Key Insights

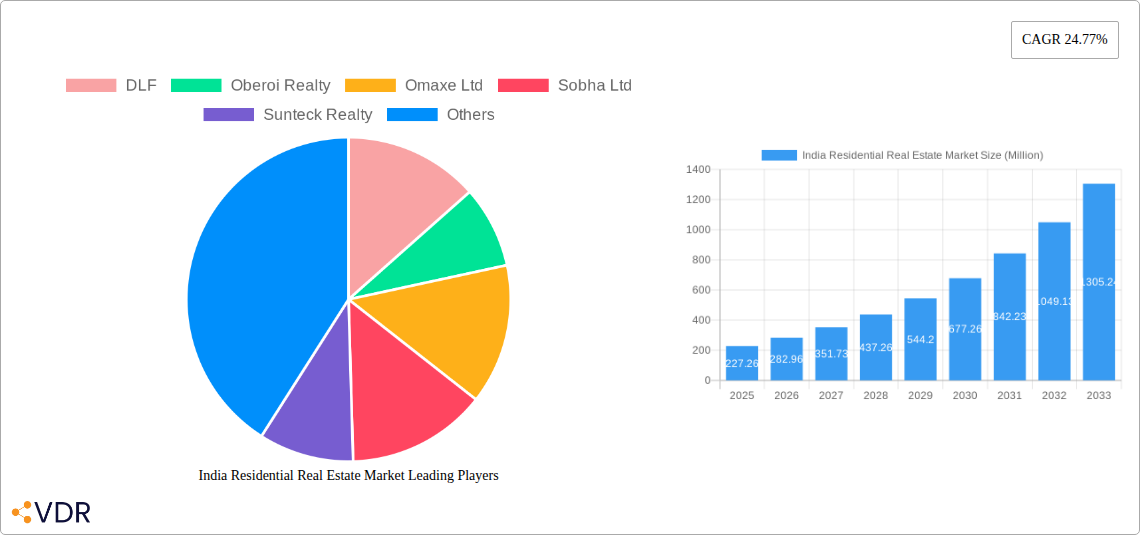

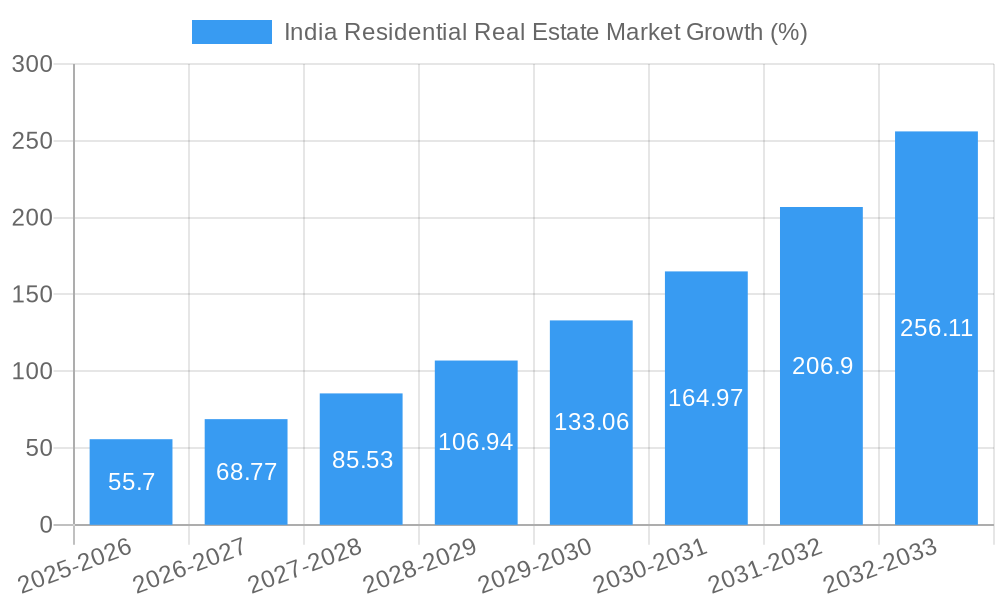

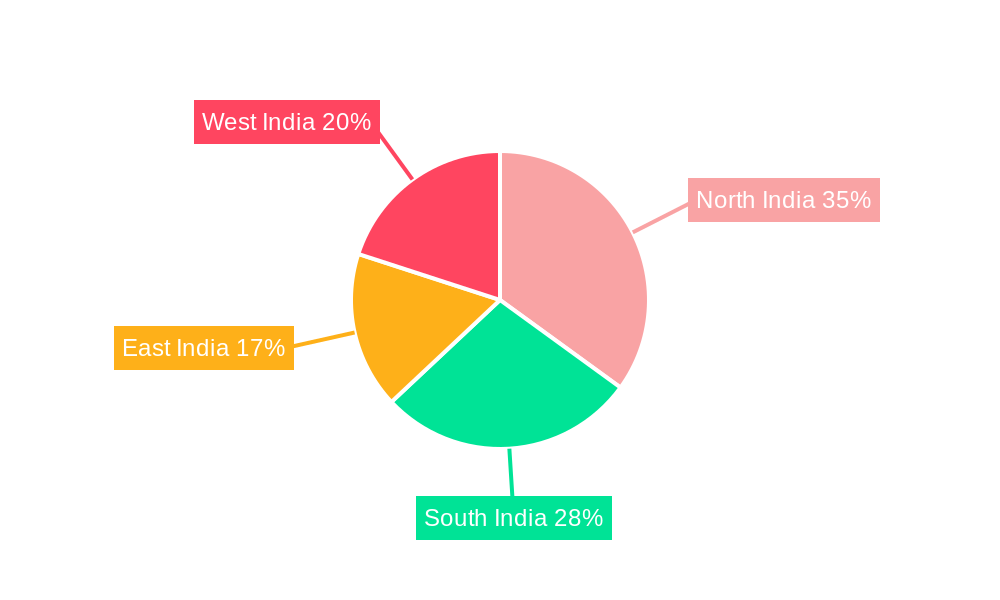

The India residential real estate market, valued at ₹227.26 billion in 2025, is poised for robust growth, exhibiting a Compound Annual Growth Rate (CAGR) of 24.77% from 2025 to 2033. This expansion is fueled by several key drivers. A burgeoning middle class with increasing disposable incomes is a primary factor, coupled with favorable government policies aimed at boosting affordable housing and infrastructure development. Urbanization continues to drive demand, particularly in major metropolitan areas and rapidly developing Tier-II cities. The preference for larger homes and improved amenities, including smart home technology and sustainable features, is also contributing to market growth. However, challenges remain. High property prices in prime locations and fluctuating interest rates can act as restraints. Furthermore, regulatory hurdles and land acquisition complexities can impact project timelines and overall market efficiency. The market is segmented by property type, with condominiums and villas dominating, and geographically, with North, South, East, and West India exhibiting varying levels of growth depending on regional economic conditions and infrastructure development. Leading players like DLF, Oberoi Realty, and Godrej Properties are strategically positioning themselves to capitalize on this expansion through innovative projects and targeted marketing campaigns.

The projected market size for 2033 can be estimated by extrapolating the CAGR. While precise figures require detailed financial modeling, a reasonable approximation, based on the 24.77% CAGR and a 2025 value of ₹227.26 billion, suggests significant market expansion over the forecast period. The segments within the market—condominiums, villas, and other types—will experience growth at varying paces reflecting differing price points and consumer preferences. Regional variations will also be significant, with some areas outpacing others in terms of both supply and demand based on factors such as infrastructure development, economic growth, and government initiatives. The competitive landscape will see existing players consolidating their market share while new entrants strive for a foothold. This dynamic environment requires continuous adaptation and strategic planning for success in this rapidly evolving market.

India Residential Real Estate Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the India residential real estate market, encompassing historical data (2019-2024), current market conditions (Base Year: 2025), and future projections (Forecast Period: 2025-2033). The report delves into market dynamics, growth trends, dominant segments (Condominiums, Villas, Other Types), key players, and emerging opportunities, providing valuable insights for industry professionals, investors, and stakeholders. The study covers a vast market landscape, examining both parent (Residential Real Estate) and child markets (Condominiums, Villas, etc.) to offer a granular perspective. Market sizes are presented in million units.

India Residential Real Estate Market Dynamics & Structure

This section analyzes the market structure, competition, technological advancements, and regulatory landscape of the Indian residential real estate market. The market is characterized by a mix of large established players and smaller regional developers. Market concentration is moderate, with a few large players holding significant market share, while numerous smaller firms contribute to the overall activity.

- Market Concentration: The top 5 players (DLF, Oberoi Realty, Prestige Estate, Godrej Properties, and L&T Realty) hold an estimated xx% market share in 2025.

- Technological Innovation: Adoption of PropTech solutions, such as online property portals and virtual reality tours, is increasing, yet faces barriers such as digital literacy and internet penetration in certain regions.

- Regulatory Framework: Government policies such as affordable housing initiatives and RERA (Real Estate (Regulation and Development) Act) significantly influence market dynamics.

- Competitive Product Substitutes: Rental markets and alternative housing solutions present some level of competitive pressure.

- End-User Demographics: Growing urbanization, rising disposable incomes, and a young population fuel the demand for residential properties.

- M&A Trends: The market witnessed xx M&A deals in the historical period (2019-2024), with an increasing trend observed in recent years. Notable deals include the Shriram Properties and ASK Property Fund partnership.

The qualitative analysis reveals that innovation faces challenges due to fragmented technology adoption across developers and a lack of standardized data sharing. The regulatory environment, while improving with RERA, still presents complexities for seamless project execution.

India Residential Real Estate Market Growth Trends & Insights

The Indian residential real estate market experienced significant growth during the historical period (2019-2024), driven by robust economic growth and increased urbanization. The market size is estimated at xx million units in 2025, exhibiting a CAGR of xx% during the historical period. The forecast period (2025-2033) projects continued growth, albeit at a slightly moderated pace, driven by factors such as government infrastructure projects and sustained demand from the burgeoning middle class. Technological disruptions, such as the increasing use of PropTech and sustainable construction methods, are impacting adoption rates and consumer preferences. Consumers are increasingly seeking technologically advanced and sustainable housing options, leading to a shift in preferences from traditional properties. This demand influences design and construction techniques, driving the integration of smart home technology and environmentally friendly materials.

Dominant Regions, Countries, or Segments in India Residential Real Estate Market

The condominium segment dominates the Indian residential real estate market, accounting for an estimated xx% market share in 2025. Key growth drivers include:

- Urbanization: Rapid migration to urban centers fuels the demand for high-density housing solutions.

- Affordability: Government initiatives promoting affordable housing increase accessibility.

- Infrastructure Development: Improvements in transportation and utilities enhance the appeal of residential areas.

- Amenities: Condominiums often offer a wide range of amenities, enhancing their appeal.

Metropolitan areas such as Mumbai, Delhi-NCR, Bengaluru, and Chennai exhibit the highest growth rates, primarily due to their robust economies and large populations. While villas represent a smaller segment, they also show positive growth, driven by increased disposable incomes and demand for luxury properties in select locations. The "Other Types" segment includes plots, row houses and other forms of housing units which showcase a moderate growth rate due to a wide range of affordability options.

India Residential Real Estate Market Product Landscape

The Indian residential real estate market offers a diverse range of products, including luxury apartments, affordable housing units, villas, and plotted developments. Product innovations focus on incorporating smart home technologies, sustainable construction materials, and enhanced security features. The unique selling propositions often center around location, amenities, and the overall lifestyle experience offered by the development. Technological advancements such as BIM (Building Information Modeling) and IoT (Internet of Things) integration are improving efficiency and the quality of construction.

Key Drivers, Barriers & Challenges in India Residential Real Estate Market

Key Drivers:

- Economic growth: Rising disposable incomes and a growing middle class fuel demand.

- Urbanization: Increased migration to cities drives the need for housing.

- Government initiatives: Policies promoting affordable housing and infrastructure development.

- Technological advancements: PropTech solutions improve efficiency and transparency.

Key Challenges:

- Land acquisition: Complex land acquisition procedures and high land costs.

- Regulatory hurdles: Navigating complex regulations and obtaining necessary approvals.

- Funding constraints: Securing funding for large-scale projects.

- Supply chain issues: Disruptions in material supply and labor shortages.

- Competition: Intense competition among developers. These challenges can lead to project delays and increased costs impacting profitability and market stability. Estimates indicate that land acquisition issues can delay projects by an average of xx months, causing a xx% increase in costs.

Emerging Opportunities in India Residential Real Estate Market

- Affordable housing: Significant untapped potential in providing affordable and quality housing.

- Smart homes: Integrating smart technologies into residential properties.

- Green buildings: Growing demand for environmentally sustainable housing.

- Senior living communities: Meeting the needs of an aging population.

- Tier II and Tier III cities: Expansion opportunities in emerging urban centers.

Growth Accelerators in the India Residential Real Estate Market Industry

Long-term growth will be fueled by continued urbanization, supportive government policies, technological innovations, and strategic partnerships. The increasing adoption of PropTech will streamline processes, enhance transparency, and improve efficiency across the value chain. Strategic partnerships between developers and technology firms will accelerate the integration of cutting-edge technologies, leading to the development of more sustainable and desirable housing solutions.

Key Players Shaping the India Residential Real Estate Market Market

- DLF

- Oberoi Realty

- Omaxe Ltd

- Sobha Ltd

- Sunteck Realty

- Prestige Estate

- Brigade Enterprises

- Indiabulls Real Estate

- NBCC (India)

- Dlip Buildcon

- Ansal Properties and Infrastructure Ltd

- Godrej Properties

- L&T Realty Ltd

- Phoenix Mills

List Not Exhaustive

Notable Milestones in India Residential Real Estate Market Sector

- October 2022: Shriram Properties Ltd and ASK Property Fund announced a INR 500 crore (USD 608.98 million) investment platform for acquiring housing projects, signaling increased investment activity and consolidation in the market.

- October 2022: Magnolia Quality Development Corporation (MQDC) expressed interest in developing a luxury residential project in the NCR, indicating a growing interest in the Indian luxury real estate sector by international players.

In-Depth India Residential Real Estate Market Market Outlook

The Indian residential real estate market is poised for sustained growth over the forecast period, driven by fundamental factors such as urbanization, rising incomes, and supportive government policies. Strategic partnerships, technological advancements, and the emergence of innovative housing solutions will shape future market dynamics. Opportunities exist in developing sustainable, affordable, and technologically advanced housing options to cater to evolving consumer preferences. The market will continue to witness consolidation, with larger players acquiring smaller developers and expanding their market share. The potential for growth in Tier II and Tier III cities also presents significant opportunities for investors and developers.

India Residential Real Estate Market Segmentation

-

1. Type

- 1.1. Condominiums and Apartments

- 1.2. Villas and Landed House

India Residential Real Estate Market Segmentation By Geography

- 1. India

India Residential Real Estate Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 24.77% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Growing urban population driving the growth of transportation infrastructure.; Sultanate's Economic Diversification Plan (Vision 2040) to provide new growth to the market

- 3.3. Market Restrains

- 3.3.1. Delay in project approvals; High cost of materials

- 3.4. Market Trends

- 3.4.1. Increasing Demand for Big Residential Spaces Driving the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. India Residential Real Estate Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Condominiums and Apartments

- 5.1.2. Villas and Landed House

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. India

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. North India India Residential Real Estate Market Analysis, Insights and Forecast, 2019-2031

- 7. South India India Residential Real Estate Market Analysis, Insights and Forecast, 2019-2031

- 8. East India India Residential Real Estate Market Analysis, Insights and Forecast, 2019-2031

- 9. West India India Residential Real Estate Market Analysis, Insights and Forecast, 2019-2031

- 10. Competitive Analysis

- 10.1. Market Share Analysis 2024

- 10.2. Company Profiles

- 10.2.1 DLF

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 Oberoi Realty

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 Omaxe Ltd

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 Sobha Ltd

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 Sunteck Realty

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 Prestige Estate

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 Brigade Enterprises**List Not Exhaustive

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 Indiabulls Real Estate

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.9 NBCC (India)

- 10.2.9.1. Overview

- 10.2.9.2. Products

- 10.2.9.3. SWOT Analysis

- 10.2.9.4. Recent Developments

- 10.2.9.5. Financials (Based on Availability)

- 10.2.10 Dlip Buildcon

- 10.2.10.1. Overview

- 10.2.10.2. Products

- 10.2.10.3. SWOT Analysis

- 10.2.10.4. Recent Developments

- 10.2.10.5. Financials (Based on Availability)

- 10.2.11 Ansal Properties and Infrastructure Ltd

- 10.2.11.1. Overview

- 10.2.11.2. Products

- 10.2.11.3. SWOT Analysis

- 10.2.11.4. Recent Developments

- 10.2.11.5. Financials (Based on Availability)

- 10.2.12 Godrej Properties

- 10.2.12.1. Overview

- 10.2.12.2. Products

- 10.2.12.3. SWOT Analysis

- 10.2.12.4. Recent Developments

- 10.2.12.5. Financials (Based on Availability)

- 10.2.13 L&T Realty Ltd

- 10.2.13.1. Overview

- 10.2.13.2. Products

- 10.2.13.3. SWOT Analysis

- 10.2.13.4. Recent Developments

- 10.2.13.5. Financials (Based on Availability)

- 10.2.14 Phoenix Mills

- 10.2.14.1. Overview

- 10.2.14.2. Products

- 10.2.14.3. SWOT Analysis

- 10.2.14.4. Recent Developments

- 10.2.14.5. Financials (Based on Availability)

- 10.2.1 DLF

List of Figures

- Figure 1: India Residential Real Estate Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: India Residential Real Estate Market Share (%) by Company 2024

List of Tables

- Table 1: India Residential Real Estate Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: India Residential Real Estate Market Revenue Million Forecast, by Type 2019 & 2032

- Table 3: India Residential Real Estate Market Revenue Million Forecast, by Region 2019 & 2032

- Table 4: India Residential Real Estate Market Revenue Million Forecast, by Country 2019 & 2032

- Table 5: North India India Residential Real Estate Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 6: South India India Residential Real Estate Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: East India India Residential Real Estate Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: West India India Residential Real Estate Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: India Residential Real Estate Market Revenue Million Forecast, by Type 2019 & 2032

- Table 10: India Residential Real Estate Market Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the India Residential Real Estate Market?

The projected CAGR is approximately 24.77%.

2. Which companies are prominent players in the India Residential Real Estate Market?

Key companies in the market include DLF, Oberoi Realty, Omaxe Ltd, Sobha Ltd, Sunteck Realty, Prestige Estate, Brigade Enterprises**List Not Exhaustive, Indiabulls Real Estate, NBCC (India), Dlip Buildcon, Ansal Properties and Infrastructure Ltd, Godrej Properties, L&T Realty Ltd, Phoenix Mills.

3. What are the main segments of the India Residential Real Estate Market?

The market segments include Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 227.26 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing urban population driving the growth of transportation infrastructure.; Sultanate's Economic Diversification Plan (Vision 2040) to provide new growth to the market.

6. What are the notable trends driving market growth?

Increasing Demand for Big Residential Spaces Driving the Market.

7. Are there any restraints impacting market growth?

Delay in project approvals; High cost of materials.

8. Can you provide examples of recent developments in the market?

October 2022- Shriram Properties Ltd and ASK Property Fund agreed to establish an INR 500 crore (USD 608.98 million) investment platform to acquire housing projects. Both companies have signed an agreement to establish an investment platform to acquire residential real estate projects. Shriram and ASK will co-invest in plotted residential development projects in Bengaluru, Chennai, and Hyderabad as part of the platform agreement.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "India Residential Real Estate Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the India Residential Real Estate Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the India Residential Real Estate Market?

To stay informed about further developments, trends, and reports in the India Residential Real Estate Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence