Key Insights

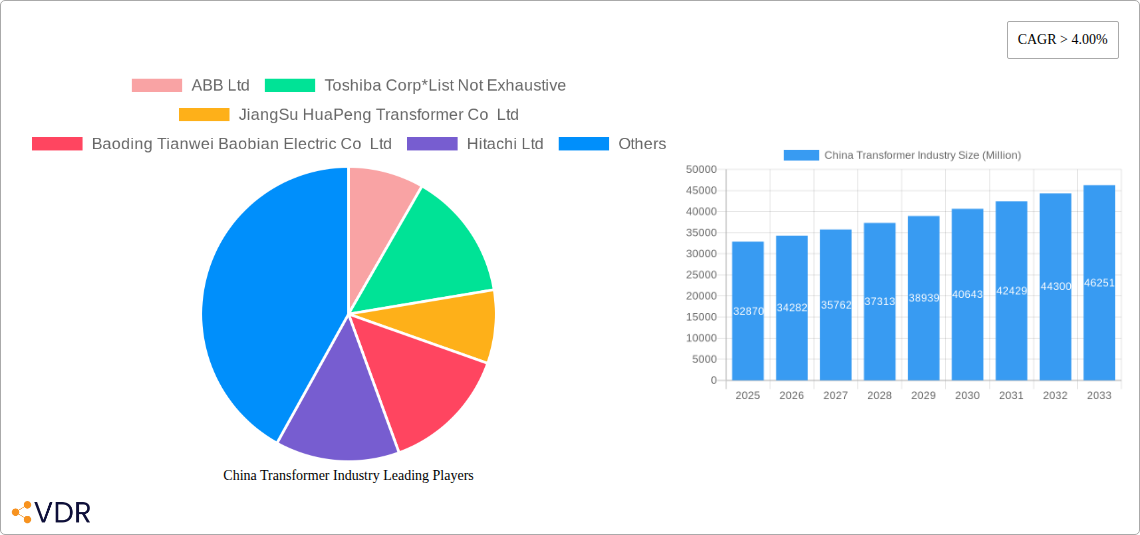

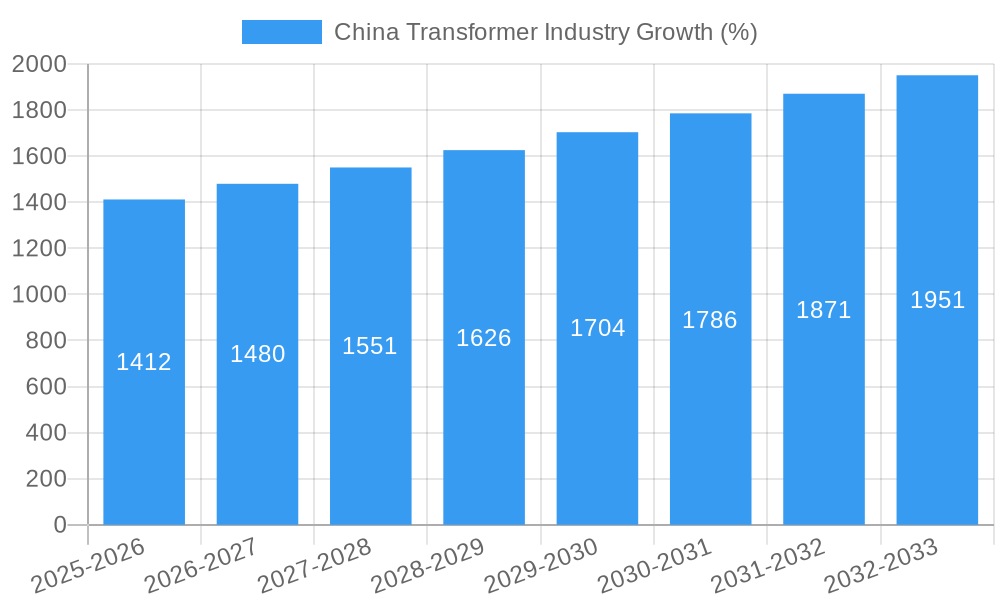

The China transformer industry, valued at $32.87 billion in 2025, is experiencing robust growth, projected to expand at a compound annual growth rate (CAGR) exceeding 4% from 2025 to 2033. This growth is fueled by several key factors. Firstly, China's ongoing investments in infrastructure development, particularly its ambitious power grid modernization programs and expansion of renewable energy sources, are driving significant demand for transformers. The increasing integration of smart grids and the growing adoption of high-voltage direct current (HVDC) transmission technologies further contribute to market expansion. Secondly, the sustained economic growth within China, coupled with rising industrialization and urbanization, necessitates the continuous upgrading and expansion of power transmission and distribution infrastructure. This creates a substantial market for power and distribution transformers across various power ratings (small, medium, and large) and cooling types (air-cooled and oil-cooled). Finally, government initiatives promoting energy efficiency and the adoption of advanced transformer technologies are contributing to market dynamism. Competition among established players like ABB, Toshiba, Hitachi, Siemens, and Schneider Electric, alongside domestic manufacturers like Jiangsu HuaPeng and Baoding Tianwei, is intense, leading to innovation and price competitiveness.

However, certain challenges persist. The industry faces potential headwinds from fluctuating raw material prices, especially for copper and steel, which directly impact production costs. Furthermore, stringent environmental regulations regarding the use of environmentally damaging insulating oils and the disposal of old transformers are pushing manufacturers towards adopting eco-friendly alternatives, which can initially raise production costs. Despite these hurdles, the long-term outlook for the China transformer market remains positive, driven by the country's unwavering commitment to infrastructure development and energy security. The segment breakdown (power rating, cooling type, and transformer type) presents opportunities for specialized manufacturers to cater to niche market segments and gain a competitive edge. Continued technological advancements, particularly in the development of energy-efficient and smart transformers, will further shape the industry's trajectory in the coming years.

China Transformer Industry: Market Report 2019-2033

This comprehensive report provides an in-depth analysis of the China transformer industry, encompassing market dynamics, growth trends, key players, and future outlook. The study period covers 2019-2033, with 2025 as the base and estimated year. This report is crucial for industry professionals, investors, and anyone seeking a detailed understanding of this vital sector within the broader Chinese power and energy infrastructure market. The report segments the market by power rating (small, medium, large), cooling type (air-cooled, oil-cooled), and transformer type (power transformer, distribution transformer).

China Transformer Industry Market Dynamics & Structure

The China transformer industry exhibits a moderately concentrated market structure, with both domestic and international players vying for market share. Technological innovation, particularly in areas like on-load tap changers and sustainable technologies (e.g., EconiQ™ transformers), is a key driver. Stringent regulatory frameworks governing safety and efficiency standards significantly impact the market. Competitive pressures from substitute technologies (e.g., advanced power electronics) are increasing. The end-user demographics are diverse, including the power grid operators (e.g., State Grid Corporation of China), industrial consumers, and renewable energy projects. The M&A landscape has seen a moderate level of activity, mostly focused on strategic acquisitions enhancing technological capabilities and market reach.

- Market Concentration: xx% market share held by top 5 players (2024).

- Technological Innovation: Focus on improving efficiency, reliability, and sustainability.

- Regulatory Framework: Stringent standards for safety and performance are in place.

- Competitive Substitutes: Growing competition from alternative power technologies.

- End-User Demographics: Power grid operators, industrial facilities, and renewable energy projects.

- M&A Trends: Moderate activity, driven by strategic acquisitions and technological integration. xx M&A deals in the past 5 years (2019-2024).

China Transformer Industry Growth Trends & Insights

The China transformer market experienced robust growth during the historical period (2019-2024), driven by sustained investments in power grid infrastructure, rapid industrialization, and the expansion of renewable energy capacity. The market size is projected to reach xx million units by 2025, exhibiting a CAGR of xx% during the forecast period (2025-2033). This growth is fueled by government policies promoting the modernization of power grids, urbanization, and increasing electricity consumption. Technological advancements, such as the adoption of smart grid technologies and the use of more efficient and environmentally friendly transformer designs, are contributing to higher adoption rates. Consumer behavior is shifting towards greater demand for higher-efficiency and more reliable transformers.

Dominant Regions, Countries, or Segments in China Transformer Industry

The eastern coastal regions of China, including Jiangsu, Guangdong, and Zhejiang provinces, dominate the transformer market. This dominance is largely due to their high concentration of industrial activities, robust power grid infrastructure, and proximity to major manufacturing hubs. The large power transformer segment is experiencing faster growth compared to the small and medium segments due to large-scale power grid expansion projects. Similarly, the oil-cooled transformers segment holds a larger market share due to its higher efficiency and reliability compared to air-cooled transformers.

- Key Drivers: Robust economic growth, significant infrastructure development, increasing electricity demand, and government policies supportive of grid modernization.

- Dominance Factors: High concentration of industrial activities, well-established power infrastructure, and strategic location.

- Growth Potential: Continuous expansion of renewable energy projects, advancements in smart grids, and sustained economic development will further drive growth in these regions and segments.

China Transformer Industry Product Landscape

The China transformer industry offers a diverse range of products catering to various power requirements and applications. Recent innovations focus on enhanced efficiency, reduced environmental impact, and improved reliability. Key features include advanced cooling systems, digital monitoring capabilities, and compact designs. Unique selling propositions are often focused on customization to meet specific project requirements, efficient designs that reduce energy losses, and increased service life to reduce maintenance costs.

Key Drivers, Barriers & Challenges in China Transformer Industry

Key Drivers:

- Government Investments: Significant investments in power grid infrastructure upgrades.

- Economic Growth: Rapid economic growth fueling increased electricity demand.

- Renewable Energy Expansion: Expansion of renewable energy projects necessitates increased transformer capacity.

Key Challenges:

- Supply Chain Disruptions: Global supply chain uncertainties and material cost fluctuations.

- Regulatory Hurdles: Complex regulatory processes can delay project implementation.

- Competitive Pressure: Intense competition from both domestic and international manufacturers. This has resulted in a xx% decrease in average profit margins in the past 2 years (2023-2024).

Emerging Opportunities in China Transformer Industry

- Smart Grid Technologies: Integration of smart grid functionalities into transformers.

- Renewable Energy Integration: Demand for transformers designed for integration with renewable energy sources.

- High-Voltage Direct Current (HVDC) Transmission: Growth in HVDC transmission projects requires specialized transformers.

Growth Accelerators in the China Transformer Industry

Technological breakthroughs in transformer design and manufacturing, coupled with strategic partnerships between domestic and international companies, are accelerating market growth. Expansion into new markets, particularly in the western regions of China, where infrastructure development is ongoing, presents significant opportunities.

Key Players Shaping the China Transformer Industry Market

- ABB Ltd

- Toshiba Corp

- Jiangsu HuaPeng Transformer Co Ltd

- Baoding Tianwei Baobian Electric Co Ltd

- Hitachi Ltd

- Mitsubishi Electric Corporation

- Siemens AG

- Schneider Electric SE

- General Electric Company

- Panasonic Corporation

Notable Milestones in China Transformer Industry Sector

- November 2022: Successful installation of the first domestically produced converter transformer with on-load tap changers in a major west-to-east power transmission project in Guangdong Province. This signifies a breakthrough in high-end electric equipment technology.

- March 2022: The State Grid Corporation of China (SGCC) ordered two 110 kV, 63 MVA EconiQ™ power transformers from Hitachi Energy for a sustainable substation project in Jiangsu Province.

In-Depth China Transformer Industry Market Outlook

The future of the China transformer industry looks promising, with continued growth driven by ongoing investments in infrastructure, the increasing adoption of renewable energy, and technological advancements. Strategic partnerships and technological innovation will play a crucial role in shaping the market landscape, offering significant opportunities for both domestic and international players. The focus on sustainability and smart grid technologies will further drive market expansion and product innovation in the coming years.

China Transformer Industry Segmentation

-

1. Power Rating

- 1.1. Small

- 1.2. Large

- 1.3. Medium

-

2. Cooling Type

- 2.1. Air-Cooled

- 2.2. Oil-Cooled

-

3. Transformer Type

- 3.1. Power Transformer

- 3.2. Distribution Transformer

China Transformer Industry Segmentation By Geography

- 1. China

China Transformer Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 4.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Increasing Natural Gas Demand4.; Rising Pipeline Network and Associated Infrastructure Development

- 3.3. Market Restrains

- 3.3.1. 4.; Rising Shift toward Renewable Energy

- 3.4. Market Trends

- 3.4.1. Distribution Transformer Expected to Dominate the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. China Transformer Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Power Rating

- 5.1.1. Small

- 5.1.2. Large

- 5.1.3. Medium

- 5.2. Market Analysis, Insights and Forecast - by Cooling Type

- 5.2.1. Air-Cooled

- 5.2.2. Oil-Cooled

- 5.3. Market Analysis, Insights and Forecast - by Transformer Type

- 5.3.1. Power Transformer

- 5.3.2. Distribution Transformer

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. China

- 5.1. Market Analysis, Insights and Forecast - by Power Rating

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 ABB Ltd

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Toshiba Corp*List Not Exhaustive

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 JiangSu HuaPeng Transformer Co Ltd

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Baoding Tianwei Baobian Electric Co Ltd

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Hitachi Ltd

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Mitsubishi Electric Corporation

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Siemens AG

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Schneider Electric SE

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 General Electric Company

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Panasonic Corporation

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 ABB Ltd

List of Figures

- Figure 1: China Transformer Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: China Transformer Industry Share (%) by Company 2024

List of Tables

- Table 1: China Transformer Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: China Transformer Industry Revenue Million Forecast, by Power Rating 2019 & 2032

- Table 3: China Transformer Industry Revenue Million Forecast, by Cooling Type 2019 & 2032

- Table 4: China Transformer Industry Revenue Million Forecast, by Transformer Type 2019 & 2032

- Table 5: China Transformer Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: China Transformer Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: China Transformer Industry Revenue Million Forecast, by Power Rating 2019 & 2032

- Table 8: China Transformer Industry Revenue Million Forecast, by Cooling Type 2019 & 2032

- Table 9: China Transformer Industry Revenue Million Forecast, by Transformer Type 2019 & 2032

- Table 10: China Transformer Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Transformer Industry?

The projected CAGR is approximately > 4.00%.

2. Which companies are prominent players in the China Transformer Industry?

Key companies in the market include ABB Ltd, Toshiba Corp*List Not Exhaustive, JiangSu HuaPeng Transformer Co Ltd, Baoding Tianwei Baobian Electric Co Ltd, Hitachi Ltd, Mitsubishi Electric Corporation, Siemens AG, Schneider Electric SE, General Electric Company, Panasonic Corporation.

3. What are the main segments of the China Transformer Industry?

The market segments include Power Rating, Cooling Type, Transformer Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 32.87 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Natural Gas Demand4.; Rising Pipeline Network and Associated Infrastructure Development.

6. What are the notable trends driving market growth?

Distribution Transformer Expected to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Rising Shift toward Renewable Energy.

8. Can you provide examples of recent developments in the market?

November 2022: An major west-to-east power transmission project in Guangdong Province, South China, successfully installed the first convertor transformer using on-load tap changers built in China. This signifies that China has successfully overcome the limitations imposed by this key technology in high-end electric equipment.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Transformer Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Transformer Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Transformer Industry?

To stay informed about further developments, trends, and reports in the China Transformer Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence