Key Insights

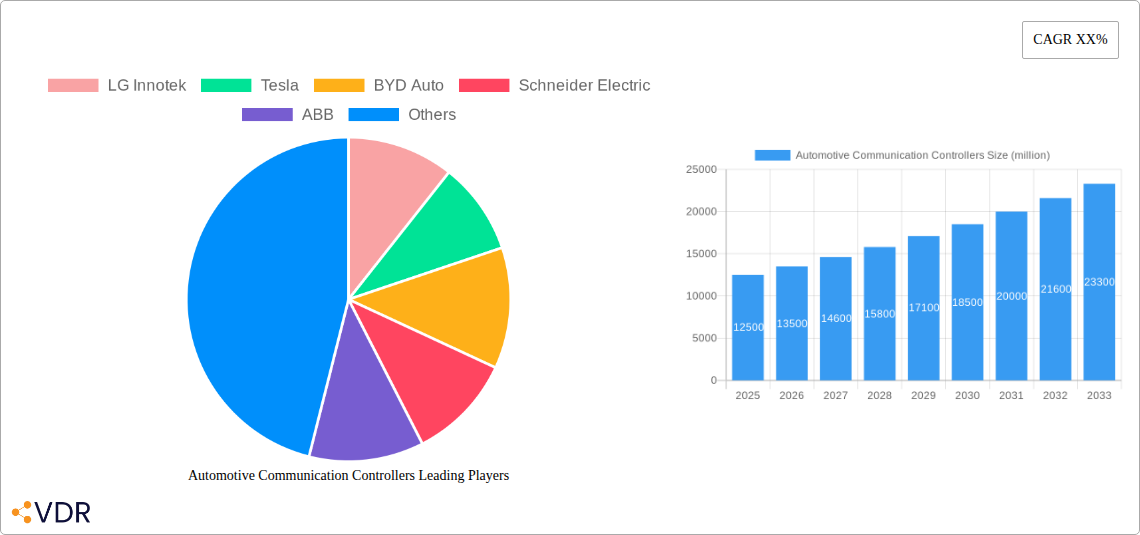

The global Automotive Communication Controllers market is poised for robust expansion, projected to reach a significant market size of approximately USD 12,500 million by 2025, with an estimated Compound Annual Growth Rate (CAGR) of around 8.5% during the forecast period of 2025-2033. This growth is primarily fueled by the increasing complexity and connectivity of modern vehicles, driven by the rapid adoption of advanced driver-assistance systems (ADAS), autonomous driving technologies, and in-car infotainment systems. The escalating demand for enhanced vehicle safety features, seamless data exchange between vehicle components and external networks, and the growing trend towards connected car services are key market accelerators. Furthermore, stringent automotive safety regulations and the continuous pursuit of improved fuel efficiency through sophisticated electronic control units (ECUs) are also contributing to the sustained demand for these critical communication components.

The market is segmented by application into Passenger Vehicles and Commercial Vehicles, with the former likely holding a dominant share due to higher production volumes and the increasing integration of advanced communication features in consumer cars. By type, CAN Bus continues to be a foundational technology, but newer, high-bandwidth protocols like Ethernet AVB (Audio Video Bridging) are gaining traction, especially for complex data-intensive applications such as sensor fusion and high-definition infotainment. Emerging trends also include the development of more efficient and secure communication solutions to support the evolving automotive landscape. Key players like Renesas Electronics, NXP, and Infineon are at the forefront of innovation, developing next-generation controllers that are more powerful, energy-efficient, and capable of handling the increasing data traffic within vehicles. However, challenges such as the high cost of advanced communication technologies and the need for robust cybersecurity measures could temper growth in certain segments.

This in-depth report provides a panoramic view of the global Automotive Communication Controllers market, meticulously analyzing its dynamics, growth trajectories, and future potential. Covering the historical period from 2019-2024 and extending through the forecast period of 2025-2033, with a base year of 2025, this research is an indispensable tool for stakeholders seeking to navigate the complexities of this rapidly evolving industry. Our analysis integrates high-traffic SEO keywords to ensure maximum visibility and engagement from automotive manufacturers, Tier-1 suppliers, semiconductor companies, and technology providers.

Automotive Communication Controllers Market Dynamics & Structure

The global Automotive Communication Controllers market is characterized by a moderate to high concentration, with a few dominant players holding significant market share. Technological innovation is the primary driver, fueled by the increasing demand for advanced driver-assistance systems (ADAS), in-vehicle infotainment (IVI), and autonomous driving capabilities. Regulatory frameworks, particularly concerning vehicle safety and emissions, are also playing a crucial role in shaping product development and adoption. Competitive product substitutes are emerging, especially with the rise of integrated domain controllers and software-defined architectures that can consolidate multiple communication functions. End-user demographics are shifting towards a greater demand for connected and intelligent vehicles, with younger demographics showing a higher propensity to adopt advanced automotive technologies. Mergers and acquisition (M&A) trends are prevalent as companies seek to expand their product portfolios, gain access to new technologies, and consolidate their market positions. For instance, recent M&A activities indicate a strategic push towards acquiring expertise in high-speed networking and cybersecurity solutions for automotive applications. Innovation barriers include the stringent validation processes for automotive-grade components and the long product development cycles inherent in the automotive industry. The market is projected to witness a notable increase in the adoption of Ethernet AVB, displacing some traditional protocols in high-bandwidth applications.

- Market Concentration: Moderately concentrated with key players focusing on specialized segments.

- Technological Innovation Drivers: ADAS, IVI, autonomous driving, cybersecurity, V2X communication.

- Regulatory Frameworks: ECE R157 (Automated Lane Keeping System), ISO 26262 (Functional Safety).

- Competitive Product Substitutes: Integrated domain controllers, software-defined vehicles, centralized computing architectures.

- End-User Demographics: Growing demand for connected, personalized, and automated driving experiences.

- M&A Trends: Acquisitions focused on semiconductor IP, software platforms, and connectivity solutions.

- Innovation Barriers: Long validation cycles, high development costs, cybersecurity concerns.

Automotive Communication Controllers Growth Trends & Insights

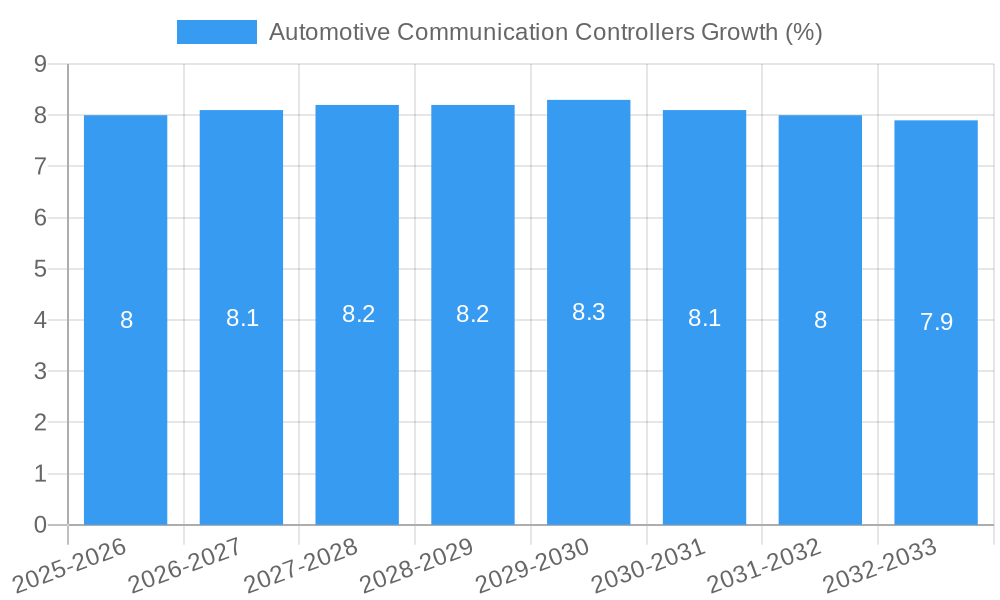

The global Automotive Communication Controllers market is poised for robust growth, driven by the relentless digital transformation within the automotive sector. The market size is expected to witness a Compound Annual Growth Rate (CAGR) of approximately 8.5% during the forecast period (2025-2033). This expansion is underpinned by the escalating adoption rates of sophisticated in-car electronics and connectivity features across passenger and commercial vehicle segments. Technological disruptions, such as the proliferation of AI in automotive applications and the advent of 5G connectivity, are creating new avenues for communication controller functionalities, including enhanced V2X (Vehicle-to-Everything) communication and real-time data processing. Consumer behavior shifts are evident, with a growing preference for seamless integration of personal devices with vehicle systems, sophisticated infotainment options, and advanced safety features. This demand translates directly into a higher need for efficient and high-performance communication controllers capable of handling increased data bandwidth and complex communication protocols. The penetration of advanced communication technologies like Automotive Ethernet is rapidly increasing, especially in premium and electric vehicles, as it offers superior bandwidth and determinism compared to traditional CAN and LIN buses. The integration of AI and machine learning for predictive maintenance and driver behavior analysis further necessitates advanced communication infrastructure. The global market for automotive communication controllers is projected to reach xx million units by 2033, up from xx million units in 2025. The increasing complexity of vehicle architectures, with the introduction of zonal architectures and domain controllers, is also a significant growth catalyst, driving the demand for versatile and powerful communication solutions.

Dominant Regions, Countries, or Segments in Automotive Communication Controllers

The Passenger Vehicle segment is the undisputed leader in the Automotive Communication Controllers market, driven by the insatiable consumer demand for advanced infotainment, connectivity, and ADAS features. This segment's dominance is further amplified by the sheer volume of passenger cars produced globally and the increasing trend towards premiumization, where cutting-edge communication technologies are a key differentiator. The economic policies in major automotive manufacturing hubs, coupled with significant investments in R&D for smart and connected mobility solutions, are pivotal in this segment's growth.

- Dominant Application Segment: Passenger Vehicles (estimated xx million units in 2025)

- High demand for ADAS, IVI, and V2X technologies.

- Increasing integration of digital cockpits and personalized user experiences.

- Rapid adoption in emerging economies as vehicle electrification accelerates.

- Significant investment in in-car connectivity solutions by OEMs.

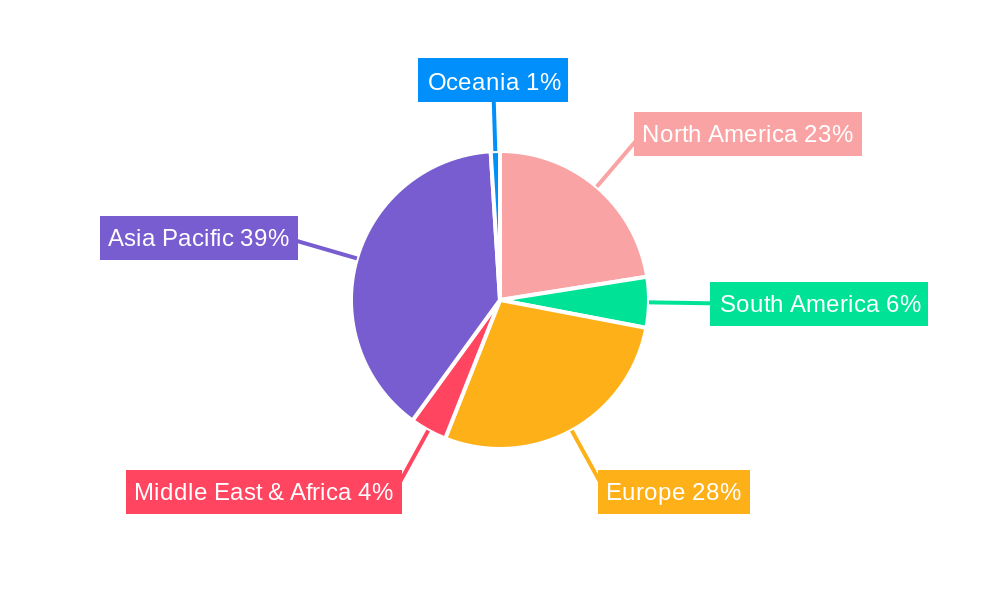

Asia-Pacific stands out as the dominant region, propelled by its status as the world's largest automotive market and a burgeoning manufacturing hub. The region's leadership is fortified by substantial government initiatives promoting automotive innovation, smart cities, and the adoption of electric and autonomous vehicles. Countries like China, Japan, and South Korea are at the forefront of this growth, with leading automotive manufacturers and semiconductor suppliers actively investing in next-generation communication technologies. The rapid expansion of the middle class in these countries further fuels the demand for feature-rich and connected passenger vehicles.

- Dominant Region: Asia-Pacific

- Largest automotive production and sales volume globally.

- Strong government support for EV adoption and intelligent transportation systems.

- Presence of major automotive OEMs and semiconductor manufacturers.

- Rapidly growing consumer appetite for advanced automotive features.

Within the types of communication controllers, Automotive Ethernet (including Ethernet AVB) is emerging as a rapidly growing segment, poised to capture significant market share from traditional protocols. Its high bandwidth, determinism, and scalability make it ideal for the increasing data demands of ADAS, autonomous driving, and complex infotainment systems. While CAN Bus remains foundational, Ethernet is increasingly being adopted for backbone communication and high-speed data transfer within the vehicle.

- Emerging Dominant Type: Ethernet AVB (Audio Video Bridging)

- Superior bandwidth for high-definition data streams (cameras, sensors).

- Improved latency and determinism for real-time applications.

- Scalability for future autonomous driving and V2X integration.

- Cost-effectiveness and simplified wiring compared to older high-speed networks.

Automotive Communication Controllers Product Landscape

The product landscape of Automotive Communication Controllers is marked by continuous innovation, focusing on higher integration, increased processing power, and enhanced safety features. Leading companies are developing intelligent controllers that not only manage in-vehicle networks but also contribute to advanced functions like sensor fusion, AI processing, and cybersecurity. Key advancements include the integration of multiple communication protocols onto a single chip, support for high-speed serial communication like Automotive Ethernet, and the implementation of robust functional safety (FuSa) features compliant with ISO 26262 standards. Products are increasingly designed with a focus on software-defined capabilities, enabling over-the-air updates and flexible functionality configurations. Unique selling propositions often revolve around power efficiency, compact form factors, and advanced diagnostic capabilities, catering to the stringent requirements of the automotive industry.

Key Drivers, Barriers & Challenges in Automotive Communication Controllers

The Automotive Communication Controllers market is propelled by several key drivers, primarily the accelerating adoption of advanced driver-assistance systems (ADAS), the growing demand for sophisticated in-vehicle infotainment (IVI) systems, and the inevitable march towards autonomous driving. The increasing connectivity of vehicles, including V2X communication, further necessitates robust and high-performance controllers. Regulatory mandates for enhanced vehicle safety and cybersecurity also play a significant role in driving innovation and adoption.

- Key Drivers:

- Rapid growth in ADAS features (e.g., adaptive cruise control, lane keeping assist).

- Escalating demand for seamless in-car connectivity and advanced infotainment.

- Development and deployment of autonomous driving technologies.

- Increasing implementation of V2X communication for enhanced safety and traffic management.

- Stricter automotive safety and cybersecurity regulations.

Conversely, the market faces several barriers and challenges. Supply chain disruptions, particularly for critical semiconductor components, can impact production volumes and lead times. The complexity and cost associated with developing and validating automotive-grade communication controllers, along with the long development cycles of vehicle platforms, present significant hurdles. Fierce competition among established players and emerging technology providers also puts pressure on pricing and margins. Furthermore, ensuring robust cybersecurity against evolving threats remains a paramount challenge.

- Key Barriers & Challenges:

- Global semiconductor shortages and supply chain volatility.

- High research and development costs and lengthy validation cycles.

- Intense competitive landscape and price pressures.

- Ensuring robust cybersecurity across complex vehicle networks.

- Evolving standardization and interoperability challenges across different protocols.

Emerging Opportunities in Automotive Communication Controllers

Emerging opportunities lie in the integration of communication controllers with artificial intelligence (AI) and machine learning (ML) capabilities, enabling advanced data processing and decision-making within the vehicle. The expansion of V2X communication, particularly vehicle-to-infrastructure (V2I) and vehicle-to-network (V2N), presents a significant opportunity for controllers capable of real-time data exchange and traffic management optimization. The growing demand for electric vehicles (EVs) also opens avenues for specialized controllers that manage battery communication, charging infrastructure connectivity, and thermal management systems. Furthermore, the trend towards software-defined vehicles creates opportunities for modular and updateable communication architectures.

- Untapped Markets: Low-cost segments in emerging economies adopting basic connected features.

- Innovative Applications: Real-time vehicle diagnostics, predictive maintenance, and over-the-air software updates for communication modules.

- Evolving Consumer Preferences: Demand for personalized in-cabin experiences and seamless digital integration.

Growth Accelerators in the Automotive Communication Controllers Industry

Growth accelerators for the Automotive Communication Controllers industry are deeply rooted in technological breakthroughs and strategic market expansion. The continuous advancement in semiconductor technology, enabling smaller, more powerful, and more energy-efficient controllers, is a significant catalyst. Strategic partnerships between semiconductor manufacturers and automotive OEMs, focusing on co-development of next-generation platforms, are accelerating product integration and market adoption. Furthermore, the increasing global push towards vehicle electrification and autonomous driving mandates will continue to drive demand for sophisticated communication solutions, acting as a powerful market expansion strategy. The development of open standards and collaborative ecosystems also fosters faster innovation and broader market reach.

Key Players Shaping the Automotive Communication Controllers Market

- LG Innotek

- Tesla

- BYD Auto

- Schneider Electric

- ABB

- Renesas Electronics

- NXP

- Infineon

- Texas Instruments

- Microchip Technology

- STMicroelectronics

Notable Milestones in Automotive Communication Controllers Sector

- 2019: Introduction of next-generation automotive Ethernet switches with enhanced security features by leading semiconductor vendors.

- 2020: Increased adoption of LIN controllers in low-cost vehicle segments for body control modules and sensors.

- 2021: Major automotive OEMs announce plans for centralized domain controllers, increasing reliance on high-speed communication protocols like Automotive Ethernet.

- 2022: Significant M&A activity focused on companies with expertise in V2X communication chips and software.

- 2023: Launch of advanced FlexRay controllers with improved error detection and fault tolerance capabilities.

- 2024: Growing industry focus on developing unified communication architectures to support software-defined vehicles.

- 2025 (Estimated): Anticipated wider deployment of Ethernet AVB for infotainment and ADAS data aggregation.

- 2026-2033 (Forecast): Continued dominance of Automotive Ethernet, with increasing integration of AI accelerators within communication controllers.

In-Depth Automotive Communication Controllers Market Outlook

The future outlook for the Automotive Communication Controllers market is exceptionally bright, fueled by ongoing technological advancements and evolving mobility trends. Growth accelerators such as the transition to software-defined vehicles, the widespread adoption of electric and autonomous driving technologies, and the increasing demand for advanced in-car connectivity will continue to propel the market forward. Strategic partnerships and continued R&D investment in areas like cybersecurity and AI integration will be crucial for market players to capitalize on emerging opportunities. The market is poised for sustained expansion, offering significant potential for innovation and business growth in the coming years.

Automotive Communication Controllers Segmentation

-

1. Application

- 1.1. Passager Vehicle

- 1.2. Commercial Vehicle

-

2. Types

- 2.1. CAN Bus

- 2.2. LIN (Local Interconnect Network)

- 2.3. FlexRay

- 2.4. MOST (Media Oriented Systems Transport)

- 2.5. Ethernet AVB (Audio Video Bridging)

- 2.6. Others

Automotive Communication Controllers Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Automotive Communication Controllers REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Automotive Communication Controllers Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Passager Vehicle

- 5.1.2. Commercial Vehicle

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. CAN Bus

- 5.2.2. LIN (Local Interconnect Network)

- 5.2.3. FlexRay

- 5.2.4. MOST (Media Oriented Systems Transport)

- 5.2.5. Ethernet AVB (Audio Video Bridging)

- 5.2.6. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Automotive Communication Controllers Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Passager Vehicle

- 6.1.2. Commercial Vehicle

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. CAN Bus

- 6.2.2. LIN (Local Interconnect Network)

- 6.2.3. FlexRay

- 6.2.4. MOST (Media Oriented Systems Transport)

- 6.2.5. Ethernet AVB (Audio Video Bridging)

- 6.2.6. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Automotive Communication Controllers Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Passager Vehicle

- 7.1.2. Commercial Vehicle

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. CAN Bus

- 7.2.2. LIN (Local Interconnect Network)

- 7.2.3. FlexRay

- 7.2.4. MOST (Media Oriented Systems Transport)

- 7.2.5. Ethernet AVB (Audio Video Bridging)

- 7.2.6. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Automotive Communication Controllers Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Passager Vehicle

- 8.1.2. Commercial Vehicle

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. CAN Bus

- 8.2.2. LIN (Local Interconnect Network)

- 8.2.3. FlexRay

- 8.2.4. MOST (Media Oriented Systems Transport)

- 8.2.5. Ethernet AVB (Audio Video Bridging)

- 8.2.6. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Automotive Communication Controllers Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Passager Vehicle

- 9.1.2. Commercial Vehicle

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. CAN Bus

- 9.2.2. LIN (Local Interconnect Network)

- 9.2.3. FlexRay

- 9.2.4. MOST (Media Oriented Systems Transport)

- 9.2.5. Ethernet AVB (Audio Video Bridging)

- 9.2.6. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Automotive Communication Controllers Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Passager Vehicle

- 10.1.2. Commercial Vehicle

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. CAN Bus

- 10.2.2. LIN (Local Interconnect Network)

- 10.2.3. FlexRay

- 10.2.4. MOST (Media Oriented Systems Transport)

- 10.2.5. Ethernet AVB (Audio Video Bridging)

- 10.2.6. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 LG Innotek

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Tesla

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 BYD Auto

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Schneider Electric

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 ABB

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Renesas Electronics

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 NXP

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Infineon

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Texas Instruments

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Microchip Technology

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 STMicroelectronics

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.1 LG Innotek

List of Figures

- Figure 1: Global Automotive Communication Controllers Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Automotive Communication Controllers Revenue (million), by Application 2024 & 2032

- Figure 3: North America Automotive Communication Controllers Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Automotive Communication Controllers Revenue (million), by Types 2024 & 2032

- Figure 5: North America Automotive Communication Controllers Revenue Share (%), by Types 2024 & 2032

- Figure 6: North America Automotive Communication Controllers Revenue (million), by Country 2024 & 2032

- Figure 7: North America Automotive Communication Controllers Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Automotive Communication Controllers Revenue (million), by Application 2024 & 2032

- Figure 9: South America Automotive Communication Controllers Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Automotive Communication Controllers Revenue (million), by Types 2024 & 2032

- Figure 11: South America Automotive Communication Controllers Revenue Share (%), by Types 2024 & 2032

- Figure 12: South America Automotive Communication Controllers Revenue (million), by Country 2024 & 2032

- Figure 13: South America Automotive Communication Controllers Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Automotive Communication Controllers Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Automotive Communication Controllers Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Automotive Communication Controllers Revenue (million), by Types 2024 & 2032

- Figure 17: Europe Automotive Communication Controllers Revenue Share (%), by Types 2024 & 2032

- Figure 18: Europe Automotive Communication Controllers Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Automotive Communication Controllers Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Automotive Communication Controllers Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Automotive Communication Controllers Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Automotive Communication Controllers Revenue (million), by Types 2024 & 2032

- Figure 23: Middle East & Africa Automotive Communication Controllers Revenue Share (%), by Types 2024 & 2032

- Figure 24: Middle East & Africa Automotive Communication Controllers Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Automotive Communication Controllers Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Automotive Communication Controllers Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Automotive Communication Controllers Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Automotive Communication Controllers Revenue (million), by Types 2024 & 2032

- Figure 29: Asia Pacific Automotive Communication Controllers Revenue Share (%), by Types 2024 & 2032

- Figure 30: Asia Pacific Automotive Communication Controllers Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Automotive Communication Controllers Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Automotive Communication Controllers Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Automotive Communication Controllers Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Automotive Communication Controllers Revenue million Forecast, by Types 2019 & 2032

- Table 4: Global Automotive Communication Controllers Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Automotive Communication Controllers Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Automotive Communication Controllers Revenue million Forecast, by Types 2019 & 2032

- Table 7: Global Automotive Communication Controllers Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Automotive Communication Controllers Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Automotive Communication Controllers Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Automotive Communication Controllers Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Automotive Communication Controllers Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Automotive Communication Controllers Revenue million Forecast, by Types 2019 & 2032

- Table 13: Global Automotive Communication Controllers Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Automotive Communication Controllers Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Automotive Communication Controllers Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Automotive Communication Controllers Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Automotive Communication Controllers Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Automotive Communication Controllers Revenue million Forecast, by Types 2019 & 2032

- Table 19: Global Automotive Communication Controllers Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Automotive Communication Controllers Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Automotive Communication Controllers Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Automotive Communication Controllers Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Automotive Communication Controllers Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Automotive Communication Controllers Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Automotive Communication Controllers Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Automotive Communication Controllers Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Automotive Communication Controllers Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Automotive Communication Controllers Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Automotive Communication Controllers Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Automotive Communication Controllers Revenue million Forecast, by Types 2019 & 2032

- Table 31: Global Automotive Communication Controllers Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Automotive Communication Controllers Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Automotive Communication Controllers Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Automotive Communication Controllers Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Automotive Communication Controllers Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Automotive Communication Controllers Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Automotive Communication Controllers Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Automotive Communication Controllers Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Automotive Communication Controllers Revenue million Forecast, by Types 2019 & 2032

- Table 40: Global Automotive Communication Controllers Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Automotive Communication Controllers Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Automotive Communication Controllers Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Automotive Communication Controllers Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Automotive Communication Controllers Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Automotive Communication Controllers Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Automotive Communication Controllers Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Automotive Communication Controllers Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Communication Controllers?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the Automotive Communication Controllers?

Key companies in the market include LG Innotek, Tesla, BYD Auto, Schneider Electric, ABB, Renesas Electronics, NXP, Infineon, Texas Instruments, Microchip Technology, STMicroelectronics.

3. What are the main segments of the Automotive Communication Controllers?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Communication Controllers," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Communication Controllers report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Communication Controllers?

To stay informed about further developments, trends, and reports in the Automotive Communication Controllers, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence