Key Insights

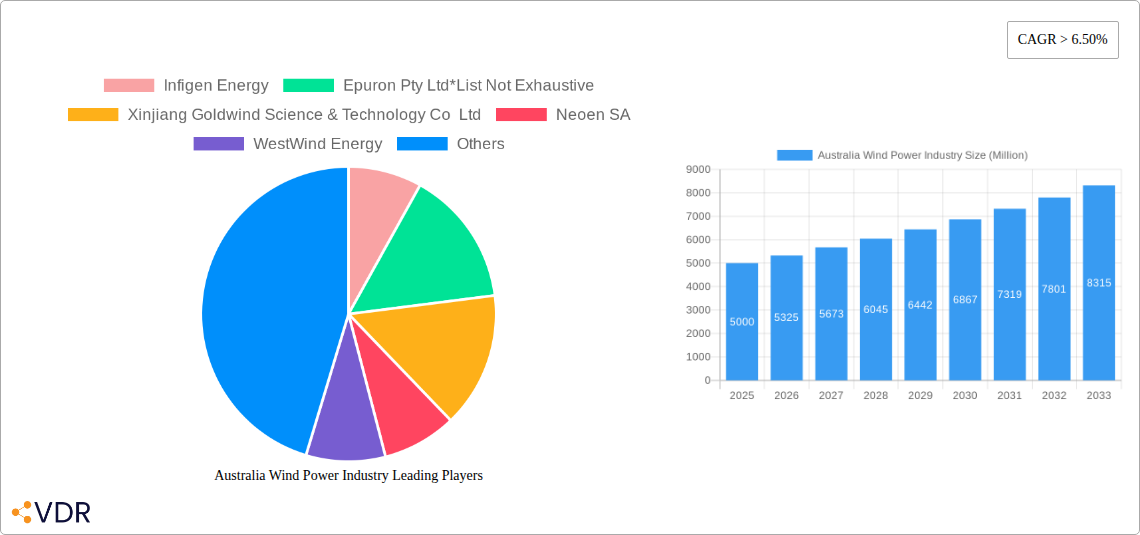

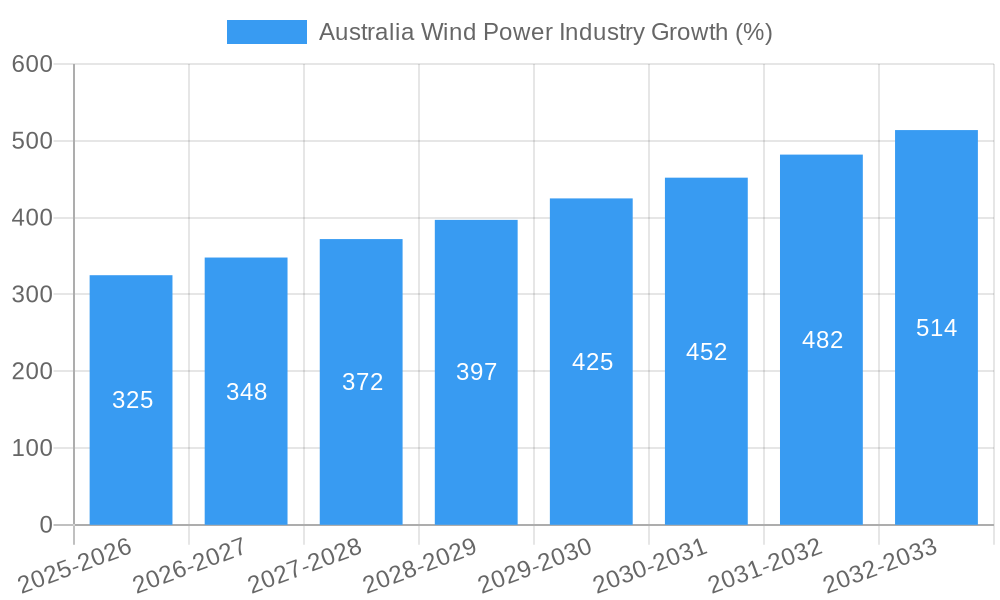

The Australian wind power industry is experiencing robust growth, driven by increasing government support for renewable energy targets, falling wind turbine costs, and a growing awareness of climate change. The market, currently valued at an estimated $X million in 2025 (assuming a logical estimation based on the provided CAGR of >6.50% and available data on similar markets), is projected to maintain a strong Compound Annual Growth Rate (CAGR) exceeding 6.5% throughout the forecast period (2025-2033). This expansion is fueled by several key factors. Firstly, the Australian government's commitment to achieving ambitious renewable energy targets is creating a favorable policy environment. Secondly, technological advancements in wind turbine technology, particularly the increasing prevalence of variable-speed turbines and larger wind farm projects, are leading to enhanced efficiency and cost reductions. Finally, a growing investor interest in sustainable energy solutions is further bolstering industry investment and expansion. The onshore segment currently dominates the market, benefiting from easier accessibility and established infrastructure. However, the offshore wind segment is anticipated to witness significant growth in the coming years, unlocking substantial untapped potential.

Market segmentation within Australia reveals a diverse landscape. The deployment location (onshore vs. offshore) significantly influences market dynamics. Onshore projects currently represent the larger share, driven by established infrastructure and lower upfront costs. Offshore wind, while still nascent, holds immense growth potential, attracting substantial investment due to higher capacity factors and reduced land constraints. Further segmentation by turbine type (fixed-speed and variable-speed) highlights the technological shift towards more efficient variable-speed turbines. Finally, the market is categorized by wind farm size (small, medium, and large), reflecting differing investment scales and project complexities. Key players including Infigen Energy, Epuron Pty Ltd, Xinjiang Goldwind Science & Technology Co Ltd, and Vestas Wind Systems AS are actively shaping market competition and innovation. Continued growth is expected, contingent on sustained policy support, grid infrastructure improvements, and overcoming potential regulatory and environmental hurdles.

This comprehensive report provides an in-depth analysis of the Australian wind power industry, encompassing market dynamics, growth trends, key players, and future outlook. The study period covers 2019-2033, with a base year of 2025 and a forecast period of 2025-2033. This report is essential for investors, industry professionals, and government agencies seeking a detailed understanding of this rapidly evolving sector. Target markets include renewable energy developers, turbine manufacturers, energy providers, and government regulatory bodies.

Australia Wind Power Industry Market Dynamics & Structure

This section analyzes the market concentration, technological advancements, regulatory environment, competitive landscape, and M&A activities within the Australian wind power industry. The analysis considers both onshore and offshore deployments, encompassing small, medium, and large-scale wind farms utilizing fixed-speed and variable-speed wind turbines.

- Market Concentration: The Australian wind power market is characterized by a moderately concentrated landscape, with a few major players holding significant market share. Market share analysis for 2024 reveals Infigen Energy and Tilt Renewables hold approximately xx% and xx%, respectively, while other players such as Neoen and AGL Energy maintain smaller but influential positions.

- Technological Innovation: Key innovation drivers include advancements in turbine technology (e.g., larger rotor diameters, higher capacity factors), improved energy storage solutions, and smart grid integration. Barriers include high initial investment costs and technological complexities associated with offshore wind farm deployments.

- Regulatory Framework: Government policies and incentives, including renewable energy targets and feed-in tariffs, play a crucial role in shaping market dynamics. Regulatory changes impact project approval timelines and investment decisions.

- Competitive Landscape: The market exhibits both cooperation and competition among players. Strategic partnerships, such as that between Vestas and Tilt Renewables, showcase collaborative efforts. Simultaneously, competition is driven by securing project contracts and securing optimal locations.

- M&A Activity: The number of M&A deals in the Australian wind power industry has shown a xx% increase from 2019 to 2024, indicating substantial consolidation and strategic expansion within the sector. Deals mostly focused on acquiring existing projects or acquiring land with wind power potential. Further growth is projected for the forecast period.

Australia Wind Power Industry Growth Trends & Insights

This section presents a comprehensive analysis of the Australian wind power market's size evolution, adoption rates, technological disruptions, and consumer behavior shifts. The analysis leverages a combination of primary and secondary research, market data, and expert interviews.

The Australian wind power market experienced a Compound Annual Growth Rate (CAGR) of xx% during the historical period (2019-2024), reaching a market size of approximately $xx million in 2024. This growth is attributed to increasing government support for renewable energy, falling technology costs, and rising demand for clean energy. The market penetration rate increased from xx% in 2019 to xx% in 2024. The forecast period (2025-2033) anticipates a CAGR of xx%, driven by continued government investment, large-scale project development, and technological advancements. Consumer demand for clean and sustainable energy is also expected to fuel growth. The shift towards more sustainable energy sources influences corporate and household adoption rates and affects the overall market demand.

Dominant Regions, Countries, or Segments in Australia Wind Power Industry

This section identifies the leading regions and segments within the Australian wind power market, based on location of deployment (onshore, offshore), turbine type (fixed-speed, variable-speed), and wind farm size (small, medium, large).

- Onshore Wind Dominance: The onshore wind segment currently dominates the Australian market, accounting for approximately xx% of the total installed capacity in 2024. Key drivers include lower development costs, established infrastructure, and readily available land. However, offshore wind is expected to emerge significantly in the forecast period.

- Variable-Speed Turbines: Variable-speed wind turbines have a larger market share (xx%) compared to fixed-speed turbines, reflecting the industry's technological progress. These turbines offer enhanced energy capture efficiency and reduced wear and tear.

- Medium and Large Wind Farms: Medium and large wind farms constitute the majority (xx%) of installed capacity, attracting significant investments due to economies of scale and higher energy yields. Smaller wind farms cater to niche markets and are more likely to appear in remote areas.

- Regional Variations: Victoria, New South Wales, and South Australia are the leading regions for wind power generation in Australia, due to their favorable wind resources and supportive government policies.

Australia Wind Power Industry Product Landscape

The Australian wind power industry is witnessing continuous advancements in turbine technology, with a focus on larger capacity turbines, improved efficiency, and enhanced reliability. Innovative features include advanced blade designs, optimized power electronics, and advanced control systems. Key performance metrics include capacity factor, energy yield, and lifecycle cost, with manufacturers constantly pushing boundaries to reduce costs and increase efficiency.

Key Drivers, Barriers & Challenges in Australia Wind Power Industry

Key Drivers:

- Government policies and incentives, such as renewable energy targets and feed-in tariffs, significantly drive market growth.

- Falling technology costs and technological advancements, particularly in turbine technology, have made wind power increasingly competitive.

- Growing concerns about climate change and the need for sustainable energy are driving demand for renewable energy sources.

Key Barriers and Challenges:

- Intermittency of wind resources and the need for effective grid integration and energy storage solutions remain significant challenges.

- High initial investment costs and lengthy project approval processes pose hurdles for large-scale projects.

- Competition from other renewable energy sources and the availability of fossil fuels pose competitive pressures on market expansion. Competition is also evident in securing funding and securing land for development.

Emerging Opportunities in Australia Wind Power Industry

- Offshore wind presents significant untapped potential, with substantial offshore wind resources available, but requires additional infrastructure development and overcoming significant technological and regulatory hurdles.

- Hybrid renewable energy projects, integrating wind power with solar or other renewable sources, are gaining traction to optimize energy production and grid stability.

- Increased focus on microgrids and distributed generation could unlock new opportunities for smaller wind farms and tailored energy solutions for remote communities and rural areas.

Growth Accelerators in the Australia Wind Power Industry

Technological advancements, particularly in larger and more efficient turbines and improved energy storage technologies, are key growth accelerators. Strategic partnerships between turbine manufacturers, developers, and energy companies are further accelerating market expansion. Government support for research and development in this sector, coupled with streamlining regulatory processes, will enhance competitiveness and facilitate faster deployment.

Key Players Shaping the Australia Wind Power Industry Market

- Infigen Energy

- Epuron Pty Ltd

- Xinjiang Goldwind Science & Technology Co Ltd

- Neoen SA

- WestWind Energy

- Tilt Renewables

- Suzlon Energy Limited

- WestWind Energy Australia

- Vestas Wind Systems AS

- Acciona SA

Notable Milestones in Australia Wind Power Industry Sector

- December 2021: Alinta Energy announces plans to build a 1GW wind farm in Portland, Victoria.

- September 2021: Vestas and Tilt Renewables secure a 396 MW contract for the Rye Park Wind Farm in New South Wales.

In-Depth Australia Wind Power Industry Market Outlook

The Australian wind power industry is poised for sustained growth in the coming years, driven by supportive government policies, technological advancements, and increasing demand for renewable energy. Strategic opportunities exist in offshore wind development, integration with other renewable energy sources, and exploration of niche markets such as microgrids. The continued reduction in technology costs and advancements in energy storage solutions will further enhance the competitiveness and market potential of wind power in Australia.

Australia Wind Power Industry Segmentation

-

1. Location of Deployment

- 1.1. Onshore

- 1.2. Offshore

Australia Wind Power Industry Segmentation By Geography

- 1. Australia

Australia Wind Power Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 6.50% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Increasing Offshore Exploration and Production Activities4.; Development of Offshore Wind Energy

- 3.3. Market Restrains

- 3.3.1. 4.; Rising Demand for Dynamic Positioning (DP) Drilling Rigs

- 3.4. Market Trends

- 3.4.1. Onshore Segment to Dominate the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Australia Wind Power Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 5.1.1. Onshore

- 5.1.2. Offshore

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Australia

- 5.1. Market Analysis, Insights and Forecast - by Location of Deployment

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Infigen Energy

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Epuron Pty Ltd*List Not Exhaustive

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Xinjiang Goldwind Science & Technology Co Ltd

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Neoen SA

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 WestWind Energy

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Tilt Renewables

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Suzlon Energy Limited

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 WestWind Energy Australia

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Vestas Wind Systems AS

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Acciona SA

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 Infigen Energy

List of Figures

- Figure 1: Australia Wind Power Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Australia Wind Power Industry Share (%) by Company 2024

List of Tables

- Table 1: Australia Wind Power Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Australia Wind Power Industry Revenue Million Forecast, by Location of Deployment 2019 & 2032

- Table 3: Australia Wind Power Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 4: Australia Wind Power Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 5: Australia Wind Power Industry Revenue Million Forecast, by Location of Deployment 2019 & 2032

- Table 6: Australia Wind Power Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Australia Wind Power Industry?

The projected CAGR is approximately > 6.50%.

2. Which companies are prominent players in the Australia Wind Power Industry?

Key companies in the market include Infigen Energy, Epuron Pty Ltd*List Not Exhaustive, Xinjiang Goldwind Science & Technology Co Ltd, Neoen SA, WestWind Energy, Tilt Renewables, Suzlon Energy Limited, WestWind Energy Australia, Vestas Wind Systems AS, Acciona SA.

3. What are the main segments of the Australia Wind Power Industry?

The market segments include Location of Deployment.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Offshore Exploration and Production Activities4.; Development of Offshore Wind Energy.

6. What are the notable trends driving market growth?

Onshore Segment to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Rising Demand for Dynamic Positioning (DP) Drilling Rigs.

8. Can you provide examples of recent developments in the market?

In December 2021, Australian energy company Alinta Energy announced to build a 1GW wind farm in Portland, south-western Victoria. The project would supply the Portland Aluminium Smelter and connect to the east coast electricity grid.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Australia Wind Power Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Australia Wind Power Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Australia Wind Power Industry?

To stay informed about further developments, trends, and reports in the Australia Wind Power Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence