Key Insights

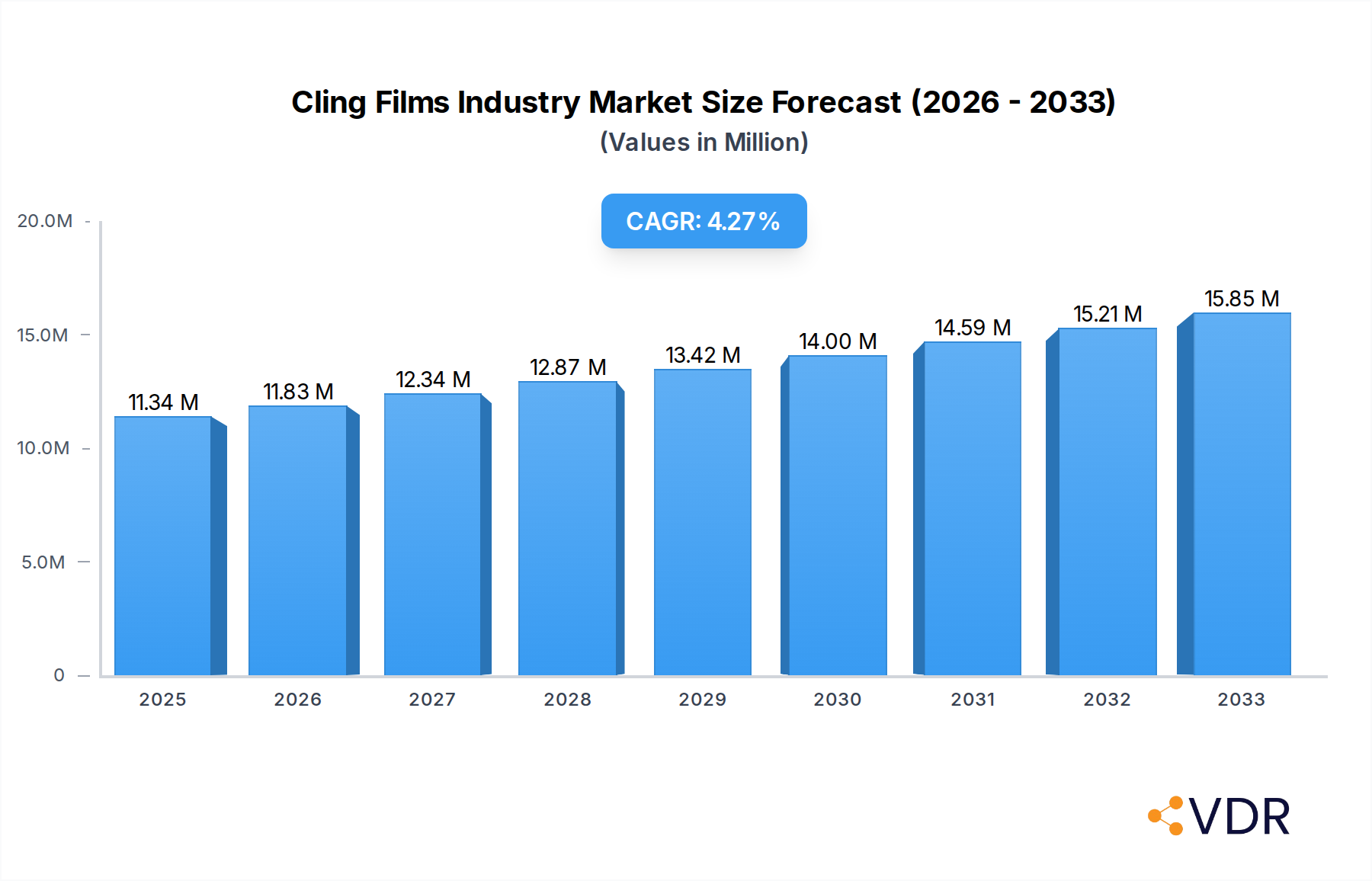

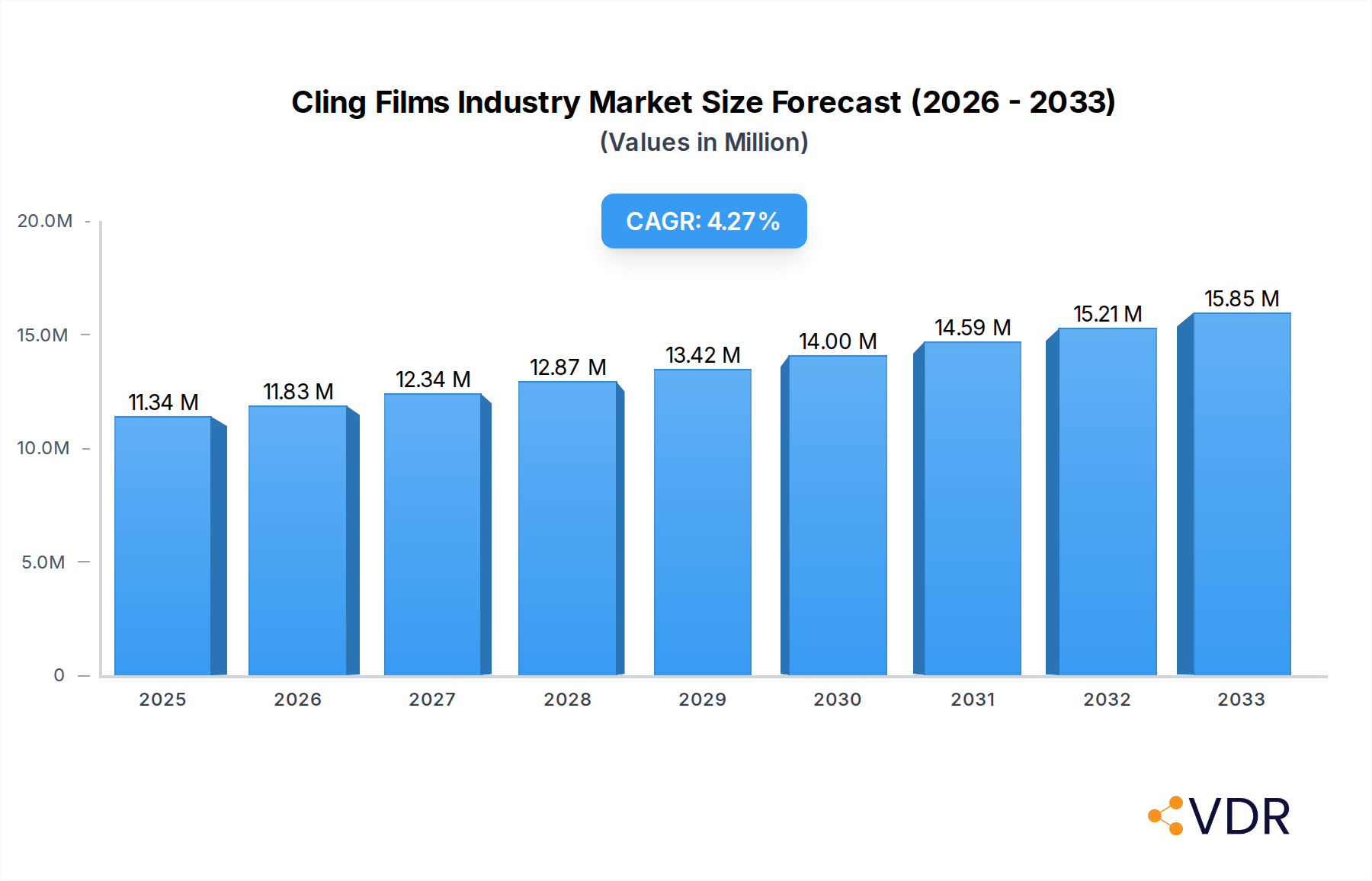

The global cling film market is experiencing robust expansion, projected to reach $11.34 million by 2025, demonstrating a healthy Compound Annual Growth Rate (CAGR) of 4.35% over the forecast period of 2025-2033. This growth is primarily propelled by the escalating demand for convenient and effective food preservation solutions across both domestic and commercial sectors. The increasing consumer awareness regarding food safety and waste reduction further fuels this demand, as cling films offer a reliable barrier against spoilage and contamination. Furthermore, advancements in material science are leading to the development of more sustainable and high-performance cling film variants, including those made from bio-based polymers and recycled content, catering to a growing eco-conscious consumer base. The healthcare sector also presents a significant growth avenue, with cling films being crucial for medical packaging and wound care. Key drivers such as the rising global population, increasing disposable incomes, and the expansion of organized retail channels, especially in emerging economies, are underpinning this positive market trajectory.

Cling Films Industry Market Size (In Million)

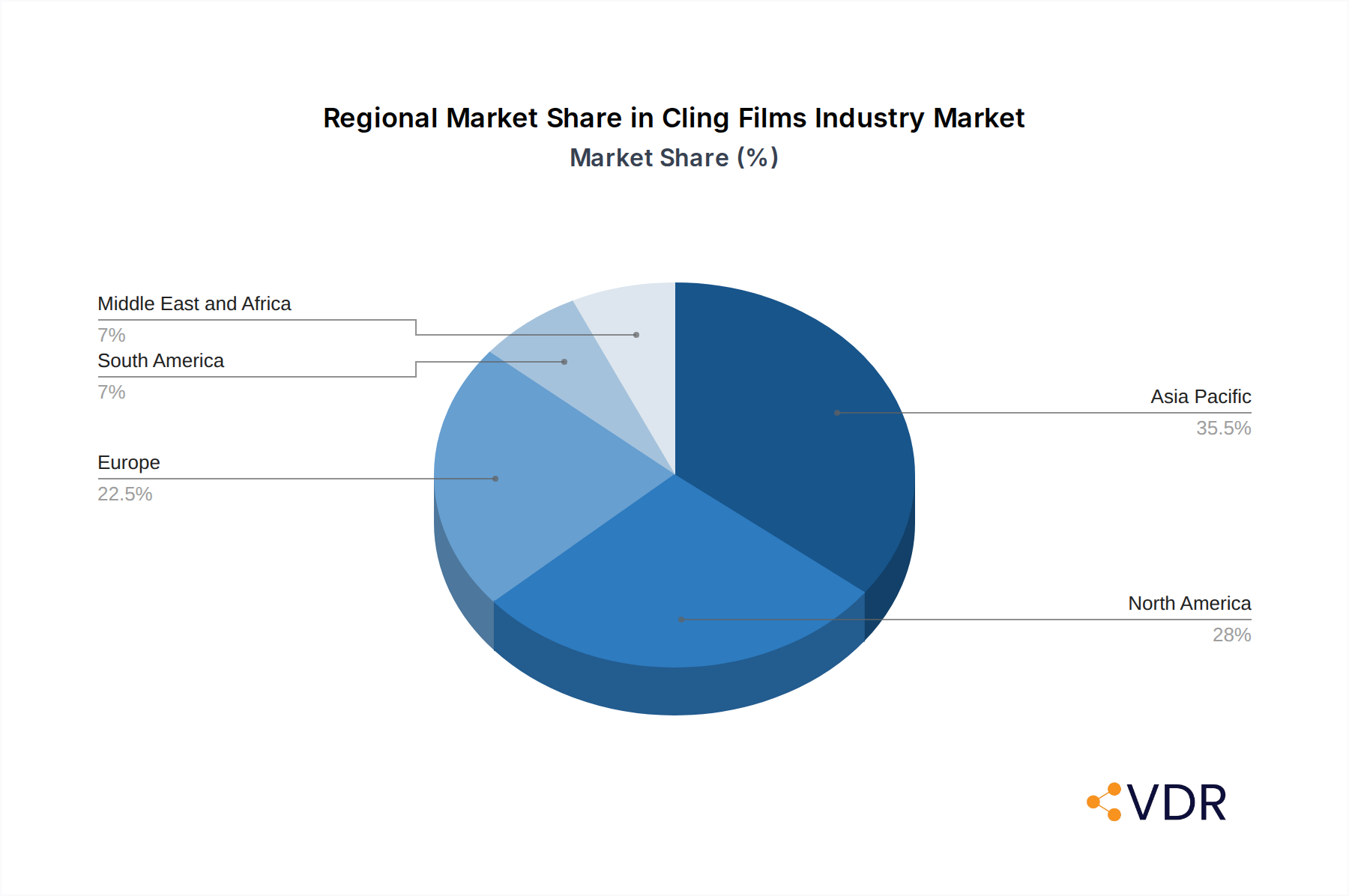

The cling film industry is segmented across various material types, with Polyethylene (PE) and Biaxially Oriented Polypropylene (BOPP) dominating the market due to their excellent barrier properties, flexibility, and cost-effectiveness. In terms of form, cast cling film holds a significant share, attributed to its superior clarity and cling properties, making it ideal for food packaging. The blow cling film segment is also witnessing growth, particularly in industrial applications requiring higher strength. The end-user industry landscape is dominated by the food sector, followed by consumer goods and healthcare, all benefiting from the protective and preserving capabilities of cling films. Geographically, the Asia Pacific region is emerging as a powerhouse, driven by rapid industrialization, a burgeoning middle class, and substantial investments in food processing and packaging infrastructure in countries like China and India. While the market exhibits strong growth potential, challenges such as fluctuating raw material prices and the increasing competition from alternative packaging solutions may pose some restraints. However, ongoing innovation in product development and a focus on sustainability are expected to mitigate these challenges, ensuring sustained market expansion.

Cling Films Industry Company Market Share

Cling Films Industry: Comprehensive Market Analysis & Future Projections (2019–2033)

This in-depth report provides a definitive analysis of the global Cling Films market, offering critical insights into its structure, dynamics, growth trajectories, and future outlook. Covering the period from 2019 to 2033, with a base and estimated year of 2025 and a forecast period of 2025–2033, this report is an essential resource for manufacturers, suppliers, investors, and stakeholders seeking to capitalize on opportunities within this evolving sector. The report presents all values in Million units for clear quantitative understanding.

Cling Films Industry Market Dynamics & Structure

The cling films industry exhibits a moderately consolidated market structure, with leading players like Jindal Poly Films Limited, Amcor plc, and Berry Global Inc. holding significant market shares. Technological innovation remains a key driver, particularly advancements in sustainable materials and barrier properties, pushing the boundaries of what cling films can achieve in terms of shelf-life extension and food safety. Regulatory frameworks, especially concerning plastic waste and recyclability, are increasingly influencing product development and market access, prompting a shift towards eco-friendly solutions. Competitive product substitutes, such as paper-based packaging and reusable containers, present a constant challenge, necessitating continuous innovation and cost-effectiveness in cling film production. End-user demographics, particularly the growing demand for convenient and safe food packaging, play a crucial role in shaping market demand. Mergers and acquisitions (M&A) trends are prevalent as companies seek to expand their product portfolios, geographic reach, and technological capabilities.

- Market Concentration: Moderate, with top players controlling a substantial portion of the market.

- Innovation Drivers: Sustainability, enhanced barrier properties, improved recyclability, and cost-efficiency.

- Regulatory Influence: Growing emphasis on plastic reduction, recycling mandates, and food safety standards.

- Competitive Landscape: Presence of diverse substitutes and continuous innovation pressure.

- M&A Activity: Strategic acquisitions and collaborations aimed at market expansion and technological integration.

Cling Films Industry Growth Trends & Insights

The global cling films market is poised for robust growth, driven by an ever-increasing global population and the escalating demand for packaged food products. The market size is projected to witness a significant expansion from an estimated $XX,XXX Million units in 2025 to $YY,YYY Million units by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of XX.X% during the forecast period. Adoption rates for advanced cling films, especially those with superior barrier properties and sustainable attributes, are rapidly increasing. Technological disruptions are focused on developing biodegradable and compostable cling films, alongside innovations that enhance recyclability and reduce material usage. Consumer behavior shifts are playing a pivotal role, with a growing preference for convenience, extended shelf-life, and food products that minimize waste. The increasing urbanization and the rise of organized retail sectors globally are further contributing to the demand for efficient and protective cling film packaging solutions. Furthermore, the healthcare sector's demand for sterile and reliable packaging for medical supplies and pharmaceuticals is a consistent growth accelerator.

Dominant Regions, Countries, or Segments in Cling Films Industry

The Food end-user industry stands as the dominant segment within the global cling films market, significantly outpacing other sectors in terms of market share and growth potential. This dominance is attributed to the universal need for food preservation, extended shelf-life, and protection against contamination across fresh produce, meats, dairy products, and ready-to-eat meals. The burgeoning global population and the expanding middle class, particularly in developing economies, are fueling an insatiable demand for convenient and safe food packaging solutions, where cling films play a crucial role.

- Asia Pacific is emerging as the leading region, driven by rapid economic development, a massive consumer base, and a growing organized retail sector. Government initiatives promoting food processing and packaging infrastructure further bolster this dominance.

- Polyethylene (PE) based cling films represent the largest material type segment. PE offers excellent flexibility, puncture resistance, and cost-effectiveness, making it a preferred choice for a wide array of food packaging applications. The increasing availability and improved properties of PE variants are sustaining its market leadership.

- Cast Cling Film is the predominant form due to its superior clarity, tackiness, and consistent thickness, which are critical for effective food wrapping and presentation. Its manufacturing process allows for greater control over film properties, catering to specific application needs.

Cling Films Industry Product Landscape

The cling films industry is characterized by a dynamic product landscape driven by relentless innovation. Manufacturers are continuously developing films with enhanced barrier properties, offering superior protection against moisture, oxygen, and odors to extend product shelf-life. Innovations include multi-layer films incorporating advanced polymers and specialized additives to achieve specific performance metrics like puncture resistance and heat sealability. The increasing focus on sustainability has led to the introduction of bio-based, biodegradable, and compostable cling films, alongside formulations with higher recycled content. Unique selling propositions often revolve around achieving a balance between performance, cost-effectiveness, and environmental responsibility, with technological advancements enabling thinner yet stronger films, reducing material consumption.

Key Drivers, Barriers & Challenges in Cling Films Industry

Key Drivers:

- Growing Demand for Packaged Food: An expanding global population and changing lifestyles drive the need for convenient and safe food packaging.

- Shelf-Life Extension: Cling films' ability to preserve food freshness and reduce spoilage is a major economic and environmental advantage.

- Technological Advancements: Development of specialized films with improved barrier properties, recyclability, and sustainability features.

- E-commerce Growth: The expansion of online retail necessitates robust and protective packaging for goods in transit.

Key Barriers & Challenges:

- Environmental Concerns & Regulations: Increasing scrutiny over plastic waste and single-use plastics can lead to stricter regulations and consumer backlash.

- Raw Material Price Volatility: Fluctuations in the prices of petrochemicals, the primary raw materials, can impact production costs and profitability.

- Competition from Alternative Packaging: Substitution by paper-based, compostable, or reusable packaging solutions.

- Recycling Infrastructure Limitations: Inadequate recycling infrastructure in certain regions can hinder the adoption of recyclable cling films.

Emerging Opportunities in Cling Films Industry

The cling films industry is ripe with emerging opportunities, particularly in the realm of sustainable packaging solutions. The growing consumer and regulatory demand for eco-friendly alternatives is spurring innovation in biodegradable, compostable, and bio-based cling films. Untapped markets in developing economies with rapidly growing food processing sectors present significant growth potential. Innovative applications, such as smart cling films that indicate food spoilage or antimicrobial cling films for enhanced food safety, are gaining traction. Furthermore, the increasing focus on circular economy principles is creating opportunities for companies that can develop and implement effective collection and recycling schemes for their cling film products.

Growth Accelerators in the Cling Films Industry Industry

Long-term growth in the cling films industry will be significantly propelled by ongoing technological breakthroughs, such as the development of advanced material science leading to thinner, stronger, and more sustainable cling films. Strategic partnerships between raw material suppliers, film manufacturers, and end-users will foster collaborative innovation and streamline the adoption of new technologies. Market expansion strategies, including entering new geographical territories and tapping into niche applications within the healthcare and industrial sectors, will further accelerate growth. The increasing global focus on food security and waste reduction will continue to underscore the essential role of effective cling film packaging, creating a consistent demand driver.

Key Players Shaping the Cling Films Industry Market

- Jindal Poly Films Limited

- Paragon Films

- Novamont SPA

- Mitsubishi Chemical Corporation

- Intertape Polymer Group

- ADEX SRL

- Nan Ya Plastics Corporation

- Deriblok SpA

- Berry Global Inc

- 3M

- Inteplast Group

- Hipac SPA

- Reynolds Consumer Products

- Technovaa Plastic Industries Pvt Ltd

- Malpack

- Alliance Plastics

- All American Poly

- Amcor plc

- Sigma Plastics Group

- Anchor Packaging LLC

Notable Milestones in Cling Films Industry Sector

- February 2023: Berry Global Group Inc. launched a next-generation version of its proven stretch hood film with a minimum of 30% recycled plastic content, supporting businesses in achieving sustainability objectives and meeting UK/European plastics packaging legislation.

- January 2023: Amcor plc announced the introduction of its new PrimeSeal and DairySeal Recycle-Ready Thermoforming Films for meat and dairy, offering outstanding packaging performance and enhanced packaging circularity. These heat-resistant films (up to 90 °C) are made with low Ethylene-Vinyl Alcohol Copolymer (EVOH) content without compromising shelf-life and are suitable for fresh and processed meat, fish, and hard cheese.

In-Depth Cling Films Industry Market Outlook

The future outlook for the cling films industry is exceptionally positive, fueled by a confluence of sustainable innovation and persistent demand from essential sectors. Growth accelerators like the development of truly biodegradable and compostable cling films, coupled with advancements in chemical and mechanical recycling technologies, are poised to reshape the market's environmental footprint. Strategic collaborations between industry giants and pioneering startups will unlock new applications and market segments, particularly in areas demanding high-performance protective packaging. The increasing integration of Industry 4.0 principles in manufacturing processes will further enhance efficiency, reduce costs, and improve product quality. Overall, the market is on a trajectory of substantial growth, driven by its indispensable role in food preservation, consumer convenience, and evolving sustainability mandates, presenting significant strategic opportunities for forward-thinking stakeholders.

Cling Films Industry Segmentation

-

1. Material Type

- 1.1. Polyethylene

- 1.2. Biaxially Oriented Polypropylene

- 1.3. Polyvinyl Chloride

- 1.4. Polyvinylidene Chloride

- 1.5. Other Material Types

-

2. Form

- 2.1. Cast Cling Film

- 2.2. Blow Cling Film

-

3. End-user Industry

- 3.1. Food

- 3.2. Healthcare

- 3.3. Consumer Goods

- 3.4. Industrial

- 3.5. Other End-user Industries

Cling Films Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. ASEAN Countries

- 1.6. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. Italy

- 3.4. France

- 3.5. Rest of Europe

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. Saudi Arabia

- 5.2. South Africa

- 5.3. Rest of Middle East and Africa

Cling Films Industry Regional Market Share

Geographic Coverage of Cling Films Industry

Cling Films Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.35% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 5.1.1. Polyethylene

- 5.1.2. Biaxially Oriented Polypropylene

- 5.1.3. Polyvinyl Chloride

- 5.1.4. Polyvinylidene Chloride

- 5.1.5. Other Material Types

- 5.2. Market Analysis, Insights and Forecast - by Form

- 5.2.1. Cast Cling Film

- 5.2.2. Blow Cling Film

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. Food

- 5.3.2. Healthcare

- 5.3.3. Consumer Goods

- 5.3.4. Industrial

- 5.3.5. Other End-user Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Asia Pacific

- 5.4.2. North America

- 5.4.3. Europe

- 5.4.4. South America

- 5.4.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 6. Global Cling Films Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 6.1.1. Polyethylene

- 6.1.2. Biaxially Oriented Polypropylene

- 6.1.3. Polyvinyl Chloride

- 6.1.4. Polyvinylidene Chloride

- 6.1.5. Other Material Types

- 6.2. Market Analysis, Insights and Forecast - by Form

- 6.2.1. Cast Cling Film

- 6.2.2. Blow Cling Film

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. Food

- 6.3.2. Healthcare

- 6.3.3. Consumer Goods

- 6.3.4. Industrial

- 6.3.5. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 7. Asia Pacific Cling Films Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Material Type

- 7.1.1. Polyethylene

- 7.1.2. Biaxially Oriented Polypropylene

- 7.1.3. Polyvinyl Chloride

- 7.1.4. Polyvinylidene Chloride

- 7.1.5. Other Material Types

- 7.2. Market Analysis, Insights and Forecast - by Form

- 7.2.1. Cast Cling Film

- 7.2.2. Blow Cling Film

- 7.3. Market Analysis, Insights and Forecast - by End-user Industry

- 7.3.1. Food

- 7.3.2. Healthcare

- 7.3.3. Consumer Goods

- 7.3.4. Industrial

- 7.3.5. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Material Type

- 8. North America Cling Films Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Material Type

- 8.1.1. Polyethylene

- 8.1.2. Biaxially Oriented Polypropylene

- 8.1.3. Polyvinyl Chloride

- 8.1.4. Polyvinylidene Chloride

- 8.1.5. Other Material Types

- 8.2. Market Analysis, Insights and Forecast - by Form

- 8.2.1. Cast Cling Film

- 8.2.2. Blow Cling Film

- 8.3. Market Analysis, Insights and Forecast - by End-user Industry

- 8.3.1. Food

- 8.3.2. Healthcare

- 8.3.3. Consumer Goods

- 8.3.4. Industrial

- 8.3.5. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Material Type

- 9. Europe Cling Films Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Material Type

- 9.1.1. Polyethylene

- 9.1.2. Biaxially Oriented Polypropylene

- 9.1.3. Polyvinyl Chloride

- 9.1.4. Polyvinylidene Chloride

- 9.1.5. Other Material Types

- 9.2. Market Analysis, Insights and Forecast - by Form

- 9.2.1. Cast Cling Film

- 9.2.2. Blow Cling Film

- 9.3. Market Analysis, Insights and Forecast - by End-user Industry

- 9.3.1. Food

- 9.3.2. Healthcare

- 9.3.3. Consumer Goods

- 9.3.4. Industrial

- 9.3.5. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Material Type

- 10. South America Cling Films Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Material Type

- 10.1.1. Polyethylene

- 10.1.2. Biaxially Oriented Polypropylene

- 10.1.3. Polyvinyl Chloride

- 10.1.4. Polyvinylidene Chloride

- 10.1.5. Other Material Types

- 10.2. Market Analysis, Insights and Forecast - by Form

- 10.2.1. Cast Cling Film

- 10.2.2. Blow Cling Film

- 10.3. Market Analysis, Insights and Forecast - by End-user Industry

- 10.3.1. Food

- 10.3.2. Healthcare

- 10.3.3. Consumer Goods

- 10.3.4. Industrial

- 10.3.5. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Material Type

- 11. Middle East and Africa Cling Films Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Material Type

- 11.1.1. Polyethylene

- 11.1.2. Biaxially Oriented Polypropylene

- 11.1.3. Polyvinyl Chloride

- 11.1.4. Polyvinylidene Chloride

- 11.1.5. Other Material Types

- 11.2. Market Analysis, Insights and Forecast - by Form

- 11.2.1. Cast Cling Film

- 11.2.2. Blow Cling Film

- 11.3. Market Analysis, Insights and Forecast - by End-user Industry

- 11.3.1. Food

- 11.3.2. Healthcare

- 11.3.3. Consumer Goods

- 11.3.4. Industrial

- 11.3.5. Other End-user Industries

- 11.1. Market Analysis, Insights and Forecast - by Material Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Jindal Poly Films Limited

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Paragon Films

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Novamont SPA

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Mitsubishi Chemical Corporation

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Intertape Polymer Group

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 ADEX SRL

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Nan Ya Plastics Corporation

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Deriblok SpA

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Berry Global Inc

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 3M

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Inteplast Group

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Hipac SPA

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Reynolds Consumer Products

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Technovaa Plastic Industries Pvt Ltd *List Not Exhaustive

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Malpack

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Alliance Plastics

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 All American Poly

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 Amcor plc

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.19 Sigma Plastics Group

- 12.1.19.1. Company Overview

- 12.1.19.2. Products

- 12.1.19.3. Company Financials

- 12.1.19.4. SWOT Analysis

- 12.1.20 Anchor Packaging LLC

- 12.1.20.1. Company Overview

- 12.1.20.2. Products

- 12.1.20.3. Company Financials

- 12.1.20.4. SWOT Analysis

- 12.1.1 Jindal Poly Films Limited

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Cling Films Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Asia Pacific Cling Films Industry Revenue (Million), by Material Type 2025 & 2033

- Figure 3: Asia Pacific Cling Films Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 4: Asia Pacific Cling Films Industry Revenue (Million), by Form 2025 & 2033

- Figure 5: Asia Pacific Cling Films Industry Revenue Share (%), by Form 2025 & 2033

- Figure 6: Asia Pacific Cling Films Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 7: Asia Pacific Cling Films Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 8: Asia Pacific Cling Films Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: Asia Pacific Cling Films Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: North America Cling Films Industry Revenue (Million), by Material Type 2025 & 2033

- Figure 11: North America Cling Films Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 12: North America Cling Films Industry Revenue (Million), by Form 2025 & 2033

- Figure 13: North America Cling Films Industry Revenue Share (%), by Form 2025 & 2033

- Figure 14: North America Cling Films Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 15: North America Cling Films Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 16: North America Cling Films Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: North America Cling Films Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Europe Cling Films Industry Revenue (Million), by Material Type 2025 & 2033

- Figure 19: Europe Cling Films Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 20: Europe Cling Films Industry Revenue (Million), by Form 2025 & 2033

- Figure 21: Europe Cling Films Industry Revenue Share (%), by Form 2025 & 2033

- Figure 22: Europe Cling Films Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 23: Europe Cling Films Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 24: Europe Cling Films Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Europe Cling Films Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Cling Films Industry Revenue (Million), by Material Type 2025 & 2033

- Figure 27: South America Cling Films Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 28: South America Cling Films Industry Revenue (Million), by Form 2025 & 2033

- Figure 29: South America Cling Films Industry Revenue Share (%), by Form 2025 & 2033

- Figure 30: South America Cling Films Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 31: South America Cling Films Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 32: South America Cling Films Industry Revenue (Million), by Country 2025 & 2033

- Figure 33: South America Cling Films Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Middle East and Africa Cling Films Industry Revenue (Million), by Material Type 2025 & 2033

- Figure 35: Middle East and Africa Cling Films Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 36: Middle East and Africa Cling Films Industry Revenue (Million), by Form 2025 & 2033

- Figure 37: Middle East and Africa Cling Films Industry Revenue Share (%), by Form 2025 & 2033

- Figure 38: Middle East and Africa Cling Films Industry Revenue (Million), by End-user Industry 2025 & 2033

- Figure 39: Middle East and Africa Cling Films Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 40: Middle East and Africa Cling Films Industry Revenue (Million), by Country 2025 & 2033

- Figure 41: Middle East and Africa Cling Films Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Cling Films Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 2: Global Cling Films Industry Revenue Million Forecast, by Form 2020 & 2033

- Table 3: Global Cling Films Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 4: Global Cling Films Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Global Cling Films Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 6: Global Cling Films Industry Revenue Million Forecast, by Form 2020 & 2033

- Table 7: Global Cling Films Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 8: Global Cling Films Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: China Cling Films Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: India Cling Films Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Japan Cling Films Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: South Korea Cling Films Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: ASEAN Countries Cling Films Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Rest of Asia Pacific Cling Films Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Global Cling Films Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 16: Global Cling Films Industry Revenue Million Forecast, by Form 2020 & 2033

- Table 17: Global Cling Films Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 18: Global Cling Films Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 19: United States Cling Films Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Canada Cling Films Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Mexico Cling Films Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Global Cling Films Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 23: Global Cling Films Industry Revenue Million Forecast, by Form 2020 & 2033

- Table 24: Global Cling Films Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 25: Global Cling Films Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 26: Germany Cling Films Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: United Kingdom Cling Films Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Italy Cling Films Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: France Cling Films Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Rest of Europe Cling Films Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 31: Global Cling Films Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 32: Global Cling Films Industry Revenue Million Forecast, by Form 2020 & 2033

- Table 33: Global Cling Films Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 34: Global Cling Films Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 35: Brazil Cling Films Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Argentina Cling Films Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 37: Rest of South America Cling Films Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Global Cling Films Industry Revenue Million Forecast, by Material Type 2020 & 2033

- Table 39: Global Cling Films Industry Revenue Million Forecast, by Form 2020 & 2033

- Table 40: Global Cling Films Industry Revenue Million Forecast, by End-user Industry 2020 & 2033

- Table 41: Global Cling Films Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 42: Saudi Arabia Cling Films Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 43: South Africa Cling Films Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 44: Rest of Middle East and Africa Cling Films Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Cling Films Industry?

The projected CAGR is approximately 4.35%.

2. Which companies are prominent players in the Cling Films Industry?

Key companies in the market include Jindal Poly Films Limited, Paragon Films, Novamont SPA, Mitsubishi Chemical Corporation, Intertape Polymer Group, ADEX SRL, Nan Ya Plastics Corporation, Deriblok SpA, Berry Global Inc, 3M, Inteplast Group, Hipac SPA, Reynolds Consumer Products, Technovaa Plastic Industries Pvt Ltd *List Not Exhaustive, Malpack, Alliance Plastics, All American Poly, Amcor plc, Sigma Plastics Group, Anchor Packaging LLC.

3. What are the main segments of the Cling Films Industry?

The market segments include Material Type, Form, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 11.34 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Food Industry and Increasing Demand For Food Packaging; Increase in Demand from the Healthcare Sector.

6. What are the notable trends driving market growth?

Food Segment to Dominate the Market.

7. Are there any restraints impacting market growth?

Low Resistance to Extreme Weather Conditions; Rising Global Regulations on its Usage.

8. Can you provide examples of recent developments in the market?

February 2023: Berry Global Group Inc. launched a next-generation version of its proven stretch hood film with a minimum of 30% recycled plastic content. This will help the company to support businesses in achieving sustainability objectives as well as meeting the requirements of current and forthcoming United Kingdom and European plastics packaging legislation.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Cling Films Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Cling Films Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Cling Films Industry?

To stay informed about further developments, trends, and reports in the Cling Films Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence