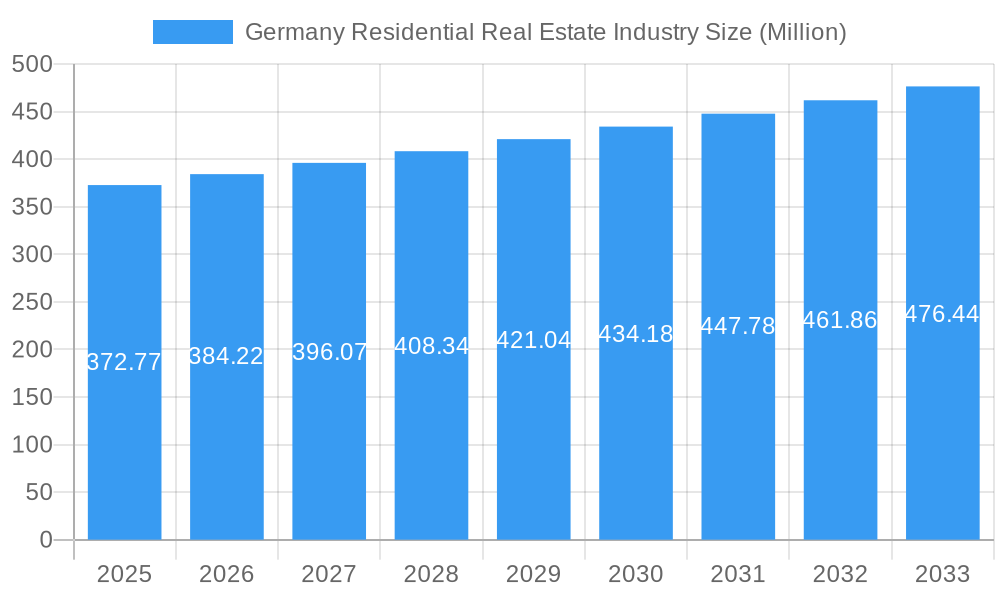

The Germany Residential Real Estate Industry is poised for steady expansion, with a current market size of approximately USD 372.77 million. This growth is underpinned by a projected Compound Annual Growth Rate (CAGR) exceeding 3.06% from 2025 to 2033. Key drivers for this sustained momentum include increasing urbanization, a persistent demand for quality housing, and supportive government initiatives aimed at boosting homeownership and rental affordability. The market's resilience is further bolstered by a robust economic environment and a growing population, particularly in key metropolitan areas. Furthermore, the sector is witnessing a notable trend towards sustainable and energy-efficient housing solutions, reflecting a growing environmental consciousness among both developers and consumers. Smart home technologies are also gaining traction, enhancing the appeal and functionality of residential properties. The landscape is characterized by a diverse range of property types, from villas and landed houses to condominiums and apartments, catering to a broad spectrum of buyer and renter preferences.

Germany Residential Real Estate Industry Market Size (In Million)

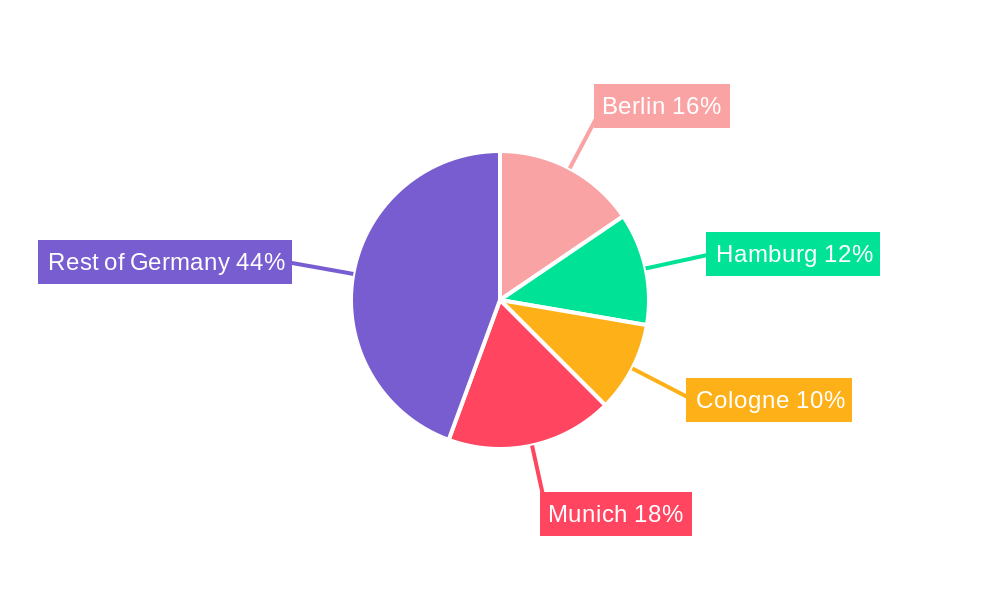

Despite the positive outlook, certain factors present challenges. Rising construction costs, including labor and material expenses, could impact profitability and potentially slow down the pace of development. Additionally, stringent regulatory frameworks and zoning laws in certain regions may create hurdles for new projects. Nevertheless, the industry is actively adapting through innovative construction methods and a focus on optimizing existing infrastructure. The market is segmented across major German cities such as Berlin, Hamburg, Cologne, and Munich, alongside the broader "Rest of Germany" category, each exhibiting unique growth dynamics and demand patterns. Major players like Vonovia SE, Deutsche Wohnen SE, and LEG Immobilien SE are instrumental in shaping the market through strategic investments, portfolio expansions, and a commitment to developing a diverse and accessible housing stock. These companies are at the forefront of addressing housing needs across different segments and price points, ensuring continued market vitality.

Germany Residential Real Estate Industry Company Market Share

This comprehensive report delves into the intricate workings of the Germany Residential Real Estate Industry, providing an in-depth analysis of its current state and future trajectory. Covering a study period from 2019 to 2033, with a base and estimated year of 2025, this report leverages extensive data and expert insights to illuminate market dynamics, growth trends, regional dominance, product innovations, key drivers, emerging opportunities, and the competitive landscape. Designed for industry professionals, investors, and stakeholders, this report offers actionable intelligence to navigate the complexities and capitalize on the opportunities within one of Europe's most robust real estate markets.

Germany Residential Real Estate Industry Market Dynamics & Structure

The Germany Residential Real Estate Industry is characterized by a moderate market concentration, with a few large players holding significant market share, alongside a fragmented landscape of smaller developers and cooperatives. Technological innovation is increasingly driven by the demand for sustainable building practices, smart home integration, and digital property management solutions. Regulatory frameworks, particularly stringent building codes and environmental standards, play a crucial role in shaping development and investment. Competitive product substitutes are primarily found in the form of rental market dynamics and evolving housing preferences, such as co-living spaces. End-user demographics are shifting towards a greater demand for energy-efficient properties, smaller urban dwellings, and properties with access to green spaces. Mergers and acquisitions (M&A) trends indicate a consolidation of larger entities seeking economies of scale and portfolio diversification, while smaller firms focus on niche markets.

- Market Concentration: While major players dominate, a robust ecosystem of regional developers and housing cooperatives contributes to market diversity.

- Technological Innovation Drivers: Sustainability mandates, digitalization of property transactions, and the integration of smart home technologies are key innovation drivers.

- Regulatory Frameworks: Strict building regulations, energy efficiency standards (e.g., KfW), and urban planning policies significantly influence market activity.

- Competitive Product Substitutes: The robust rental market, evolving co-living models, and the increasing popularity of serviced apartments offer alternatives to traditional ownership.

- End-User Demographics: Growing demand for affordable housing, environmentally conscious properties, and flexible living arrangements are reshaping consumer preferences.

- M&A Trends: Consolidation among large real estate companies and strategic acquisitions of smaller, specialized firms are observed trends.

Germany Residential Real Estate Industry Growth Trends & Insights

The Germany Residential Real Estate Industry is poised for sustained growth, driven by a confluence of economic stability, favorable demographic trends, and a persistent housing shortage in key urban centers. The market size evolution is projected to demonstrate a steady upward trajectory, with an estimated Compound Annual Growth Rate (CAGR) of approximately 3.5% over the forecast period. Adoption rates for sustainable building technologies and smart home solutions are on the rise, reflecting increasing consumer awareness and regulatory push. Technological disruptions, such as the application of AI in property valuation and management, and the use of prefabrication in construction, are set to enhance efficiency and affordability. Consumer behavior shifts are evident in the increasing preference for energy-efficient homes, flexible living spaces, and properties that offer a good work-life balance. The market penetration of green building certifications is expected to increase significantly.

The robust economic performance of Germany, coupled with historically low interest rates preceding recent adjustments, has fueled demand for residential properties. The demographic shift, with an aging population and continued urbanization, creates a sustained need for diverse housing options. The report highlights a significant increase in demand for condominiums and apartments in metropolitan areas, driven by young professionals and smaller households. Simultaneously, the segment of villas and landed houses in suburban and rural areas continues to attract families and individuals seeking more space. The base year of 2025 marks a crucial point for analyzing market recovery and adaptation post-pandemic influences, with the forecast period of 2025–2033 indicating a period of stable and predictable expansion. The historical period from 2019 to 2024 provides a baseline for understanding pre-existing market dynamics and the initial impacts of global economic shifts. Insights into evolving consumer preferences, such as the growing importance of community living, remote work-friendly infrastructure, and proximity to amenities, will shape future development strategies. The adoption of digital tools for property search, virtual tours, and online transaction processing is accelerating, improving accessibility and efficiency. The market penetration of sustainable housing solutions is expected to surpass previous benchmarks as environmental consciousness becomes a primary purchasing factor.

Dominant Regions, Countries, or Segments in Germany Residential Real Estate Industry

Within the Germany Residential Real Estate Industry, Condominiums and Apartments represent the dominant segment driving market growth, particularly in key cities like Berlin, Hamburg, and Munich. This dominance is fueled by ongoing urbanization, a growing population of young professionals and smaller households, and a persistent undersupply of housing in these metropolitan hubs. The "Rest of Germany" also contributes significantly to overall market volume, driven by a more balanced demand for both apartments and landed properties in its diverse sub-regions.

Key Drivers for Condominiums and Apartments:

- Urbanization and Population Density: Major cities attract a high concentration of people seeking career opportunities, leading to increased demand for urban living solutions.

- Affordability and Accessibility: While prices are high, apartments often offer a more attainable entry point into property ownership compared to villas and landed houses in prime locations.

- Lifestyle Preferences: Modern lifestyles, characterized by a desire for convenience, proximity to amenities, and less maintenance, favor apartment living.

- Investment Potential: Apartments in sought-after urban areas continue to demonstrate strong rental yields and capital appreciation.

Dominance Factors:

- Market Share: Condominiums and apartments account for an estimated 65% of new residential construction starts and a significant portion of the existing housing stock.

- Growth Potential: The segment is projected to experience a higher growth rate compared to villas and landed houses due to sustained demand pressure in urban centers.

- Economic Policies: Government initiatives aimed at increasing housing supply and promoting affordable urban living indirectly support this segment.

- Infrastructure Development: Investment in public transportation and urban amenities further enhances the attractiveness of apartment living in cities.

While villas and landed houses hold significant appeal, especially in suburban and more rural "Rest of Germany" areas, their market share is comparatively smaller due to land availability constraints and higher price points. However, they cater to a crucial demographic seeking family-oriented living, larger spaces, and private outdoor areas.

Germany Residential Real Estate Industry Product Landscape

The product landscape within the Germany Residential Real Estate Industry is increasingly defined by a focus on sustainability, energy efficiency, and smart home integration. Innovations range from advanced insulation materials and renewable energy sources like solar panels to intelligent building management systems that optimize energy consumption and enhance resident comfort. The rise of modular and prefabricated construction techniques is also reshaping the industry, offering faster build times and greater cost predictability. Performance metrics are being driven by stricter energy performance certificates (EPCs) and certifications like DGNB (German Sustainable Building Council), emphasizing a shift towards higher quality and environmentally responsible construction. Unique selling propositions increasingly include features like low-emission heating systems, smart thermostats, and integrated digital access control.

Key Drivers, Barriers & Challenges in Germany Residential Real Estate Industry

Key Drivers: The Germany Residential Real Estate Industry is propelled by a persistent housing shortage, particularly in metropolitan areas, a stable economy underpinning strong demand, and government support for energy-efficient construction through subsidies and favorable loan programs. Technological advancements in construction and property management are also key drivers, enhancing efficiency and sustainability.

Barriers & Challenges: Significant barriers include rising construction material costs and labor shortages, which drive up development expenses. Stringent regulatory requirements and lengthy permitting processes can delay projects. Furthermore, the increasing complexity of zoning laws and the push for higher environmental standards present ongoing challenges. Competitive pressures from a multitude of developers and the growing popularity of alternative housing models like co-living also contribute to the dynamic landscape. Supply chain disruptions remain a persistent concern.

Emerging Opportunities in Germany Residential Real Estate Industry

Emerging opportunities lie in the development of sustainable and energy-positive buildings, catering to the growing demand for eco-friendly living. The renovation and retrofitting of existing building stock to meet modern energy efficiency standards represent a significant untapped market. Furthermore, the increasing demand for specialized housing, such as senior living facilities and affordable housing solutions in underserved urban and suburban areas, presents lucrative avenues. The integration of proptech solutions for enhanced property management, digital transactions, and smart community features also offers substantial growth potential.

Growth Accelerators in the Germany Residential Real Estate Industry Industry

Growth in the Germany Residential Real Estate Industry is being accelerated by significant investments in renewable energy integration within new and existing properties, alongside advancements in digital platforms that streamline property searches, transactions, and management. Strategic partnerships between construction companies, technology providers, and financing institutions are fostering innovation and improving project delivery. Furthermore, targeted government incentives aimed at boosting housing construction and encouraging sustainable development are playing a crucial role. The expansion of infrastructure in secondary cities, making them more attractive for residents and businesses, is also a key growth accelerator.

Key Players Shaping the Germany Residential Real Estate Industry Market

- Deutsche Wohnen SE

- Wohnungsbaugenossenschaft Musikwinkel eG (WBG)

- Consus Real Estate

- Vonovia SE

- Residia Care Holding GmbH & Co

- SAGA Siedlungs-Aktiengesellschaft Hamburg

- Vivawest

- ABG Frankfurt Holding

- Degewo

- LEG Immobilien SE

- 63 Other Companies

Notable Milestones in Germany Residential Real Estate Industry Sector

- 2020: Increased focus on digitalization of sales and property management processes due to global pandemic.

- 2021: Strong government stimulus packages for housing construction and energy-efficient renovations announced.

- 2022: Growing emphasis on ESG (Environmental, Social, and Governance) factors in real estate investment and development.

- 2023: Significant investment in retrofitting existing buildings to improve energy efficiency gains traction.

- 2024: Introduction of new building codes and sustainability standards by the German government.

In-Depth Germany Residential Real Estate Industry Market Outlook

The outlook for the Germany Residential Real Estate Industry remains robust, characterized by sustained demand and a continued focus on sustainable and technologically advanced housing solutions. Growth accelerators, including government initiatives, technological innovation in construction, and evolving consumer preferences for eco-friendly and smart homes, will propel the market forward. Strategic opportunities lie in addressing the persistent housing deficit through innovative development models, expanding into emerging urban and suburban growth corridors, and leveraging proptech for enhanced efficiency and customer experience. The market is poised for a period of steady expansion and transformation.

Germany Residential Real Estate Industry Segmentation

-

1. Type

- 1.1. Villas and Landed Houses

- 1.2. Condominiums and Apartments

-

2. Key Cities

- 2.1. Berlin

- 2.2. Hamburg

- 2.3. Cologne

- 2.4. Munich

- 2.5. Rest of Germany

Germany Residential Real Estate Industry Segmentation By Geography

- 1. Germany

Germany Residential Real Estate Industry Regional Market Share

Geographic Coverage of Germany Residential Real Estate Industry

Germany Residential Real Estate Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of > 3.06% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Villas and Landed Houses

- 5.1.2. Condominiums and Apartments

- 5.2. Market Analysis, Insights and Forecast - by Key Cities

- 5.2.1. Berlin

- 5.2.2. Hamburg

- 5.2.3. Cologne

- 5.2.4. Munich

- 5.2.5. Rest of Germany

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Germany

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Germany Residential Real Estate Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Villas and Landed Houses

- 6.1.2. Condominiums and Apartments

- 6.2. Market Analysis, Insights and Forecast - by Key Cities

- 6.2.1. Berlin

- 6.2.2. Hamburg

- 6.2.3. Cologne

- 6.2.4. Munich

- 6.2.5. Rest of Germany

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Deutsche Wohnen SE

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Wohnungsbaugenossenschaft Musikwinkel eG (WBG)

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Consus Real Estate

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Vonovia SE

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Residia Care Holding GmbH & Co

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 SAGA Siedlungs-Aktiengesellschaft Hamburg

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Vivawest

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 ABG Frankfurt Holding**List Not Exhaustive 6 3 Other Companie

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Degewo

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 LEG Immobilien SE

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Deutsche Wohnen SE

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Germany Residential Real Estate Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Germany Residential Real Estate Industry Share (%) by Company 2025

List of Tables

- Table 1: Germany Residential Real Estate Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Germany Residential Real Estate Industry Revenue Million Forecast, by Key Cities 2020 & 2033

- Table 3: Germany Residential Real Estate Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Germany Residential Real Estate Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 5: Germany Residential Real Estate Industry Revenue Million Forecast, by Key Cities 2020 & 2033

- Table 6: Germany Residential Real Estate Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Germany Residential Real Estate Industry?

The projected CAGR is approximately > 3.06%.

2. Which companies are prominent players in the Germany Residential Real Estate Industry?

Key companies in the market include Deutsche Wohnen SE, Wohnungsbaugenossenschaft Musikwinkel eG (WBG), Consus Real Estate, Vonovia SE, Residia Care Holding GmbH & Co, SAGA Siedlungs-Aktiengesellschaft Hamburg, Vivawest, ABG Frankfurt Holding**List Not Exhaustive 6 3 Other Companie, Degewo, LEG Immobilien SE.

3. What are the main segments of the Germany Residential Real Estate Industry?

The market segments include Type, Key Cities.

4. Can you provide details about the market size?

The market size is estimated to be USD 372.77 Million as of 2022.

5. What are some drivers contributing to market growth?

Strong Demand and Rising Construction Activities to Drive the Market; Rising House Prices in Germany Affecting Demand in the Market.

6. What are the notable trends driving market growth?

Strong Demand And Rising Construction Activities To Drive The Market.

7. Are there any restraints impacting market growth?

Weak economic environment.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Germany Residential Real Estate Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Germany Residential Real Estate Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Germany Residential Real Estate Industry?

To stay informed about further developments, trends, and reports in the Germany Residential Real Estate Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence