Key Insights

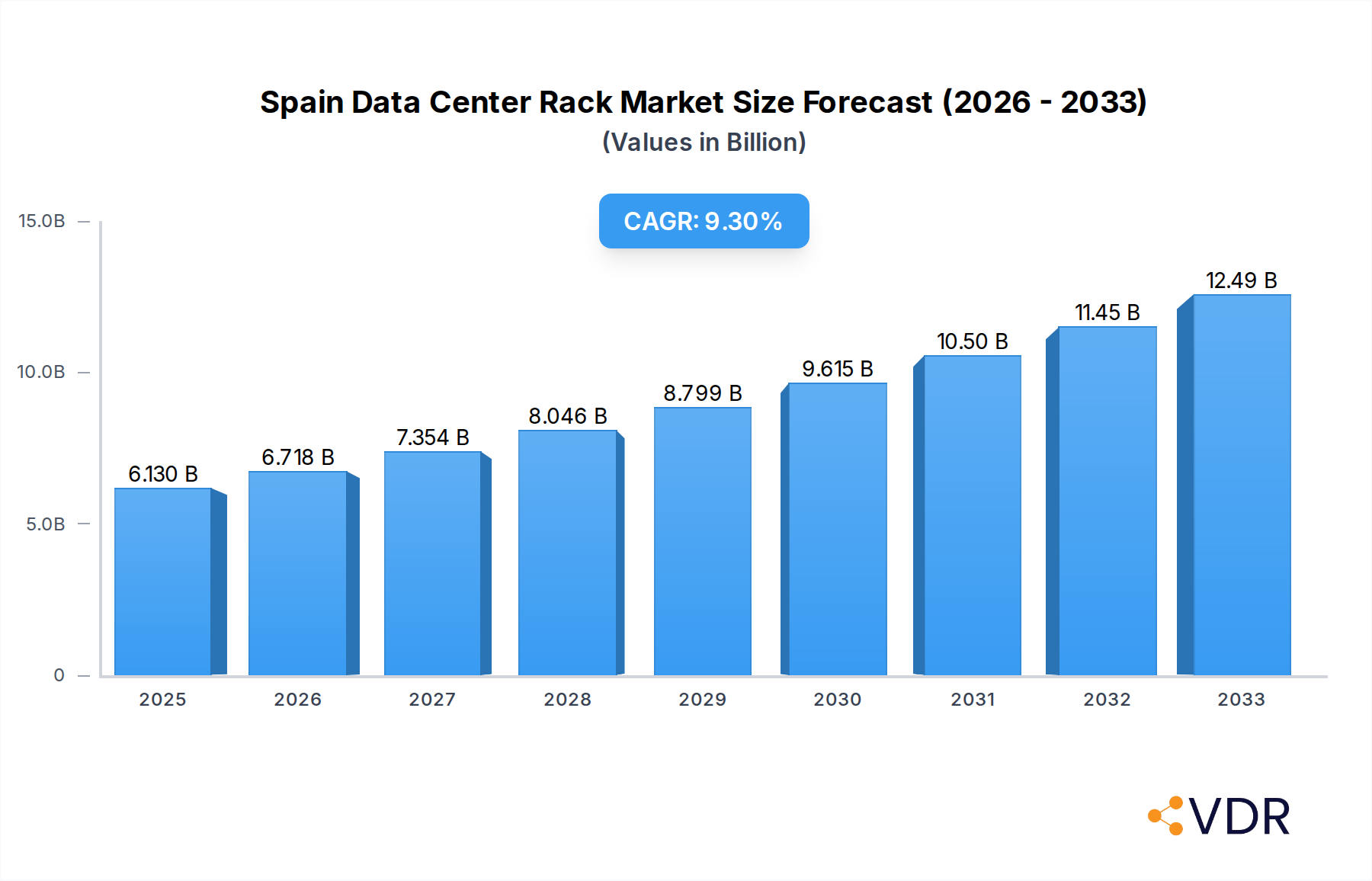

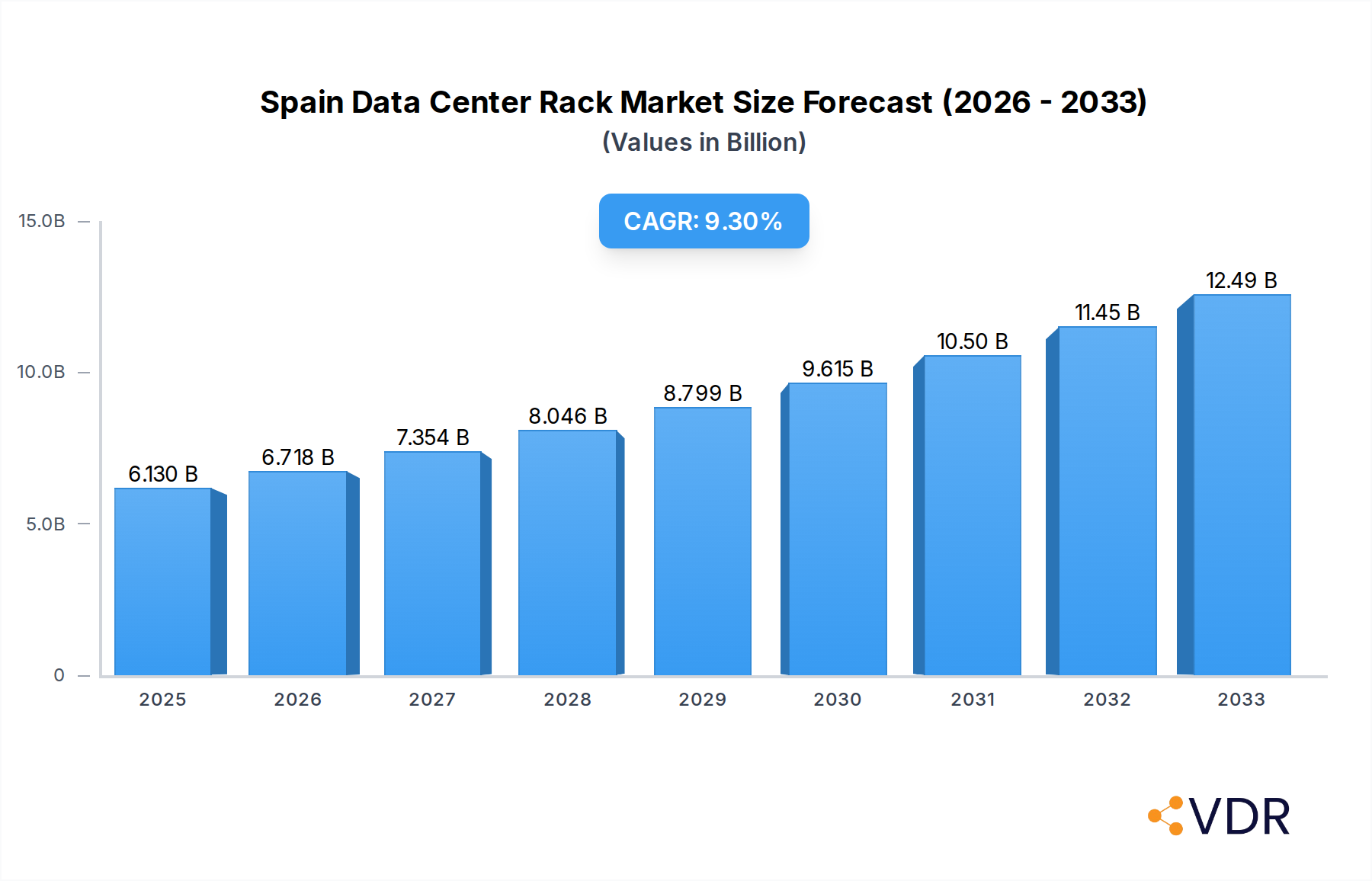

The Spain Data Center Rack Market is poised for significant expansion, with a projected market size of 6.13 billion in 2025, growing at a robust Compound Annual Growth Rate (CAGR) of 9.56% through 2033. This growth is primarily propelled by the escalating demand for digital services across key sectors. The IT & Telecommunication industry, a cornerstone of Spain's digital infrastructure, is a major driver, alongside the burgeoning needs of the BFSI sector for secure and efficient data management. The government's increasing investment in digital transformation initiatives and the expanding media and entertainment landscape further fuel this upward trajectory. The market is segmented by rack size, with Quarter Rack, Half Rack, and Full Rack solutions all witnessing adoption based on specific data center requirements.

Spain Data Center Rack Market Market Size (In Billion)

The market dynamics are further shaped by a confluence of enabling trends and certain challenges. Investments in hyperscale and colocation data centers are creating a sustained demand for high-density rack solutions. The increasing adoption of cloud computing and the subsequent need for robust on-premises infrastructure to support hybrid cloud models are also critical growth factors. Furthermore, advancements in cooling technologies integrated within rack designs are addressing the thermal management challenges associated with high-performance computing. While the market exhibits strong growth potential, potential restraints such as the high initial capital expenditure for advanced rack infrastructure and the ongoing need for skilled personnel to manage and maintain these sophisticated systems need to be strategically addressed by market participants to ensure sustained and optimal market penetration.

Spain Data Center Rack Market Company Market Share

Spain Data Center Rack Market: Comprehensive Growth Insights and Forecast (2019-2033)

This in-depth report provides a definitive analysis of the Spain Data Center Rack Market, offering critical insights into market dynamics, growth trajectories, and competitive landscapes. We delve into the intricate workings of parent market and child market segments, identifying key drivers and emerging opportunities. With a comprehensive study period spanning 2019–2033, a base year of 2025, and a forecast period of 2025–2033, this report equips industry professionals with actionable intelligence to navigate this rapidly evolving sector. Gain a strategic advantage with detailed breakdowns of rack size (Quarter Rack, Half Rack, Full Rack) and end-user segments (IT & Telecommunication, BFSI, Government, Media & Entertainment, Other End-Users). All values are presented in billion units for clarity and impact.

Spain Data Center Rack Market Market Dynamics & Structure

The Spain Data Center Rack Market exhibits a moderate to high market concentration, with key players like Rittal GMBH & Co KG, Schneider Electric SE, and Vertiv Group Corp holding significant market shares. Technological innovation is a primary driver, fueled by increasing demand for high-density computing solutions, efficient power management, and advanced cooling technologies within data centers. Regulatory frameworks, primarily concerning data privacy and security (e.g., GDPR compliance), indirectly influence rack design and deployment standards, emphasizing robust security features. Competitive product substitutes are limited for core rack infrastructure, but innovative modular solutions and integrated power/cooling systems offer differentiation. End-user demographics reveal a strong reliance on the IT & Telecommunication sector, followed by BFSI and Government, each with distinct requirements for rack capacity and security. Mergers & Acquisitions (M&A) trends are observed as companies aim to expand their product portfolios and geographic reach. For instance, recent M&A activity has seen consolidation in the cooling and power distribution segments, aiming to offer more integrated solutions. The market size for data center racks in Spain is estimated to reach $1.2 billion in 2025, with an anticipated CAGR of 6.5% through 2033. Barriers to innovation include high capital expenditure for advanced manufacturing and the need for extensive interoperability testing.

- Market Concentration: Moderate to High, dominated by a few key global players.

- Technological Innovation Drivers: Demand for hyperscale computing, AI/ML integration, edge computing solutions, and energy efficiency.

- Regulatory Frameworks: Data privacy laws (GDPR), sustainability mandates, and IT infrastructure security standards.

- Competitive Substitutes: Limited for core rack infrastructure, but evolving modular and integrated solutions.

- End-User Demographics: IT & Telecommunication leading, followed by BFSI, Government, and Media & Entertainment.

- M&A Trends: Focus on portfolio expansion and integrated solution offerings.

Spain Data Center Rack Market Growth Trends & Insights

The Spain Data Center Rack Market is poised for significant expansion driven by the relentless digital transformation across industries. The estimated market size for data center racks in Spain was approximately $1.0 billion in 2024, with projections indicating a substantial growth to $1.2 billion in 2025. This upward trajectory is underpinned by a projected Compound Annual Growth Rate (CAGR) of 6.5% over the forecast period of 2025–2033. Adoption rates for advanced rack solutions are accelerating as businesses increasingly recognize the critical role of efficient and scalable infrastructure in supporting their digital operations. Technological disruptions, such as the advent of liquid cooling solutions and the demand for hyper-converged infrastructure, are reshaping rack designs and capabilities. Consumer behavior shifts are evident in the growing preference for modular and customizable rack configurations that can adapt to evolving IT workloads and density requirements. The rise of edge computing is also creating new demand for smaller, localized data center racks. Furthermore, the ongoing expansion and modernization of cloud infrastructure, coupled with Spain's strategic location as a digital gateway between Europe and Africa, are significant growth catalysts. The IT & Telecommunication sector continues to be the largest consumer, driven by massive data generation and the proliferation of 5G networks, demanding higher rack density and advanced power distribution. The BFSI sector's need for secure and reliable data storage, alongside government initiatives for digital infrastructure development, further contribute to market expansion. Media and entertainment industries are also increasing their reliance on robust data center infrastructure to handle growing content streaming and production demands. The historical period of 2019–2024 saw consistent growth, building a strong foundation for the forecasted expansion. The market penetration of advanced rack technologies is expected to rise as businesses prioritize performance, efficiency, and sustainability.

Dominant Regions, Countries, or Segments in Spain Data Center Rack Market

Within the Spain Data Center Rack Market, the IT & Telecommunication end-user segment stands as the most dominant force driving market growth. This leadership is attributed to the sector's insatiable appetite for high-density computing, robust network infrastructure, and scalable data storage solutions. The proliferation of 5G networks, the expansion of cloud services, and the increasing adoption of data-intensive applications are all compelling factors contributing to this dominance. The market size for racks catering to IT & Telecommunication is estimated to reach $0.5 billion in 2025, with a projected CAGR of 7.2% through 2033.

Key Drivers for IT & Telecommunication Dominance:

- 5G Network Rollout: Requires significant investment in new and expanded data center facilities, demanding high-density racks for telecommunication equipment.

- Cloud Infrastructure Expansion: Major cloud providers are continuously investing in new data centers and upgrading existing ones, necessitating a substantial influx of racks.

- Data Growth and Analytics: The exponential increase in data generation across all digital services fuels the need for more powerful and dense computing environments.

- Edge Computing Adoption: While creating distributed demand, the core infrastructure for managing these edge nodes often resides in centralized or regional data centers, benefiting the IT & Telecommunication sector.

From a Rack Size perspective, Full Rack solutions are currently the most dominant, accounting for an estimated $0.4 billion in 2025. This dominance is driven by the requirements of large-scale data centers, hyperscale deployments, and enterprise-level server consolidation projects where maximum capacity and flexibility are paramount. However, the Half Rack segment is exhibiting a faster growth rate, projected at a CAGR of 6.8%, driven by the increasing adoption of modular data center designs and the need for more distributed, yet substantial, computing power. The Quarter Rack segment, while smaller, is crucial for edge deployments and specialized applications, experiencing a CAGR of 5.9%.

Dominance Factors and Growth Potential:

- Economic Policies: Government initiatives promoting digital infrastructure development and investment in technology hubs indirectly benefit the IT & Telecommunication sector.

- Infrastructure Investment: Ongoing upgrades and expansions of national broadband networks and data center facilities directly correlate with rack demand.

- Market Share: The IT & Telecommunication sector is estimated to hold approximately 45% of the total Spain Data Center Rack Market share in 2025.

- Growth Potential: Continued digital transformation, the ongoing need for robust network infrastructure, and the emergence of new data-intensive technologies ensure sustained growth for this segment.

Spain Data Center Rack Market Product Landscape

The Spain Data Center Rack Market is characterized by a landscape of innovative and performance-driven product offerings. Manufacturers are focusing on enhanced structural integrity, improved airflow management, and integrated power distribution units (PDUs) to support high-density server deployments. Notable product innovations include self-supporting and seismic-rated racks, advanced cable management solutions for optimal airflow, and smart racks with integrated environmental monitoring capabilities. Applications range from housing traditional IT infrastructure to supporting specialized equipment for AI, machine learning, and edge computing. Performance metrics are increasingly emphasizing load capacity, seismic resistance, thermal management efficiency, and ease of deployment and maintenance. Unique selling propositions often lie in the modularity and scalability of rack designs, allowing for seamless expansion and customization to meet evolving data center needs. Technological advancements such as advanced materials for lighter yet stronger racks and intelligent rack systems that provide real-time data on power consumption and environmental conditions are setting new industry standards.

Key Drivers, Barriers & Challenges in Spain Data Center Rack Market

Key Drivers:

- Digital Transformation: The pervasive adoption of digital technologies across all sectors necessitates robust and scalable data center infrastructure, driving demand for racks.

- Cloud Computing Expansion: Significant investments by cloud service providers in expanding their infrastructure directly translate to increased rack purchases.

- 5G Network Deployment: The rollout of 5G requires a densification of network infrastructure, leading to the establishment of new data centers and increased demand for racks.

- Edge Computing Growth: The expansion of edge computing facilities creates a new demand segment for data center racks, particularly in distributed locations.

- Energy Efficiency Demands: Increasing focus on sustainability and reduced operational costs drives the adoption of racks designed for optimized airflow and cooling efficiency.

Key Barriers & Challenges:

- High Initial Investment: The cost of advanced data center racks and associated infrastructure can be substantial, posing a barrier for smaller organizations.

- Supply Chain Disruptions: Global supply chain volatility can lead to extended lead times and increased costs for raw materials and components.

- Skilled Labor Shortage: The deployment and maintenance of sophisticated data center infrastructure require specialized skills, which can be in short supply.

- Rapid Technological Obsolescence: The fast-paced evolution of IT hardware can lead to racks becoming outdated quickly, necessitating frequent upgrades.

- Regulatory Compliance: Adhering to evolving data privacy, security, and environmental regulations can add complexity and cost to infrastructure decisions.

Emerging Opportunities in Spain Data Center Rack Market

Emerging opportunities in the Spain Data Center Rack Market are largely driven by the decentralization of computing power and the growing demand for specialized infrastructure. The expansion of edge data centers, particularly in retail, manufacturing, and telecommunications, presents a significant untapped market for compact and robust rack solutions. Furthermore, the increasing adoption of AI and machine learning workloads is creating a niche for high-density, liquid-cooled racks that can handle the immense thermal demands of these advanced processing units. The growing emphasis on sustainability and energy efficiency also opens avenues for manufacturers offering eco-friendly rack materials and designs optimized for reduced power consumption. Strategic partnerships between rack manufacturers and cooling solution providers to offer integrated, turnkey solutions are also poised to gain traction.

Growth Accelerators in the Spain Data Center Rack Market Industry

Several key catalysts are accelerating long-term growth in the Spain Data Center Rack Market. The ongoing advancements in server technology, leading to higher power consumption and heat generation per rack unit, directly drive the demand for more sophisticated cooling and power management integrated within rack systems. Strategic partnerships between data center operators, colocation providers, and rack manufacturers are crucial for developing tailored solutions that meet specific infrastructure needs. Furthermore, government initiatives promoting digitalization and the establishment of tech hubs are creating a favorable environment for data center investments. The increasing adoption of modular and prefabricated data center solutions also acts as a growth accelerator, streamlining deployment processes and reducing time-to-market for new facilities.

Key Players Shaping the Spain Data Center Rack Market Market

- Espaciorack S

- Hewlett Packard Enterprise

- nVent Electric PLC

- Esnova Racks S A

- Schneider Electric SE

- Dell Inc

- Black Box Corporation

- Vertiv Group Corp

- Rittal GMBH & Co KG

- Eaton Corporation

Notable Milestones in Spain Data Center Rack Market Sector

- 2023: Launch of new modular rack solutions with enhanced cooling capabilities by leading manufacturers.

- 2023: Increased M&A activity focusing on integrated power and cooling solutions for data centers.

- 2022: Significant investments in expanding hyperscale data center capacity across Spain.

- 2021: Growing demand for high-density racks to support AI and machine learning workloads.

- 2020: Emergence of smart racks with advanced monitoring and management features.

- 2019: Increased focus on sustainable materials and energy-efficient rack designs.

In-Depth Spain Data Center Rack Market Market Outlook

The Spain Data Center Rack Market is set for robust and sustained growth, driven by the unwavering march of digitalization and technological innovation. The market's future is characterized by an increasing demand for high-density, energy-efficient, and intelligent rack solutions. Growth accelerators such as the continuous expansion of cloud infrastructure, the critical role of racks in enabling 5G networks, and the burgeoning adoption of edge computing will continue to fuel market expansion. Strategic opportunities lie in providing integrated solutions that combine advanced cooling, power management, and intelligent monitoring within a single rack ecosystem. The Spanish market, with its strategic geographic position and increasing digital infrastructure investments, is well-positioned to capitalize on these trends, presenting lucrative prospects for manufacturers and solution providers aiming to meet the evolving needs of a dynamic data center landscape. The market is projected to reach an estimated $1.8 billion by 2033.

Spain Data Center Rack Market Segmentation

-

1. Rack Size

- 1.1. Quarter Rack

- 1.2. Half Rack

- 1.3. Full Rack

-

2. End-User

- 2.1. IT & Telecommunication

- 2.2. BFSI

- 2.3. Government

- 2.4. Media & Entertainment

- 2.5. Other End-Users

Spain Data Center Rack Market Segmentation By Geography

- 1. Spain

Spain Data Center Rack Market Regional Market Share

Geographic Coverage of Spain Data Center Rack Market

Spain Data Center Rack Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.56% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Rack Size

- 5.1.1. Quarter Rack

- 5.1.2. Half Rack

- 5.1.3. Full Rack

- 5.2. Market Analysis, Insights and Forecast - by End-User

- 5.2.1. IT & Telecommunication

- 5.2.2. BFSI

- 5.2.3. Government

- 5.2.4. Media & Entertainment

- 5.2.5. Other End-Users

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Spain

- 5.1. Market Analysis, Insights and Forecast - by Rack Size

- 6. Spain Data Center Rack Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Rack Size

- 6.1.1. Quarter Rack

- 6.1.2. Half Rack

- 6.1.3. Full Rack

- 6.2. Market Analysis, Insights and Forecast - by End-User

- 6.2.1. IT & Telecommunication

- 6.2.2. BFSI

- 6.2.3. Government

- 6.2.4. Media & Entertainment

- 6.2.5. Other End-Users

- 6.1. Market Analysis, Insights and Forecast - by Rack Size

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Espaciorack S

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Hewlett Packard Enterprise

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 nVent Electric PLC

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Esnova Racks S A

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Schneider Electric SE

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Dell Inc

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Black Box Corporation

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Vertiv Group Corp

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Rittal GMBH & Co KG

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Eaton Corporation

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Espaciorack S

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Spain Data Center Rack Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Spain Data Center Rack Market Share (%) by Company 2025

List of Tables

- Table 1: Spain Data Center Rack Market Revenue billion Forecast, by Rack Size 2020 & 2033

- Table 2: Spain Data Center Rack Market Revenue billion Forecast, by End-User 2020 & 2033

- Table 3: Spain Data Center Rack Market Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Spain Data Center Rack Market Revenue billion Forecast, by Rack Size 2020 & 2033

- Table 5: Spain Data Center Rack Market Revenue billion Forecast, by End-User 2020 & 2033

- Table 6: Spain Data Center Rack Market Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Spain Data Center Rack Market ?

The projected CAGR is approximately 9.56%.

2. Which companies are prominent players in the Spain Data Center Rack Market ?

Key companies in the market include Espaciorack S, Hewlett Packard Enterprise, nVent Electric PLC, Esnova Racks S A, Schneider Electric SE, Dell Inc, Black Box Corporation, Vertiv Group Corp, Rittal GMBH & Co KG, Eaton Corporation.

3. What are the main segments of the Spain Data Center Rack Market ?

The market segments include Rack Size, End-User.

4. Can you provide details about the market size?

The market size is estimated to be USD 6.13 billion as of 2022.

5. What are some drivers contributing to market growth?

Increased Migration to Cloud-based Business Operations; Internet Adoption and Information Technology Services to Boost Market Progress.

6. What are the notable trends driving market growth?

Cloud segment to hold major share in the market.

7. Are there any restraints impacting market growth?

Low Availability of Resources.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Spain Data Center Rack Market ," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Spain Data Center Rack Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Spain Data Center Rack Market ?

To stay informed about further developments, trends, and reports in the Spain Data Center Rack Market , consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence