Key Insights

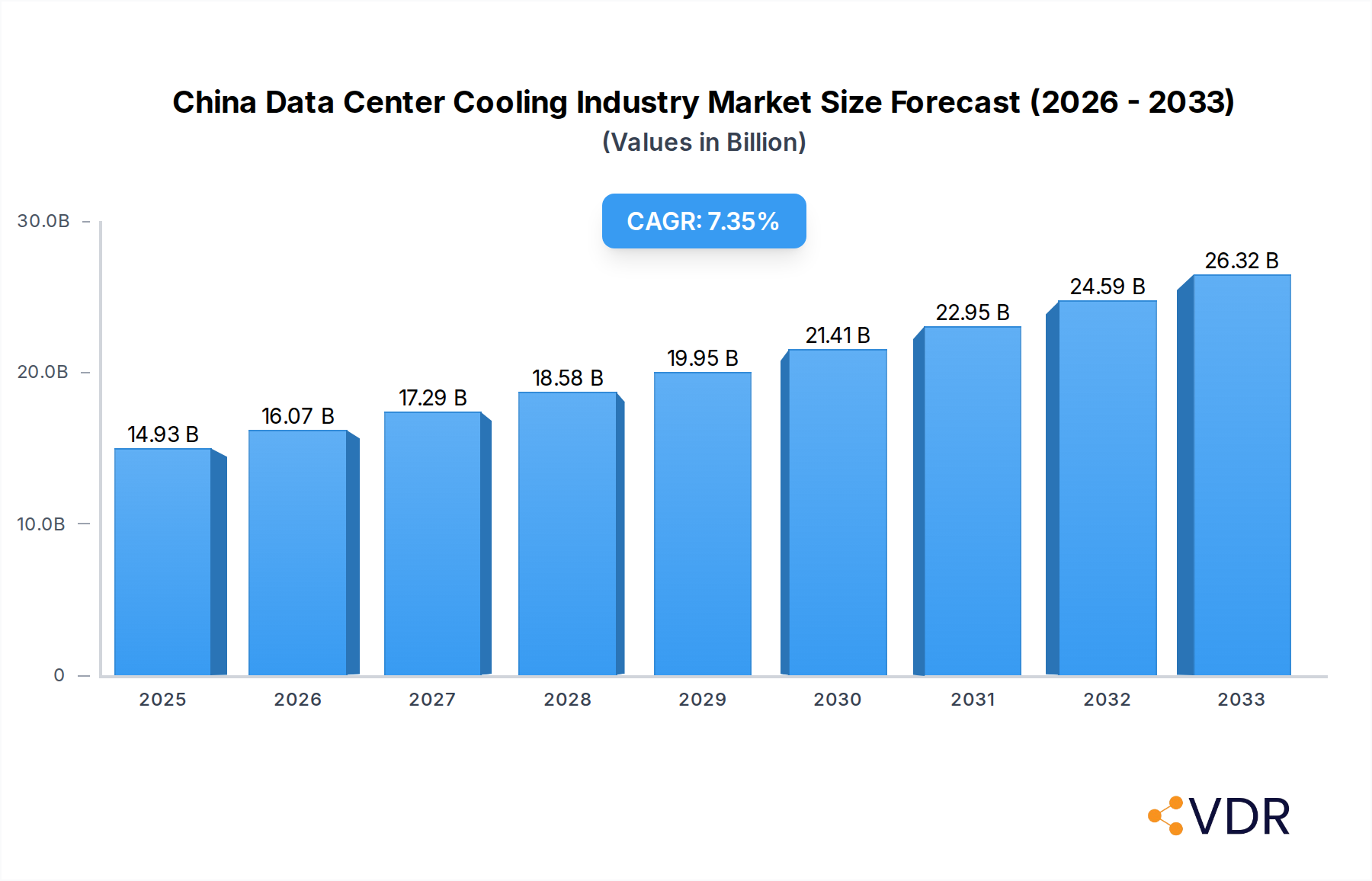

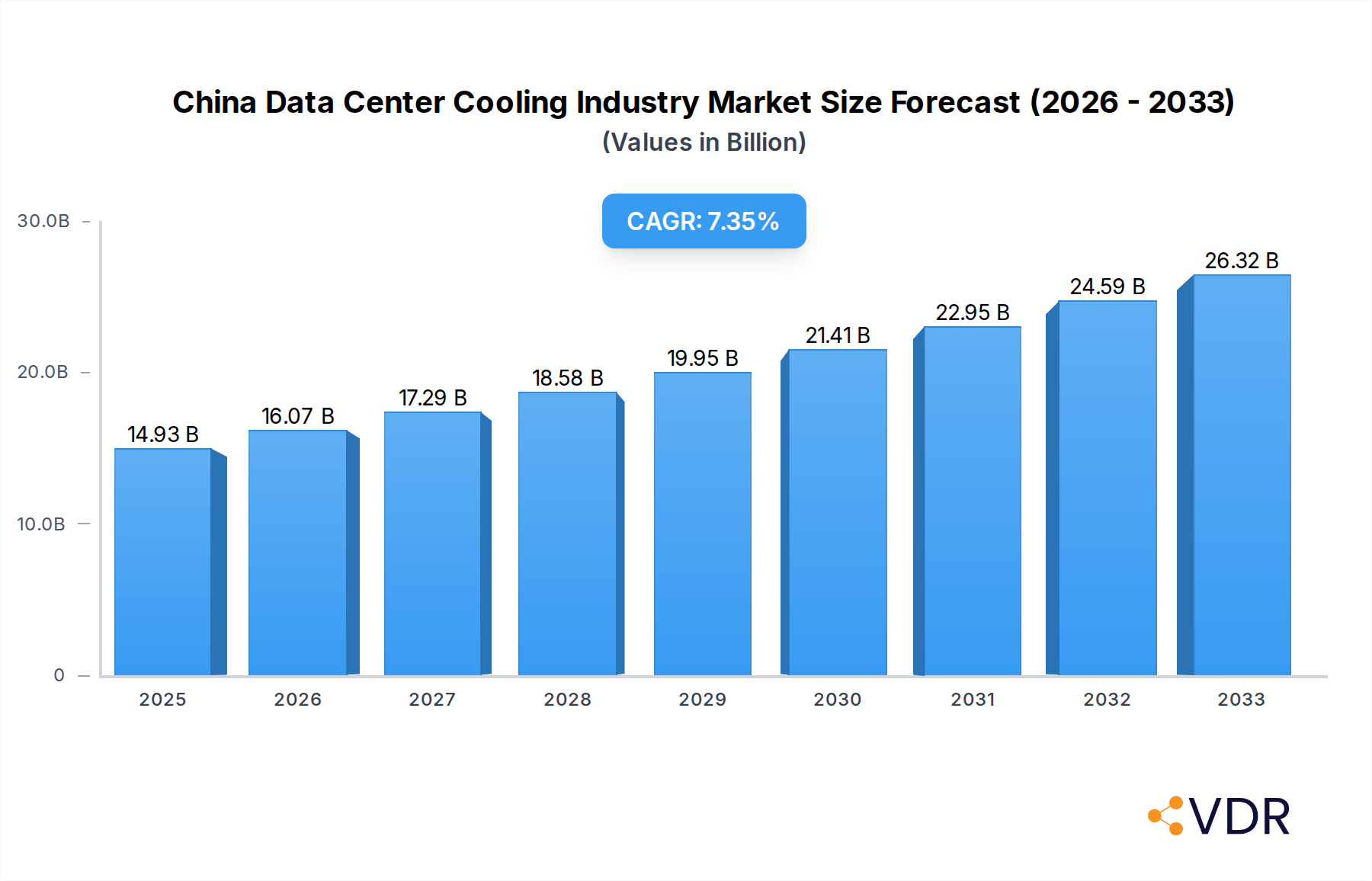

The China Data Center Cooling Industry is poised for significant expansion, driven by the escalating demand for data processing and storage fueled by digital transformation across various sectors. With a projected market size of $14.93 billion in 2025, the industry is set to witness a robust CAGR of 7.68% through 2033. This growth is propelled by the rapid proliferation of hyperscale data centers, the increasing adoption of advanced technologies like AI and IoT, and the burgeoning e-commerce and cloud computing markets. The surge in data generation from sectors such as IT and Telecom, Media and Entertainment, and Healthcare necessitates efficient and scalable cooling solutions to maintain optimal operating temperatures and ensure data center reliability. This dynamic landscape presents substantial opportunities for providers of innovative cooling technologies, including both air-based and liquid-based systems.

China Data Center Cooling Industry Market Size (In Billion)

The industry's trajectory is further shaped by the increasing focus on energy efficiency and sustainability within data center operations. As operators grapple with rising energy costs and environmental regulations, there is a growing preference for advanced cooling techniques such as immersion cooling and direct-to-chip cooling, which offer superior thermal management and reduced energy consumption compared to traditional air-based methods. While the substantial investments in new data center infrastructure and upgrades to existing facilities serve as key growth drivers, challenges such as high initial investment costs for advanced cooling systems and the need for specialized technical expertise in deploying and maintaining these solutions may present some restraints. However, the overarching trend towards digitalization and the continuous need for high-performance computing power will continue to fuel the demand for sophisticated data center cooling solutions in China.

China Data Center Cooling Industry Company Market Share

Dive deep into the rapidly evolving China Data Center Cooling industry with our comprehensive market analysis. This report provides critical insights into market dynamics, growth trends, regional dominance, and the competitive landscape, essential for stakeholders seeking to capitalize on this booming sector. Covering the period from 2019 to 2033, with a base and estimated year of 2025, this report offers a forward-looking perspective on a market projected for substantial expansion.

China Data Center Cooling Industry Market Dynamics & Structure

The China data center cooling market is characterized by dynamic evolution, driven by escalating demand for digital infrastructure and a growing emphasis on energy efficiency. Market concentration varies across segments, with established global players and emerging domestic innovators vying for market share. Technological innovation is a paramount driver, particularly advancements in liquid cooling solutions and waterless cooling technologies, responding to sustainability mandates and the increasing power densities of high-performance computing. Regulatory frameworks, while evolving, are increasingly favoring green data center practices, influencing investment and operational strategies. Competitive product substitutes range from traditional air-based cooling systems like chillers and CRAHs to advanced liquid-based solutions such as immersion cooling and direct-to-chip cooling, offering diverse solutions for different needs. End-user demographics are expanding beyond traditional IT and telecom to include retail, healthcare, and media, each with unique cooling requirements. Merger and acquisition (M&A) trends are indicative of consolidation and strategic partnerships aimed at expanding technological capabilities and market reach.

- Technological Innovation: Focus on energy efficiency, water conservation, and higher heat removal capacities.

- Regulatory Influence: Government initiatives promoting green data centers and carbon emission reductions.

- Competitive Landscape: Intense competition between providers of air-based and liquid-based cooling solutions.

- End-User Diversification: Growing adoption by non-traditional data center users seeking robust cooling infrastructure.

- M&A Activity: Strategic acquisitions to gain market share and technological expertise.

China Data Center Cooling Industry Growth Trends & Insights

The China data center cooling market is poised for robust growth, fueled by the relentless expansion of digital services, the proliferation of Artificial Intelligence (AI), and the continuous upgrade of IT infrastructure. As China solidifies its position as a global technology powerhouse, the demand for high-density computing environments necessitates sophisticated and efficient cooling solutions. The market size is projected to witness a significant expansion, with an estimated Compound Annual Growth Rate (CAGR) of approximately 15% from 2025 to 2033. Adoption rates of advanced cooling technologies, particularly liquid cooling, are accelerating as data centers confront thermal challenges associated with next-generation hardware. Technological disruptions, such as the increasing adoption of AI and machine learning, are driving the need for specialized cooling that can handle extreme heat loads, leading to higher market penetration of direct-to-chip and immersion cooling. Consumer behavior shifts are also playing a role, with enterprises prioritizing sustainability and operational cost reduction, making energy-efficient cooling solutions increasingly attractive. The integration of smart cooling management systems, leveraging IoT and AI for predictive maintenance and optimized performance, is becoming a standard expectation. Furthermore, the ongoing build-out of hyperscale data centers, coupled with the growth of colocation facilities, provides a substantial and consistent demand for cooling infrastructure. The increasing focus on water-efficient cooling technologies, driven by environmental concerns and regional water scarcity, is another key trend shaping the market. The overall market trajectory points towards a sophisticated ecosystem where cutting-edge cooling technologies are indispensable for maintaining the integrity and performance of critical digital infrastructure. The market is expected to reach a valuation of approximately $15 billion by 2033, up from an estimated $6 billion in 2025.

Dominant Regions, Countries, or Segments in China Data Center Cooling Industry

Within the China data center cooling industry, the Hyperscaler (Owned and Leased) segment emerges as the dominant force, driving significant market growth and technological adoption. These hyperscale operators, responsible for massive data center infrastructures supporting cloud services, social media, and e-commerce giants, have a voracious appetite for advanced cooling solutions. Their investments in new builds and expansions, driven by escalating data traffic and the increasing demand for cloud computing, directly translate into substantial procurement of cooling equipment and services. This segment is characterized by a high degree of technological sophistication, pushing the boundaries of efficiency and sustainability.

Key Drivers for Hyperscaler Dominance:

- Massive Infrastructure Investments: Hyperscalers are continuously building and expanding their data center footprints to meet global demand, requiring extensive cooling capacity.

- High Power Densities: The deployment of high-performance computing (HPC) and AI accelerators within hyperscale facilities generates immense heat loads, necessitating advanced cooling technologies.

- Focus on Efficiency and Sustainability: To manage operational costs and meet environmental goals, hyperscalers are at the forefront of adopting energy-efficient cooling solutions, including liquid cooling and waterless technologies.

- Strategic Partnerships: Hyperscalers often collaborate with leading cooling providers to develop bespoke solutions, fostering innovation and driving market trends.

- Economies of Scale: Their large-scale deployments allow for significant cost efficiencies, making advanced cooling solutions more accessible.

Beyond hyperscalers, the Liquid-based Cooling technologies, particularly Direct-to-chip Cooling and Immersion Cooling, are experiencing accelerated adoption and represent a critical growth segment. As server densities continue to climb, traditional air-cooling methods are proving insufficient. Direct-to-chip solutions offer targeted cooling for high-heat components like CPUs and GPUs, while immersion cooling provides a highly efficient method for submerging entire IT hardware in dielectric fluids, offering superior heat dissipation. The increasing prevalence of AI, machine learning, and HPC workloads within both hyperscale and enterprise data centers is a primary catalyst for this shift. The Federal and Institutional agencies segment is also showing increasing interest in these advanced solutions for their high-performance computing needs.

Key Drivers for Liquid Cooling Growth:

- Rising Heat Densities: The increasing power consumption and heat output of modern processors and accelerators.

- Demand for Higher Performance: Enabling sustained peak performance of cutting-edge hardware.

- Energy Efficiency Gains: Liquid cooling systems can offer significant improvements in Power Usage Effectiveness (PUE).

- Reduced Footprint: Potentially enabling denser server deployments within existing data center spaces.

- Water Conservation: Immersion cooling, in particular, eliminates the need for water-based cooling towers in many applications.

China Data Center Cooling Industry Product Landscape

The China data center cooling industry product landscape is characterized by a spectrum of innovative solutions designed to meet diverse thermal management needs. From highly efficient air-based systems like advanced chillers and economizers to cutting-edge liquid-based technologies such as direct-to-chip and immersion cooling, the market offers a comprehensive suite of products. Recent product innovations include waterless cooling technologies like Chindata Group's X-Cooling, which promises zero cooling water usage (WUE Zero Cooling) and unprecedented efficiency. The product portfolio encompasses cooling technologies like CRAH units, rear-door heat exchangers, and specialized cooling solutions for high-density racks. These products are crucial for optimizing data center performance, reducing energy consumption, and ensuring the reliability of critical IT infrastructure across various end-user industries.

Key Drivers, Barriers & Challenges in China Data Center Cooling Industry

Key Drivers:

- Explosive Data Growth: The relentless increase in data generation and consumption, driven by cloud computing, AI, and IoT, necessitates robust data center infrastructure and advanced cooling.

- Government Support for Digitalization: National initiatives promoting digital transformation and the development of smart cities create a fertile ground for data center expansion.

- Technological Advancements: Innovations in liquid cooling and energy-efficient air-cooling systems are enhancing performance and sustainability.

- Demand for High-Performance Computing: The rise of AI, machine learning, and big data analytics requires cooling solutions capable of managing extreme heat loads.

Barriers & Challenges:

- High Initial Investment Costs: Advanced cooling solutions, especially liquid cooling, can have substantial upfront costs, posing a barrier for some organizations.

- Skilled Workforce Shortage: The deployment and maintenance of sophisticated cooling systems require specialized expertise, and a shortage of skilled technicians can hinder widespread adoption.

- Supply Chain Disruptions: Geopolitical factors and global supply chain vulnerabilities can impact the availability and cost of critical components.

- Energy Consumption Concerns: While efficiency is improving, data centers remain significant energy consumers, and ongoing pressure exists to further reduce their environmental footprint.

- Regulatory Complexity: Navigating evolving environmental regulations and building codes can be challenging for new installations and upgrades.

Emerging Opportunities in China Data Center Cooling Industry

Emerging opportunities in the China data center cooling industry are centered around the burgeoning demand for sustainable and high-performance solutions. The rapid adoption of AI and HPC is creating a significant need for advanced liquid cooling technologies, including direct-to-chip and immersion cooling, offering substantial market potential. Furthermore, the growing focus on water conservation is driving innovation in waterless cooling solutions and free-cooling techniques, particularly in regions facing water scarcity. The expansion of edge computing infrastructure also presents an opportunity for localized, modular cooling solutions. Finally, the increasing integration of smart cooling management systems, leveraging AI and IoT for predictive maintenance and energy optimization, is opening up new avenues for service-based revenue models.

Growth Accelerators in the China Data Center Cooling Industry Industry

Several key catalysts are accelerating the growth of the China data center cooling industry. Firstly, the rapid adoption of Artificial Intelligence (AI) and High-Performance Computing (HPC) is a major growth driver, demanding cooling solutions capable of managing unprecedented heat densities. Secondly, governmental policies promoting green energy and sustainability are encouraging the adoption of energy-efficient cooling technologies, reducing the environmental impact of data centers. Thirdly, the continuous expansion of hyperscale and colocation data centers, fueled by the surging demand for cloud services and digital content, creates a consistent and substantial market for cooling infrastructure. Strategic partnerships between technology providers and data center operators are also playing a crucial role in accelerating the development and deployment of innovative cooling solutions.

Key Players Shaping the China Data Center Cooling Industry Market

- Johnson Controls International PLC

- Daikin Industries Ltd

- Munters Air Treatment Equipment (Beijing) Co Ltd

- STULZ GMBH

- Carrier Global Corporation

- Trane Inc

- Condair Group

- Vertiv Co

- Schneider Electric SE

- Chat Union Climaveneta

- RITTAL Electro-Mechanical Technology Co Ltd (RITTAL GMBH & CO KG)

- Gree Electric Appliances Inc of Zhuhai

- Mitsubishi Heavy Industries Ltd

Notable Milestones in China Data Center Cooling Industry Sector

- July 2022: During the 2022 China Computing Conference, Chindata Group, in collaboration with Vertiv Technology, unveiled groundbreaking waterless cooling technology known as X-Cooling, enabling data centers to achieve WUE Zero Cooling and setting a new industry standard for efficiency and sustainability.

- February 2022: Gigabyte introduced cutting-edge high-performance computing servers utilizing CoolIT's direct liquid cooling system, powered by AMD EPYC and Nvidia A100 processors, designed for optimal thermal management and sustained performance.

In-Depth China Data Center Cooling Industry Market Outlook

The China data center cooling industry is on an upward trajectory, with future market potential driven by the persistent evolution of digital technologies and a strong commitment to sustainability. The increasing adoption of AI, machine learning, and 5G infrastructure will continue to fuel the demand for high-density computing, thereby propelling the need for advanced liquid cooling solutions. Strategic opportunities lie in expanding the reach of immersion cooling and direct-to-chip technologies into a broader range of enterprise and hyperscale deployments. Furthermore, the ongoing development of intelligent cooling management systems, integrating IoT and AI for enhanced efficiency and predictive maintenance, presents a significant avenue for growth. Investments in research and development for next-generation cooling technologies that prioritize water conservation and energy efficiency will be crucial for long-term success in this dynamic market.

China Data Center Cooling Industry Segmentation

-

1. Cooling Technology

-

1.1. Air-based Cooling

- 1.1.1. Chiller and Economizer

- 1.1.2. CRAH

- 1.1.3. Cooling

- 1.1.4. Other Air-based Cooling Technologies

-

1.2. Liquid-based Cooling

- 1.2.1. Immersion Cooling

- 1.2.2. Direct-to-chip Cooling

- 1.2.3. Rear-door Heat Exchanger

-

1.1. Air-based Cooling

-

2. Type

- 2.1. Hyperscaler (Owned and Leased)

- 2.2. Enterprise (On-premise)

- 2.3. Colocation

-

3. End-user Industry

- 3.1. IT and Telecom

- 3.2. Retail and Consumer Goods

- 3.3. Healthcare

- 3.4. Media and Entertainment

- 3.5. Federal and Institutional agencies

- 3.6. Other End-user Industries

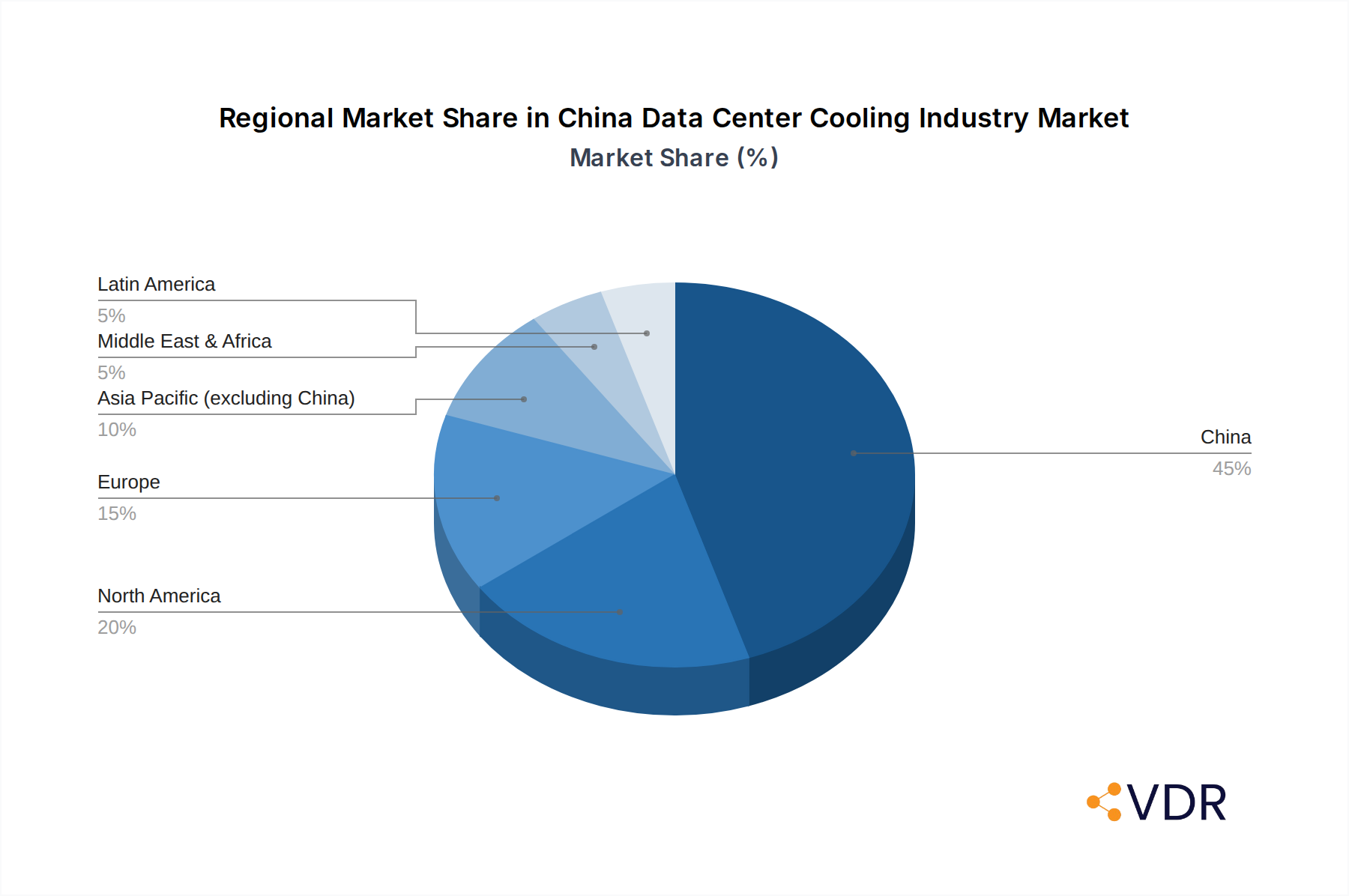

China Data Center Cooling Industry Segmentation By Geography

- 1. China

China Data Center Cooling Industry Regional Market Share

Geographic Coverage of China Data Center Cooling Industry

China Data Center Cooling Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 22.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Cooling Technology

- 5.1.1. Air-based Cooling

- 5.1.1.1. Chiller and Economizer

- 5.1.1.2. CRAH

- 5.1.1.3. Cooling

- 5.1.1.4. Other Air-based Cooling Technologies

- 5.1.2. Liquid-based Cooling

- 5.1.2.1. Immersion Cooling

- 5.1.2.2. Direct-to-chip Cooling

- 5.1.2.3. Rear-door Heat Exchanger

- 5.1.1. Air-based Cooling

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Hyperscaler (Owned and Leased)

- 5.2.2. Enterprise (On-premise)

- 5.2.3. Colocation

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. IT and Telecom

- 5.3.2. Retail and Consumer Goods

- 5.3.3. Healthcare

- 5.3.4. Media and Entertainment

- 5.3.5. Federal and Institutional agencies

- 5.3.6. Other End-user Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. China

- 5.1. Market Analysis, Insights and Forecast - by Cooling Technology

- 6. China Data Center Cooling Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Cooling Technology

- 6.1.1. Air-based Cooling

- 6.1.1.1. Chiller and Economizer

- 6.1.1.2. CRAH

- 6.1.1.3. Cooling

- 6.1.1.4. Other Air-based Cooling Technologies

- 6.1.2. Liquid-based Cooling

- 6.1.2.1. Immersion Cooling

- 6.1.2.2. Direct-to-chip Cooling

- 6.1.2.3. Rear-door Heat Exchanger

- 6.1.1. Air-based Cooling

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Hyperscaler (Owned and Leased)

- 6.2.2. Enterprise (On-premise)

- 6.2.3. Colocation

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. IT and Telecom

- 6.3.2. Retail and Consumer Goods

- 6.3.3. Healthcare

- 6.3.4. Media and Entertainment

- 6.3.5. Federal and Institutional agencies

- 6.3.6. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Cooling Technology

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Johnson Controls International PLC

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Daikin Industries Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Munters Air Treatment Equipment (Beijing) Co Ltd

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 STULZ GMBH

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Carrier Global Corporation

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Trane Inc

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Condair Group

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Vertiv Co

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Schneider Electric SE

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Chat Union Climaveneta *List Not Exhaustive

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 RITTAL Electro-Mechanical Technology Co Ltd (RITTAL GMBH & CO KG)

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Gree Electric Appliances Inc of Zhuhai

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Mitsubishi Heavy Industries Ltd

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.1 Johnson Controls International PLC

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China Data Center Cooling Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: China Data Center Cooling Industry Share (%) by Company 2025

List of Tables

- Table 1: China Data Center Cooling Industry Revenue billion Forecast, by Cooling Technology 2020 & 2033

- Table 2: China Data Center Cooling Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 3: China Data Center Cooling Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 4: China Data Center Cooling Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: China Data Center Cooling Industry Revenue billion Forecast, by Cooling Technology 2020 & 2033

- Table 6: China Data Center Cooling Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 7: China Data Center Cooling Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 8: China Data Center Cooling Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Data Center Cooling Industry?

The projected CAGR is approximately 22.3%.

2. Which companies are prominent players in the China Data Center Cooling Industry?

Key companies in the market include Johnson Controls International PLC, Daikin Industries Ltd, Munters Air Treatment Equipment (Beijing) Co Ltd, STULZ GMBH, Carrier Global Corporation, Trane Inc, Condair Group, Vertiv Co, Schneider Electric SE, Chat Union Climaveneta *List Not Exhaustive, RITTAL Electro-Mechanical Technology Co Ltd (RITTAL GMBH & CO KG), Gree Electric Appliances Inc of Zhuhai, Mitsubishi Heavy Industries Ltd.

3. What are the main segments of the China Data Center Cooling Industry?

The market segments include Cooling Technology, Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 26.31 billion as of 2022.

5. What are some drivers contributing to market growth?

Development of IT Infrastructure in the Region; Emergence of Green Data Centers.

6. What are the notable trends driving market growth?

Liquid-based cooling is the fastest growing segment.

7. Are there any restraints impacting market growth?

Costs. Adaptability Requirements. and Power Outages.

8. Can you provide examples of recent developments in the market?

July 2022: During the 2022 China Computing Conference, Chindata Group, in collaboration with their technology research partner Vertiv Technology, unveiled groundbreaking waterless cooling technology known as X-Cooling. This innovation enables data centers to achieve an unprecedented level of efficiency with WUE Zero Cooling, setting a new industry standard. By embracing X-Cooling, data centers can significantly contribute to sustainability efforts, inspiring further advancements in the development of highly efficient data centers.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Data Center Cooling Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Data Center Cooling Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Data Center Cooling Industry?

To stay informed about further developments, trends, and reports in the China Data Center Cooling Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence