Key Insights

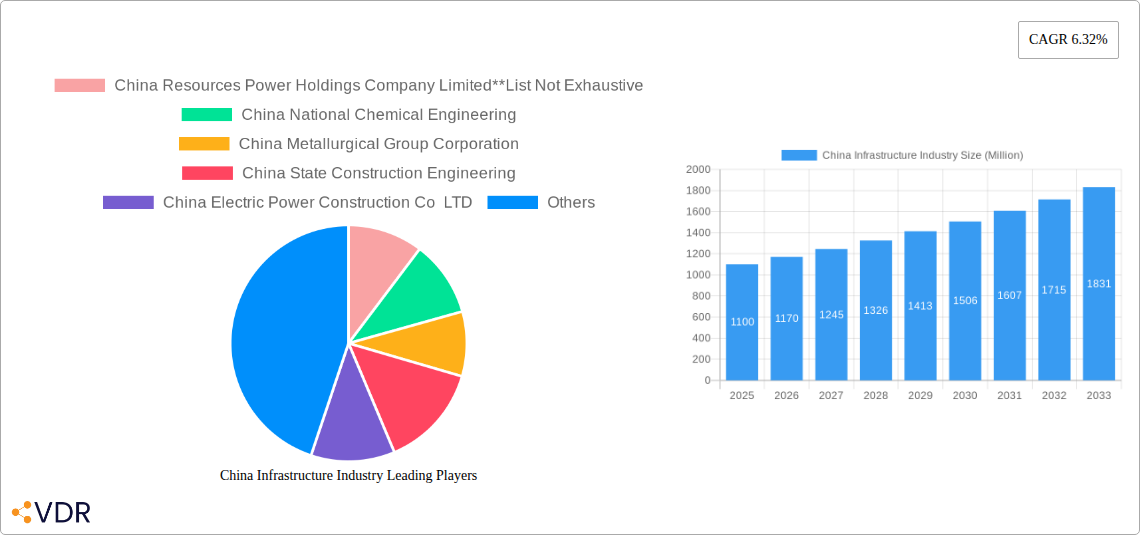

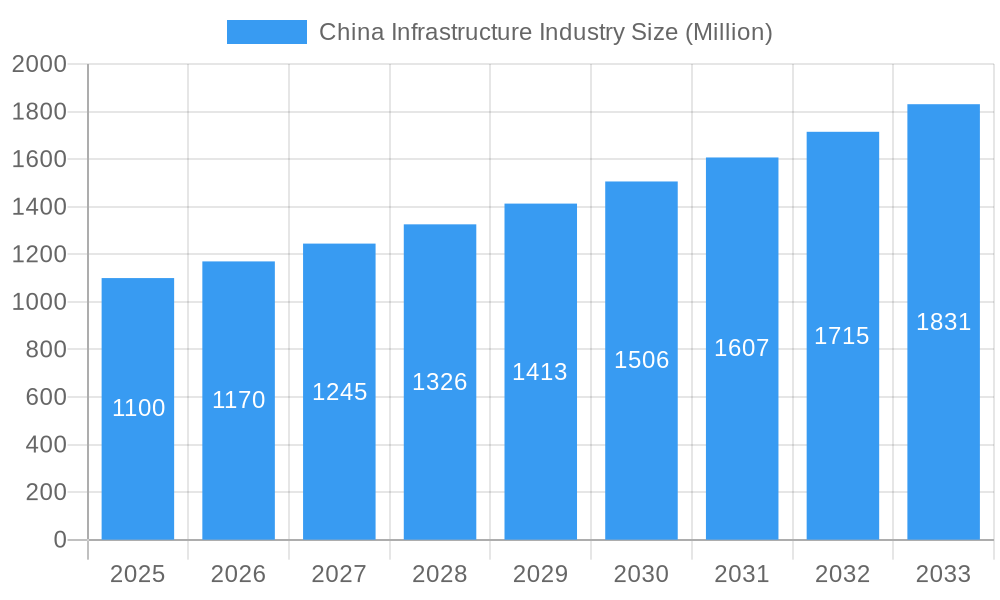

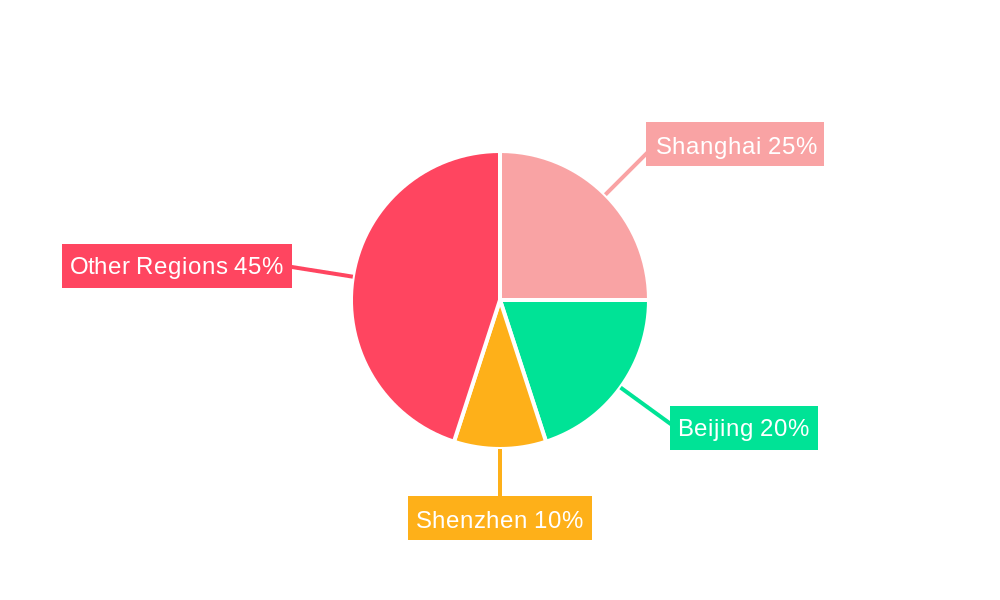

The China infrastructure market, valued at $1.10 billion in 2025, is projected to experience robust growth, driven by significant government investments in social infrastructure (including transportation, waterways, and telecommunications) and manufacturing infrastructure development. A compound annual growth rate (CAGR) of 6.32% from 2025 to 2033 indicates a substantial expansion, reaching an estimated market value exceeding $2 billion by 2033. Key drivers include urbanization, increasing industrial activity, and the government's ongoing commitment to improving connectivity and national infrastructure resilience. While data on specific segment breakdowns is limited, the significant investments in major cities like Shanghai, Beijing, and Shenzhen suggest these regions will contribute disproportionately to overall market growth. Competition is fierce among leading players like China Resources Power Holdings, China National Chemical Engineering, and China State Construction Engineering, highlighting a consolidated market with established industry giants. Continued economic growth and strategic government initiatives are expected to propel this market forward, although potential headwinds such as fluctuating global commodity prices and evolving environmental regulations could influence the growth trajectory.

China Infrastructure Industry Market Size (In Billion)

The robust growth forecast is further supported by the projected increase in demand for advanced technologies in infrastructure construction and maintenance. This includes the adoption of digital technologies for project management, smart city initiatives, and advancements in materials science leading to improved infrastructure longevity and efficiency. The ongoing expansion of the national transportation network, alongside developments in waterway infrastructure and modernization of telecommunications networks, ensures continued demand for infrastructure-related services. The competitive landscape necessitates continuous innovation and efficiency improvements for companies to maintain market share. The government's emphasis on sustainable infrastructure development presents both opportunities and challenges, demanding that companies adapt to evolving environmental regulations and adopt green technologies to minimize environmental impacts.

China Infrastructure Industry Company Market Share

This comprehensive report provides an in-depth analysis of the China infrastructure industry, covering market dynamics, growth trends, key players, and future outlook. With a focus on key segments like social infrastructure, transportation, waterways, telecoms, and manufacturing, the report offers valuable insights for industry professionals, investors, and policymakers. The study period spans 2019-2033, with a base year of 2025 and a forecast period of 2025-2033. Market values are presented in million units.

China Infrastructure Industry Market Dynamics & Structure

The China infrastructure industry is characterized by high market concentration amongst state-owned enterprises (SOEs) and a complex regulatory framework. Technological innovation is driven by government initiatives focused on smart cities and digital infrastructure, while competition is intense, particularly in areas like high-speed rail and renewable energy. Mergers and acquisitions (M&A) activity is significant, primarily involving SOEs seeking to consolidate market share and expand capabilities. Substitute products and services are limited in certain segments, while others face increasing competition from private players and foreign investment. End-user demographics are influenced by rapid urbanization and economic development.

- Market Concentration: Top 5 players hold approximately xx% market share (2024).

- M&A Activity: xx deals valued at xx million USD were recorded between 2019 and 2024.

- Innovation Barriers: Bureaucracy, lack of transparency, and access to funding pose challenges.

- Regulatory Framework: Stringent environmental regulations and land acquisition processes impact project timelines.

China Infrastructure Industry Growth Trends & Insights

The China infrastructure industry experienced robust growth during the historical period (2019-2024), driven by government investments in large-scale projects. The market size is projected to reach xx million units by 2025, exhibiting a CAGR of xx% during the forecast period (2025-2033). Technological disruptions, such as the adoption of 5G and IoT, are transforming the industry, while consumer behavior shifts towards greater demand for sustainable and resilient infrastructure. This expansion is further fueled by increasing urbanization, rising middle-class incomes, and government initiatives promoting technological advancements and international collaboration. The shift towards green infrastructure projects will be another catalyst for expansion, increasing adoption of sustainable materials and technologies.

Dominant Regions, Countries, or Segments in China Infrastructure Industry

The transportation infrastructure segment, particularly high-speed rail and road networks, dominates the market in terms of both value and growth. Key cities like Shanghai, Beijing, and Shenzhen lead in terms of infrastructure development due to their high population density and economic activity. Provincial governments' focus on improving regional connectivity also significantly boosts the growth in certain regions.

- Transportation Infrastructure: Accounts for xx% of the total market in 2025. Key drivers include government initiatives such as the Belt and Road Initiative.

- Shanghai: Highest concentration of infrastructure projects due to its role as a major economic hub and high population density.

- Beijing: Significant government investment in infrastructure development contributes to its market dominance.

- Shenzhen: Focus on technological innovation and smart city initiatives boosts the market in this region.

China Infrastructure Industry Product Landscape

The product landscape is characterized by a wide range of offerings, from traditional construction materials to advanced technologies like smart sensors and AI-powered management systems. Innovation focuses on enhancing efficiency, durability, sustainability, and safety of infrastructure projects. Companies are increasingly integrating digital technologies to improve project management, monitor performance, and optimize resource allocation. Unique selling propositions often center on cost-effectiveness, efficiency, and compliance with stringent environmental regulations.

Key Drivers, Barriers & Challenges in China Infrastructure Industry

Key Drivers: Government investment in large-scale projects; urbanization; economic growth; technological advancements; supportive policies focusing on sustainable development.

Key Challenges: High construction costs; land acquisition difficulties; environmental regulations; competition; financing constraints; skilled labor shortages; supply chain disruptions. The supply chain issues, particularly post-pandemic, have led to xx% increase in project delays in 2024.

Emerging Opportunities in China Infrastructure Industry

Emerging opportunities include the growth of smart cities, the expansion of renewable energy infrastructure, the development of advanced transportation systems, and the increasing demand for resilient infrastructure capable of withstanding natural disasters. These opportunities are particularly apparent in smaller cities and rural areas where infrastructure development lags behind.

Growth Accelerators in the China Infrastructure Industry Industry

Strategic partnerships between domestic and international companies are accelerating growth, bringing in foreign expertise and technologies. Technological breakthroughs in materials science and construction techniques enhance efficiency and sustainability, while initiatives focused on digitalization and smart infrastructure management optimize resource allocation and project delivery. Expansion into underserved markets continues to be a catalyst for growth.

Key Players Shaping the China Infrastructure Industry Market

- China Resources Power Holdings Company Limited

- China National Chemical Engineering

- China Metallurgical Group Corporation

- China State Construction Engineering

- China Electric Power Construction Co LTD

- China Communications Construction Company

- China Energy Engineering Corporation

- Shanghai Construction Group

- China Railway Group Limited

- China Power International Development Limited

- China Railway Construction Corporation

Notable Milestones in China Infrastructure Industry Sector

- 2020, Q4: Launch of the National New Infrastructure Strategy, significantly boosting investment in 5G, AI, and IoT infrastructure.

- 2022, Q2: Completion of the Hong Kong-Zhuhai-Macau Bridge, a landmark project demonstrating advanced engineering capabilities.

- 2023, Q1: Significant increase in investment in renewable energy infrastructure, driven by government targets for carbon neutrality.

In-Depth China Infrastructure Industry Market Outlook

The China infrastructure industry is poised for continued growth driven by government investment, technological innovation, and sustained economic development. Strategic opportunities exist in areas such as smart city development, renewable energy infrastructure, and the upgrading of existing infrastructure to meet the needs of a growing and increasingly affluent population. The focus on sustainable development and improved efficiency will remain key aspects shaping the industry's trajectory.

China Infrastructure Industry Segmentation

-

1. Type

-

1.1. Social Infrastructure

- 1.1.1. Schools

- 1.1.2. Hospitals

- 1.1.3. Defence

- 1.1.4. Other Social Infrastructures

-

1.2. Transportation Infrastructure

- 1.2.1. Railways

- 1.2.2. Roadways

- 1.2.3. Airports

- 1.2.4. Waterways

-

1.3. Extraction Infrastructure

- 1.3.1. Power Generation

- 1.3.2. Electricity Transmission and Distribution

- 1.3.3. Gas

- 1.3.4. Telecoms

-

1.4. Manufacturing Infrastructure

- 1.4.1. Metal and Ore Production

- 1.4.2. Petroleum Refining

- 1.4.3. Chemical Manufacturing

- 1.4.4. Industrial Parks and clusters

- 1.4.5. Other Manufacturing Infrastructures

-

1.1. Social Infrastructure

-

2. Key Cities

- 2.1. Shanghai

- 2.2. Beijing

- 2.3. Shenzhen

China Infrastructure Industry Segmentation By Geography

- 1. China

China Infrastructure Industry Regional Market Share

Geographic Coverage of China Infrastructure Industry

China Infrastructure Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.32% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Social Infrastructure

- 5.1.1.1. Schools

- 5.1.1.2. Hospitals

- 5.1.1.3. Defence

- 5.1.1.4. Other Social Infrastructures

- 5.1.2. Transportation Infrastructure

- 5.1.2.1. Railways

- 5.1.2.2. Roadways

- 5.1.2.3. Airports

- 5.1.2.4. Waterways

- 5.1.3. Extraction Infrastructure

- 5.1.3.1. Power Generation

- 5.1.3.2. Electricity Transmission and Distribution

- 5.1.3.3. Gas

- 5.1.3.4. Telecoms

- 5.1.4. Manufacturing Infrastructure

- 5.1.4.1. Metal and Ore Production

- 5.1.4.2. Petroleum Refining

- 5.1.4.3. Chemical Manufacturing

- 5.1.4.4. Industrial Parks and clusters

- 5.1.4.5. Other Manufacturing Infrastructures

- 5.1.1. Social Infrastructure

- 5.2. Market Analysis, Insights and Forecast - by Key Cities

- 5.2.1. Shanghai

- 5.2.2. Beijing

- 5.2.3. Shenzhen

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. China

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. China Infrastructure Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Social Infrastructure

- 6.1.1.1. Schools

- 6.1.1.2. Hospitals

- 6.1.1.3. Defence

- 6.1.1.4. Other Social Infrastructures

- 6.1.2. Transportation Infrastructure

- 6.1.2.1. Railways

- 6.1.2.2. Roadways

- 6.1.2.3. Airports

- 6.1.2.4. Waterways

- 6.1.3. Extraction Infrastructure

- 6.1.3.1. Power Generation

- 6.1.3.2. Electricity Transmission and Distribution

- 6.1.3.3. Gas

- 6.1.3.4. Telecoms

- 6.1.4. Manufacturing Infrastructure

- 6.1.4.1. Metal and Ore Production

- 6.1.4.2. Petroleum Refining

- 6.1.4.3. Chemical Manufacturing

- 6.1.4.4. Industrial Parks and clusters

- 6.1.4.5. Other Manufacturing Infrastructures

- 6.1.1. Social Infrastructure

- 6.2. Market Analysis, Insights and Forecast - by Key Cities

- 6.2.1. Shanghai

- 6.2.2. Beijing

- 6.2.3. Shenzhen

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 China Resources Power Holdings Company Limited**List Not Exhaustive

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 China National Chemical Engineering

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 China Metallurgical Group Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 China State Construction Engineering

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 China Electric Power Construction Co LTD

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 China Communications Construction Company

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 China Energy Engineering Corporation

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Shanghai Construction Group

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 China Railway Group Limited

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 China Power International Development Limited

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 China Railway Construction Corporation

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.1 China Resources Power Holdings Company Limited**List Not Exhaustive

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China Infrastructure Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: China Infrastructure Industry Share (%) by Company 2025

List of Tables

- Table 1: China Infrastructure Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: China Infrastructure Industry Revenue Million Forecast, by Key Cities 2020 & 2033

- Table 3: China Infrastructure Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: China Infrastructure Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 5: China Infrastructure Industry Revenue Million Forecast, by Key Cities 2020 & 2033

- Table 6: China Infrastructure Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Infrastructure Industry?

The projected CAGR is approximately 6.32%.

2. Which companies are prominent players in the China Infrastructure Industry?

Key companies in the market include China Resources Power Holdings Company Limited**List Not Exhaustive, China National Chemical Engineering, China Metallurgical Group Corporation, China State Construction Engineering, China Electric Power Construction Co LTD, China Communications Construction Company, China Energy Engineering Corporation, Shanghai Construction Group, China Railway Group Limited, China Power International Development Limited, China Railway Construction Corporation.

3. What are the main segments of the China Infrastructure Industry?

The market segments include Type, Key Cities.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.10 Million as of 2022.

5. What are some drivers contributing to market growth?

Asia Pacific countries are investing in infrastructure projects to improve regional connectivity and promote economic integration; The Asia Pacific region has a large and growing population. along with a rising middle class.

6. What are the notable trends driving market growth?

Transportation Infrastructure is Witnessing Significant Growth.

7. Are there any restraints impacting market growth?

Limited public budgets and difficulties in attracting private investment can hinder the financing of large-scale projects; Delays in land acquisition can significantly impact project timelines and costs.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Infrastructure Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Infrastructure Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Infrastructure Industry?

To stay informed about further developments, trends, and reports in the China Infrastructure Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence