Key Insights

The UK mobile payments market is experiencing robust growth, fueled by increasing smartphone penetration, rising consumer preference for contactless transactions, and the expansion of mobile payment platforms. The market, valued at approximately £X million in 2025 (assuming a logical estimation based on the provided CAGR of 22.30% and a stated value unit of millions), is projected to reach £Y million by 2033. This substantial expansion is driven by several key factors. Firstly, the convenience and speed of mobile payments are attracting both consumers and businesses, particularly in urban areas. Secondly, enhanced security features and fraud prevention measures are boosting user confidence. Thirdly, the integration of mobile payments with loyalty programs and other reward systems is incentivizing adoption. Finally, the increasing prevalence of near-field communication (NFC) technology in smartphones and point-of-sale (POS) systems is further facilitating seamless transactions. The segment analysis reveals a strong preference for proximity payments (like Apple Pay and Google Pay), driven by their ease of use in everyday transactions. However, remote payments are also demonstrating significant growth potential, particularly in e-commerce and online services. Businesses are actively adopting mobile payment solutions to streamline transactions and improve customer experience. The strong presence of major players like Apple, Google, and Samsung, alongside emerging fintech companies, creates a competitive but innovative landscape within the UK market.

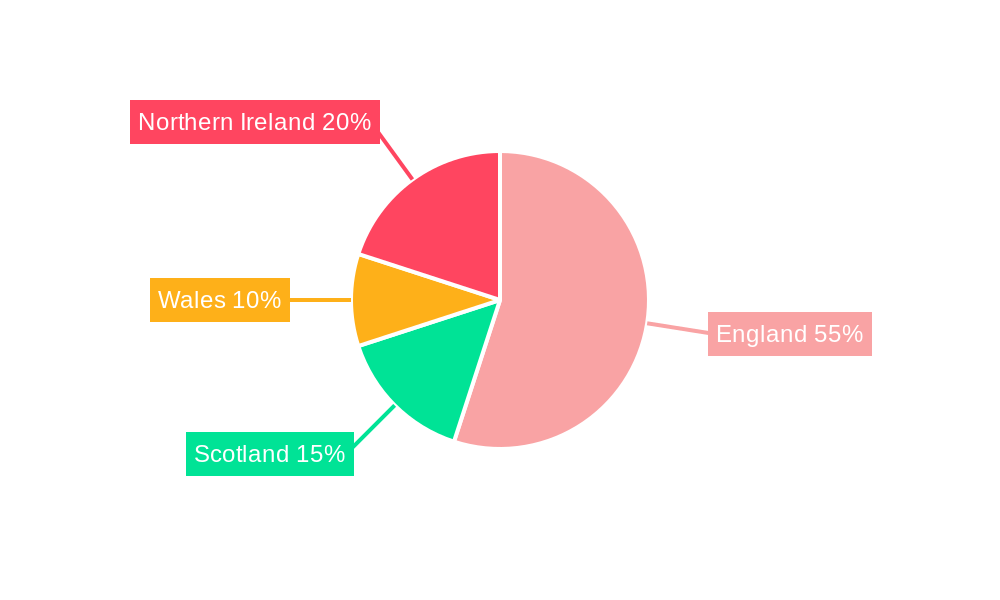

The regional breakdown indicates significant activity across England, Wales, Scotland, and Northern Ireland, reflecting the ubiquitous nature of mobile phone usage across the UK. While some challenges remain – such as security concerns and the need for broader digital literacy – the overall market outlook remains strongly positive. The continued investment in technological advancements and the increasing regulatory support are expected to further accelerate the growth of the UK mobile payments industry in the coming years, driving both innovation and wider adoption among different user demographics. Competition among established players and new entrants will remain fierce, pushing for enhanced functionalities, lower transaction fees, and more attractive user experiences.

UK Mobile Payments Industry: Market Report 2019-2033

This comprehensive report provides an in-depth analysis of the UK mobile payments industry, covering market dynamics, growth trends, key players, and future outlook. The study period spans from 2019 to 2033, with a base year of 2025 and a forecast period from 2025 to 2033. This report is essential for businesses, investors, and industry professionals seeking to understand and capitalize on the opportunities within this rapidly evolving market. The report delves into the parent market of digital payments and the child market of mobile payments, offering a granular perspective on market segmentation (Proximity Payment, Remote Payment) and end-user segments (Consumers, Businesses).

UK Mobile Payments Industry Market Dynamics & Structure

The UK mobile payments market is characterized by intense competition, rapid technological advancements, and a constantly evolving regulatory landscape. Market concentration is moderate, with a few dominant players and a large number of smaller participants. Technological innovation, driven by advancements in NFC technology, biometric authentication, and mobile wallets, is a key driver of growth. The regulatory framework, while generally supportive, presents some challenges related to data security and consumer protection. Competitive substitutes include traditional payment methods (cash, cards), but the convenience and speed of mobile payments are driving market penetration. End-user demographics show a strong correlation between mobile payment adoption and younger age groups, with a growing adoption among older demographics. M&A activity has been moderate in recent years, with xx deals recorded between 2019 and 2024, valued at approximately £xx million.

- Market Concentration: Moderate, with a few major players commanding significant market share. Apple Pay and Google Pay hold a combined xx% market share in 2024, with other players such as Samsung Pay and PayPal holding smaller, yet still significant shares.

- Technological Innovation: Significant advancements in NFC technology, biometric authentication (fingerprint, facial recognition), and tokenization are driving innovation.

- Regulatory Framework: The UK’s regulatory environment is generally supportive but requires compliance with data privacy regulations (GDPR) and financial security standards (PSD2).

- Competitive Substitutes: Traditional payment methods (cash, cards) present competition, but mobile payments' convenience is gaining traction.

- End-User Demographics: High adoption among younger demographics, with a significant upward trend in usage amongst older generations.

- M&A Activity: Moderate activity in recent years, with xx deals valued at approximately £xx million (2019-2024).

UK Mobile Payments Industry Growth Trends & Insights

The UK mobile payments market exhibited robust growth between 2019 and 2024, achieving a Compound Annual Growth Rate (CAGR) of [Insert Precise CAGR Percentage]%. This surge is attributed to several key factors: the widespread adoption of smartphones, a marked consumer preference for contactless transactions, and the continuous expansion of mobile wallet services. Market penetration reached [Insert Precise Penetration Percentage]% in 2024, with projections forecasting continued expansion. This growth trajectory is further fueled by technological innovations, including the introduction of cutting-edge payment solutions and enhanced security features. The shift in consumer behavior towards digital transactions, coupled with increasing merchant acceptance of mobile payments, is significantly propelling market expansion. The market is projected to maintain its strong growth momentum, reaching an estimated £[Insert Precise Projected Value] million by 2033.

Dominant Regions, Countries, or Segments in UK Mobile Payments Industry

London and other major UK urban centers spearhead mobile payments adoption. This leadership stems from higher smartphone penetration rates, increased consumer tech familiarity, and concentrated business activity. Analyzing the segment breakdown, proximity payments (e.g., NFC-enabled transactions) currently hold the dominant position, accounting for [Insert Precise Market Share Percentage]% of the market in 2024. This dominance is driven by the extensive availability of contactless payment terminals. However, remote payment methods are experiencing accelerated growth, fueled by the increasing popularity of online shopping and the expanding use of digital wallets. While the consumer segment constitutes the larger market share ([Insert Precise Market Share Percentage]% in 2024), the business segment demonstrates faster growth, driven by increased efficiency and reduced transaction costs associated with mobile payment processing. This suggests a potentially significant shift in the market share distribution in the coming years.

- Key Drivers: High smartphone penetration, rising consumer preference for contactless payments, widespread business acceptance, and the increasing integration of mobile payments into online platforms.

- Dominant Segments: Proximity payments maintain a leading position, but remote payments show significant growth potential. The consumer segment currently holds the largest market share.

- Geographic Dominance: London and other major urban areas exhibit the highest adoption rates.

UK Mobile Payments Industry Product Landscape

The UK mobile payments landscape features a wide range of products, from simple NFC-enabled contactless payment solutions to sophisticated mobile wallets offering diverse features like peer-to-peer transfers, loyalty programs, and bill payment functionalities. These products often incorporate advanced security features such as tokenization and biometric authentication. Key innovations include Tap to Pay functionality, allowing businesses to accept payments directly via their smartphones. The market is characterized by a continuous cycle of improvement in security, user experience, and transaction speeds.

Key Drivers, Barriers & Challenges in UK Mobile Payments Industry

Key Drivers: The widespread adoption of smartphones, the increasing popularity of contactless payments, supportive government initiatives promoting digital payments, and continuous innovation in mobile payment technologies are key drivers of market growth. Seamless integration of mobile payment solutions into existing e-commerce platforms further accelerates adoption.

Key Barriers & Challenges: Security concerns, including data breaches and fraud, remain a significant hurdle. Meeting regulatory compliance requirements related to data privacy and consumer protection presents complexities for businesses. Intense competition from established payment processors and the need for widespread merchant adoption pose ongoing challenges. Limited access to digital infrastructure in certain regions hinders broader market penetration and equitable access to mobile payment services.

Emerging Opportunities in UK Mobile Payments Industry

The integration of mobile payments with other financial services, such as budgeting tools and investment platforms, presents significant opportunities for growth. The increasing use of mobile payments in the public transport sector and other utility payments is expanding market reach. Furthermore, emerging technologies like blockchain and cryptocurrencies present potential avenues for innovation within the mobile payments space. Expansion into untapped rural markets by reducing infrastructure constraints will unlock further potential.

Growth Accelerators in the UK Mobile Payments Industry

Strategic partnerships between mobile payment providers and financial institutions are key to expanding reach and facilitating seamless integration with existing banking systems. Technological innovations, such as improved security features, enhanced user interfaces, and the expansion of Tap to Pay functionality, will drive adoption. Marketing and educational campaigns targeting underpenetrated demographics will accelerate growth. Expanding the acceptance of mobile payments in smaller businesses and across diverse sectors will lead to continued market expansion.

Key Players Shaping the UK Mobile Payments Industry Market

- Samsung Electronics (Samsung Pay)

- BitPay Inc

- Paypal Inc

- Apple Inc (Apple Pay)

- Barclays Bank UK PLC bPay

- Fitbit International Limited (Fitbit Pay)

- Google LLC (Google Pay)

- Amazon Payments Inc

- Mobile Payments Service Company Limited (Paym)

- Klarna Bank AB (publ)

Notable Milestones in UK Mobile Payments Industry Sector

- May 2022: Google launched Google Wallet, significantly expanding mobile payment capabilities and strengthening its market position.

- May 2022: The Big Issue Group partnered with PayPal's Zettle, accelerating contactless payment adoption among small businesses and demonstrating the potential of Tap to Pay technology. This highlights the increasing accessibility of mobile payment solutions for businesses of all sizes.

- [Add other significant milestones with dates and brief descriptions]

In-Depth UK Mobile Payments Industry Market Outlook

The UK mobile payments market is poised for continued robust growth, propelled by technological advancements, increasing consumer adoption, and strategic partnerships. The enhancement of mobile wallet functionalities, integration with other financial services, and expanding merchant acceptance create significant opportunities for market participants. Continued innovation in security features and user experience will be crucial for sustained growth. The long-term outlook suggests a dynamic and robust market with substantial potential for future expansion, particularly in areas currently underserved by digital infrastructure and mobile payment adoption.

UK Mobile Payments Industry Segmentation

-

1. Type

- 1.1. Proximity Payment

- 1.2. Remote Payment

UK Mobile Payments Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

UK Mobile Payments Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 22.30% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Development of M-Commerce Ecosystem with High Internet Penetration; Favorable Government Initiatives and Regulations

- 3.3. Market Restrains

- 3.3.1. Cybersecurity and Data Breaches for Mobile Payments

- 3.4. Market Trends

- 3.4.1. Internet Penetration in the UK is Driving the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global UK Mobile Payments Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Proximity Payment

- 5.1.2. Remote Payment

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. South America

- 5.2.3. Europe

- 5.2.4. Middle East & Africa

- 5.2.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. North America UK Mobile Payments Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Proximity Payment

- 6.1.2. Remote Payment

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. South America UK Mobile Payments Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Proximity Payment

- 7.1.2. Remote Payment

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe UK Mobile Payments Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Proximity Payment

- 8.1.2. Remote Payment

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Middle East & Africa UK Mobile Payments Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Proximity Payment

- 9.1.2. Remote Payment

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Asia Pacific UK Mobile Payments Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Proximity Payment

- 10.1.2. Remote Payment

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. England UK Mobile Payments Industry Analysis, Insights and Forecast, 2019-2031

- 12. Wales UK Mobile Payments Industry Analysis, Insights and Forecast, 2019-2031

- 13. Scotland UK Mobile Payments Industry Analysis, Insights and Forecast, 2019-2031

- 14. Northern UK Mobile Payments Industry Analysis, Insights and Forecast, 2019-2031

- 15. Ireland UK Mobile Payments Industry Analysis, Insights and Forecast, 2019-2031

- 16. Competitive Analysis

- 16.1. Global Market Share Analysis 2024

- 16.2. Company Profiles

- 16.2.1 Samsung Electronics (Samsung Pay)

- 16.2.1.1. Overview

- 16.2.1.2. Products

- 16.2.1.3. SWOT Analysis

- 16.2.1.4. Recent Developments

- 16.2.1.5. Financials (Based on Availability)

- 16.2.2 BitPay Inc

- 16.2.2.1. Overview

- 16.2.2.2. Products

- 16.2.2.3. SWOT Analysis

- 16.2.2.4. Recent Developments

- 16.2.2.5. Financials (Based on Availability)

- 16.2.3 Paypal Inc

- 16.2.3.1. Overview

- 16.2.3.2. Products

- 16.2.3.3. SWOT Analysis

- 16.2.3.4. Recent Developments

- 16.2.3.5. Financials (Based on Availability)

- 16.2.4 Apple Inc (Apple Pay)

- 16.2.4.1. Overview

- 16.2.4.2. Products

- 16.2.4.3. SWOT Analysis

- 16.2.4.4. Recent Developments

- 16.2.4.5. Financials (Based on Availability)

- 16.2.5 Barclays Bank UK PLC bPay

- 16.2.5.1. Overview

- 16.2.5.2. Products

- 16.2.5.3. SWOT Analysis

- 16.2.5.4. Recent Developments

- 16.2.5.5. Financials (Based on Availability)

- 16.2.6 Fitbit International Limited (Fitbit Pay)

- 16.2.6.1. Overview

- 16.2.6.2. Products

- 16.2.6.3. SWOT Analysis

- 16.2.6.4. Recent Developments

- 16.2.6.5. Financials (Based on Availability)

- 16.2.7 Google LLC (Google Pay)

- 16.2.7.1. Overview

- 16.2.7.2. Products

- 16.2.7.3. SWOT Analysis

- 16.2.7.4. Recent Developments

- 16.2.7.5. Financials (Based on Availability)

- 16.2.8 Amazon Payments Inc

- 16.2.8.1. Overview

- 16.2.8.2. Products

- 16.2.8.3. SWOT Analysis

- 16.2.8.4. Recent Developments

- 16.2.8.5. Financials (Based on Availability)

- 16.2.9 Mobile Payments Service Company Limited (Paym)

- 16.2.9.1. Overview

- 16.2.9.2. Products

- 16.2.9.3. SWOT Analysis

- 16.2.9.4. Recent Developments

- 16.2.9.5. Financials (Based on Availability)

- 16.2.10 Klarna Bank AB (publ)

- 16.2.10.1. Overview

- 16.2.10.2. Products

- 16.2.10.3. SWOT Analysis

- 16.2.10.4. Recent Developments

- 16.2.10.5. Financials (Based on Availability)

- 16.2.1 Samsung Electronics (Samsung Pay)

List of Figures

- Figure 1: Global UK Mobile Payments Industry Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: United kingdom Region UK Mobile Payments Industry Revenue (Million), by Country 2024 & 2032

- Figure 3: United kingdom Region UK Mobile Payments Industry Revenue Share (%), by Country 2024 & 2032

- Figure 4: North America UK Mobile Payments Industry Revenue (Million), by Type 2024 & 2032

- Figure 5: North America UK Mobile Payments Industry Revenue Share (%), by Type 2024 & 2032

- Figure 6: North America UK Mobile Payments Industry Revenue (Million), by Country 2024 & 2032

- Figure 7: North America UK Mobile Payments Industry Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America UK Mobile Payments Industry Revenue (Million), by Type 2024 & 2032

- Figure 9: South America UK Mobile Payments Industry Revenue Share (%), by Type 2024 & 2032

- Figure 10: South America UK Mobile Payments Industry Revenue (Million), by Country 2024 & 2032

- Figure 11: South America UK Mobile Payments Industry Revenue Share (%), by Country 2024 & 2032

- Figure 12: Europe UK Mobile Payments Industry Revenue (Million), by Type 2024 & 2032

- Figure 13: Europe UK Mobile Payments Industry Revenue Share (%), by Type 2024 & 2032

- Figure 14: Europe UK Mobile Payments Industry Revenue (Million), by Country 2024 & 2032

- Figure 15: Europe UK Mobile Payments Industry Revenue Share (%), by Country 2024 & 2032

- Figure 16: Middle East & Africa UK Mobile Payments Industry Revenue (Million), by Type 2024 & 2032

- Figure 17: Middle East & Africa UK Mobile Payments Industry Revenue Share (%), by Type 2024 & 2032

- Figure 18: Middle East & Africa UK Mobile Payments Industry Revenue (Million), by Country 2024 & 2032

- Figure 19: Middle East & Africa UK Mobile Payments Industry Revenue Share (%), by Country 2024 & 2032

- Figure 20: Asia Pacific UK Mobile Payments Industry Revenue (Million), by Type 2024 & 2032

- Figure 21: Asia Pacific UK Mobile Payments Industry Revenue Share (%), by Type 2024 & 2032

- Figure 22: Asia Pacific UK Mobile Payments Industry Revenue (Million), by Country 2024 & 2032

- Figure 23: Asia Pacific UK Mobile Payments Industry Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global UK Mobile Payments Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global UK Mobile Payments Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 3: Global UK Mobile Payments Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 4: Global UK Mobile Payments Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 5: England UK Mobile Payments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 6: Wales UK Mobile Payments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Scotland UK Mobile Payments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Northern UK Mobile Payments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Ireland UK Mobile Payments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Global UK Mobile Payments Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 11: Global UK Mobile Payments Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 12: United States UK Mobile Payments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Canada UK Mobile Payments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Mexico UK Mobile Payments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Global UK Mobile Payments Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 16: Global UK Mobile Payments Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 17: Brazil UK Mobile Payments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Argentina UK Mobile Payments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Rest of South America UK Mobile Payments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Global UK Mobile Payments Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 21: Global UK Mobile Payments Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 22: United Kingdom UK Mobile Payments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Germany UK Mobile Payments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: France UK Mobile Payments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: Italy UK Mobile Payments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Spain UK Mobile Payments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 27: Russia UK Mobile Payments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: Benelux UK Mobile Payments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 29: Nordics UK Mobile Payments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 30: Rest of Europe UK Mobile Payments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 31: Global UK Mobile Payments Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 32: Global UK Mobile Payments Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 33: Turkey UK Mobile Payments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 34: Israel UK Mobile Payments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 35: GCC UK Mobile Payments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 36: North Africa UK Mobile Payments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 37: South Africa UK Mobile Payments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 38: Rest of Middle East & Africa UK Mobile Payments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 39: Global UK Mobile Payments Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 40: Global UK Mobile Payments Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 41: China UK Mobile Payments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 42: India UK Mobile Payments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 43: Japan UK Mobile Payments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 44: South Korea UK Mobile Payments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN UK Mobile Payments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 46: Oceania UK Mobile Payments Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific UK Mobile Payments Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the UK Mobile Payments Industry?

The projected CAGR is approximately 22.30%.

2. Which companies are prominent players in the UK Mobile Payments Industry?

Key companies in the market include Samsung Electronics (Samsung Pay), BitPay Inc, Paypal Inc, Apple Inc (Apple Pay), Barclays Bank UK PLC bPay, Fitbit International Limited (Fitbit Pay), Google LLC (Google Pay), Amazon Payments Inc, Mobile Payments Service Company Limited (Paym), Klarna Bank AB (publ).

3. What are the main segments of the UK Mobile Payments Industry?

The market segments include Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Development of M-Commerce Ecosystem with High Internet Penetration; Favorable Government Initiatives and Regulations.

6. What are the notable trends driving market growth?

Internet Penetration in the UK is Driving the Market.

7. Are there any restraints impacting market growth?

Cybersecurity and Data Breaches for Mobile Payments.

8. Can you provide examples of recent developments in the market?

May 2022 - Google announced Google Wallet to store payment and non-payment assets in virtual cloud-based storage. The payment assets could include credit cards, debit cards, etc., which could be used to make payments by using the Tap to Pay feature from the smartphone, wherever Google Pay is acceptable for a mode of payment. The app will be available in 39 markets worldwide, including the United Kingdom.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "UK Mobile Payments Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the UK Mobile Payments Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the UK Mobile Payments Industry?

To stay informed about further developments, trends, and reports in the UK Mobile Payments Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence