Key Insights

The Semi-active WDM market is poised for substantial expansion, projected to reach $5.92 billion in 2025. This robust growth is underpinned by a compelling Compound Annual Growth Rate (CAGR) of 16.69% throughout the forecast period. The increasing demand for higher bandwidth and faster data transmission, driven by the proliferation of 5G networks, the exponential rise in cloud computing, and the burgeoning data center infrastructure, are the primary catalysts propelling this market forward. Furthermore, the continuous evolution of optical networking technologies and the growing need for efficient spectrum utilization in telecommunication networks are also significant drivers. As businesses and consumers alike demand more data-intensive applications, the role of semi-active WDM in enabling scalable and cost-effective network upgrades becomes increasingly critical. The market's trajectory indicates a strong reliance on advanced components and solutions that can manage complex optical signals efficiently.

Semi-active WDM Market Size (In Billion)

The market is characterized by a dynamic competitive landscape with key players like Infinera, FIBERSTAMP, and Huawei driving innovation and market penetration. The segmentation by application highlights the dominance of Data Centers and Engine Rooms, which require high-density and high-performance WDM solutions. The 12-channel variants are expected to see significant adoption due to their superior capacity compared to 6-channel counterparts. Geographically, Asia Pacific, led by China and India, is anticipated to be a major growth engine, owing to rapid digital transformation initiatives and substantial investments in telecommunications infrastructure. While the market presents significant opportunities, potential restraints such as the high initial cost of deployment and the complexities associated with network integration could temper growth in certain regions. However, the overarching trend towards enhanced network performance and capacity will likely outweigh these challenges.

Semi-active WDM Company Market Share

This comprehensive report offers an in-depth analysis of the Semi-active WDM market, providing critical insights into its dynamics, growth trends, regional dominance, product landscape, and competitive environment. Designed for industry professionals, stakeholders, and investors, this report leverages high-traffic keywords to maximize search engine visibility and deliver actionable intelligence. We cover the entire market value chain, from fundamental technology to end-user applications, with a focus on Wavelength Division Multiplexing advancements. The report encompasses a study period from 2019 to 2033, with a base and estimated year of 2025, and a forecast period from 2025 to 2033, building upon historical data from 2019 to 2024.

Semi-active WDM Market Dynamics & Structure

The semi-active WDM market is characterized by a moderately concentrated structure, driven by continuous technological innovation and evolving network demands. Key players are investing heavily in research and development to enhance spectral efficiency and reduce operational costs. Regulatory frameworks, particularly those promoting broadband expansion and 5G deployment, are indirectly fueling market growth. Competitive product substitutes include passive WDM solutions and advanced Ethernet technologies, pushing semi-active WDM providers to differentiate through performance and cost-effectiveness. End-user demographics are shifting towards hyperscale data centers and telecommunication infrastructure providers seeking scalable and flexible optical networking solutions. Merger and acquisition (M&A) trends are observed as larger entities seek to consolidate market share and acquire specialized technological capabilities.

- Market Concentration: Dominated by a few key players alongside a growing number of specialized vendors, indicating a competitive yet consolidating landscape.

- Technological Innovation Drivers: Focus on higher channel counts, improved power efficiency, and integration with advanced network management systems.

- Regulatory Frameworks: Government initiatives for digital infrastructure development and broadband penetration act as significant catalysts.

- Competitive Product Substitutes: Passive WDM, dedicated fiber solutions, and advanced Ethernet technologies.

- End-User Demographics: Telecommunication carriers, data center operators, cloud service providers, and enterprise networks.

- M&A Trends: Strategic acquisitions to gain market share, acquire intellectual property, and expand product portfolios.

Semi-active WDM Growth Trends & Insights

The semi-active WDM market is poised for robust growth, projected to reach an estimated market size of $X.XX billion in 2025, with a significant CAGR of XX.X% forecasted between 2025 and 2033. This upward trajectory is primarily propelled by the escalating demand for high-bandwidth connectivity, driven by the proliferation of cloud computing, big data analytics, and the continuous expansion of 5G mobile networks. The increasing need for efficient data transmission in data centers and base stations is a fundamental market driver. Technological disruptions, such as the development of more advanced optical components and integrated photonic circuits, are enhancing the performance and reducing the cost of semi-active WDM systems. Consumer behavior shifts, particularly the growing reliance on bandwidth-intensive applications like high-definition video streaming, online gaming, and virtual reality, further amplify the demand for scalable optical network solutions. The market penetration of semi-active WDM technology is expected to deepen as its cost-effectiveness and flexibility become more appealing compared to traditional point-to-point optical links. Furthermore, the ongoing upgrade cycles in telecommunications infrastructure globally necessitate the adoption of advanced WDM solutions to accommodate future traffic demands. The transition from legacy network architectures to more agile and software-defined networking (SDN) environments also favors the adoption of semi-active WDM, which offers enhanced control and manageability. The development of smaller form factor devices and lower power consumption are also key trends influencing adoption rates, especially in space-constrained environments like mobile base stations. The increasing adoption of open networking principles in the telecom industry is also creating opportunities for interoperable semi-active WDM solutions.

Dominant Regions, Countries, or Segments in Semi-active WDM

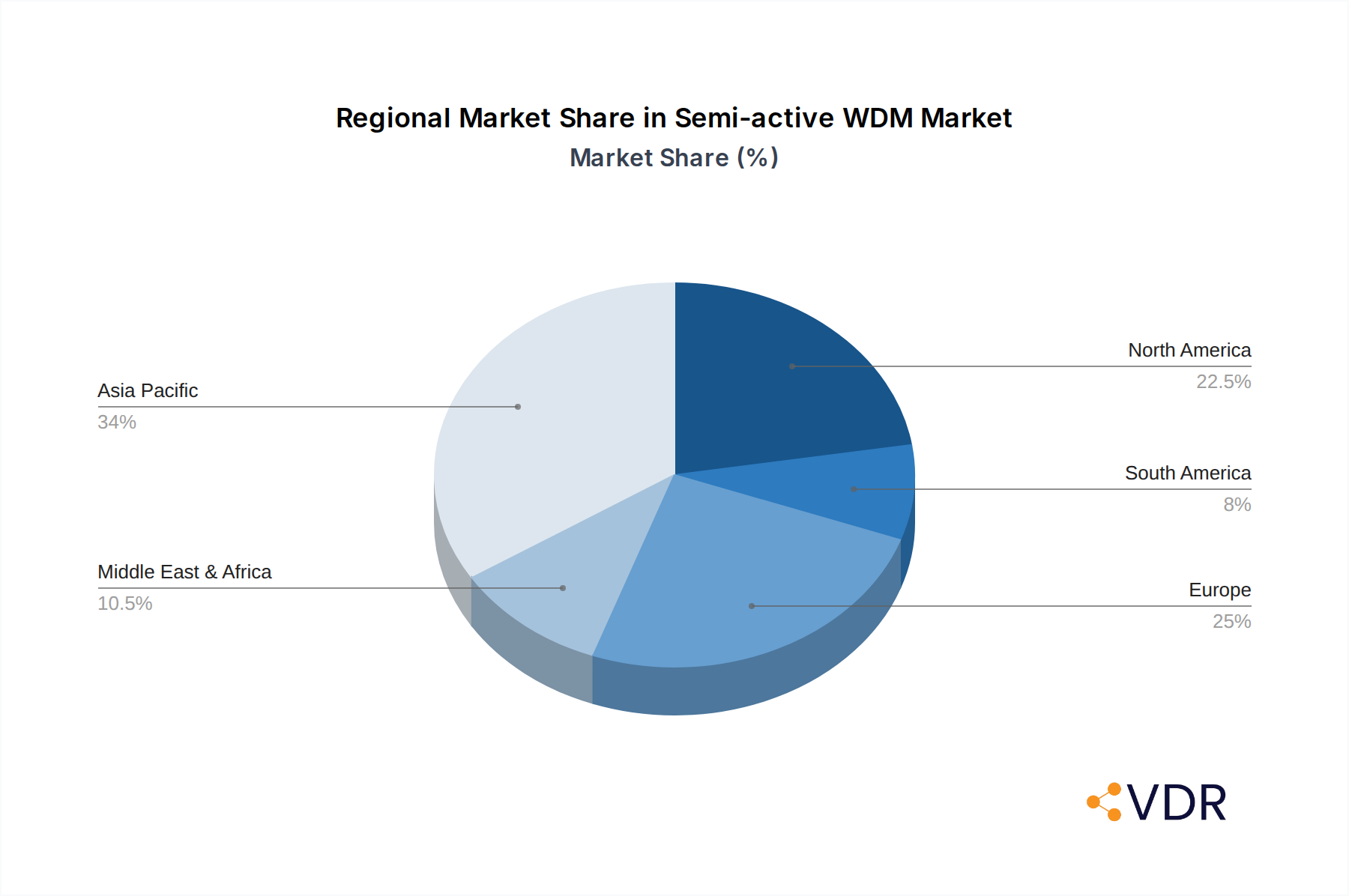

The Data Center segment is emerging as a dominant force in the semi-active WDM market, driven by the insatiable demand for high-speed data transfer and increased server connectivity within these facilities. The North America region, with its established robust digital infrastructure and significant investments in cloud computing and hyperscale data centers, is anticipated to lead market growth. The Asia-Pacific region, particularly countries like China, is also a significant growth engine, fueled by massive investments in 5G deployment and the rapid expansion of its data center footprint.

- Dominant Segment (Application): Data Center:

- Exponential growth in data traffic from cloud services, AI, and big data analytics.

- Need for high-density, high-speed interconnections within data centers.

- Scalability and flexibility offered by semi-active WDM to accommodate fluctuating bandwidth demands.

- Growing adoption of hyperscale and edge data centers requiring efficient optical networking.

- Dominant Region: North America:

- Leadership in cloud computing and hyperscale data center development.

- Significant investments in 5G infrastructure and fiber-to-the-home (FTTH) deployments.

- Strong presence of key technology companies driving innovation and adoption.

- Supportive government policies and initiatives for digital transformation.

- Leading Type: 12 Channels:

- Offers a balanced approach between spectral efficiency and cost-effectiveness for medium to large-scale deployments.

- Ideal for enterprise networks and mid-sized data centers requiring more capacity than 6-channel solutions.

- Growing demand for higher port densities in network aggregation layers.

Semi-active WDM Product Landscape

The semi-active WDM product landscape is marked by continuous innovation, focusing on enhanced performance, increased channel density, and improved power efficiency. Manufacturers are developing compact, modular, and integrated solutions for easier deployment and maintenance. Key product advancements include higher data rate support (e.g., 100Gbps, 400Gbps per channel), extended reach capabilities, and advanced monitoring and management features. These products are increasingly designed to integrate seamlessly with existing network infrastructures, offering flexibility for upgrades and expansions. Unique selling propositions often revolve around reduced latency, superior signal integrity, and simplified network management.

Key Drivers, Barriers & Challenges in Semi-active WDM

Key Drivers: The primary forces propelling the semi-active WDM market include the exponential growth in global data traffic, the widespread deployment of 5G networks, and the burgeoning demand for high-capacity optical interconnects within data centers. Technological advancements in optical components and the increasing adoption of cloud services are also significant drivers.

Key Barriers & Challenges: Significant challenges include intense price competition, the complexity of integration with legacy networks, and the ongoing need for skilled personnel to manage and maintain these systems. Supply chain disruptions for critical optical components and evolving cybersecurity concerns also pose hurdles. The capital expenditure required for initial deployment can be a barrier for smaller enterprises.

Emerging Opportunities in Semi-active WDM

Emerging opportunities lie in the development of higher-density WDM solutions (e.g., 24 or 48 channels) to meet the escalating bandwidth needs of future networks. The expansion of edge computing and the Internet of Things (IoT) presents new application areas for semi-active WDM in localized data processing and network aggregation. Furthermore, the increasing focus on energy-efficient networking solutions opens avenues for products with reduced power consumption. The integration of AI and machine learning for network optimization and predictive maintenance within WDM systems also represents a significant growth area.

Growth Accelerators in the Semi-active WDM Industry

Growth in the semi-active WDM industry is being significantly accelerated by strategic partnerships between telecommunications providers and network equipment manufacturers to accelerate 5G rollouts and data center expansions. Technological breakthroughs in silicon photonics and advanced modulation techniques are enabling higher bandwidth and lower costs. Market expansion into emerging economies with rapidly developing telecommunications infrastructures further fuels growth. The increasing demand for specialized WDM solutions tailored for specific applications, such as enterprise private networks and industrial IoT, also acts as a key accelerator.

Key Players Shaping the Semi-active WDM Market

- Infinera

- FIBERSTAMP

- Huawei

- Guangzhou Sintai Communication

- 3C-Link Technology

- WDMLight

- Shenzhen HTFuture

- Shenzhen HUANET Technology

- Guilin GLSUN Science and Tech Group

- SONT Technologies

- Sino-Telecom Technology

- Triple-Stone

- Genew Technologies

- GIGALIGHT

- FHTEK

- ATOP Corporation

- Fiberhome

- Hymo Connect

Notable Milestones in Semi-active WDM Sector

- 2019: Introduction of 400G coherent optical modules, enabling higher data rates over existing WDM infrastructure.

- 2020: Increased adoption of compact, pluggable WDM transceivers for data center interconnects.

- 2021: Significant investment in R&D for higher channel count semi-active WDM systems to support 5G densification.

- 2022: Growing interest in coherent WDM solutions for metro and long-haul networks to enhance capacity.

- 2023: Launch of more power-efficient semi-active WDM components driven by sustainability initiatives.

- 2024: Expansion of semi-active WDM applications into industrial IoT and private network deployments.

In-Depth Semi-active WDM Market Outlook

The semi-active WDM market is projected for sustained robust growth, driven by fundamental shifts in data consumption and network infrastructure requirements. The confluence of 5G expansion, hyperscale data center proliferation, and the increasing adoption of cloud services will continue to fuel demand. Strategic investments in advanced technologies like silicon photonics and the development of higher channel density solutions will be crucial for market participants. Emerging markets present significant untapped potential, while evolving consumer preferences for bandwidth-intensive applications will ensure ongoing market dynamism. The industry's ability to innovate and adapt to these evolving demands will define its future trajectory.

Semi-active WDM Segmentation

-

1. Application

- 1.1. Base Station

- 1.2. Engine Room

- 1.3. Data Center

- 1.4. Others

-

2. Types

- 2.1. 6 Channels

- 2.2. 12 Channels

- 2.3. Others

Semi-active WDM Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Semi-active WDM Regional Market Share

Geographic Coverage of Semi-active WDM

Semi-active WDM REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 16.69% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Base Station

- 5.1.2. Engine Room

- 5.1.3. Data Center

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. 6 Channels

- 5.2.2. 12 Channels

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Semi-active WDM Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Base Station

- 6.1.2. Engine Room

- 6.1.3. Data Center

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. 6 Channels

- 6.2.2. 12 Channels

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Semi-active WDM Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Base Station

- 7.1.2. Engine Room

- 7.1.3. Data Center

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. 6 Channels

- 7.2.2. 12 Channels

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Semi-active WDM Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Base Station

- 8.1.2. Engine Room

- 8.1.3. Data Center

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. 6 Channels

- 8.2.2. 12 Channels

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Semi-active WDM Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Base Station

- 9.1.2. Engine Room

- 9.1.3. Data Center

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. 6 Channels

- 9.2.2. 12 Channels

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Semi-active WDM Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Base Station

- 10.1.2. Engine Room

- 10.1.3. Data Center

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. 6 Channels

- 10.2.2. 12 Channels

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Semi-active WDM Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Base Station

- 11.1.2. Engine Room

- 11.1.3. Data Center

- 11.1.4. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. 6 Channels

- 11.2.2. 12 Channels

- 11.2.3. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Infinera

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 FIBERSTAMP

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Huawei

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Guangzhou Sintai Communication

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 3C-Link Technology

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 WDMLight

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Shenzhen HTFuture

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Shenzhen HUANET Technology

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Guilin GLSUN Science and Tech Group

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 SONT Technologies

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Sino-Telecom Technology

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Triple-Stone

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Genew Technologies

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 GIGALIGHT

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 FHTEK

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 ATOP Corporation

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Fiberhome

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 Hymo Connect

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.1 Infinera

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Semi-active WDM Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Semi-active WDM Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Semi-active WDM Revenue (billion), by Application 2025 & 2033

- Figure 4: North America Semi-active WDM Volume (K), by Application 2025 & 2033

- Figure 5: North America Semi-active WDM Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Semi-active WDM Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Semi-active WDM Revenue (billion), by Types 2025 & 2033

- Figure 8: North America Semi-active WDM Volume (K), by Types 2025 & 2033

- Figure 9: North America Semi-active WDM Revenue Share (%), by Types 2025 & 2033

- Figure 10: North America Semi-active WDM Volume Share (%), by Types 2025 & 2033

- Figure 11: North America Semi-active WDM Revenue (billion), by Country 2025 & 2033

- Figure 12: North America Semi-active WDM Volume (K), by Country 2025 & 2033

- Figure 13: North America Semi-active WDM Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Semi-active WDM Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Semi-active WDM Revenue (billion), by Application 2025 & 2033

- Figure 16: South America Semi-active WDM Volume (K), by Application 2025 & 2033

- Figure 17: South America Semi-active WDM Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Semi-active WDM Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Semi-active WDM Revenue (billion), by Types 2025 & 2033

- Figure 20: South America Semi-active WDM Volume (K), by Types 2025 & 2033

- Figure 21: South America Semi-active WDM Revenue Share (%), by Types 2025 & 2033

- Figure 22: South America Semi-active WDM Volume Share (%), by Types 2025 & 2033

- Figure 23: South America Semi-active WDM Revenue (billion), by Country 2025 & 2033

- Figure 24: South America Semi-active WDM Volume (K), by Country 2025 & 2033

- Figure 25: South America Semi-active WDM Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Semi-active WDM Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Semi-active WDM Revenue (billion), by Application 2025 & 2033

- Figure 28: Europe Semi-active WDM Volume (K), by Application 2025 & 2033

- Figure 29: Europe Semi-active WDM Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Semi-active WDM Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Semi-active WDM Revenue (billion), by Types 2025 & 2033

- Figure 32: Europe Semi-active WDM Volume (K), by Types 2025 & 2033

- Figure 33: Europe Semi-active WDM Revenue Share (%), by Types 2025 & 2033

- Figure 34: Europe Semi-active WDM Volume Share (%), by Types 2025 & 2033

- Figure 35: Europe Semi-active WDM Revenue (billion), by Country 2025 & 2033

- Figure 36: Europe Semi-active WDM Volume (K), by Country 2025 & 2033

- Figure 37: Europe Semi-active WDM Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Semi-active WDM Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Semi-active WDM Revenue (billion), by Application 2025 & 2033

- Figure 40: Middle East & Africa Semi-active WDM Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Semi-active WDM Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Semi-active WDM Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Semi-active WDM Revenue (billion), by Types 2025 & 2033

- Figure 44: Middle East & Africa Semi-active WDM Volume (K), by Types 2025 & 2033

- Figure 45: Middle East & Africa Semi-active WDM Revenue Share (%), by Types 2025 & 2033

- Figure 46: Middle East & Africa Semi-active WDM Volume Share (%), by Types 2025 & 2033

- Figure 47: Middle East & Africa Semi-active WDM Revenue (billion), by Country 2025 & 2033

- Figure 48: Middle East & Africa Semi-active WDM Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Semi-active WDM Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Semi-active WDM Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Semi-active WDM Revenue (billion), by Application 2025 & 2033

- Figure 52: Asia Pacific Semi-active WDM Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Semi-active WDM Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Semi-active WDM Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Semi-active WDM Revenue (billion), by Types 2025 & 2033

- Figure 56: Asia Pacific Semi-active WDM Volume (K), by Types 2025 & 2033

- Figure 57: Asia Pacific Semi-active WDM Revenue Share (%), by Types 2025 & 2033

- Figure 58: Asia Pacific Semi-active WDM Volume Share (%), by Types 2025 & 2033

- Figure 59: Asia Pacific Semi-active WDM Revenue (billion), by Country 2025 & 2033

- Figure 60: Asia Pacific Semi-active WDM Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Semi-active WDM Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Semi-active WDM Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Semi-active WDM Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Semi-active WDM Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Semi-active WDM Revenue billion Forecast, by Types 2020 & 2033

- Table 4: Global Semi-active WDM Volume K Forecast, by Types 2020 & 2033

- Table 5: Global Semi-active WDM Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Semi-active WDM Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Semi-active WDM Revenue billion Forecast, by Application 2020 & 2033

- Table 8: Global Semi-active WDM Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Semi-active WDM Revenue billion Forecast, by Types 2020 & 2033

- Table 10: Global Semi-active WDM Volume K Forecast, by Types 2020 & 2033

- Table 11: Global Semi-active WDM Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Global Semi-active WDM Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Semi-active WDM Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United States Semi-active WDM Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Semi-active WDM Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada Semi-active WDM Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Semi-active WDM Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Mexico Semi-active WDM Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Semi-active WDM Revenue billion Forecast, by Application 2020 & 2033

- Table 20: Global Semi-active WDM Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Semi-active WDM Revenue billion Forecast, by Types 2020 & 2033

- Table 22: Global Semi-active WDM Volume K Forecast, by Types 2020 & 2033

- Table 23: Global Semi-active WDM Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Global Semi-active WDM Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Semi-active WDM Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Brazil Semi-active WDM Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Semi-active WDM Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Argentina Semi-active WDM Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Semi-active WDM Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Semi-active WDM Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Semi-active WDM Revenue billion Forecast, by Application 2020 & 2033

- Table 32: Global Semi-active WDM Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Semi-active WDM Revenue billion Forecast, by Types 2020 & 2033

- Table 34: Global Semi-active WDM Volume K Forecast, by Types 2020 & 2033

- Table 35: Global Semi-active WDM Revenue billion Forecast, by Country 2020 & 2033

- Table 36: Global Semi-active WDM Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Semi-active WDM Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Semi-active WDM Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Semi-active WDM Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Germany Semi-active WDM Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Semi-active WDM Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: France Semi-active WDM Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Semi-active WDM Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: Italy Semi-active WDM Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Semi-active WDM Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Spain Semi-active WDM Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Semi-active WDM Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: Russia Semi-active WDM Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Semi-active WDM Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: Benelux Semi-active WDM Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Semi-active WDM Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Nordics Semi-active WDM Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Semi-active WDM Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Semi-active WDM Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Semi-active WDM Revenue billion Forecast, by Application 2020 & 2033

- Table 56: Global Semi-active WDM Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Semi-active WDM Revenue billion Forecast, by Types 2020 & 2033

- Table 58: Global Semi-active WDM Volume K Forecast, by Types 2020 & 2033

- Table 59: Global Semi-active WDM Revenue billion Forecast, by Country 2020 & 2033

- Table 60: Global Semi-active WDM Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Semi-active WDM Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: Turkey Semi-active WDM Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Semi-active WDM Revenue (billion) Forecast, by Application 2020 & 2033

- Table 64: Israel Semi-active WDM Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Semi-active WDM Revenue (billion) Forecast, by Application 2020 & 2033

- Table 66: GCC Semi-active WDM Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Semi-active WDM Revenue (billion) Forecast, by Application 2020 & 2033

- Table 68: North Africa Semi-active WDM Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Semi-active WDM Revenue (billion) Forecast, by Application 2020 & 2033

- Table 70: South Africa Semi-active WDM Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Semi-active WDM Revenue (billion) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Semi-active WDM Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Semi-active WDM Revenue billion Forecast, by Application 2020 & 2033

- Table 74: Global Semi-active WDM Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Semi-active WDM Revenue billion Forecast, by Types 2020 & 2033

- Table 76: Global Semi-active WDM Volume K Forecast, by Types 2020 & 2033

- Table 77: Global Semi-active WDM Revenue billion Forecast, by Country 2020 & 2033

- Table 78: Global Semi-active WDM Volume K Forecast, by Country 2020 & 2033

- Table 79: China Semi-active WDM Revenue (billion) Forecast, by Application 2020 & 2033

- Table 80: China Semi-active WDM Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Semi-active WDM Revenue (billion) Forecast, by Application 2020 & 2033

- Table 82: India Semi-active WDM Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Semi-active WDM Revenue (billion) Forecast, by Application 2020 & 2033

- Table 84: Japan Semi-active WDM Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Semi-active WDM Revenue (billion) Forecast, by Application 2020 & 2033

- Table 86: South Korea Semi-active WDM Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Semi-active WDM Revenue (billion) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Semi-active WDM Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Semi-active WDM Revenue (billion) Forecast, by Application 2020 & 2033

- Table 90: Oceania Semi-active WDM Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Semi-active WDM Revenue (billion) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Semi-active WDM Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Semi-active WDM?

The projected CAGR is approximately 16.69%.

2. Which companies are prominent players in the Semi-active WDM?

Key companies in the market include Infinera, FIBERSTAMP, Huawei, Guangzhou Sintai Communication, 3C-Link Technology, WDMLight, Shenzhen HTFuture, Shenzhen HUANET Technology, Guilin GLSUN Science and Tech Group, SONT Technologies, Sino-Telecom Technology, Triple-Stone, Genew Technologies, GIGALIGHT, FHTEK, ATOP Corporation, Fiberhome, Hymo Connect.

3. What are the main segments of the Semi-active WDM?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 5.92 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Semi-active WDM," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Semi-active WDM report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Semi-active WDM?

To stay informed about further developments, trends, and reports in the Semi-active WDM, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence