Key Insights

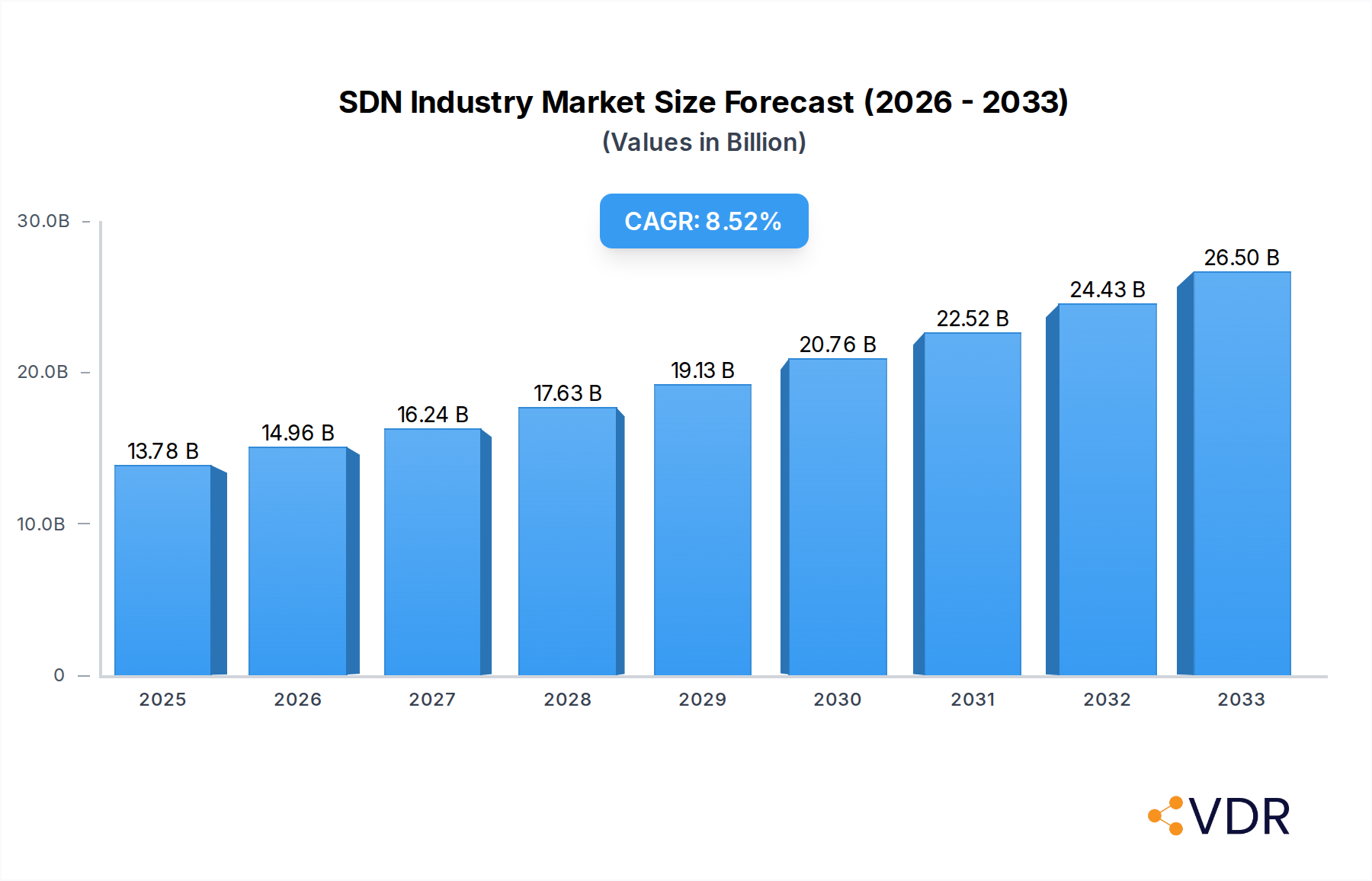

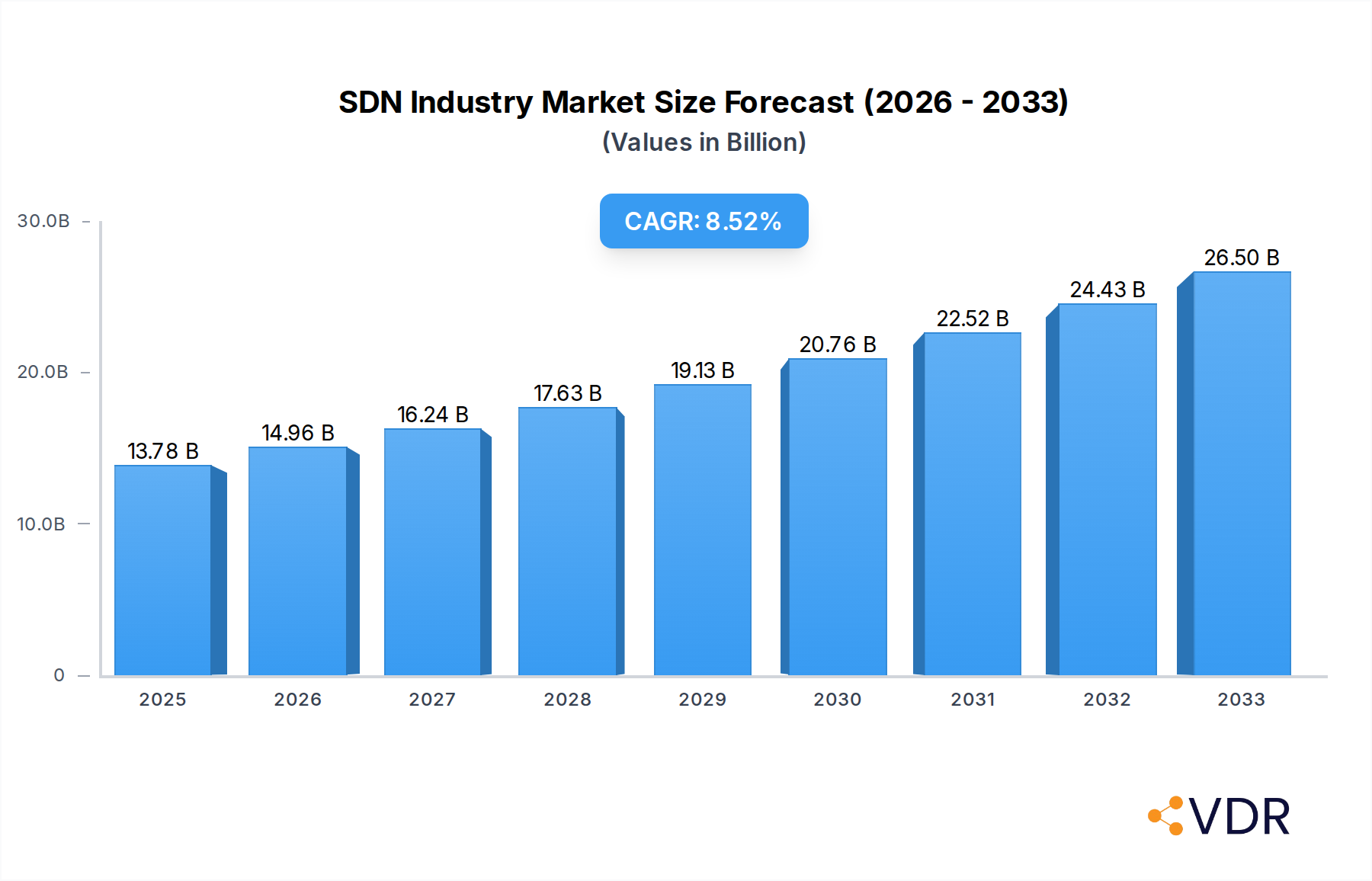

The Software-Defined Networking (SDN) industry is poised for significant expansion, driven by an escalating demand for agile, programmable, and efficient network infrastructure across diverse sectors. In 2025, the market is valued at an impressive $13.78 billion, with a robust projected Compound Annual Growth Rate (CAGR) of 8.54%. This substantial growth is fueled by key drivers such as the increasing adoption of cloud computing, the proliferation of IoT devices, and the continuous need for network virtualization to enhance scalability and reduce operational costs. Industries like BFSI, Healthcare, and Telecom are at the forefront of this adoption, leveraging SDN for improved network performance, enhanced security, and streamlined management. The ability of SDN to decouple network control from forwarding functions empowers organizations to automate network provisioning, optimize resource allocation, and respond dynamically to changing business requirements. This shift towards more intelligent and flexible networks is a critical enabler for digital transformation initiatives globally.

SDN Industry Market Size (In Billion)

The market's trajectory is also shaped by emerging trends and existing restraints. While the growth potential is high, factors such as the complexity of initial SDN deployment and integration with legacy systems can present challenges for some organizations. However, advancements in SDN technologies, including open networking solutions and the growing ecosystem of SDN controllers and applications, are progressively mitigating these barriers. The competitive landscape features established players like Cisco Systems, VMware, and HPE, alongside innovative companies such as Versa Networks and Fortinet, all vying to capture market share by offering advanced SDN solutions. The ongoing development and wider acceptance of SDN are critical for enterprises seeking to build future-proof, cost-effective, and high-performance networks capable of supporting the ever-increasing demands of the digital economy.

SDN Industry Company Market Share

Comprehensive SDN Industry Market Analysis: 2019-2033

Unlock the future of network infrastructure with our in-depth Software-Defined Networking (SDN) industry report. This definitive analysis delves into the intricate dynamics, growth trajectories, and competitive landscape of the global SDN market, providing actionable insights for stakeholders across all levels. With the market projected to reach a substantial $XX billion by 2025, and a robust CAGR of XX% expected from 2025-2033, this report is your indispensable guide to capitalizing on this rapidly evolving sector. We meticulously examine parent and child markets, offering a granular understanding of market segmentation, key influencers, and future expansion avenues.

SDN Industry Market Dynamics & Structure

The SDN industry exhibits a dynamic market concentration influenced by continuous technological innovation and evolving regulatory frameworks. Key players are actively engaged in product development and strategic alliances to capture market share. The market is characterized by moderate concentration, with a few dominant vendors alongside a growing number of specialized solution providers. Technological innovation, particularly in areas like network automation, AI-driven insights, and enhanced security protocols, serves as a primary driver. Regulatory landscapes, while generally supportive of digital transformation, can introduce complexities in cross-border implementations. Competitive product substitutes, while present in traditional networking solutions, are increasingly being supplanted by the agility and cost-effectiveness offered by SDN. End-user demographics are diversifying, with significant adoption across various sectors. Mergers and acquisitions (M&A) trends are on the rise as larger entities seek to consolidate their offerings and acquire innovative technologies.

- Market Concentration: Moderate, with key players like Cisco Systems, VMware, and Juniper Networks holding significant positions, alongside emerging specialists.

- Technological Innovation Drivers: Network automation, AI/ML integration for traffic optimization, enhanced cybersecurity features, and 5G network slicing capabilities.

- Regulatory Frameworks: Evolving global regulations impacting data privacy, network security, and cross-border data flows.

- Competitive Product Substitutes: Primarily traditional networking hardware and software, facing increasing pressure from SDN's flexibility and programmability.

- End-User Demographics: Broad adoption across BFSI, Healthcare, Retail, Telecom, Cloud Service Providers, Manufacturing, and Education.

- M&A Trends: Increasing activity as companies seek to expand their SDN portfolios and gain a competitive edge.

SDN Industry Growth Trends & Insights

The Software-Defined Networking (SDN) industry is experiencing exponential growth, fueled by an increasing demand for agile, programmable, and cost-efficient network infrastructures. The market size, estimated at $XX billion in 2025, is poised for substantial expansion throughout the forecast period (2025-2033), driven by a projected Compound Annual Growth Rate (CAGR) of XX%. This growth is underpinned by escalating adoption rates across diverse enterprise segments, propelled by the transformative capabilities of SDN in optimizing network performance, enhancing security, and facilitating the rapid deployment of new services.

Technological disruptions are at the forefront of this expansion. The evolution from traditional hardware-centric networks to software-defined architectures offers unparalleled flexibility and centralized control, allowing organizations to dynamically manage network resources, adapt to changing traffic demands, and streamline operational complexities. This shift is critical for enterprises navigating the demands of cloud computing, big data analytics, the Internet of Things (IoT), and the burgeoning requirements of 5G networks.

Consumer behavior shifts are also playing a pivotal role. Businesses are increasingly prioritizing digital transformation initiatives, seeking solutions that can support enhanced user experiences, seamless connectivity, and the rapid innovation cycles demanded by today's digital economy. SDN’s ability to provide on-demand network services, automate provisioning, and offer granular visibility into network performance directly addresses these evolving needs. The market penetration of SDN solutions is steadily increasing, moving beyond early adopters in the telecommunications sector to encompass a wider array of industries seeking to leverage its advantages for competitive differentiation and operational efficiency. The integration of Artificial Intelligence (AI) and Machine Learning (ML) into SDN platforms further enhances their capabilities, enabling predictive analytics, automated fault detection, and intelligent traffic management, thereby accelerating adoption and expanding the market's overall value.

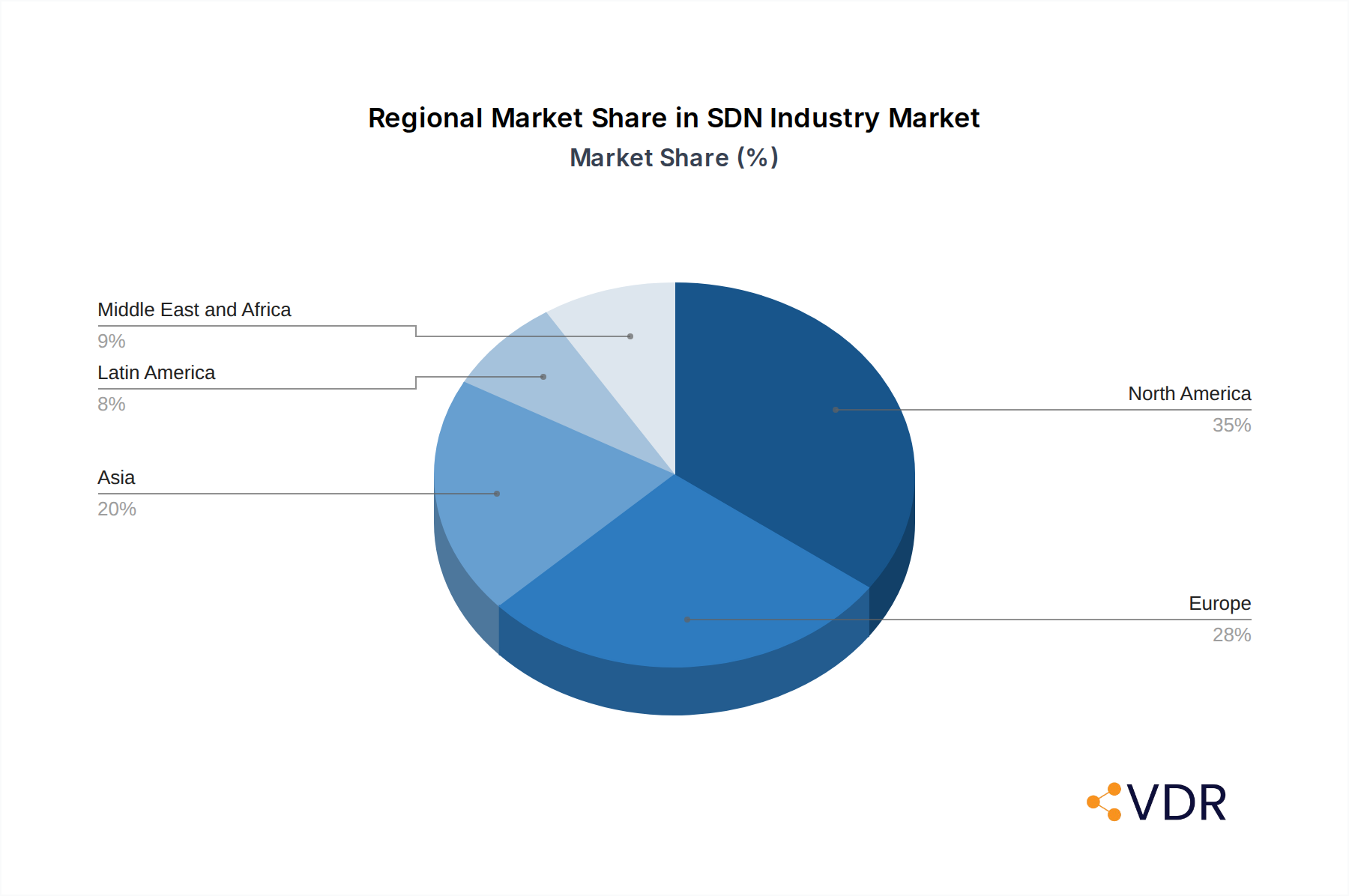

Dominant Regions, Countries, or Segments in SDN Industry

The global SDN market is experiencing significant growth, with North America currently leading as the dominant region. This leadership is attributed to a confluence of factors including robust technological infrastructure, high adoption rates of cloud computing and advanced networking technologies, and a strong presence of major technology companies driving innovation. The United States, in particular, stands out as a key country within this region, benefiting from substantial investments in research and development, a mature enterprise landscape, and favorable government initiatives promoting digital transformation.

Among the various organization sizes, Large Enterprises are the primary drivers of SDN adoption. Their complex network requirements, extensive IT budgets, and the critical need for scalable, secure, and agile infrastructure make them ideal candidates for SDN solutions. These organizations leverage SDN to optimize data center operations, improve application performance, and enhance their overall IT agility.

In terms of end-user segments, Telecom and Cloud Service Providers consistently remain at the forefront of SDN adoption. Their inherent need for highly dynamic, programmable, and scalable networks to manage massive traffic volumes and deliver diverse services efficiently positions them as early and continuous adopters. The development of 5G networks, with its stringent requirements for network slicing and ultra-low latency, further amplifies the importance of SDN for this sector.

- Dominant Region: North America, driven by technological advancement and enterprise adoption.

- Key Country: United States, leading in R&D and digital transformation initiatives.

- Dominant Organization Size: Large Enterprises, owing to their complex and evolving network needs.

- Key End-User Segment: Telecom and Cloud Service Providers, critical for 5G deployment and service delivery.

- Market Share Potential: Significant growth expected in BFSI and Healthcare as they increasingly adopt digital technologies.

- Growth Drivers: Government policies supporting digital infrastructure, increased focus on network automation, and the proliferation of IoT devices.

- Infrastructure Investment: Continuous upgrades to telecommunications and enterprise networks are accelerating SDN adoption.

SDN Industry Product Landscape

The SDN industry's product landscape is characterized by a rapid evolution of innovative solutions designed to enhance network agility, automation, and security. Key product categories include Software-Defined WAN (SD-WAN), Network Function Virtualization (NFV) infrastructure, and centralized SDN controllers. SD-WAN solutions, for instance, are revolutionizing enterprise connectivity by offering intelligent path selection, simplified management, and cost savings over traditional WAN architectures. NFV enables the deployment of network functions as software on commodity hardware, providing unprecedented flexibility and scalability. Centralized controllers serve as the brain of the SDN architecture, enabling programmatic control and orchestration of the entire network. Performance metrics such as latency reduction, throughput enhancement, and improved network uptime are key differentiators.

Key Drivers, Barriers & Challenges in SDN Industry

Key Drivers:

The SDN industry is propelled by several potent forces. Technologically, the demand for greater network agility, automation, and programmability is paramount. Economically, the pursuit of reduced operational expenditure (OpEx) and capital expenditure (CapEx) through resource optimization and hardware decoupling is a significant catalyst. Policy-driven factors, such as government initiatives promoting digital transformation and the deployment of advanced communication infrastructure like 5G, further accelerate adoption. The increasing adoption of cloud computing and the proliferation of IoT devices also necessitate more flexible and scalable network solutions, driving SDN growth.

Barriers & Challenges:

Despite its promising trajectory, the SDN industry faces several challenges. Integration complexity with legacy network infrastructure remains a significant hurdle for many organizations. Security concerns, particularly regarding the centralized control plane, require robust and sophisticated security measures. A shortage of skilled professionals with expertise in SDN technologies can hinder effective deployment and management. Furthermore, the initial investment required for transitioning to SDN, despite long-term cost savings, can be a barrier for some businesses. Regulatory compliance and the need for interoperability standards across different vendor solutions also present ongoing challenges.

Emerging Opportunities in SDN Industry

Emerging opportunities in the SDN industry are abundant and poised for significant expansion. The rapid growth of edge computing presents a substantial avenue for SDN solutions, enabling distributed network intelligence and localized data processing closer to the source. The increasing demand for highly secure and segmented networks in sectors like healthcare and finance opens doors for advanced SDN security features and micro-segmentation capabilities. Furthermore, the burgeoning IoT market necessitates scalable and manageable network infrastructures, a domain where SDN excels. The development of AI-driven network analytics and autonomous networking solutions represents another significant growth frontier, promising to further automate network operations and enhance performance.

Growth Accelerators in the SDN Industry Industry

Several key catalysts are accelerating long-term growth in the SDN industry. Technological breakthroughs, particularly in areas like AI-powered network automation and advanced orchestration platforms, are continuously enhancing the capabilities and appeal of SDN. Strategic partnerships between hardware vendors, software providers, and system integrators are crucial for developing comprehensive and interoperable SDN ecosystems. Market expansion strategies, including the penetration of SDN into previously underserved verticals and geographical regions, are also significant growth accelerators. The increasing recognition of SDN's role in enabling digital transformation initiatives and supporting emerging technologies like 5G and edge computing further solidifies its growth trajectory.

Key Players Shaping the SDN Industry Market

- Versa Networks

- HPE

- Dell EMC

- Fortinet

- VMware

- Juniper Networks

- Barracuda Networks

- Arista Networks

- Cisco Systems

- Huawei Technologies

Notable Milestones in SDN Industry Sector

- February 2023: BICS, an international communications platform company, intensified its network with a new SDN controller from Nokia. This development enhances traffic routing automation and performance, laying groundwork for 5G network slicing and optimizing flow and capacity management.

- July 2023: ActivePort Group launched its Global Edge Network-as-a-Service (NaaS) platform. This self-service, fully automated portal aims to revolutionize how businesses build, design, and manage their data networks.

In-Depth SDN Industry Market Outlook

The future outlook for the SDN industry is exceptionally promising, characterized by sustained growth and innovation. The continuous evolution of cloud-native architectures, the widespread adoption of edge computing, and the persistent demand for enhanced cybersecurity are key factors driving this positive trajectory. Strategic collaborations and the development of more intelligent, AI-driven SDN solutions will further solidify market dominance. As organizations increasingly prioritize digital transformation and seek to leverage the agility and efficiency offered by software-defined infrastructures, the market for SDN technologies is set to expand significantly. This presents substantial opportunities for stakeholders to capitalize on the ongoing network revolution.

SDN Industry Segmentation

-

1. Organization size

- 1.1. SMEs

- 1.2. Large Enterprises

-

2. End User

- 2.1. BFSI

- 2.2. Healthcare

- 2.3. Retail

- 2.4. Telecom and Cloud Service Providers

- 2.5. Manufacturing

- 2.6. Education

- 2.7. Other End Users

SDN Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia

- 4. Latin America

- 5. Middle East and Africa

SDN Industry Regional Market Share

Geographic Coverage of SDN Industry

SDN Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 17.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Organization size

- 5.1.1. SMEs

- 5.1.2. Large Enterprises

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. BFSI

- 5.2.2. Healthcare

- 5.2.3. Retail

- 5.2.4. Telecom and Cloud Service Providers

- 5.2.5. Manufacturing

- 5.2.6. Education

- 5.2.7. Other End Users

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia

- 5.3.4. Latin America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Organization size

- 6. Global SDN Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Organization size

- 6.1.1. SMEs

- 6.1.2. Large Enterprises

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. BFSI

- 6.2.2. Healthcare

- 6.2.3. Retail

- 6.2.4. Telecom and Cloud Service Providers

- 6.2.5. Manufacturing

- 6.2.6. Education

- 6.2.7. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Organization size

- 7. North America SDN Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Organization size

- 7.1.1. SMEs

- 7.1.2. Large Enterprises

- 7.2. Market Analysis, Insights and Forecast - by End User

- 7.2.1. BFSI

- 7.2.2. Healthcare

- 7.2.3. Retail

- 7.2.4. Telecom and Cloud Service Providers

- 7.2.5. Manufacturing

- 7.2.6. Education

- 7.2.7. Other End Users

- 7.1. Market Analysis, Insights and Forecast - by Organization size

- 8. Europe SDN Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Organization size

- 8.1.1. SMEs

- 8.1.2. Large Enterprises

- 8.2. Market Analysis, Insights and Forecast - by End User

- 8.2.1. BFSI

- 8.2.2. Healthcare

- 8.2.3. Retail

- 8.2.4. Telecom and Cloud Service Providers

- 8.2.5. Manufacturing

- 8.2.6. Education

- 8.2.7. Other End Users

- 8.1. Market Analysis, Insights and Forecast - by Organization size

- 9. Asia SDN Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Organization size

- 9.1.1. SMEs

- 9.1.2. Large Enterprises

- 9.2. Market Analysis, Insights and Forecast - by End User

- 9.2.1. BFSI

- 9.2.2. Healthcare

- 9.2.3. Retail

- 9.2.4. Telecom and Cloud Service Providers

- 9.2.5. Manufacturing

- 9.2.6. Education

- 9.2.7. Other End Users

- 9.1. Market Analysis, Insights and Forecast - by Organization size

- 10. Latin America SDN Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Organization size

- 10.1.1. SMEs

- 10.1.2. Large Enterprises

- 10.2. Market Analysis, Insights and Forecast - by End User

- 10.2.1. BFSI

- 10.2.2. Healthcare

- 10.2.3. Retail

- 10.2.4. Telecom and Cloud Service Providers

- 10.2.5. Manufacturing

- 10.2.6. Education

- 10.2.7. Other End Users

- 10.1. Market Analysis, Insights and Forecast - by Organization size

- 11. Middle East and Africa SDN Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Organization size

- 11.1.1. SMEs

- 11.1.2. Large Enterprises

- 11.2. Market Analysis, Insights and Forecast - by End User

- 11.2.1. BFSI

- 11.2.2. Healthcare

- 11.2.3. Retail

- 11.2.4. Telecom and Cloud Service Providers

- 11.2.5. Manufacturing

- 11.2.6. Education

- 11.2.7. Other End Users

- 11.1. Market Analysis, Insights and Forecast - by Organization size

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Versa Networks

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 HPE

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Dell EMC

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Fortinet

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 VMware

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Juniper Networks

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Barracuda Networks

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Arista Networks

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Cisco Systems

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Huawei Technologies

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Versa Networks

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global SDN Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America SDN Industry Revenue (billion), by Organization size 2025 & 2033

- Figure 3: North America SDN Industry Revenue Share (%), by Organization size 2025 & 2033

- Figure 4: North America SDN Industry Revenue (billion), by End User 2025 & 2033

- Figure 5: North America SDN Industry Revenue Share (%), by End User 2025 & 2033

- Figure 6: North America SDN Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America SDN Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe SDN Industry Revenue (billion), by Organization size 2025 & 2033

- Figure 9: Europe SDN Industry Revenue Share (%), by Organization size 2025 & 2033

- Figure 10: Europe SDN Industry Revenue (billion), by End User 2025 & 2033

- Figure 11: Europe SDN Industry Revenue Share (%), by End User 2025 & 2033

- Figure 12: Europe SDN Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe SDN Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia SDN Industry Revenue (billion), by Organization size 2025 & 2033

- Figure 15: Asia SDN Industry Revenue Share (%), by Organization size 2025 & 2033

- Figure 16: Asia SDN Industry Revenue (billion), by End User 2025 & 2033

- Figure 17: Asia SDN Industry Revenue Share (%), by End User 2025 & 2033

- Figure 18: Asia SDN Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Asia SDN Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Latin America SDN Industry Revenue (billion), by Organization size 2025 & 2033

- Figure 21: Latin America SDN Industry Revenue Share (%), by Organization size 2025 & 2033

- Figure 22: Latin America SDN Industry Revenue (billion), by End User 2025 & 2033

- Figure 23: Latin America SDN Industry Revenue Share (%), by End User 2025 & 2033

- Figure 24: Latin America SDN Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Latin America SDN Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa SDN Industry Revenue (billion), by Organization size 2025 & 2033

- Figure 27: Middle East and Africa SDN Industry Revenue Share (%), by Organization size 2025 & 2033

- Figure 28: Middle East and Africa SDN Industry Revenue (billion), by End User 2025 & 2033

- Figure 29: Middle East and Africa SDN Industry Revenue Share (%), by End User 2025 & 2033

- Figure 30: Middle East and Africa SDN Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Middle East and Africa SDN Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global SDN Industry Revenue billion Forecast, by Organization size 2020 & 2033

- Table 2: Global SDN Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 3: Global SDN Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global SDN Industry Revenue billion Forecast, by Organization size 2020 & 2033

- Table 5: Global SDN Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 6: Global SDN Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Global SDN Industry Revenue billion Forecast, by Organization size 2020 & 2033

- Table 8: Global SDN Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 9: Global SDN Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Global SDN Industry Revenue billion Forecast, by Organization size 2020 & 2033

- Table 11: Global SDN Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 12: Global SDN Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Global SDN Industry Revenue billion Forecast, by Organization size 2020 & 2033

- Table 14: Global SDN Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 15: Global SDN Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Global SDN Industry Revenue billion Forecast, by Organization size 2020 & 2033

- Table 17: Global SDN Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 18: Global SDN Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the SDN Industry?

The projected CAGR is approximately 17.9%.

2. Which companies are prominent players in the SDN Industry?

Key companies in the market include Versa Networks, HPE, Dell EMC, Fortinet, VMware, Juniper Networks, Barracuda Networks, Arista Networks, Cisco Systems, Huawei Technologies.

3. What are the main segments of the SDN Industry?

The market segments include Organization size, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 34.29 billion as of 2022.

5. What are some drivers contributing to market growth?

Rising investment toward automation of network infrastructure; Increasing adoption of IoT and cloud services.

6. What are the notable trends driving market growth?

Telecom and Cloud-Based Service Provider is expected to witness a significant growth.

7. Are there any restraints impacting market growth?

Security and Privacy Concerns.

8. Can you provide examples of recent developments in the market?

February 2023: The international communications platform company BICS has intensified its network with a new SDN controller established by Nokia. The new intelligence module primarily automates optimal traffic routing on the network, developing the overall performance for users while laying the groundwork for 5G network slicing. The new SDN controller would also manage flow and capacity routing throughout its global network.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "SDN Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the SDN Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the SDN Industry?

To stay informed about further developments, trends, and reports in the SDN Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence