Key Insights

The European Artificial Intelligence (AI) in Defense market is set for significant expansion, projected to reach $3.28 billion by 2025, with a Compound Annual Growth Rate (CAGR) of 16% through 2033. This growth is driven by escalating geopolitical tensions and the imperative for enhanced national security. European governments are strategically investing in AI solutions to bolster defense capabilities, including advanced threat detection, predictive maintenance, sophisticated battlefield healthcare, and robust cybersecurity. The integration of AI is now a critical factor for maintaining a strategic advantage in the evolving global security landscape.

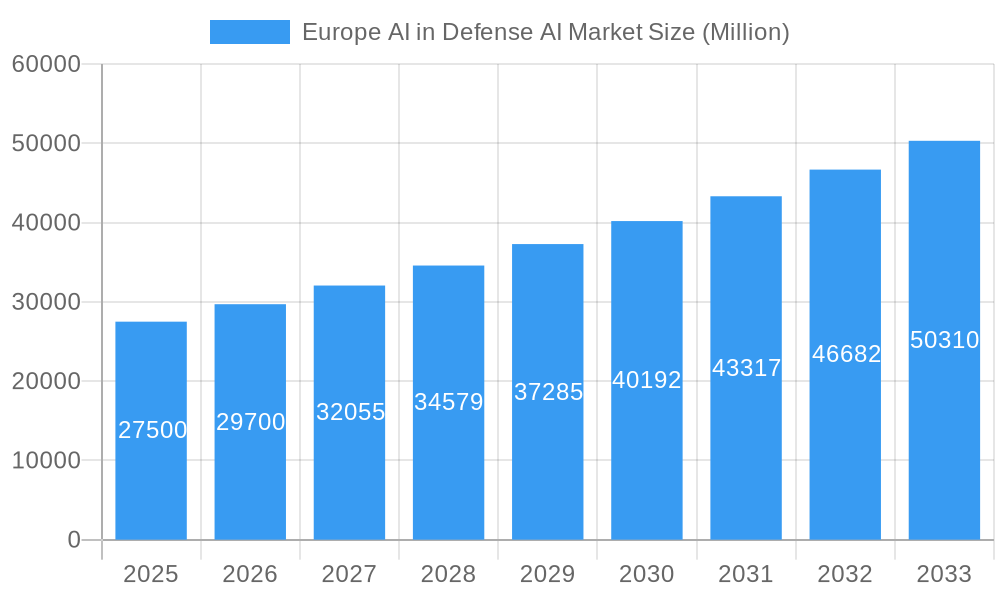

Europe AI in Defense AI Market Market Size (In Billion)

The market exhibits strong demand across hardware, software, and platform solutions. Land, air, and naval applications are all seeing significant AI adoption, reflecting a comprehensive approach to modernizing defense infrastructure. Key application areas like cybersecurity, battlefield healthcare, and warfare platform enhancements are realizing transformative benefits, improving operational efficiency, situational awareness, and personnel safety. Leading companies are at the forefront of AI innovation in this sector. While the market offers immense opportunities, challenges include data security, ethical considerations for autonomous systems, and high implementation costs. However, strategic advantages and the pursuit of technological superiority are expected to drive sustained and significant market growth.

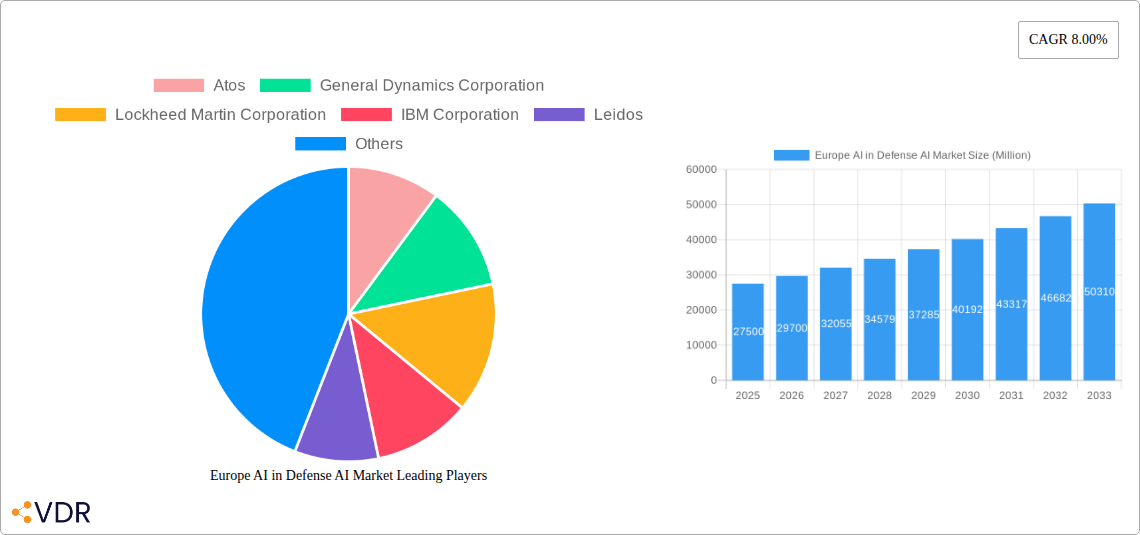

Europe AI in Defense AI Market Company Market Share

This report provides an in-depth analysis of the Europe AI in Defense Market, a sector undergoing rapid digital transformation. It offers valuable insights into AI adoption dynamics within European defense industries for stakeholders. We meticulously examine parent market trends alongside child market developments, presenting a holistic view of market opportunities and challenges. Our analysis covers the historical period (2019-2024), base year (2025), and a forecast period (2025-2033). Discover how AI is reshaping military capabilities, from enhanced cybersecurity and intelligent warfare platforms to advanced battlefield healthcare and autonomous systems.

Europe AI in Defense AI Market Market Dynamics & Structure

The Europe AI in Defense market is characterized by a moderately concentrated structure, with a few dominant players alongside emerging innovators. Technological innovation is the primary driver, fueled by the escalating geopolitical landscape and the continuous need for advanced military capabilities. Regulatory frameworks are evolving to address ethical considerations, data security, and interoperability standards for AI in defense. Competitive product substitutes are primarily traditional defense technologies, but AI is rapidly offering superior alternatives. End-user demographics are defined by government defense ministries, armed forces, and defense contractors prioritizing operational efficiency, enhanced situational awareness, and reduced human risk. Mergers and Acquisitions (M&A) activity is increasing as larger defense conglomerates seek to integrate cutting-edge AI capabilities and smaller specialized AI firms aim for market consolidation and expansion.

- Market Concentration: Dominated by established defense contractors and major technology firms, with increasing M&A activity.

- Technological Innovation Drivers: Geopolitical tensions, demand for autonomous systems, data fusion, predictive maintenance, and advanced C4ISR capabilities.

- Regulatory Frameworks: Focus on ethical AI, data sovereignty, interoperability standards, and the responsible deployment of autonomous weapon systems.

- Competitive Product Substitutes: Traditional defense systems, human-led operations, and less sophisticated automation.

- End-User Demographics: National defense ministries, military branches (Army, Navy, Air Force), defense research agencies, and prime defense contractors.

- M&A Trends: Strategic acquisitions to gain AI expertise, market share, and technology integration capabilities. Significant M&A deal volumes projected in the coming years, with approximately 25-35 deals expected annually by 2028.

Europe AI in Defense AI Market Growth Trends & Insights

The Europe AI in Defense market is poised for substantial growth, driven by an imperative to modernize defense capabilities and maintain strategic advantage in an increasingly complex global environment. The market size is projected to expand significantly from approximately USD 5,500 million in 2025 to over USD 18,000 million by 2033, exhibiting a robust Compound Annual Growth Rate (CAGR) of approximately 15.5% during the forecast period. Adoption rates for AI-driven solutions are accelerating across all defense branches, propelled by the demonstrable benefits in terms of enhanced decision-making, improved operational efficiency, and reduced logistical burdens. Technological disruptions, such as advancements in machine learning, natural language processing, and computer vision, are continuously reshaping the defense landscape, enabling more sophisticated applications in areas like autonomous systems, cyber warfare, and intelligence analysis. Consumer behavior shifts are evident as defense organizations move from experimental AI adoption to full-scale integration, prioritizing solutions that offer quantifiable performance improvements and cost savings through automation and predictive capabilities.

The market's evolution is further shaped by the increasing reliance on big data analytics for strategic insights and threat detection. The ability of AI to process and analyze vast datasets generated by sensors, reconnaissance missions, and operational feedback is critical for effective defense planning and execution. This has led to significant investments in AI-powered intelligence, surveillance, and reconnaissance (ISR) systems, as well as command and control (C2) platforms. The integration of AI into warfare platforms is also a key growth area, with nations investing in AI-enabled unmanned aerial vehicles (UAVs), autonomous ground vehicles, and smart naval systems. Furthermore, the growing awareness of cybersecurity threats has amplified the demand for AI-powered defense solutions that can detect, prevent, and respond to sophisticated cyber-attacks in real-time. The development of AI for battlefield healthcare, including diagnostic tools and robotic surgery assistance, is another nascent but promising segment, aiming to improve soldier well-being and medical response in combat zones. The European Union's initiatives to foster defense cooperation and technological sovereignty are also contributing to the growth, encouraging cross-border R&D and procurement of AI in defense technologies.

Dominant Regions, Countries, or Segments in Europe AI in Defense AI Market

The Air Platform segment is a dominant force within the Europe AI in Defense market, driven by extensive investments in autonomous aerial systems, advanced surveillance, and enhanced combat capabilities. This segment's dominance is underpinned by nations heavily investing in next-generation fighter jets, drones, and airborne early warning systems that leverage AI for improved navigation, target recognition, and mission planning. The technological sophistication of airborne AI solutions, including predictive maintenance and enhanced pilot assistance, provides a significant performance advantage.

Dominant Segment: Platform - Air

- Market Share: Projected to hold approximately 35-40% of the total market value by 2033.

- Key Drivers:

- Technological Advancements: Development of AI-powered autonomous drones, unmanned combat aerial vehicles (UCAVs), and advanced aerial ISR platforms.

- Strategic Importance: Air superiority remains a cornerstone of modern defense strategies, necessitating cutting-edge AI integration.

- R&D Investments: Significant national and multinational investments in advanced avionics, sensor fusion, and AI-driven flight control systems.

- Operational Efficiency: AI optimizes flight paths, fuel consumption, and mission effectiveness for aerial assets.

Leading Countries:

- France: A key player due to its strong aerospace industry and significant investment in AI for defense, exemplified by joint ventures for advanced AI and big data platforms.

- United Kingdom: Demonstrates a clear commitment to AI in defense, with contracts for data analytics platforms to enhance operational efficiency and cost reduction.

- Germany: Actively investing in AI research and development for its armed forces, with a focus on autonomous systems and cybersecurity.

- Italy: Growing emphasis on AI integration into naval and air defense systems, contributing to its market share.

Dominant Applications within Air Platforms:

- Intelligence, Surveillance, and Reconnaissance (ISR): AI enables real-time analysis of aerial imagery and sensor data for enhanced situational awareness.

- Autonomous Flight Operations: AI facilitates the development of highly autonomous UAVs for reconnaissance, strike, and logistics missions.

- Electronic Warfare: AI-powered systems for signal intelligence, jamming, and counter-measures in the aerial domain.

Europe AI in Defense AI Market Product Landscape

The Europe AI in Defense market is characterized by a dynamic product landscape focusing on intelligent automation, predictive analytics, and enhanced situational awareness. Key innovations include AI-powered cybersecurity platforms for threat detection and response, autonomous warfare systems with advanced target recognition, and AI-enhanced battlefield healthcare solutions for improved diagnostics and medical support. Hardware components like specialized processors and sensors are crucial for AI functionality, while advanced software, including machine learning algorithms and data fusion frameworks, drives these capabilities. Platforms range from AI-integrated land vehicles and naval vessels to sophisticated unmanned aerial systems, all designed to improve operational effectiveness, reduce human risk, and optimize resource allocation. Unique selling propositions revolve around enhanced decision-making speed, increased accuracy, and the ability to operate in complex and contested environments.

Key Drivers, Barriers & Challenges in Europe AI in Defense AI Market

Key Drivers: The Europe AI in Defense market is propelled by several critical factors: the escalating geopolitical tensions demanding advanced technological superiority, the imperative to enhance operational efficiency and reduce human risk in combat scenarios, and the rapid advancements in AI technologies such as machine learning and computer vision. Government initiatives aimed at fostering digital transformation within defense sectors and the growing need for sophisticated cybersecurity solutions also act as significant drivers, creating a fertile ground for AI adoption.

Barriers & Challenges: Despite the promising outlook, the market faces significant challenges. High implementation costs and the need for substantial R&D investments pose a barrier for some nations. Stringent regulatory frameworks and ethical concerns surrounding autonomous weapon systems require careful navigation. Interoperability issues between legacy systems and new AI technologies, coupled with data security and privacy concerns, present complex hurdles. Supply chain vulnerabilities for specialized AI hardware and the scarcity of skilled AI talent in the defense sector further restrain growth. Quantifiable impacts of these challenges can result in project delays of up to 18 months and an estimated 10-15% increase in project costs.

Emerging Opportunities in Europe AI in Defense AI Market

Emerging opportunities lie in the development of AI-powered explainable AI (XAI) for defense applications, fostering trust and transparency in decision-making processes. The untapped potential of AI in predictive maintenance for military equipment, significantly reducing downtime and operational costs, presents a lucrative avenue. There is also a growing demand for AI solutions that enhance soldier training and simulation, providing realistic and adaptive learning environments. Furthermore, the increasing focus on autonomous logistics and resupply operations, particularly in remote or contested areas, offers significant growth potential. Collaboration between defense entities and AI startups is expected to unlock novel applications and accelerate innovation.

Growth Accelerators in the Europe AI in Defense AI Market Industry

Catalysts driving long-term growth include breakthroughs in AI algorithms for complex threat analysis and prediction, enabling proactive defense strategies. Strategic partnerships between established defense prime contractors and leading AI technology providers are accelerating the integration of advanced capabilities into existing and future defense systems. Market expansion strategies, driven by European Union defense initiatives aimed at fostering common procurement and interoperability, are also significant growth accelerators. The continuous drive for autonomous systems across land, air, and naval domains, supported by sustained government funding and a commitment to technological sovereignty, will further propel the industry forward.

Key Players Shaping the Europe AI in Defense AI Market Market

- Atos

- General Dynamics Corporation

- Lockheed Martin Corporation

- IBM Corporation

- Leidos

- Thales Group

- BAE Systems PLC

- Airbus S

- Raytheon Technologies Corporation

Notable Milestones in Europe AI in Defense AI Market Sector

- Jul 2022: The Defense Ministry of France announced authorization for the final phase of a new AI and big data processing capability developed by Athea (Thales and Atos joint venture) for secure, sovereign data analysis.

- May 2022: Palantir Technologies Inc. secured a USD 12.5 million contract with the UK Defense Ministry to support its Foundry platform, enabling cost reduction through work automation and faster data processing.

In-Depth Europe AI in Defense AI Market Market Outlook

The Europe AI in Defense market is set for a future characterized by pervasive AI integration across all defense domains. Growth accelerators, including breakthroughs in AI-driven predictive analytics for threat assessment and the strategic expansion of autonomous systems, will redefine military capabilities. Sustained government investment and collaborative R&D initiatives, particularly those fostering European technological sovereignty, will continue to fuel innovation. The increasing adoption of AI in cybersecurity and intelligence gathering, alongside the development of more sophisticated unmanned platforms, promises to enhance operational effectiveness and strategic advantage. This forward trajectory indicates a robust future market potential, with significant opportunities for companies leading in AI development and integration within the defense sector.

Europe AI in Defense AI Market Segmentation

-

1. Component

- 1.1. Hardware

- 1.2. Software

-

2. Platform

- 2.1. Land

- 2.2. Air

- 2.3. Naval

-

3. Application

- 3.1. Cybersecurity

- 3.2. Battlefield Healthcare

- 3.3. Warfare Platform

Europe AI in Defense AI Market Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

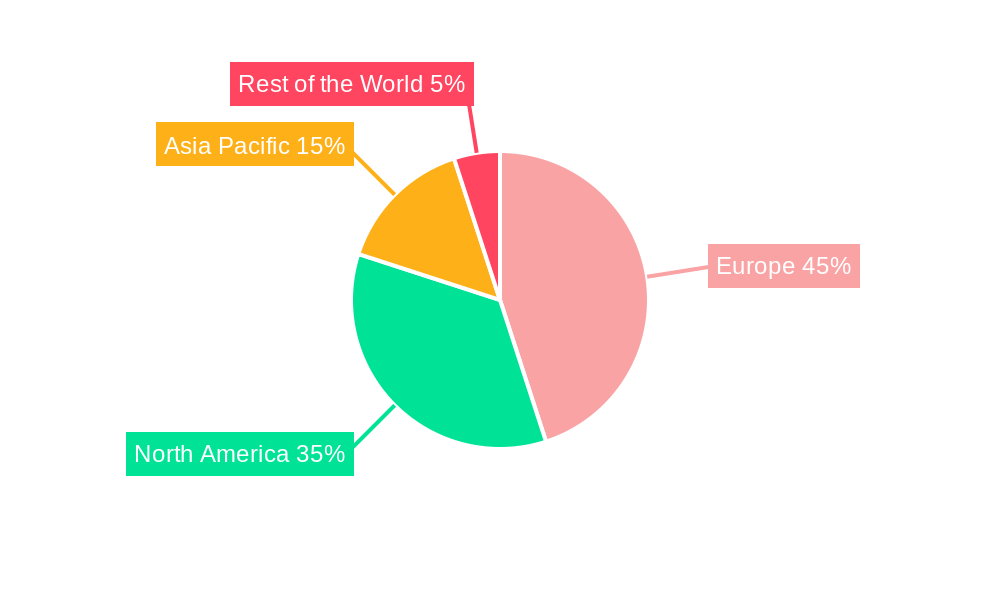

Europe AI in Defense AI Market Regional Market Share

Geographic Coverage of Europe AI in Defense AI Market

Europe AI in Defense AI Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 16% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Component

- 5.1.1. Hardware

- 5.1.2. Software

- 5.2. Market Analysis, Insights and Forecast - by Platform

- 5.2.1. Land

- 5.2.2. Air

- 5.2.3. Naval

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Cybersecurity

- 5.3.2. Battlefield Healthcare

- 5.3.3. Warfare Platform

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Component

- 6. Europe AI in Defense AI Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Component

- 6.1.1. Hardware

- 6.1.2. Software

- 6.2. Market Analysis, Insights and Forecast - by Platform

- 6.2.1. Land

- 6.2.2. Air

- 6.2.3. Naval

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Cybersecurity

- 6.3.2. Battlefield Healthcare

- 6.3.3. Warfare Platform

- 6.1. Market Analysis, Insights and Forecast - by Component

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Atos

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 General Dynamics Corporation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Lockheed Martin Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 IBM Corporation

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Leidos

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Thales Group

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 BAE Systems PLC

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Airbus S

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Raytheon technologies Corporation

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 Atos

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe AI in Defense AI Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Europe AI in Defense AI Market Share (%) by Company 2025

List of Tables

- Table 1: Europe AI in Defense AI Market Revenue billion Forecast, by Component 2020 & 2033

- Table 2: Europe AI in Defense AI Market Revenue billion Forecast, by Platform 2020 & 2033

- Table 3: Europe AI in Defense AI Market Revenue billion Forecast, by Application 2020 & 2033

- Table 4: Europe AI in Defense AI Market Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Europe AI in Defense AI Market Revenue billion Forecast, by Component 2020 & 2033

- Table 6: Europe AI in Defense AI Market Revenue billion Forecast, by Platform 2020 & 2033

- Table 7: Europe AI in Defense AI Market Revenue billion Forecast, by Application 2020 & 2033

- Table 8: Europe AI in Defense AI Market Revenue billion Forecast, by Country 2020 & 2033

- Table 9: United Kingdom Europe AI in Defense AI Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Germany Europe AI in Defense AI Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: France Europe AI in Defense AI Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Italy Europe AI in Defense AI Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Spain Europe AI in Defense AI Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Netherlands Europe AI in Defense AI Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Belgium Europe AI in Defense AI Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Sweden Europe AI in Defense AI Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Norway Europe AI in Defense AI Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Poland Europe AI in Defense AI Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Denmark Europe AI in Defense AI Market Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe AI in Defense AI Market?

The projected CAGR is approximately 16%.

2. Which companies are prominent players in the Europe AI in Defense AI Market?

Key companies in the market include Atos, General Dynamics Corporation, Lockheed Martin Corporation, IBM Corporation, Leidos, Thales Group, BAE Systems PLC, Airbus S, Raytheon technologies Corporation.

3. What are the main segments of the Europe AI in Defense AI Market?

The market segments include Component, Platform, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.28 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Increasing Investments In Artificial Intelligence Will Drive The Market During The Forecast Period.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

Jul 2022: The Defense Ministry of France announced that it had authorized the go-ahead for the final phase of new artificial intelligence and big data processing capability, which is being developed by the company Athea, a joint venture between Thales and Atos. The main aim of such a project will be to provide France with secure and sovereign artificial intelligence and big data platforms that can analyze massive data generated by military equipment as well as other sensors.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe AI in Defense AI Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe AI in Defense AI Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe AI in Defense AI Market?

To stay informed about further developments, trends, and reports in the Europe AI in Defense AI Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence