Key Insights

The United States automotive dealership market, a significant component of the broader automotive industry, is experiencing robust growth, driven by several key factors. The market's size in 2025 is estimated at $800 billion, considering a global market size of XX million (assuming XX is a significantly larger figure than the US market, given the US is a major automotive market) and reasonable allocation based on global market share. A Compound Annual Growth Rate (CAGR) exceeding 4% indicates a sustained upward trajectory through 2033. This growth is fueled by increasing vehicle sales, particularly within the passenger car segment, alongside a rising demand for vehicle financing and insurance products. The expanding used vehicle market, driven by affordability concerns and a growing preference for pre-owned vehicles in good condition, also contributes significantly to overall market expansion. Technological advancements, such as the integration of online sales platforms and digital marketing strategies, are transforming the customer experience and further stimulating growth. Franchised retailers continue to dominate the market, leveraging established brand recognition and customer loyalty. However, the non-franchised sector is also witnessing significant expansion, driven by increased competition and a broader range of service offerings.

Despite these positive trends, the market faces certain challenges. Fluctuations in fuel prices, economic downturns, and the increasing availability of electric and autonomous vehicles (EVs and AVs) present potential headwinds. Supply chain disruptions impacting vehicle availability have also presented short-term challenges. The ongoing shift towards electric vehicles introduces opportunities and challenges simultaneously, requiring dealerships to adapt their infrastructure, expertise, and service offerings. The competitive landscape remains dynamic, with established players like AutoNation Inc. and Lithia Motors Inc. competing against smaller, regional dealerships. Strategic partnerships, mergers, and acquisitions are expected to shape market consolidation in the coming years. Furthermore, evolving consumer preferences and the need for enhanced digital capabilities will dictate the success of dealership groups in the long term.

United States Automotive Dealership Market Report: 2019-2033

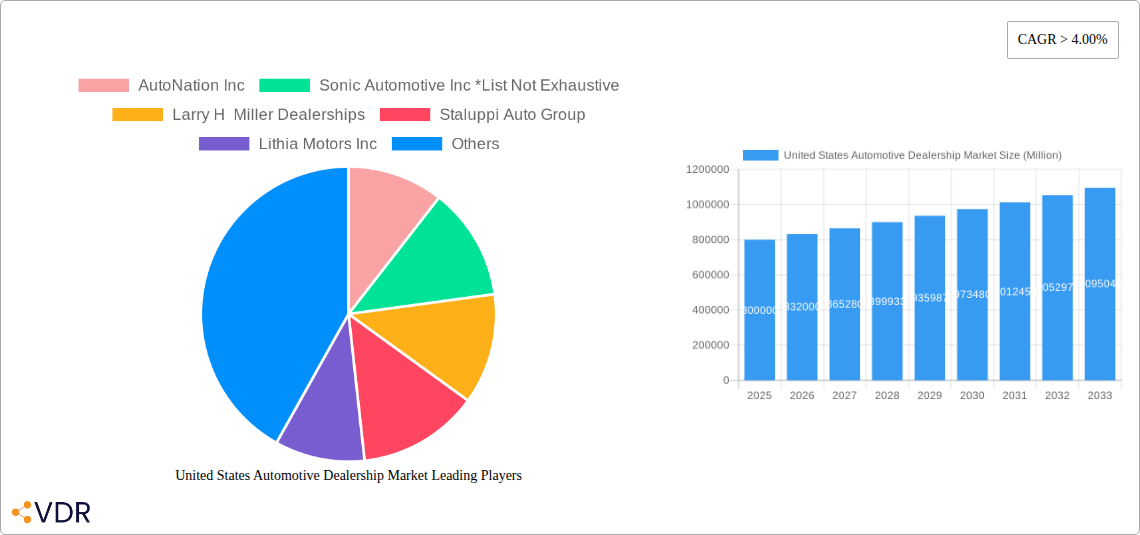

This comprehensive report provides an in-depth analysis of the United States automotive dealership market, encompassing market size, growth trends, competitive landscape, and future outlook. The report covers the period from 2019 to 2033, with a focus on the base year 2025. It segments the market by type (new vehicle dealership, used vehicle dealership, parts and services, finance and insurance), retailer (franchised, non-franchised), and vehicle type (passenger cars, commercial vehicles), providing granular insights into each segment's performance and growth trajectory. Key players such as AutoNation Inc, Sonic Automotive Inc, Larry H Miller Dealerships, Staluppi Auto Group, Lithia Motors Inc, Asbury Automotive Group Inc, Hendrick Automotive Group, Group 1 Automotive Inc, Penske Automotive Group, and Ken Garff Automotive Group are analyzed, offering a complete understanding of the market dynamics and competitive landscape. The report is essential for automotive industry professionals, investors, and stakeholders seeking to navigate this dynamic market.

United States Automotive Dealership Market Dynamics & Structure

The US automotive dealership market is characterized by a moderately concentrated structure, with large dealership groups holding significant market share. Technological innovation, particularly in areas like online sales platforms and digital marketing, is driving significant changes. Stringent regulatory frameworks, including those related to emissions and consumer protection, significantly influence market operations. The rise of used car sales and the increasing popularity of electric vehicles represent key competitive substitutes, impacting the traditional new car dealership model. Demographic shifts, such as the increasing preference for SUVs and trucks, also shape market demand. The industry has experienced notable M&A activity in recent years.

- Market Concentration: The top 10 dealership groups account for approximately xx% of the total market revenue (2024).

- Technological Innovation: Adoption of digital retailing platforms and data analytics is growing but faces challenges in legacy system integration.

- Regulatory Framework: Compliance with emissions standards and consumer protection laws adds complexity and costs for dealerships.

- Competitive Substitutes: The growth of used car sales and electric vehicle options impacts new car sales volume.

- End-User Demographics: Shifting consumer preferences towards SUVs and trucks influence vehicle demand.

- M&A Trends: Consolidation continues, with approximately xx M&A deals recorded between 2019 and 2024, representing a xx% increase compared to the previous period.

United States Automotive Dealership Market Growth Trends & Insights

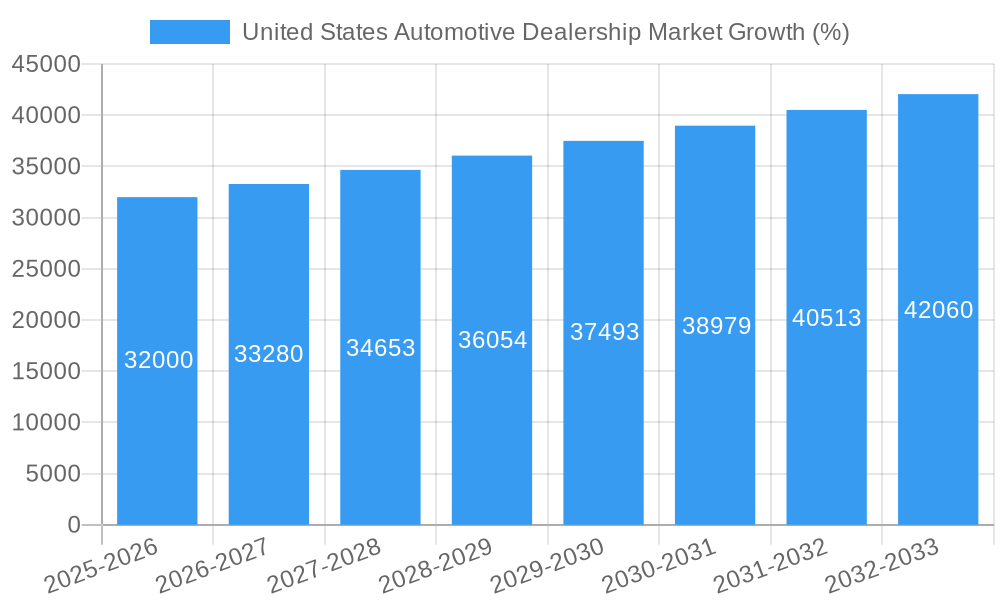

The US automotive dealership market experienced a xx Million units market size in 2024, registering a CAGR of xx% during 2019-2024. The forecast period (2025-2033) projects sustained growth, with a projected CAGR of xx%, driven by factors such as economic recovery, pent-up demand, and technological advancements. Increased adoption of online sales channels and the expansion of digital marketing strategies contribute to market growth. However, supply chain constraints and chip shortages during the early forecast period have impacted sales. Consumer behavior shifts toward larger vehicles like SUVs and trucks continues to drive growth in specific segments. Market penetration of electric vehicles is gradually increasing, although it still represents a relatively small share of the overall market. The market is estimated to reach xx Million units by 2033.

Dominant Regions, Countries, or Segments in United States Automotive Dealership Market

The largest segments by type in the US automotive dealership market are New Vehicle Dealerships (xx Million units in 2024) and Used Vehicle Dealerships (xx Million units in 2024). Within the retail segment, Franchised Retailers hold the largest market share, benefiting from brand recognition and established customer bases. Geographically, the strongest growth is concentrated in the South and West, driven by population growth and economic expansion.

- By Type:

- New Vehicle Dealerships: High growth due to new model releases and economic expansion.

- Used Vehicle Dealerships: Strong growth fueled by affordability and pre-owned vehicle demand.

- Parts and Services: Steady growth driven by vehicle maintenance and repair needs.

- Finance and Insurance: Consistent growth due to financial products offered alongside vehicle purchases.

- By Retailer:

- Franchised Retailers: Dominate the market due to brand recognition and established networks.

- Non-Franchised Retailers: Growing segment benefiting from flexibility and competitive pricing.

- By Vehicle Type:

- Passenger Cars: Mature segment, with slight decline in growth, superseded by SUV and truck segments.

- Commercial Vehicles: Growth driven by economic activity and construction sector performance.

- Geographic Dominance: Strong growth in the South and West regions, driven by population growth and economic expansion.

United States Automotive Dealership Market Product Landscape

The product landscape within the US automotive dealership market is evolving rapidly, encompassing a broad range of vehicles, services, and technological innovations. Dealerships are increasingly leveraging digital tools for enhanced customer experience, including online vehicle configurators, virtual tours, and personalized financing options. The integration of telematics and data analytics plays a crucial role in optimizing inventory management, service scheduling, and customer retention. Unique selling propositions are centered around brand loyalty programs, customer service excellence, and convenient financing options.

Key Drivers, Barriers & Challenges in United States Automotive Dealership Market

Key Drivers: Strong economic growth, increased consumer spending, the introduction of innovative vehicle technologies (such as electric vehicles and autonomous driving features), and government incentives for vehicle purchases are key drivers.

Key Challenges and Restraints: Supply chain disruptions, semiconductor chip shortages, rising interest rates, and increasing competition from online marketplaces pose significant challenges. Regulatory changes related to emissions and fuel economy standards also create challenges for dealerships. The overall impact of these constraints is estimated to reduce market growth by approximately xx% during the forecast period.

Emerging Opportunities in United States Automotive Dealership Market

Emerging opportunities include the expansion of electric vehicle sales, the growth of subscription services for vehicles, the increasing demand for maintenance and repair services for electric vehicles, and the development of personalized customer experiences through data-driven marketing strategies. Untapped markets exist in rural areas and among younger demographics.

Growth Accelerators in the United States Automotive Dealership Market Industry

Technological advancements, such as the adoption of AI-powered sales tools and predictive analytics, are accelerating market growth. Strategic partnerships between dealerships and technology companies are enhancing the customer experience and streamlining operations. Expansion into new markets and diversification of services, such as offering maintenance packages and extended warranties, also play a significant role.

Key Players Shaping the United States Automotive Dealership Market Market

- AutoNation Inc

- Sonic Automotive Inc

- Larry H Miller Dealerships

- Staluppi Auto Group

- Lithia Motors Inc

- Asbury Automotive Group Inc

- Hendrick Automotive Group

- Group 1 Automotive Inc

- Penske Automotive Group

- Ken Garff Automotive Group

Notable Milestones in United States Automotive Dealership Market Sector

- July 2022: Lithia & Driveway (LAD) expands its US presence, acquiring dealerships expected to add nearly USD 1 billion in annual revenue.

- March 2022: Group1 Automotive Inc. secures a USD 2.0 billion credit facility, demonstrating financial strength and expansion capacity.

- January 2022: Penske Automotive Group expands its Honda dealership network in Texas.

- January 2022: Sonic Automotive Inc. acquires Sun Chevrolet and Caputo's used car locations, expanding its market reach.

In-Depth United States Automotive Dealership Market Market Outlook

The US automotive dealership market is poised for continued growth, driven by technological innovation, evolving consumer preferences, and strategic partnerships. The market is expected to witness significant transformation in the coming years, with increased integration of digital technologies, expansion of service offerings, and consolidation among key players. Strategic investments in electric vehicle infrastructure and the development of innovative customer engagement strategies will be crucial for achieving long-term success in this dynamic market.

United States Automotive Dealership Market Segmentation

-

1. Type

- 1.1. New Vehicle dealership

- 1.2. Used Vehicle dealership

- 1.3. Parts and Services

- 1.4. Finance and Insurance

-

2. Retailer

- 2.1. Franchised Retailer

- 2.2. Non-Franchised Retailer

-

3. Vehicle Type

- 3.1. Passenger Cars

- 3.2. Commercial Vehicles

United States Automotive Dealership Market Segmentation By Geography

- 1. United States

United States Automotive Dealership Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 4.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Rapid Urbanization and Demand for Convinient Transportation

- 3.3. Market Restrains

- 3.3.1. Traffic Congestion in Major Cities

- 3.4. Market Trends

- 3.4.1. Rising Focus of Automotive Dealers on Enhancing Consumer Experience and Dealer Network to Drive Demand

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. United States Automotive Dealership Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. New Vehicle dealership

- 5.1.2. Used Vehicle dealership

- 5.1.3. Parts and Services

- 5.1.4. Finance and Insurance

- 5.2. Market Analysis, Insights and Forecast - by Retailer

- 5.2.1. Franchised Retailer

- 5.2.2. Non-Franchised Retailer

- 5.3. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.3.1. Passenger Cars

- 5.3.2. Commercial Vehicles

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United States

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. North America United States Automotive Dealership Market Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 6.1.1 United States

- 6.1.2 Canada

- 6.1.3 Rest of North America

- 7. Europe United States Automotive Dealership Market Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 7.1.1 Germany

- 7.1.2 United Kingdom

- 7.1.3 France

- 7.1.4 Russia

- 7.1.5 Spain

- 7.1.6 Rest of Europe

- 8. Asia Pacific United States Automotive Dealership Market Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 8.1.1 India

- 8.1.2 China

- 8.1.3 Japan

- 8.1.4 South Korea

- 8.1.5 Australia

- 8.1.6 Rest of Asia Pacific

- 9. Latin America United States Automotive Dealership Market Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 9.1.1 Mexico

- 9.1.2 Brazil

- 9.1.3 Argentina

- 9.1.4 Rest Of Latin America

- 10. Middle East and Africa United States Automotive Dealership Market Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 10.1.1 United Arab Emirates

- 10.1.2 Saudi Arabia

- 10.1.3 Rest of Middle East and Africa

- 11. Competitive Analysis

- 11.1. Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 AutoNation Inc

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Sonic Automotive Inc *List Not Exhaustive

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Larry H Miller Dealerships

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Staluppi Auto Group

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Lithia Motors Inc

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Asbury Automotive Group Inc

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Hendrick Automotive Group

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Group 1 Automotive Inc

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Penske Automotive Group

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Ken Garff Automotive Group

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 AutoNation Inc

List of Figures

- Figure 1: United States Automotive Dealership Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: United States Automotive Dealership Market Share (%) by Company 2024

List of Tables

- Table 1: United States Automotive Dealership Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: United States Automotive Dealership Market Revenue Million Forecast, by Type 2019 & 2032

- Table 3: United States Automotive Dealership Market Revenue Million Forecast, by Retailer 2019 & 2032

- Table 4: United States Automotive Dealership Market Revenue Million Forecast, by Vehicle Type 2019 & 2032

- Table 5: United States Automotive Dealership Market Revenue Million Forecast, by Region 2019 & 2032

- Table 6: United States Automotive Dealership Market Revenue Million Forecast, by Country 2019 & 2032

- Table 7: United States United States Automotive Dealership Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Canada United States Automotive Dealership Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Rest of North America United States Automotive Dealership Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: United States Automotive Dealership Market Revenue Million Forecast, by Country 2019 & 2032

- Table 11: Germany United States Automotive Dealership Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: United Kingdom United States Automotive Dealership Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: France United States Automotive Dealership Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Russia United States Automotive Dealership Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Spain United States Automotive Dealership Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Rest of Europe United States Automotive Dealership Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: United States Automotive Dealership Market Revenue Million Forecast, by Country 2019 & 2032

- Table 18: India United States Automotive Dealership Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: China United States Automotive Dealership Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Japan United States Automotive Dealership Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: South Korea United States Automotive Dealership Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Australia United States Automotive Dealership Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Rest of Asia Pacific United States Automotive Dealership Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: United States Automotive Dealership Market Revenue Million Forecast, by Country 2019 & 2032

- Table 25: Mexico United States Automotive Dealership Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Brazil United States Automotive Dealership Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 27: Argentina United States Automotive Dealership Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: Rest Of Latin America United States Automotive Dealership Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 29: United States Automotive Dealership Market Revenue Million Forecast, by Country 2019 & 2032

- Table 30: United Arab Emirates United States Automotive Dealership Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 31: Saudi Arabia United States Automotive Dealership Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 32: Rest of Middle East and Africa United States Automotive Dealership Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 33: United States Automotive Dealership Market Revenue Million Forecast, by Type 2019 & 2032

- Table 34: United States Automotive Dealership Market Revenue Million Forecast, by Retailer 2019 & 2032

- Table 35: United States Automotive Dealership Market Revenue Million Forecast, by Vehicle Type 2019 & 2032

- Table 36: United States Automotive Dealership Market Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the United States Automotive Dealership Market?

The projected CAGR is approximately > 4.00%.

2. Which companies are prominent players in the United States Automotive Dealership Market?

Key companies in the market include AutoNation Inc, Sonic Automotive Inc *List Not Exhaustive, Larry H Miller Dealerships, Staluppi Auto Group, Lithia Motors Inc, Asbury Automotive Group Inc, Hendrick Automotive Group, Group 1 Automotive Inc, Penske Automotive Group, Ken Garff Automotive Group.

3. What are the main segments of the United States Automotive Dealership Market?

The market segments include Type, Retailer, Vehicle Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Rapid Urbanization and Demand for Convinient Transportation.

6. What are the notable trends driving market growth?

Rising Focus of Automotive Dealers on Enhancing Consumer Experience and Dealer Network to Drive Demand.

7. Are there any restraints impacting market growth?

Traffic Congestion in Major Cities.

8. Can you provide examples of recent developments in the market?

July 2022: Lithia & Driveway (LAD) continued its US expansion by buying nine dealerships in southern Florida and one in Nevada, which are expected to add nearly USD 1 billion in annual revenue for the company. LAD also announced its expansion in Las Vegas, Nevada, with the addition of Henderson Hyundai and Genesis. With this purchase, LAD becomes the sole owner of the Hyundai and Genesis stores in the greater metro area.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "United States Automotive Dealership Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the United States Automotive Dealership Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the United States Automotive Dealership Market?

To stay informed about further developments, trends, and reports in the United States Automotive Dealership Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence