Key Insights

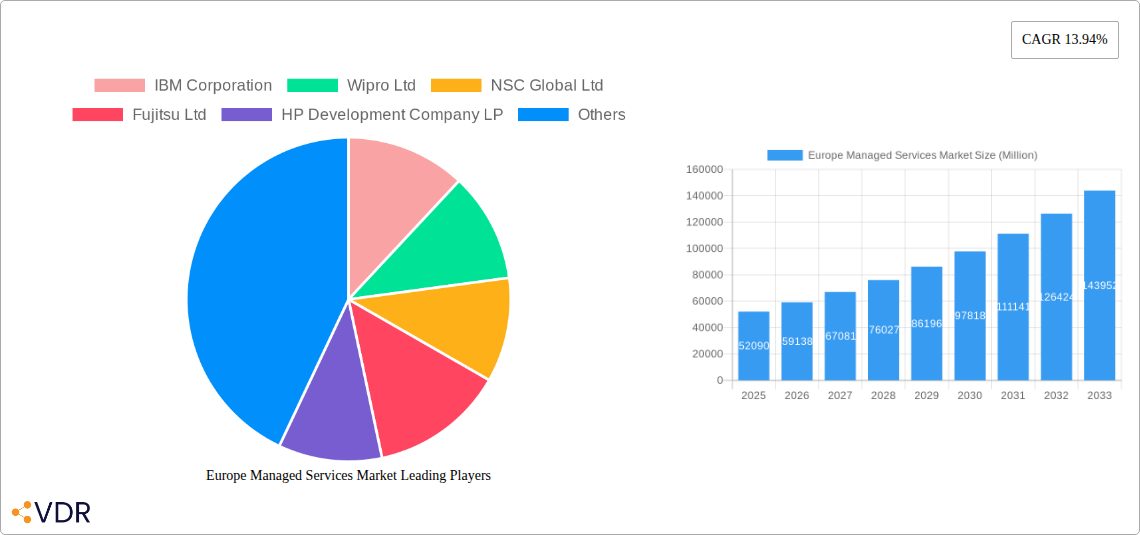

The European managed services market, valued at €52.09 billion in 2025, is projected to experience robust growth, driven by the increasing adoption of cloud technologies, the rising demand for enhanced cybersecurity, and the need for streamlined IT infrastructure management across various sectors. Small and medium-sized enterprises (SMEs) are increasingly outsourcing IT functions to focus on core business operations, contributing significantly to market expansion. The BFSI (Banking, Financial Services, and Insurance) and manufacturing sectors are key drivers, demanding sophisticated managed services for data security, compliance, and operational efficiency. Growth is further fueled by the transition to cloud-based solutions, offering scalability, cost-effectiveness, and improved accessibility. While the on-premise deployment model still holds a significant share, the cloud segment is exhibiting the highest growth rate, reflecting the ongoing digital transformation across Europe. Competitive pressures and the need for continuous innovation are pushing service providers to offer comprehensive and integrated solutions encompassing managed data centers, security, communications, networks, infrastructure, and mobility.

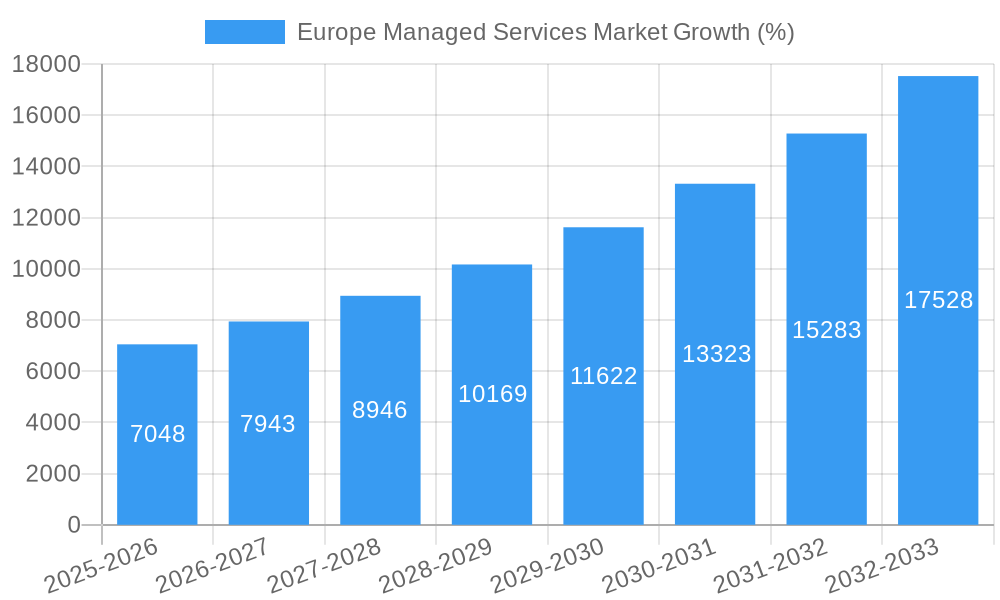

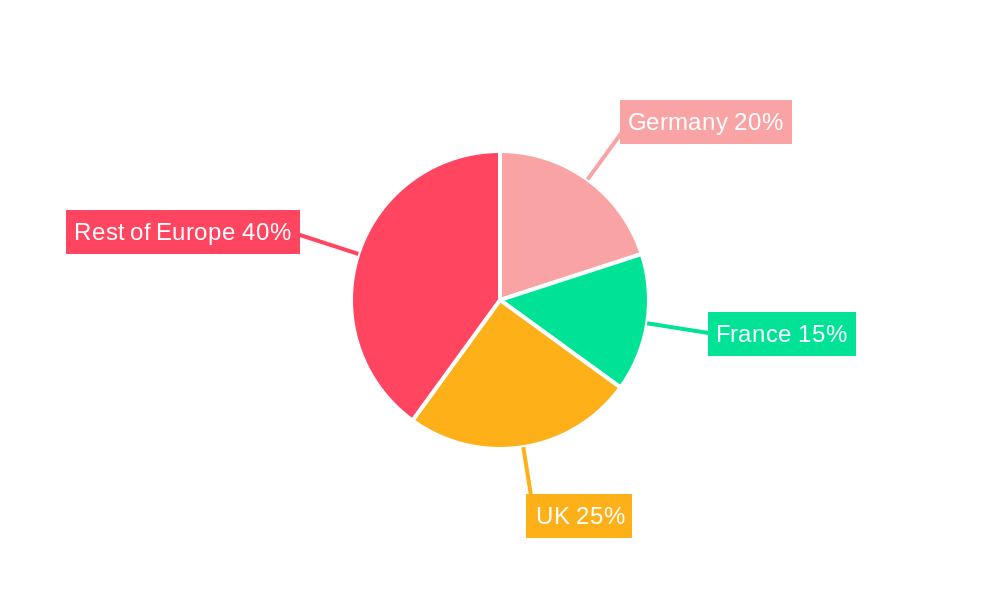

The market's growth trajectory is anticipated to remain strong throughout the forecast period (2025-2033), with a Compound Annual Growth Rate (CAGR) of 13.94%. However, potential restraints include economic fluctuations, cybersecurity threats, and the complexities associated with integrating diverse IT systems. Germany, France, and the United Kingdom represent the largest national markets, owing to their advanced digital infrastructure and robust IT sectors. Nevertheless, other European countries are also witnessing increased adoption, contributing to the overall market expansion. The competitive landscape is characterized by a mix of global technology giants and specialized managed service providers, fostering innovation and driving down prices, creating opportunities for smaller companies to emerge and compete. The market's future hinges on its ability to adapt to evolving technological advancements and the ever-changing needs of businesses across various sectors.

Europe Managed Services Market: A Comprehensive Report (2019-2033)

This comprehensive report provides an in-depth analysis of the Europe Managed Services Market, encompassing market dynamics, growth trends, dominant segments, and key players. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report offers invaluable insights for industry professionals seeking to navigate this dynamic landscape. The market is segmented by Enterprise Size (Small and Medium Enterprises, Large Enterprises), End-user Vertical (BFSI, Manufacturing, Healthcare, Retail, Other End-user Verticals), Country (United Kingdom, Germany, France, Rest of Europe), Deployment (On-premise, Cloud), and Type (Managed Data Center, Managed Security, Managed Communications, Managed Network, Managed Infrastructure, Managed Mobility). The total market size is projected to reach xx Million by 2033.

Europe Managed Services Market Market Dynamics & Structure

The European managed services market exhibits a moderately concentrated structure, with several multinational corporations holding significant market share. Technological innovation, particularly in areas like cloud computing, AI, and cybersecurity, is a primary growth driver. Stringent data privacy regulations like GDPR significantly influence market practices, demanding robust security solutions and compliance frameworks. Competitive pressures are intense, with traditional players facing competition from agile cloud-based providers. The market also witnesses substantial M&A activity as companies seek to expand their service portfolios and geographic reach.

- Market Concentration: The top 5 players account for approximately xx% of the market share in 2025.

- Technological Innovation: Cloud adoption, AI-powered automation, and the rise of SASE are key innovation drivers.

- Regulatory Framework: GDPR and other data protection laws shape security and compliance requirements.

- Competitive Substitutes: Cloud-based services and in-house IT teams present competitive alternatives.

- End-user Demographics: Large enterprises currently dominate the market, but SMEs are increasingly adopting managed services.

- M&A Trends: xx M&A deals were recorded in the European managed services sector between 2019 and 2024, indicating a consolidated market trend.

Europe Managed Services Market Growth Trends & Insights

The European managed services market has experienced consistent growth throughout the historical period (2019-2024), driven by increasing digitalization across various industries and the growing need for IT infrastructure management expertise. The market size is estimated at xx Million in 2025 and is projected to grow at a CAGR of xx% from 2025 to 2033. This growth is fueled by several factors including the expanding adoption of cloud services, the increasing prevalence of cybersecurity threats demanding enhanced security solutions, and the rising demand for flexible and scalable IT solutions. Shifting consumer behavior towards remote work and digital transformation initiatives across organizations are further accelerating market expansion. Technological disruptions, such as the advent of 5G and edge computing, are creating new opportunities while also presenting challenges for businesses to adapt quickly. Market penetration remains relatively low in certain segments (e.g., SMEs in specific verticals), indicating substantial growth potential.

Dominant Regions, Countries, or Segments in Europe Managed Services Market

The United Kingdom, Germany, and France represent the largest national markets within Europe, driven by robust digital infrastructure, high technology adoption rates, and substantial IT spending by large enterprises and government agencies. The Large Enterprises segment shows the highest adoption rate and expenditure, largely driven by their need for sophisticated IT infrastructure. Within end-user verticals, BFSI (Banking, Financial Services, and Insurance) demonstrates a significant demand for managed security and data center services, due to stringent regulatory compliance and the protection of sensitive data. The Cloud deployment model is rapidly gaining traction, surpassing on-premise solutions in growth rate, reflecting the advantages of scalability, cost-efficiency, and accessibility. The Managed Security segment is experiencing strong growth due to heightened cybersecurity threats.

- Key Drivers: Strong digital infrastructure, high IT spending, government initiatives, stringent regulatory compliance, and industry-specific needs.

- Dominance Factors: Market size, growth rate, technology adoption, regulatory landscape, and the presence of major players.

- Growth Potential: Significant untapped potential remains within the SME segment and in emerging technologies like AI-powered managed services.

Europe Managed Services Market Product Landscape

The European managed services market showcases a diverse product landscape, encompassing a wide range of solutions tailored to specific customer needs. Products vary from traditional managed infrastructure and data center services to more sophisticated offerings like managed security, managed communications, and managed mobility solutions. Key innovations include AI-powered automation for improved efficiency and cost optimization, along with enhanced security features to address evolving cyber threats. The unique selling propositions often center on scalability, flexibility, cost-effectiveness, and enhanced security capabilities.

Key Drivers, Barriers & Challenges in Europe Managed Services Market

Key Drivers: The primary growth drivers include increasing digital transformation initiatives across industries, the rising adoption of cloud computing, and the expanding need for robust cybersecurity solutions. Government initiatives promoting digital infrastructure and economic policies supporting technological advancements also play a significant role.

Key Challenges: The market faces challenges from factors like fierce competition among established players and new entrants, the complexity of integrating various managed services, and the potential for skills shortages in specialized areas like cybersecurity. Supply chain disruptions and evolving regulatory frameworks also create uncertainty. Data privacy regulations impact service offerings and compliance costs, while competition from in-house IT teams can limit adoption in certain segments.

Emerging Opportunities in Europe Managed Services Market

Emerging opportunities lie in expanding managed services to SMEs, leveraging AI and machine learning to enhance service efficiency and security, and focusing on niche vertical markets with specialized needs. The growing demand for hybrid cloud solutions and the expansion of 5G infrastructure create further opportunities. Increased adoption of SASE and other Zero Trust security solutions presents a strong avenue for growth.

Growth Accelerators in the Europe Managed Services Market Industry

Strategic partnerships between technology providers and managed service providers (MSPs) are accelerating market growth, enabling broader service offerings and enhanced customer support. Technological breakthroughs in automation, AI, and cybersecurity continuously enhance the value proposition of managed services. Market expansion into untapped segments like SMEs and focus on specific industry verticals presents strong growth potential.

Key Players Shaping the Europe Managed Services Market Market

- IBM Corporation

- Wipro Ltd

- NSC Global Ltd

- Fujitsu Ltd

- HP Development Company LP

- Cisco Systems Inc

- Verizon Communications Inc

- Microsoft Corporation

- Nokia Solutions and Networks

- Tata Consultancy Services Limited

- Deutsche Telekom AG

- Telefonica Europe PL

- Dell Technologies Inc

- AT&T Inc

- Citrix Systems Inc

Notable Milestones in Europe Managed Services Market Sector

- November 2023: Netskope and Telstra International expand their partnership to deliver fully managed SASE services globally, impacting the managed security segment.

- February 2023: Infosys collaborates with ng-voice GmbH to provide managed services for cloud-native network solutions across Europe, impacting the managed network and communications segments.

In-Depth Europe Managed Services Market Market Outlook

The future of the European managed services market looks promising, driven by sustained technological innovation, increasing digital transformation, and the growing demand for robust and secure IT solutions. The market is poised for significant expansion, with opportunities for companies to capitalize on emerging trends like AI-powered automation, cloud-native solutions, and heightened cybersecurity concerns. Strategic partnerships and investments in R&D will play a vital role in shaping the market landscape and driving long-term growth.

Europe Managed Services Market Segmentation

-

1. Deployment

- 1.1. On-premise

- 1.2. Cloud

-

2. Type

- 2.1. Managed Data Center

- 2.2. Managed Security

- 2.3. Managed Communications

- 2.4. Managed Network

- 2.5. Managed Infrastructure

- 2.6. Managed Mobility

-

3. Enterprise Size

- 3.1. Small and Medium Enterprises

- 3.2. Large Enterprises

-

4. End-user Vertical

- 4.1. BFSI

- 4.2. Manufacturing

- 4.3. Healthcare

- 4.4. Retail

- 4.5. Other End-user Verticals

Europe Managed Services Market Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Managed Services Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 13.94% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Shift to Hybrid IT; Improved Cost and Operational Efficiency

- 3.3. Market Restrains

- 3.3.1. Integration and Regulatory Issues and Reliability Concerns

- 3.4. Market Trends

- 3.4.1. Cloud segment is expected to grow at a higher pace

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Europe Managed Services Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Deployment

- 5.1.1. On-premise

- 5.1.2. Cloud

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Managed Data Center

- 5.2.2. Managed Security

- 5.2.3. Managed Communications

- 5.2.4. Managed Network

- 5.2.5. Managed Infrastructure

- 5.2.6. Managed Mobility

- 5.3. Market Analysis, Insights and Forecast - by Enterprise Size

- 5.3.1. Small and Medium Enterprises

- 5.3.2. Large Enterprises

- 5.4. Market Analysis, Insights and Forecast - by End-user Vertical

- 5.4.1. BFSI

- 5.4.2. Manufacturing

- 5.4.3. Healthcare

- 5.4.4. Retail

- 5.4.5. Other End-user Verticals

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Deployment

- 6. Germany Europe Managed Services Market Analysis, Insights and Forecast, 2019-2031

- 7. France Europe Managed Services Market Analysis, Insights and Forecast, 2019-2031

- 8. Italy Europe Managed Services Market Analysis, Insights and Forecast, 2019-2031

- 9. United Kingdom Europe Managed Services Market Analysis, Insights and Forecast, 2019-2031

- 10. Netherlands Europe Managed Services Market Analysis, Insights and Forecast, 2019-2031

- 11. Sweden Europe Managed Services Market Analysis, Insights and Forecast, 2019-2031

- 12. Rest of Europe Europe Managed Services Market Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 IBM Corporation

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 Wipro Ltd

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 NSC Global Ltd

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 Fujitsu Ltd

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 HP Development Company LP

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 Cisco Systems Inc

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 Verizon Communications Inc

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 Microsoft Corporation

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 Nokia Solutions and Networks

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.10 Tata Consultancy Services Limited

- 13.2.10.1. Overview

- 13.2.10.2. Products

- 13.2.10.3. SWOT Analysis

- 13.2.10.4. Recent Developments

- 13.2.10.5. Financials (Based on Availability)

- 13.2.11 Deutsche Telekom AG

- 13.2.11.1. Overview

- 13.2.11.2. Products

- 13.2.11.3. SWOT Analysis

- 13.2.11.4. Recent Developments

- 13.2.11.5. Financials (Based on Availability)

- 13.2.12 Telefonica Europe PL

- 13.2.12.1. Overview

- 13.2.12.2. Products

- 13.2.12.3. SWOT Analysis

- 13.2.12.4. Recent Developments

- 13.2.12.5. Financials (Based on Availability)

- 13.2.13 Dell Technologies Inc

- 13.2.13.1. Overview

- 13.2.13.2. Products

- 13.2.13.3. SWOT Analysis

- 13.2.13.4. Recent Developments

- 13.2.13.5. Financials (Based on Availability)

- 13.2.14 AT&T Inc

- 13.2.14.1. Overview

- 13.2.14.2. Products

- 13.2.14.3. SWOT Analysis

- 13.2.14.4. Recent Developments

- 13.2.14.5. Financials (Based on Availability)

- 13.2.15 Citrix Systems Inc

- 13.2.15.1. Overview

- 13.2.15.2. Products

- 13.2.15.3. SWOT Analysis

- 13.2.15.4. Recent Developments

- 13.2.15.5. Financials (Based on Availability)

- 13.2.1 IBM Corporation

List of Figures

- Figure 1: Europe Managed Services Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Europe Managed Services Market Share (%) by Company 2024

List of Tables

- Table 1: Europe Managed Services Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Europe Managed Services Market Revenue Million Forecast, by Deployment 2019 & 2032

- Table 3: Europe Managed Services Market Revenue Million Forecast, by Type 2019 & 2032

- Table 4: Europe Managed Services Market Revenue Million Forecast, by Enterprise Size 2019 & 2032

- Table 5: Europe Managed Services Market Revenue Million Forecast, by End-user Vertical 2019 & 2032

- Table 6: Europe Managed Services Market Revenue Million Forecast, by Region 2019 & 2032

- Table 7: Europe Managed Services Market Revenue Million Forecast, by Country 2019 & 2032

- Table 8: Germany Europe Managed Services Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: France Europe Managed Services Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Italy Europe Managed Services Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: United Kingdom Europe Managed Services Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Netherlands Europe Managed Services Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Sweden Europe Managed Services Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Rest of Europe Europe Managed Services Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Europe Managed Services Market Revenue Million Forecast, by Deployment 2019 & 2032

- Table 16: Europe Managed Services Market Revenue Million Forecast, by Type 2019 & 2032

- Table 17: Europe Managed Services Market Revenue Million Forecast, by Enterprise Size 2019 & 2032

- Table 18: Europe Managed Services Market Revenue Million Forecast, by End-user Vertical 2019 & 2032

- Table 19: Europe Managed Services Market Revenue Million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Europe Managed Services Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Germany Europe Managed Services Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: France Europe Managed Services Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Italy Europe Managed Services Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Spain Europe Managed Services Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: Netherlands Europe Managed Services Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Belgium Europe Managed Services Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 27: Sweden Europe Managed Services Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: Norway Europe Managed Services Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 29: Poland Europe Managed Services Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 30: Denmark Europe Managed Services Market Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Managed Services Market?

The projected CAGR is approximately 13.94%.

2. Which companies are prominent players in the Europe Managed Services Market?

Key companies in the market include IBM Corporation, Wipro Ltd, NSC Global Ltd, Fujitsu Ltd, HP Development Company LP, Cisco Systems Inc, Verizon Communications Inc, Microsoft Corporation, Nokia Solutions and Networks, Tata Consultancy Services Limited, Deutsche Telekom AG, Telefonica Europe PL, Dell Technologies Inc, AT&T Inc, Citrix Systems Inc.

3. What are the main segments of the Europe Managed Services Market?

The market segments include Deployment, Type, Enterprise Size, End-user Vertical.

4. Can you provide details about the market size?

The market size is estimated to be USD 52.09 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Shift to Hybrid IT; Improved Cost and Operational Efficiency.

6. What are the notable trends driving market growth?

Cloud segment is expected to grow at a higher pace.

7. Are there any restraints impacting market growth?

Integration and Regulatory Issues and Reliability Concerns.

8. Can you provide examples of recent developments in the market?

November 2023: Netskope, a player in Secure Access Service Edge (SASE), and Telstra International, the global arm of telecommunications and technology company Telstra, today announced the expansion of their partnership to enable Telstra to deliver fully managed Netskope cloud-native Secure Access Service Edge (SASE) —including Zero Trust Network Access (ZTNA) services—to organizations globally. Customers worldwide use Telstra's managed security services to help address the changing needs of the digital workplace and mitigate the ever-evolving cyber threats landscape.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Managed Services Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Managed Services Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Managed Services Market?

To stay informed about further developments, trends, and reports in the Europe Managed Services Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence