Key Insights

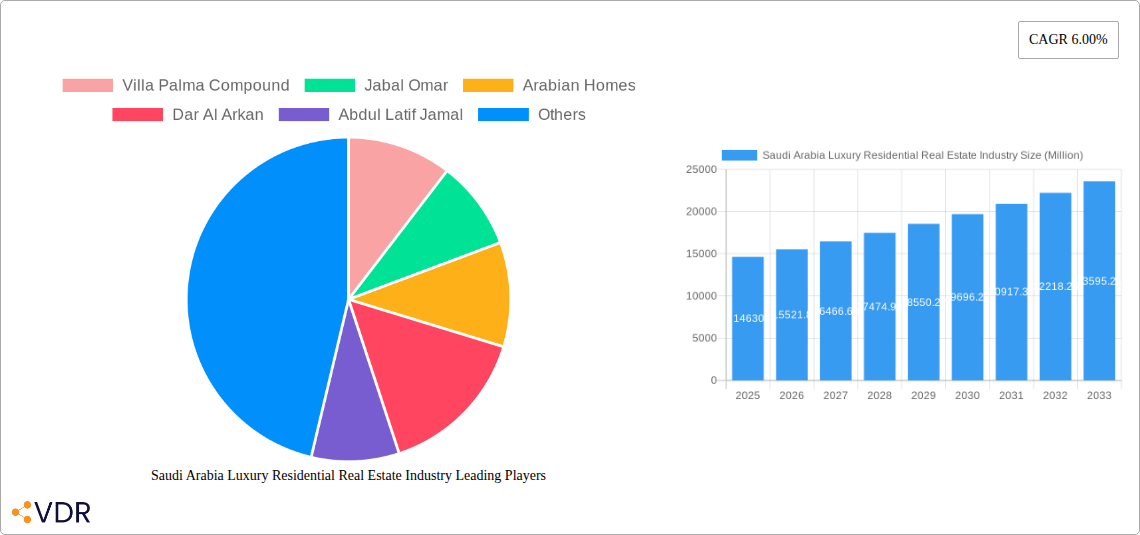

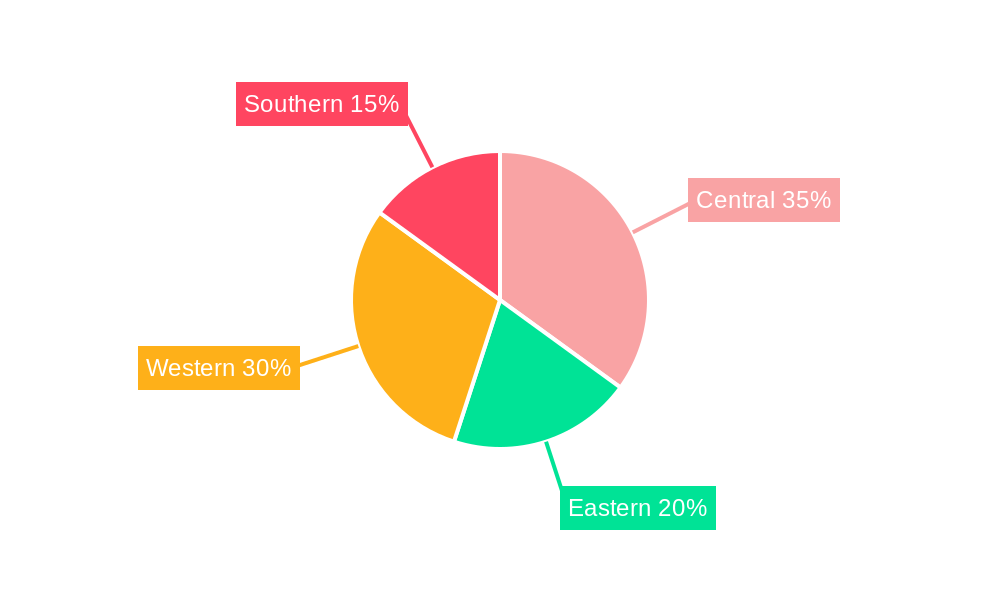

The Saudi Arabian luxury residential real estate market, valued at $14.63 billion in 2025, is poised for robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of 6% from 2025 to 2033. This growth is fueled by several key factors. Firstly, significant government initiatives aimed at diversifying the Saudi economy (Vision 2030) are attracting substantial foreign investment and high-net-worth individuals, increasing demand for upscale properties. Secondly, a burgeoning middle class with rising disposable incomes is also contributing to the market's expansion. The preference for larger, more luxurious homes, particularly villas and landed houses, is evident across major cities like Riyadh, Jeddah, and Dammam, driving segment-specific growth. However, challenges remain, including potential fluctuations in oil prices and the overall economic climate, which could influence investor confidence and purchasing power. Furthermore, the availability of land suitable for luxury developments and stringent building regulations might pose some constraints on the market's expansion. The competitive landscape is marked by established players like Villa Palma Compound, Jabal Omar, and Dar AI Arkan, alongside emerging developers, signifying a dynamic and evolving market. The regional distribution of luxury properties shows a higher concentration in the Western and Central regions of the Kingdom, aligning with the concentration of major cities and economic activity.

The segmentation of the market into apartments/condominiums and villas/landed houses provides valuable insights. Villas and landed houses currently command a larger market share, reflecting a strong preference for spacious, independent living among high-net-worth buyers. The geographical breakdown highlights the dominance of Riyadh, Jeddah, and Dammam, representing key hubs for economic growth and luxury real estate development. The "Other Cities" segment demonstrates potential for future growth as infrastructural development and economic diversification expand beyond the main metropolitan areas. Future projections indicate a sustained, albeit potentially moderated, growth trajectory, contingent on the continued success of Vision 2030 and the stability of global economic conditions. The market's performance will be closely tied to broader macroeconomic trends, government policies, and evolving consumer preferences within the luxury residential sector.

Saudi Arabia Luxury Residential Real Estate Industry: Market Report 2019-2033

This comprehensive report provides an in-depth analysis of the burgeoning Saudi Arabia luxury residential real estate market, encompassing the period 2019-2033. It examines market dynamics, growth trends, key players, and future opportunities within this lucrative sector. The report is essential for investors, developers, industry professionals, and anyone seeking to understand the complexities and potential of this rapidly evolving market. This report segments the market by Type (Apartments & Condominiums, Villas & Landed Houses) and City (Riyadh, Jeddah, Dammam Metropolitan Area, Other Cities).

Saudi Arabia Luxury Residential Real Estate Industry Market Dynamics & Structure

The Saudi Arabian luxury residential real estate market is characterized by a moderately concentrated landscape, with a few major players holding significant market share. The market’s growth is driven by technological innovations in construction and design, government initiatives promoting real estate development (Vision 2030), and a rising high-net-worth individual (HNWI) population. Regulatory frameworks, while evolving, are increasingly supportive of foreign investment and development. The main competitive substitutes are existing luxury properties and alternative investment options. End-user demographics show a strong preference for villas and landed houses, particularly in Riyadh and Jeddah. M&A activity has been moderate, with a reported xx deals valued at approximately xx Million USD in 2024.

- Market Concentration: Moderately concentrated, with top 5 players holding approximately xx% market share (2024).

- Technological Innovation: Adoption of smart home technology, sustainable building materials, and advanced construction techniques are key drivers. Barriers include high initial investment costs and limited skilled labor.

- Regulatory Framework: Supportive government policies and streamlined approvals processes are driving growth, though specific regulations may vary across cities.

- Competitive Substitutes: Existing luxury properties, international real estate investments, and alternative asset classes compete for investment capital.

- End-User Demographics: High-net-worth individuals (HNWIs), expatriates, and affluent Saudi nationals are primary target consumers. Demand for villas and landed properties in prime locations is substantial.

- M&A Trends: Moderate M&A activity, with a focus on strategic acquisitions to expand market reach and product portfolios.

Saudi Arabia Luxury Residential Real Estate Industry Growth Trends & Insights

The Saudi Arabian luxury residential real estate market experienced significant growth in the historical period (2019-2024), with a CAGR of xx%. This growth is projected to continue during the forecast period (2025-2033), with an estimated CAGR of xx%, driven by factors including Vision 2030 initiatives, rising disposable incomes, and increasing demand for luxury housing. The market size in 2025 is estimated at xx Million USD, and it is forecast to reach xx Million USD by 2033. The adoption rate of smart home technologies is increasing steadily, alongside a growing preference for sustainable and energy-efficient properties. Shifting consumer behavior shows a rising demand for personalized and bespoke luxury housing solutions. Technological disruptions, including the use of Building Information Modeling (BIM) and 3D printing, are slowly transforming the industry. Market penetration of luxury properties remains relatively low, indicating significant growth potential.

Dominant Regions, Countries, or Segments in Saudi Arabia Luxury Residential Real Estate Industry

Riyadh and Jeddah dominate the Saudi Arabian luxury residential real estate market, accounting for xx% and xx% of the total market value in 2024 respectively. Villas and landed houses comprise the largest segment by type, reflecting strong cultural preferences and the availability of larger land parcels.

- Key Drivers for Riyadh: Strong economic activity, government investment in infrastructure, and the concentration of high-net-worth individuals.

- Key Drivers for Jeddah: Coastal location, established luxury real estate developments, and a significant expatriate population.

- Key Drivers for Villas & Landed Houses: Cultural preferences for spacious living, larger land parcels, and greater privacy.

- Market Share: Riyadh holds the largest market share, exceeding xx% in 2024, followed by Jeddah with xx%. Growth potential remains high across all cities, particularly in areas experiencing infrastructural development.

Saudi Arabia Luxury Residential Real Estate Industry Product Landscape

The luxury residential real estate sector in Saudi Arabia offers a diverse range of products, from ultra-modern high-rise apartments and penthouses to sprawling villas with bespoke amenities. Innovations include the incorporation of smart home technology, sustainable building materials, and personalized design features tailored to individual client preferences. Key performance metrics include property values, rental yields, and occupancy rates. Unique selling propositions include prime locations, luxurious finishes, state-of-the-art amenities, and access to exclusive services. Technological advancements are enhancing design efficiency, construction speed, and energy efficiency.

Key Drivers, Barriers & Challenges in Saudi Arabia Luxury Residential Real Estate Industry

Key Drivers:

- Vision 2030 initiatives promoting real estate development and diversification of the economy.

- Rising disposable incomes amongst the Saudi population and a growing HNW population.

- Increased foreign investment and tourism.

- Government support for infrastructure development in key cities.

Key Challenges:

- High construction costs and land scarcity in prime locations.

- Potential supply chain disruptions and material price fluctuations.

- Regulatory hurdles and complexities in obtaining permits and approvals.

- Intense competition from established and emerging players. This competition leads to pressure on pricing and profit margins, potentially impacting development investment decisions. This effect is estimated to reduce market growth by approximately xx% by 2030.

Emerging Opportunities in Saudi Arabia Luxury Residential Real Estate Industry

- Development of sustainable and eco-friendly luxury properties catering to environmentally conscious buyers.

- Increased focus on smart home technologies and integrated security systems.

- Expansion into new markets, such as those catering to specific lifestyle preferences (e.g., golf course communities, beachfront properties).

- Growth of fractional ownership and alternative investment models for luxury properties.

Growth Accelerators in the Saudi Arabia Luxury Residential Real Estate Industry Industry

Technological breakthroughs in sustainable construction methods, smart home technology and design software are driving efficiency and reducing costs. Strategic partnerships between local and international developers facilitate access to capital and expertise, propelling large-scale development projects. Market expansion strategies focusing on untapped markets and new luxury amenities cater to a broadening range of buyer preferences.

Key Players Shaping the Saudi Arabia Luxury Residential Real Estate Market

- Villa Palma Compound

- Jabal Omar

- Arabian Homes

- Dar Al Arkan

- Abdul Latif Jamal

- AL Nassar

- AI Sedan

- Rafal Real Estate Development Company

- Sedco Development

- Alfirah United Company for Real Estate

- Saudi Real Estate Company (Al Akaria)

Notable Milestones in Saudi Arabia Luxury Residential Real Estate Industry Sector

- May 2023: Sedco Development partners with Hamad M.AlMousa Real Estate Co. to develop a 1.9 million square meter project in Al-Qadisiyah, Riyadh. This significantly expands the supply of luxury residential land in a prime location.

- April 2023: Dar Al Arkan launches "Ai Masyuf," a new residential project in Riyadh offering diverse housing options, increasing luxury housing supply and choice.

In-Depth Saudi Arabia Luxury Residential Real Estate Industry Market Outlook

The Saudi Arabian luxury residential real estate market is poised for sustained growth over the next decade, driven by strong economic fundamentals, supportive government policies, and evolving consumer preferences. Strategic opportunities abound for developers who can adapt to emerging trends, leverage technological advancements, and meet the evolving needs of discerning luxury buyers. The market's future potential is significant, with substantial growth anticipated in key cities and segments. Continued diversification of product offerings and expansion into new luxury markets will define future success in this dynamic sector.

Saudi Arabia Luxury Residential Real Estate Industry Segmentation

-

1. Type

- 1.1. Apartments and Condominiums

- 1.2. Villas and Landed Houses

-

2. City

- 2.1. Riyadh

- 2.2. Jeddah

- 2.3. Dammam Metropolitan Area

- 2.4. Other Cities

Saudi Arabia Luxury Residential Real Estate Industry Segmentation By Geography

- 1. Saudi Arabia

Saudi Arabia Luxury Residential Real Estate Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 6.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Rising Disposable Incomes4.; Government Initiatives4.; Growing Expatriate Population

- 3.3. Market Restrains

- 3.3.1. 4.; Regulatory Framework4.; The Risk of Oversupply

- 3.4. Market Trends

- 3.4.1. Demand for Apartments remains High due to Cultural Preferences in Saudi Arabia

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Saudi Arabia Luxury Residential Real Estate Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Apartments and Condominiums

- 5.1.2. Villas and Landed Houses

- 5.2. Market Analysis, Insights and Forecast - by City

- 5.2.1. Riyadh

- 5.2.2. Jeddah

- 5.2.3. Dammam Metropolitan Area

- 5.2.4. Other Cities

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Saudi Arabia

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Central Saudi Arabia Luxury Residential Real Estate Industry Analysis, Insights and Forecast, 2019-2031

- 7. Eastern Saudi Arabia Luxury Residential Real Estate Industry Analysis, Insights and Forecast, 2019-2031

- 8. Western Saudi Arabia Luxury Residential Real Estate Industry Analysis, Insights and Forecast, 2019-2031

- 9. Southern Saudi Arabia Luxury Residential Real Estate Industry Analysis, Insights and Forecast, 2019-2031

- 10. Competitive Analysis

- 10.1. Market Share Analysis 2024

- 10.2. Company Profiles

- 10.2.1 Villa Palma Compound

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 Jabal Omar

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 Arabian Homes

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 Dar AI Arkan

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 Abdul Latif Jamal

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 AL Nassar**List Not Exhaustive

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 AI Sedan

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 Rafal Real Estate Development Company

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.9 Sedco Development

- 10.2.9.1. Overview

- 10.2.9.2. Products

- 10.2.9.3. SWOT Analysis

- 10.2.9.4. Recent Developments

- 10.2.9.5. Financials (Based on Availability)

- 10.2.10 Alfirah United Company for Real Estate

- 10.2.10.1. Overview

- 10.2.10.2. Products

- 10.2.10.3. SWOT Analysis

- 10.2.10.4. Recent Developments

- 10.2.10.5. Financials (Based on Availability)

- 10.2.11 Saudi Real Estate Company (Al Akaria)

- 10.2.11.1. Overview

- 10.2.11.2. Products

- 10.2.11.3. SWOT Analysis

- 10.2.11.4. Recent Developments

- 10.2.11.5. Financials (Based on Availability)

- 10.2.1 Villa Palma Compound

List of Figures

- Figure 1: Saudi Arabia Luxury Residential Real Estate Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Saudi Arabia Luxury Residential Real Estate Industry Share (%) by Company 2024

List of Tables

- Table 1: Saudi Arabia Luxury Residential Real Estate Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Saudi Arabia Luxury Residential Real Estate Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 3: Saudi Arabia Luxury Residential Real Estate Industry Revenue Million Forecast, by City 2019 & 2032

- Table 4: Saudi Arabia Luxury Residential Real Estate Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Saudi Arabia Luxury Residential Real Estate Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: Central Saudi Arabia Luxury Residential Real Estate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Eastern Saudi Arabia Luxury Residential Real Estate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Western Saudi Arabia Luxury Residential Real Estate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Southern Saudi Arabia Luxury Residential Real Estate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Saudi Arabia Luxury Residential Real Estate Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 11: Saudi Arabia Luxury Residential Real Estate Industry Revenue Million Forecast, by City 2019 & 2032

- Table 12: Saudi Arabia Luxury Residential Real Estate Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Saudi Arabia Luxury Residential Real Estate Industry?

The projected CAGR is approximately 6.00%.

2. Which companies are prominent players in the Saudi Arabia Luxury Residential Real Estate Industry?

Key companies in the market include Villa Palma Compound, Jabal Omar, Arabian Homes, Dar AI Arkan, Abdul Latif Jamal, AL Nassar**List Not Exhaustive, AI Sedan, Rafal Real Estate Development Company, Sedco Development, Alfirah United Company for Real Estate, Saudi Real Estate Company (Al Akaria).

3. What are the main segments of the Saudi Arabia Luxury Residential Real Estate Industry?

The market segments include Type, City.

4. Can you provide details about the market size?

The market size is estimated to be USD 14.63 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Rising Disposable Incomes4.; Government Initiatives4.; Growing Expatriate Population.

6. What are the notable trends driving market growth?

Demand for Apartments remains High due to Cultural Preferences in Saudi Arabia.

7. Are there any restraints impacting market growth?

4.; Regulatory Framework4.; The Risk of Oversupply.

8. Can you provide examples of recent developments in the market?

May 2023: Sedco Development has partnered with Hamad M.AlMousa Real Estate Co. to develop a new 1.9 million square meter land development in Al-Qadisiyah, Riyadh. The project is part of SEDCO'S real estate strategy to make Riyadh a key business, commercial, and residential hub.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Saudi Arabia Luxury Residential Real Estate Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Saudi Arabia Luxury Residential Real Estate Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Saudi Arabia Luxury Residential Real Estate Industry?

To stay informed about further developments, trends, and reports in the Saudi Arabia Luxury Residential Real Estate Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence