Key Insights

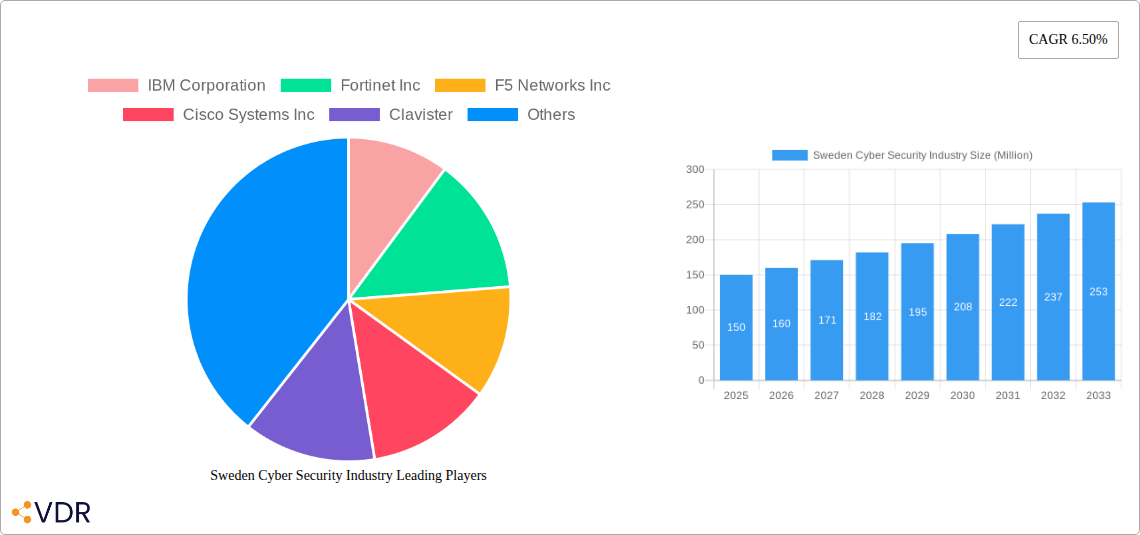

The Swedish cybersecurity market, valued at approximately €150 million in 2025, is projected to experience robust growth, exhibiting a Compound Annual Growth Rate (CAGR) of 6.5% from 2025 to 2033. This expansion is fueled by several key drivers. Increasing digitalization across various sectors, including BFSI (Banking, Financial Services, and Insurance), healthcare, and manufacturing, necessitates enhanced cybersecurity measures to mitigate rising cyber threats. The growing adoption of cloud-based solutions and the increasing prevalence of sophisticated cyberattacks, such as ransomware and data breaches, are further bolstering market demand. Government initiatives promoting cybersecurity awareness and regulations mandating robust security protocols are also contributing to market growth. While the market faces restraints such as a shortage of skilled cybersecurity professionals and the complexity of implementing comprehensive security solutions, the overall growth trajectory remains positive. The market is segmented by offering (solutions and services), deployment (cloud and on-premise), and end-user (BFSI, healthcare, manufacturing, government & defense, IT & telecommunications, and others). Major players like IBM, Fortinet, F5 Networks, Cisco, and others compete in this dynamic landscape, offering a diverse range of solutions to meet the evolving cybersecurity needs of Swedish organizations.

The dominance of cloud-based solutions is expected to continue, driven by their scalability, cost-effectiveness, and ease of management. The BFSI and government & defense sectors are anticipated to be significant contributors to market growth due to their critical reliance on robust cybersecurity infrastructure and their vulnerability to targeted attacks. However, the manufacturing and healthcare sectors are also increasingly investing in cybersecurity solutions to protect sensitive patient data and critical operational technology. The forecast period (2025-2033) will likely witness a shift towards proactive security measures, including advanced threat intelligence, AI-powered security analytics, and robust incident response capabilities. The ongoing need for continuous improvement in cybersecurity strategies, coupled with the escalating sophistication of cyber threats, will ensure sustained growth in the Swedish cybersecurity market throughout the forecast period.

Sweden Cyber Security Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the Sweden cyber security market, offering invaluable insights for industry professionals, investors, and strategic decision-makers. Covering the period from 2019 to 2033, with a focus on 2025, this report segments the market by offering (solutions and services), deployment (cloud and on-premise), and end-user (BFSI, healthcare, manufacturing, government & defense, IT & telecommunication, and others), providing a granular understanding of this dynamic landscape. The report leverages extensive data analysis to forecast market trends and identify key growth opportunities. High-impact keywords include Sweden cybersecurity market, Swedish cyber security solutions, cloud security Sweden, cybersecurity services Sweden, and Swedish cybersecurity industry growth.

Sweden Cyber Security Industry Market Dynamics & Structure

The Swedish cyber security market exhibits a moderately concentrated structure, with both global giants and regional players competing for market share. Market concentration is estimated at xx% in 2025, driven by the presence of established players like IBM, Cisco, and Fortinet. Technological innovation, particularly in AI-powered threat detection and cloud security, is a primary growth driver. Stringent data privacy regulations, such as GDPR, significantly influence market dynamics, fostering demand for compliant solutions. The market also witnesses the emergence of innovative solutions like bug bounty programs (as exemplified by the YesWeHack and Telenor collaboration), further shaping the competitive landscape. Substitutes include legacy security systems, but the increasing sophistication of cyber threats makes advanced solutions increasingly essential. M&A activity remains moderate, with xx deals recorded in the historical period (2019-2024), indicating consolidation among smaller players.

- Market Concentration (2025): xx%

- Key Technological Drivers: AI-powered threat detection, cloud security, blockchain-based security

- Regulatory Influence: GDPR, national cybersecurity strategies

- M&A Activity (2019-2024): xx deals

- Innovation Barriers: High R&D costs, skills shortages

Sweden Cyber Security Industry Growth Trends & Insights

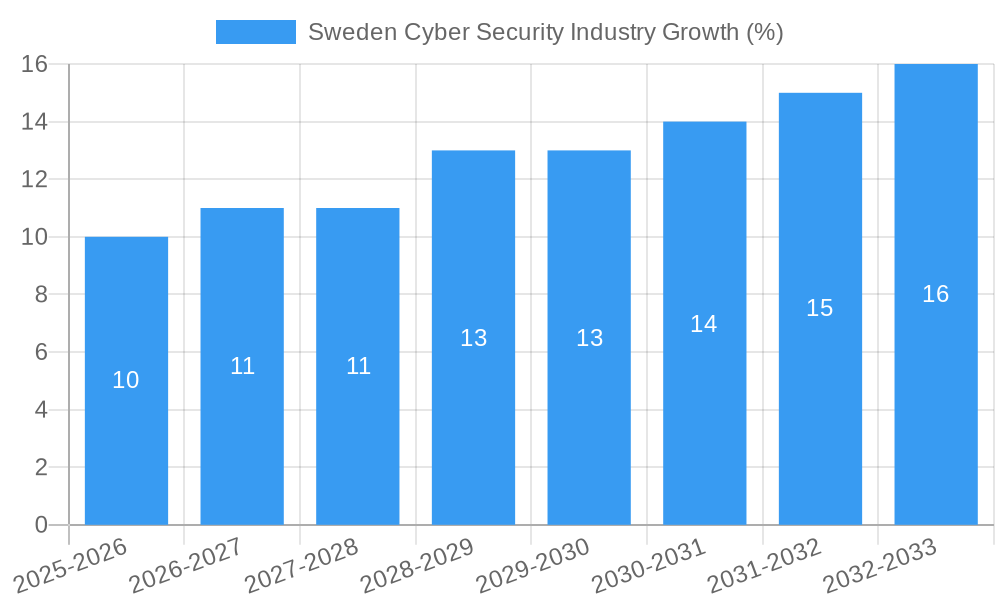

The Swedish cyber security market experienced robust growth during the historical period (2019-2024), driven by increasing digitalization across all sectors and heightened awareness of cyber risks. Market size reached xx Million in 2024, exhibiting a CAGR of xx% during this period. This growth is projected to continue, with the market expected to reach xx Million in 2025 and xx Million by 2033, driven by factors like increasing adoption of cloud computing, expanding IoT deployments, and the rising prevalence of sophisticated cyberattacks. Technological disruptions, including the adoption of AI and automation in security operations, are further accelerating market expansion. Consumer behavior shifts towards greater digital reliance fuel demand for robust cyber security measures. The market penetration of advanced security solutions is expected to rise from xx% in 2024 to xx% by 2033.

Dominant Regions, Countries, or Segments in Sweden Cyber Security Industry

The Swedish cyber security market demonstrates relatively even distribution across its regions. However, urban centers like Stockholm and Gothenburg exhibit higher demand due to concentrated IT infrastructure and a large number of businesses. The "Solutions" segment, encompassing advanced threat detection, data security, and network security solutions, constitutes the largest segment, with a projected market share of xx% in 2025. The cloud deployment model is experiencing rapid growth, driven by the adoption of cloud services across multiple sectors. Government & Defense, along with BFSI, are major end-user segments, driven by stringent regulatory requirements and heightened sensitivity to data breaches.

- Largest Segment (2025): Solutions (xx%)

- Fastest-Growing Segment (2025-2033): Cloud Deployment

- Key End-User Segments: Government & Defense, BFSI

- Geographic Distribution: Relatively balanced; higher concentration in Stockholm and Gothenburg.

Sweden Cyber Security Industry Product Landscape

The Swedish cyber security market showcases a diverse range of products, including advanced threat detection systems leveraging AI and machine learning, cloud-based security solutions, data loss prevention tools, and network security appliances. These products are characterized by advanced features like automated threat response, enhanced visibility, and robust compliance functionalities. Many vendors focus on unique selling propositions such as streamlined integration with existing IT infrastructure and user-friendly interfaces. Technological advancements in areas such as behavioral analytics and cryptographic techniques are driving product innovation.

Key Drivers, Barriers & Challenges in Sweden Cyber Security Industry

Key Drivers: Increasing cyber threats, growing digitalization, stringent data privacy regulations (GDPR), government initiatives promoting cybersecurity.

Challenges: High investment costs for advanced security solutions, skills shortage in cybersecurity professionals (estimated at xx% shortage in 2025), complexity of integrating multiple security tools, and evolving threat landscape demanding continuous updates and adaptations. This leads to an average increase in operational costs by approximately xx% annually for businesses.

Emerging Opportunities in Sweden Cyber Security Industry

Untapped markets exist in smaller businesses and SMEs, which often lack robust security measures. Opportunities also lie in the growing adoption of IoT devices and edge computing requiring specialized security solutions. The integration of security into DevOps processes presents a significant opportunity for vendors specializing in DevSecOps tools and services. Finally, the increased focus on privacy and data protection opens opportunities for privacy-enhancing technologies and data security solutions.

Growth Accelerators in the Sweden Cyber Security Industry

Technological breakthroughs in AI, machine learning, and blockchain significantly accelerate market growth. Strategic partnerships between security vendors and technology providers extend the reach of security solutions. Government initiatives promoting cybersecurity awareness and investments in national cyber infrastructure enhance the market's growth trajectory. Market expansion into new sectors, such as the expanding renewable energy sector, offers significant opportunities.

Key Players Shaping the Sweden Cyber Security Industry Market

- IBM Corporation

- Fortinet Inc

- F5 Networks Inc

- Cisco Systems Inc

- Clavister

- AVG Technologies

- Intel Security (Intel Corporation)

- Dell Technologies Inc

- Capgemini

- IDECSI Enterprise Security

Notable Milestones in Sweden Cyber Security Industry Sector

- May 2022: Cisco released the Cisco Cloud Controls Framework (CCF), a comprehensive security compliance framework.

- March 2022: YesWeHack and Telenor Sweden partnered to enhance the security of Telenor's telecom infrastructure.

In-Depth Sweden Cyber Security Industry Market Outlook

The Swedish cyber security market demonstrates substantial growth potential in the coming years. Continued digital transformation, escalating cyber threats, and evolving regulatory landscapes will fuel demand for advanced security solutions. Strategic investments in R&D, innovative partnerships, and expansion into untapped markets will further contribute to the market's long-term growth trajectory. The focus on proactive security measures and the adoption of AI-driven solutions will be pivotal in shaping the future of the industry.

Sweden Cyber Security Industry Segmentation

-

1. Offering

-

1.1. Solution

- 1.1.1. Application Security

- 1.1.2. Cloud Security

- 1.1.3. Data Security

- 1.1.4. Network Security

- 1.1.5. Other Solutions

- 1.2. Services

-

1.1. Solution

-

2. Deployment

- 2.1. Cloud

- 2.2. On-premise

-

3. End User

- 3.1. BFSI

- 3.2. Healthcare

- 3.3. Manufacturing

- 3.4. Government & Defense

- 3.5. IT and Telecommunication

- 3.6. Other End Users

Sweden Cyber Security Industry Segmentation By Geography

- 1. Sweden

Sweden Cyber Security Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 6.50% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1 Increasing Demand for Digitalization and Scalable IT Infrastructure; Need to tackle risks from various trends such as third-party vendor risks

- 3.2.2 the evolution of MSSPs

- 3.2.3 and adoption of cloud-first strategy

- 3.3. Market Restrains

- 3.3.1. Lack of Cybersecurity Professionals; High Reliance on Traditional Authentication Methods and Low Preparedness

- 3.4. Market Trends

- 3.4.1. Cloud Segment is one of the Factor Driving the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Sweden Cyber Security Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Offering

- 5.1.1. Solution

- 5.1.1.1. Application Security

- 5.1.1.2. Cloud Security

- 5.1.1.3. Data Security

- 5.1.1.4. Network Security

- 5.1.1.5. Other Solutions

- 5.1.2. Services

- 5.1.1. Solution

- 5.2. Market Analysis, Insights and Forecast - by Deployment

- 5.2.1. Cloud

- 5.2.2. On-premise

- 5.3. Market Analysis, Insights and Forecast - by End User

- 5.3.1. BFSI

- 5.3.2. Healthcare

- 5.3.3. Manufacturing

- 5.3.4. Government & Defense

- 5.3.5. IT and Telecommunication

- 5.3.6. Other End Users

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Sweden

- 5.1. Market Analysis, Insights and Forecast - by Offering

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 IBM Corporation

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Fortinet Inc

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 F5 Networks Inc

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Cisco Systems Inc

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Clavister

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 AVG Technologies

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Intel Security (Intel Corporation)

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Dell Technologies Inc

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Capgemini

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 IDECSI Enterprise Security

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 IBM Corporation

List of Figures

- Figure 1: Sweden Cyber Security Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Sweden Cyber Security Industry Share (%) by Company 2024

List of Tables

- Table 1: Sweden Cyber Security Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Sweden Cyber Security Industry Revenue Million Forecast, by Offering 2019 & 2032

- Table 3: Sweden Cyber Security Industry Revenue Million Forecast, by Deployment 2019 & 2032

- Table 4: Sweden Cyber Security Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 5: Sweden Cyber Security Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Sweden Cyber Security Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: Sweden Cyber Security Industry Revenue Million Forecast, by Offering 2019 & 2032

- Table 8: Sweden Cyber Security Industry Revenue Million Forecast, by Deployment 2019 & 2032

- Table 9: Sweden Cyber Security Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 10: Sweden Cyber Security Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Sweden Cyber Security Industry?

The projected CAGR is approximately 6.50%.

2. Which companies are prominent players in the Sweden Cyber Security Industry?

Key companies in the market include IBM Corporation, Fortinet Inc, F5 Networks Inc, Cisco Systems Inc, Clavister, AVG Technologies, Intel Security (Intel Corporation), Dell Technologies Inc, Capgemini, IDECSI Enterprise Security.

3. What are the main segments of the Sweden Cyber Security Industry?

The market segments include Offering, Deployment, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Digitalization and Scalable IT Infrastructure; Need to tackle risks from various trends such as third-party vendor risks. the evolution of MSSPs. and adoption of cloud-first strategy.

6. What are the notable trends driving market growth?

Cloud Segment is one of the Factor Driving the Market.

7. Are there any restraints impacting market growth?

Lack of Cybersecurity Professionals; High Reliance on Traditional Authentication Methods and Low Preparedness.

8. Can you provide examples of recent developments in the market?

May 2022 - Cisco announced that it had released the Cisco Cloud Controls Framework (CCF) to the public. Cisco CCF is a comprehensive set of national and international security compliance and certification requirements aggregated in one framework.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Sweden Cyber Security Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Sweden Cyber Security Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Sweden Cyber Security Industry?

To stay informed about further developments, trends, and reports in the Sweden Cyber Security Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence