Key Insights

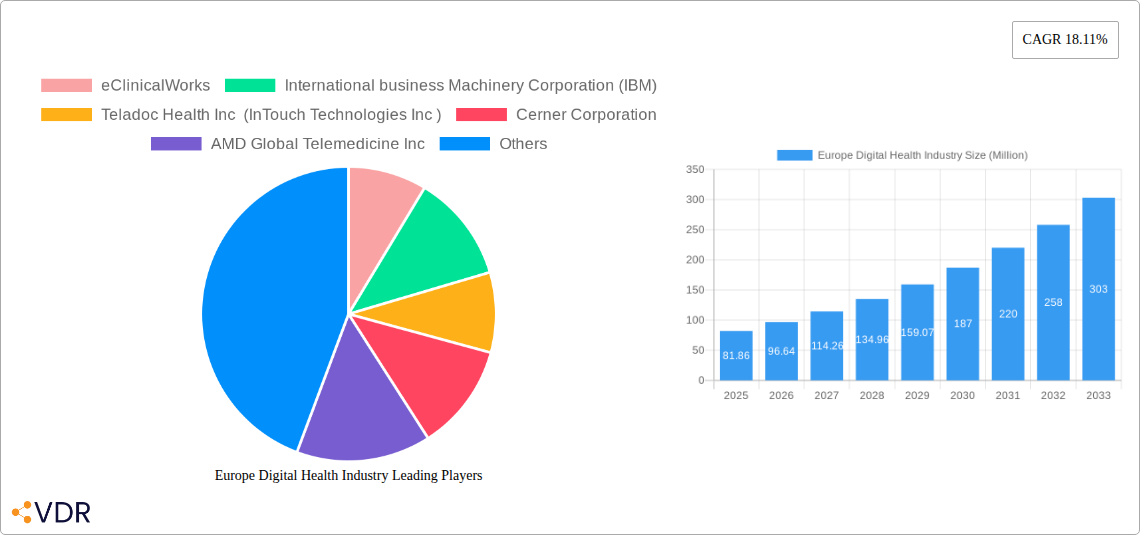

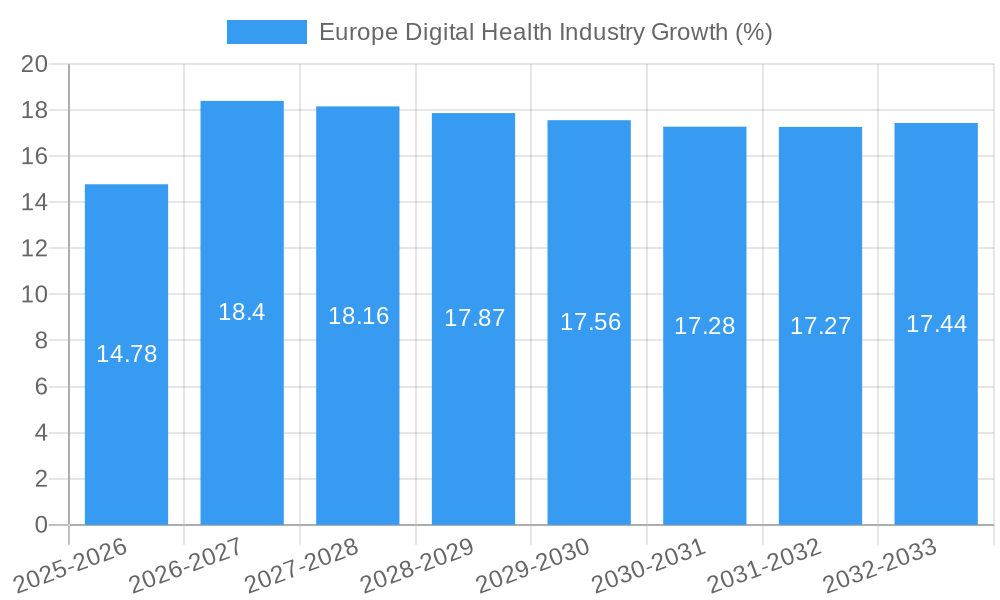

The European digital health market, valued at €81.86 million in 2025, is experiencing robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of 18.11% from 2025 to 2033. This surge is driven by several key factors. Firstly, increasing adoption of telemedicine and mHealth solutions addresses the growing demand for accessible and affordable healthcare, particularly in regions with limited access to traditional medical facilities. Secondly, a rising prevalence of chronic diseases necessitates remote patient monitoring and personalized healthcare management, fueling demand for digital health platforms and applications. Furthermore, supportive government initiatives and investments in digital health infrastructure across major European nations (Germany, France, UK, etc.) are accelerating market expansion. The market is segmented across various components (hardware, software, other), technologies (telehealth, mHealth), applications (health analytics, digital health systems), and delivery modes (on-premise, cloud-based). The competitive landscape comprises established players like IBM, Philips, and McKesson, alongside specialized digital health companies such as eClinicalWorks and Teladoc Health, all vying for market share through innovation and strategic partnerships.

The European digital health market's growth trajectory is expected to remain strong throughout the forecast period. Continued technological advancements in areas such as AI-powered diagnostics, wearable health trackers, and big data analytics will further enhance the capabilities of digital health solutions. However, challenges remain, including data security and privacy concerns, regulatory hurdles in different European countries, and the need for robust digital literacy among healthcare providers and patients. Addressing these challenges will be crucial to fully realizing the market's potential and ensuring widespread adoption of digital health technologies across Europe, benefiting both patients and healthcare systems. The growth will be particularly pronounced in countries with well-established healthcare IT infrastructures and supportive regulatory environments.

Europe Digital Health Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the burgeoning Europe Digital Health Industry, offering invaluable insights for industry professionals, investors, and strategists. Covering the period 2019-2033, with a base year of 2025 and a forecast period of 2025-2033, this report meticulously examines market dynamics, growth trends, and key players shaping the future of healthcare in Europe. We leverage advanced analytical methodologies to deliver precise market sizing and forecasts, allowing for informed decision-making in this rapidly evolving sector. The report incorporates key segments including Hardware, Software, and Other Components within the Component parent market and Tele-healthcare, Mobile Health (mHealth) and Health Analytics within the Technology parent market, along with various delivery modes.

Europe Digital Health Industry Market Dynamics & Structure

The European digital health market is characterized by moderate concentration, with several large players alongside numerous smaller, specialized firms. Technological innovation, driven by advancements in AI, IoT, and cloud computing, is a primary growth driver. Stringent regulatory frameworks, including GDPR and national health data protection laws, shape market access and data handling practices. Competitive substitutes, such as traditional healthcare delivery models, exert pressure on market adoption. The end-user demographic is diverse, encompassing hospitals, clinics, patients, and healthcare providers. M&A activity has been significant, with deal volumes increasing in recent years (xx deals in 2024, expected xx in 2025).

- Market Concentration: Moderately concentrated, with a Herfindahl-Hirschman Index (HHI) of xx in 2024.

- Technological Innovation: AI-powered diagnostics, remote patient monitoring, and blockchain-based data security are key drivers.

- Regulatory Landscape: GDPR and national regulations influence data privacy and security measures.

- Competitive Substitutes: Traditional healthcare models and legacy systems pose competition.

- End-User Demographics: Hospitals, clinics, patients, and healthcare providers.

- M&A Trends: Increasing deal volumes, reflecting market consolidation and expansion strategies.

Europe Digital Health Industry Growth Trends & Insights

The European digital health market experienced significant growth during the historical period (2019-2024), expanding from €xx million in 2019 to €xx million in 2024, representing a CAGR of xx%. This growth is fueled by increasing healthcare expenditure, rising adoption of digital technologies by healthcare providers, and growing patient demand for convenient and accessible healthcare solutions. Technological disruptions, such as the proliferation of mobile health apps and the adoption of telemedicine, have accelerated market expansion. Consumer behavior shifts, including increasing health awareness and comfort with digital platforms, further support market growth. Market penetration is projected to reach xx% by 2033, driven by government initiatives and increased funding. The forecast period (2025-2033) predicts robust growth, reaching €xx million by 2033, with a CAGR of xx%.

Dominant Regions, Countries, or Segments in Europe Digital Health Industry

The UK and Germany currently hold the largest market share within Europe, driven by robust healthcare infrastructure, substantial government investments, and a high density of technology companies. The Cloud-based Delivery mode is experiencing the fastest growth, fuelled by scalability, cost-effectiveness, and enhanced accessibility. Within the Component segment, Software dominates, reflecting the increasing importance of digital health applications and data analytics. Mobile Health (mHealth) within the Technology segment shows rapid expansion due to smartphone penetration and user-friendly health monitoring tools.

- Key Drivers:

- UK & Germany: Strong healthcare infrastructure, government initiatives, and technological hubs.

- Cloud-based Delivery: Scalability, cost-effectiveness, and remote access capabilities.

- Software: Demand for advanced analytics, data-driven decision making, and digital applications.

- Mobile Health (mHealth): Smartphone penetration, user-friendly apps, and convenient health monitoring.

Europe Digital Health Industry Product Landscape

The digital health product landscape is marked by innovation in wearable sensors, AI-powered diagnostic tools, and personalized health management applications. Products focus on improved patient engagement, remote monitoring capabilities, and data-driven insights for healthcare providers. Key features include seamless integration with existing healthcare systems, advanced security protocols, and user-friendly interfaces. Technological advancements in machine learning and cloud computing drive product enhancements, enabling predictive analytics and personalized treatment plans.

Key Drivers, Barriers & Challenges in Europe Digital Health Industry

Key Drivers: Increasing healthcare expenditure, rising adoption of digital technologies, government initiatives promoting digital health, and growing patient demand for convenient healthcare services. For example, the increasing prevalence of chronic diseases has amplified demand for remote monitoring solutions.

Key Challenges: Data security and privacy concerns, regulatory hurdles (e.g., varying regulations across European countries), interoperability issues between different systems, and high initial investment costs for healthcare providers can hinder market growth. Data breaches, for instance, could erode patient trust and impact market adoption.

Emerging Opportunities in Europe Digital Health Industry

Untapped markets in rural areas, the expansion of telehealth services to underserved populations, and the development of innovative applications in areas such as mental health and preventive care offer significant opportunities. Growing consumer preferences for personalized medicine and proactive health management create new market segments. The integration of AI and blockchain technologies further presents potential for enhancing security and data management.

Growth Accelerators in the Europe Digital Health Industry

Technological breakthroughs in artificial intelligence, the Internet of Things (IoT), and big data analytics are driving innovation and market expansion. Strategic partnerships between healthcare providers, technology companies, and government agencies are crucial for successful implementation of digital health initiatives. Market expansion into new geographic areas and the development of customized solutions for specific healthcare needs further contribute to growth acceleration.

Key Players Shaping the Europe Digital Health Industry Market

- eClinicalWorks

- International Business Machines Corporation (IBM)

- Teladoc Health Inc (InTouch Technologies Inc)

- Cerner Corporation

- AMD Global Telemedicine Inc

- Cisco Systems

- Koninklijke Philips NV

- Allscripts Healthcare Solutions Inc

- McKesson Corporation

- Aerotel Medical Systems (1998) Ltd

Notable Milestones in Europe Digital Health Industry Sector

- April 2022: University College London (UCL) and Amazon Web Services (AWS) launched a digital innovation center, accelerating digital transformation in healthcare and education.

- July 2022: Smith+Nephew launched the Wound Compass Clinical Support App in the UK, improving wound care management.

In-Depth Europe Digital Health Industry Market Outlook

The European digital health market is poised for continued robust growth, driven by technological advancements, increasing healthcare spending, and supportive government policies. Strategic partnerships, expansion into underserved markets, and the development of innovative solutions will be key to unlocking the market’s full potential. The focus on personalized medicine, preventative care, and improved patient engagement will shape future market dynamics, creating lucrative opportunities for both established players and new entrants.

Europe Digital Health Industry Segmentation

-

1. Component

- 1.1. Hardware

- 1.2. Software

- 1.3. Other Components

-

2. Technology

- 2.1. Tele-healthcare

-

2.2. Mobile Health (mHealth)

- 2.2.1. Wearables

- 2.2.2. Apps

- 2.3. Health Analytics

-

2.4. Digital Health Systems

- 2.4.1. E-Health Records

- 2.4.2. E-Prescription

-

3. Mode of Delivery

- 3.1. On-premise Delivery

- 3.2. Cloud-based Delivery

Europe Digital Health Industry Segmentation By Geography

- 1. Germany

- 2. United Kingdom

- 3. France

- 4. Italy

- 5. Spain

- 6. Rest of Europe

Europe Digital Health Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 18.11% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Rising Adoption of Digital Health Services and Government Initiatives; Technological Advancements in the Area of Digital Health; Increasing Demand of Remote Patient Monitoring

- 3.3. Market Restrains

- 3.3.1. Cybersecurity Concerns for Patient Data; High Deployment and Maintenance Expenditure

- 3.4. Market Trends

- 3.4.1. The Telehealthcare Segment is Expected to Witness Growth Over the Forecast Period

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Europe Digital Health Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Component

- 5.1.1. Hardware

- 5.1.2. Software

- 5.1.3. Other Components

- 5.2. Market Analysis, Insights and Forecast - by Technology

- 5.2.1. Tele-healthcare

- 5.2.2. Mobile Health (mHealth)

- 5.2.2.1. Wearables

- 5.2.2.2. Apps

- 5.2.3. Health Analytics

- 5.2.4. Digital Health Systems

- 5.2.4.1. E-Health Records

- 5.2.4.2. E-Prescription

- 5.3. Market Analysis, Insights and Forecast - by Mode of Delivery

- 5.3.1. On-premise Delivery

- 5.3.2. Cloud-based Delivery

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Germany

- 5.4.2. United Kingdom

- 5.4.3. France

- 5.4.4. Italy

- 5.4.5. Spain

- 5.4.6. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Component

- 6. Germany Europe Digital Health Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Component

- 6.1.1. Hardware

- 6.1.2. Software

- 6.1.3. Other Components

- 6.2. Market Analysis, Insights and Forecast - by Technology

- 6.2.1. Tele-healthcare

- 6.2.2. Mobile Health (mHealth)

- 6.2.2.1. Wearables

- 6.2.2.2. Apps

- 6.2.3. Health Analytics

- 6.2.4. Digital Health Systems

- 6.2.4.1. E-Health Records

- 6.2.4.2. E-Prescription

- 6.3. Market Analysis, Insights and Forecast - by Mode of Delivery

- 6.3.1. On-premise Delivery

- 6.3.2. Cloud-based Delivery

- 6.1. Market Analysis, Insights and Forecast - by Component

- 7. United Kingdom Europe Digital Health Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Component

- 7.1.1. Hardware

- 7.1.2. Software

- 7.1.3. Other Components

- 7.2. Market Analysis, Insights and Forecast - by Technology

- 7.2.1. Tele-healthcare

- 7.2.2. Mobile Health (mHealth)

- 7.2.2.1. Wearables

- 7.2.2.2. Apps

- 7.2.3. Health Analytics

- 7.2.4. Digital Health Systems

- 7.2.4.1. E-Health Records

- 7.2.4.2. E-Prescription

- 7.3. Market Analysis, Insights and Forecast - by Mode of Delivery

- 7.3.1. On-premise Delivery

- 7.3.2. Cloud-based Delivery

- 7.1. Market Analysis, Insights and Forecast - by Component

- 8. France Europe Digital Health Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Component

- 8.1.1. Hardware

- 8.1.2. Software

- 8.1.3. Other Components

- 8.2. Market Analysis, Insights and Forecast - by Technology

- 8.2.1. Tele-healthcare

- 8.2.2. Mobile Health (mHealth)

- 8.2.2.1. Wearables

- 8.2.2.2. Apps

- 8.2.3. Health Analytics

- 8.2.4. Digital Health Systems

- 8.2.4.1. E-Health Records

- 8.2.4.2. E-Prescription

- 8.3. Market Analysis, Insights and Forecast - by Mode of Delivery

- 8.3.1. On-premise Delivery

- 8.3.2. Cloud-based Delivery

- 8.1. Market Analysis, Insights and Forecast - by Component

- 9. Italy Europe Digital Health Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Component

- 9.1.1. Hardware

- 9.1.2. Software

- 9.1.3. Other Components

- 9.2. Market Analysis, Insights and Forecast - by Technology

- 9.2.1. Tele-healthcare

- 9.2.2. Mobile Health (mHealth)

- 9.2.2.1. Wearables

- 9.2.2.2. Apps

- 9.2.3. Health Analytics

- 9.2.4. Digital Health Systems

- 9.2.4.1. E-Health Records

- 9.2.4.2. E-Prescription

- 9.3. Market Analysis, Insights and Forecast - by Mode of Delivery

- 9.3.1. On-premise Delivery

- 9.3.2. Cloud-based Delivery

- 9.1. Market Analysis, Insights and Forecast - by Component

- 10. Spain Europe Digital Health Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Component

- 10.1.1. Hardware

- 10.1.2. Software

- 10.1.3. Other Components

- 10.2. Market Analysis, Insights and Forecast - by Technology

- 10.2.1. Tele-healthcare

- 10.2.2. Mobile Health (mHealth)

- 10.2.2.1. Wearables

- 10.2.2.2. Apps

- 10.2.3. Health Analytics

- 10.2.4. Digital Health Systems

- 10.2.4.1. E-Health Records

- 10.2.4.2. E-Prescription

- 10.3. Market Analysis, Insights and Forecast - by Mode of Delivery

- 10.3.1. On-premise Delivery

- 10.3.2. Cloud-based Delivery

- 10.1. Market Analysis, Insights and Forecast - by Component

- 11. Rest of Europe Europe Digital Health Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - by Component

- 11.1.1. Hardware

- 11.1.2. Software

- 11.1.3. Other Components

- 11.2. Market Analysis, Insights and Forecast - by Technology

- 11.2.1. Tele-healthcare

- 11.2.2. Mobile Health (mHealth)

- 11.2.2.1. Wearables

- 11.2.2.2. Apps

- 11.2.3. Health Analytics

- 11.2.4. Digital Health Systems

- 11.2.4.1. E-Health Records

- 11.2.4.2. E-Prescription

- 11.3. Market Analysis, Insights and Forecast - by Mode of Delivery

- 11.3.1. On-premise Delivery

- 11.3.2. Cloud-based Delivery

- 11.1. Market Analysis, Insights and Forecast - by Component

- 12. Germany Europe Digital Health Industry Analysis, Insights and Forecast, 2019-2031

- 13. France Europe Digital Health Industry Analysis, Insights and Forecast, 2019-2031

- 14. Italy Europe Digital Health Industry Analysis, Insights and Forecast, 2019-2031

- 15. United Kingdom Europe Digital Health Industry Analysis, Insights and Forecast, 2019-2031

- 16. Netherlands Europe Digital Health Industry Analysis, Insights and Forecast, 2019-2031

- 17. Sweden Europe Digital Health Industry Analysis, Insights and Forecast, 2019-2031

- 18. Rest of Europe Europe Digital Health Industry Analysis, Insights and Forecast, 2019-2031

- 19. Competitive Analysis

- 19.1. Market Share Analysis 2024

- 19.2. Company Profiles

- 19.2.1 eClinicalWorks

- 19.2.1.1. Overview

- 19.2.1.2. Products

- 19.2.1.3. SWOT Analysis

- 19.2.1.4. Recent Developments

- 19.2.1.5. Financials (Based on Availability)

- 19.2.2 International business Machinery Corporation (IBM)

- 19.2.2.1. Overview

- 19.2.2.2. Products

- 19.2.2.3. SWOT Analysis

- 19.2.2.4. Recent Developments

- 19.2.2.5. Financials (Based on Availability)

- 19.2.3 Teladoc Health Inc (InTouch Technologies Inc )

- 19.2.3.1. Overview

- 19.2.3.2. Products

- 19.2.3.3. SWOT Analysis

- 19.2.3.4. Recent Developments

- 19.2.3.5. Financials (Based on Availability)

- 19.2.4 Cerner Corporation

- 19.2.4.1. Overview

- 19.2.4.2. Products

- 19.2.4.3. SWOT Analysis

- 19.2.4.4. Recent Developments

- 19.2.4.5. Financials (Based on Availability)

- 19.2.5 AMD Global Telemedicine Inc

- 19.2.5.1. Overview

- 19.2.5.2. Products

- 19.2.5.3. SWOT Analysis

- 19.2.5.4. Recent Developments

- 19.2.5.5. Financials (Based on Availability)

- 19.2.6 Cisco Systems

- 19.2.6.1. Overview

- 19.2.6.2. Products

- 19.2.6.3. SWOT Analysis

- 19.2.6.4. Recent Developments

- 19.2.6.5. Financials (Based on Availability)

- 19.2.7 Koninklijke Philips NV

- 19.2.7.1. Overview

- 19.2.7.2. Products

- 19.2.7.3. SWOT Analysis

- 19.2.7.4. Recent Developments

- 19.2.7.5. Financials (Based on Availability)

- 19.2.8 Allscripts Healthcare Solutions Inc

- 19.2.8.1. Overview

- 19.2.8.2. Products

- 19.2.8.3. SWOT Analysis

- 19.2.8.4. Recent Developments

- 19.2.8.5. Financials (Based on Availability)

- 19.2.9 McKesson Corporation

- 19.2.9.1. Overview

- 19.2.9.2. Products

- 19.2.9.3. SWOT Analysis

- 19.2.9.4. Recent Developments

- 19.2.9.5. Financials (Based on Availability)

- 19.2.10 Aerotel Medical Systems (1998) Ltd

- 19.2.10.1. Overview

- 19.2.10.2. Products

- 19.2.10.3. SWOT Analysis

- 19.2.10.4. Recent Developments

- 19.2.10.5. Financials (Based on Availability)

- 19.2.1 eClinicalWorks

List of Figures

- Figure 1: Europe Digital Health Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Europe Digital Health Industry Share (%) by Company 2024

List of Tables

- Table 1: Europe Digital Health Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Europe Digital Health Industry Volume K Unit Forecast, by Region 2019 & 2032

- Table 3: Europe Digital Health Industry Revenue Million Forecast, by Component 2019 & 2032

- Table 4: Europe Digital Health Industry Volume K Unit Forecast, by Component 2019 & 2032

- Table 5: Europe Digital Health Industry Revenue Million Forecast, by Technology 2019 & 2032

- Table 6: Europe Digital Health Industry Volume K Unit Forecast, by Technology 2019 & 2032

- Table 7: Europe Digital Health Industry Revenue Million Forecast, by Mode of Delivery 2019 & 2032

- Table 8: Europe Digital Health Industry Volume K Unit Forecast, by Mode of Delivery 2019 & 2032

- Table 9: Europe Digital Health Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 10: Europe Digital Health Industry Volume K Unit Forecast, by Region 2019 & 2032

- Table 11: Europe Digital Health Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 12: Europe Digital Health Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 13: Germany Europe Digital Health Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Germany Europe Digital Health Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 15: France Europe Digital Health Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: France Europe Digital Health Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 17: Italy Europe Digital Health Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Italy Europe Digital Health Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 19: United Kingdom Europe Digital Health Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: United Kingdom Europe Digital Health Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 21: Netherlands Europe Digital Health Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Netherlands Europe Digital Health Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 23: Sweden Europe Digital Health Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Sweden Europe Digital Health Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 25: Rest of Europe Europe Digital Health Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Rest of Europe Europe Digital Health Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 27: Europe Digital Health Industry Revenue Million Forecast, by Component 2019 & 2032

- Table 28: Europe Digital Health Industry Volume K Unit Forecast, by Component 2019 & 2032

- Table 29: Europe Digital Health Industry Revenue Million Forecast, by Technology 2019 & 2032

- Table 30: Europe Digital Health Industry Volume K Unit Forecast, by Technology 2019 & 2032

- Table 31: Europe Digital Health Industry Revenue Million Forecast, by Mode of Delivery 2019 & 2032

- Table 32: Europe Digital Health Industry Volume K Unit Forecast, by Mode of Delivery 2019 & 2032

- Table 33: Europe Digital Health Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 34: Europe Digital Health Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 35: Europe Digital Health Industry Revenue Million Forecast, by Component 2019 & 2032

- Table 36: Europe Digital Health Industry Volume K Unit Forecast, by Component 2019 & 2032

- Table 37: Europe Digital Health Industry Revenue Million Forecast, by Technology 2019 & 2032

- Table 38: Europe Digital Health Industry Volume K Unit Forecast, by Technology 2019 & 2032

- Table 39: Europe Digital Health Industry Revenue Million Forecast, by Mode of Delivery 2019 & 2032

- Table 40: Europe Digital Health Industry Volume K Unit Forecast, by Mode of Delivery 2019 & 2032

- Table 41: Europe Digital Health Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 42: Europe Digital Health Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 43: Europe Digital Health Industry Revenue Million Forecast, by Component 2019 & 2032

- Table 44: Europe Digital Health Industry Volume K Unit Forecast, by Component 2019 & 2032

- Table 45: Europe Digital Health Industry Revenue Million Forecast, by Technology 2019 & 2032

- Table 46: Europe Digital Health Industry Volume K Unit Forecast, by Technology 2019 & 2032

- Table 47: Europe Digital Health Industry Revenue Million Forecast, by Mode of Delivery 2019 & 2032

- Table 48: Europe Digital Health Industry Volume K Unit Forecast, by Mode of Delivery 2019 & 2032

- Table 49: Europe Digital Health Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 50: Europe Digital Health Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 51: Europe Digital Health Industry Revenue Million Forecast, by Component 2019 & 2032

- Table 52: Europe Digital Health Industry Volume K Unit Forecast, by Component 2019 & 2032

- Table 53: Europe Digital Health Industry Revenue Million Forecast, by Technology 2019 & 2032

- Table 54: Europe Digital Health Industry Volume K Unit Forecast, by Technology 2019 & 2032

- Table 55: Europe Digital Health Industry Revenue Million Forecast, by Mode of Delivery 2019 & 2032

- Table 56: Europe Digital Health Industry Volume K Unit Forecast, by Mode of Delivery 2019 & 2032

- Table 57: Europe Digital Health Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 58: Europe Digital Health Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 59: Europe Digital Health Industry Revenue Million Forecast, by Component 2019 & 2032

- Table 60: Europe Digital Health Industry Volume K Unit Forecast, by Component 2019 & 2032

- Table 61: Europe Digital Health Industry Revenue Million Forecast, by Technology 2019 & 2032

- Table 62: Europe Digital Health Industry Volume K Unit Forecast, by Technology 2019 & 2032

- Table 63: Europe Digital Health Industry Revenue Million Forecast, by Mode of Delivery 2019 & 2032

- Table 64: Europe Digital Health Industry Volume K Unit Forecast, by Mode of Delivery 2019 & 2032

- Table 65: Europe Digital Health Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 66: Europe Digital Health Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 67: Europe Digital Health Industry Revenue Million Forecast, by Component 2019 & 2032

- Table 68: Europe Digital Health Industry Volume K Unit Forecast, by Component 2019 & 2032

- Table 69: Europe Digital Health Industry Revenue Million Forecast, by Technology 2019 & 2032

- Table 70: Europe Digital Health Industry Volume K Unit Forecast, by Technology 2019 & 2032

- Table 71: Europe Digital Health Industry Revenue Million Forecast, by Mode of Delivery 2019 & 2032

- Table 72: Europe Digital Health Industry Volume K Unit Forecast, by Mode of Delivery 2019 & 2032

- Table 73: Europe Digital Health Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 74: Europe Digital Health Industry Volume K Unit Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Digital Health Industry?

The projected CAGR is approximately 18.11%.

2. Which companies are prominent players in the Europe Digital Health Industry?

Key companies in the market include eClinicalWorks, International business Machinery Corporation (IBM), Teladoc Health Inc (InTouch Technologies Inc ), Cerner Corporation, AMD Global Telemedicine Inc, Cisco Systems, Koninklijke Philips NV, Allscripts Healthcare Solutions Inc, McKesson Corporation, Aerotel Medical Systems (1998) Ltd.

3. What are the main segments of the Europe Digital Health Industry?

The market segments include Component, Technology, Mode of Delivery.

4. Can you provide details about the market size?

The market size is estimated to be USD 81.86 Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Adoption of Digital Health Services and Government Initiatives; Technological Advancements in the Area of Digital Health; Increasing Demand of Remote Patient Monitoring.

6. What are the notable trends driving market growth?

The Telehealthcare Segment is Expected to Witness Growth Over the Forecast Period.

7. Are there any restraints impacting market growth?

Cybersecurity Concerns for Patient Data; High Deployment and Maintenance Expenditure.

8. Can you provide examples of recent developments in the market?

April 2022: University College London (UCL) and Amazon Web Services (AWS) teamed up to build a digital innovation center at the IDEALondon technology hub. The center will assist healthcare and education organizations to accelerate digital innovation and address global concerns in their fields.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Digital Health Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Digital Health Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Digital Health Industry?

To stay informed about further developments, trends, and reports in the Europe Digital Health Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence